July 10, 2026

The global rare earth supply chain faces an infrastructure paradox that has persisted for decades. Mining operations expand across continents while processing capabilities remain concentrated in a single geographic region, creating bottlenecks that constrain both supply security and economic development. Australia's decision to construct dedicated processing infrastructure for clay-hosted rare earth deposits represents a fundamental pivot in critical minerals that addresses these strategic vulnerabilities.

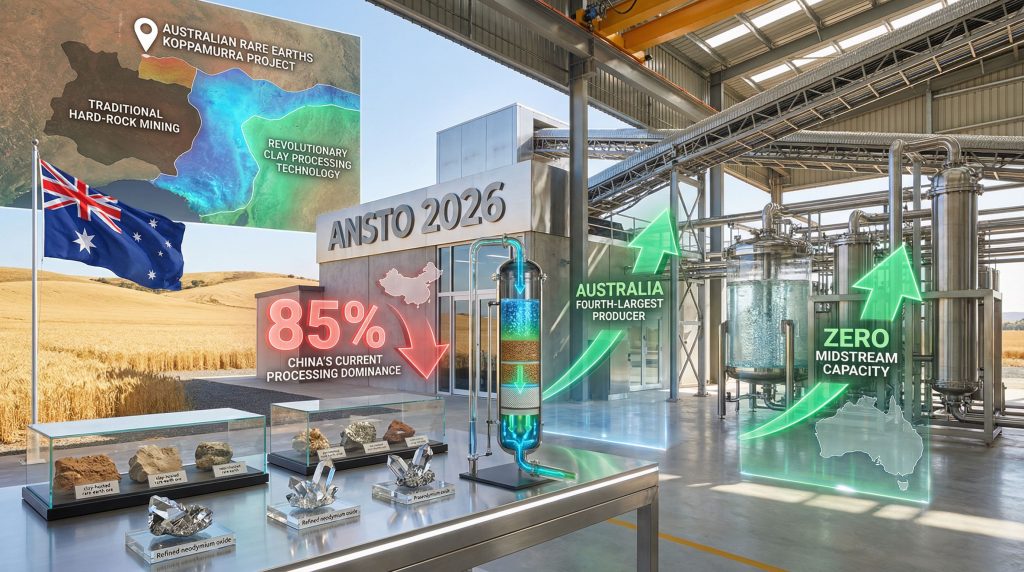

This strategic pivot addresses more than simple processing capacity gaps. It targets the specific technical requirements of ion-adsorption clay deposits, which demand different hydrometallurgical approaches than traditional hard-rock mining operations. The Australia clay rare earth processing plant, operated by the Australian Nuclear Science and Technology Organisation and scheduled for commissioning in 2026, will serve as the testing ground for whether Western nations can successfully compete with established Asian processing networks.

What Makes Clay-Based Rare Earth Processing Different from Traditional Hard-Rock Mining?

Ion-Adsorption Clay Deposits vs. Hard-Rock Mineralisation

Clay-hosted rare earth deposits fundamentally differ from conventional hard-rock mining in their geological formation and extraction requirements. Ion-adsorption clay forms through weathering processes where rare earth elements become electrostatically bound to clay mineral surfaces rather than locked within crystal lattice structures.

This physical arrangement creates significant processing advantages:

- Recovery efficiency: Clay deposits achieve 70-90% leaching efficiency compared to 50-75% for hard-rock flotation methods

- Grade advantages: Ion-adsorption clays operate with 100-2,000 parts per million total rare earth oxides, while hard-rock deposits require processing ore with 0.1-0.5% rare earth content

- Processing duration: Clay hydrometallurgy requires 3-8 weeks from leaching to oxide production, versus 6-18 months for hard-rock processing chains

Environmental footprint analysis reveals additional distinctions between processing methodologies. Clay processing consumes 500-800 litres of water per kilogram of rare earth oxide produced, significantly below the 2,000-4,000 litres required for hard-rock hydrometallurgical routes. Furthermore, tailings generation follows similar patterns, with clay processing producing 1-2 tonnes of waste per tonne of final product compared to 8-15 tonnes for hard-rock operations.

Hydrometallurgical Processing Requirements

The technical specifications for the Australia clay rare earth processing plant operations centre on acid leaching circuits designed specifically for ion-adsorption materials. Unlike hard-rock processing that requires crushing, grinding, and flotation concentration, clay processing begins with relatively simple acid percolation through prepared ore.

The hydrometallurgical sequence involves five distinct stages:

- Leaching: Ammonium sulfate or dilute hydrochloric acid displaces rare earth ions from clay surfaces at ambient temperature

- Solid-liquid separation: Filtration removes clay residues while preserving rare earth-bearing solutions

- Impurity removal: Selective precipitation eliminates iron, aluminium, and radioactive elements when present

- Rare earth concentration: Sequential precipitation with oxalic acid produces individual rare earth compounds

- Calcination: High-temperature treatment at 800-1,000°C converts precipitates to commercial-grade oxides

Quality control standards for magnet-grade rare earth oxides demand 99.5-99.9% purity levels, achievable through clay processing without the multi-stage solvent extraction systems required for hard-rock concentrates. This technical simplicity reduces both capital expenditure and operational complexity for new processing facilities.

When big ASX news breaks, our subscribers know first

Why is Australia Building National Processing Infrastructure Now?

Strategic Supply Chain Vulnerabilities

China maintains approximately 85% of global rare earth processing capacity, creating systemic vulnerabilities for consuming nations dependent on these materials. This processing concentration represents over 400,000 tonnes of annual capacity from a global total near 470,000 tonnes, according to United States Geological Survey data.

Australia's position exemplifies the resource-processing disconnect affecting multiple mining nations. As the world's fourth-largest rare earth producer with approximately 19,000 tonnes of rare earth oxide equivalent production in 2023, Australia ships 100% of its concentrate offshore for midstream processing. This arrangement captures only 15-25% of final processed oxide value, representing annual revenue leakage of $570-950 million based on current market pricing.

The economic implications extend beyond immediate revenue loss:

- Value capture: Processed oxides command $40-60 per kilogram versus $8-15 for raw concentrates

- Supply security: Offshore processing creates dependency on foreign infrastructure and regulatory environments

- Industrial development: Lack of domestic processing constrains downstream manufacturing capabilities

Historical precedent demonstrates the risks of processing concentration. China's 2010 rare earth export quota reductions caused 300% price increases in neodymium-praseodymium oxides within six months, highlighting single-point failure vulnerabilities in concentrated supply chains.

Government Investment Rationale

The Australian Nuclear Science and Technology Organisation's role as facility operator reflects strategic considerations beyond commercial viability. ANSTO's existing expertise in hydrometallurgical processes, developed through nuclear fuel cycle operations and medical isotope production, provides technical competency for rare earth separation chemistry.

Government infrastructure investment addresses market failures preventing private sector development. The economics of shared processing infrastructure create a coordination problem where explorers cannot commit to dedicated facilities without proven resources, while processors cannot justify investment without guaranteed feedstock supply. Consequently, public investment breaks this deadlock by providing accessible infrastructure enabling project development.

Timeline pressures intensify the strategic imperative for processing capacity expansion. Global electric vehicle sales projections indicate growth from 14 million units in 2023 to 40-50 million annually by 2030. Each electric motor requires 300-600 grams of neodymium-praseodymium permanent magnet material, translating to 12,000-30,000 tonnes of additional rare earth demand by decade's end. This growth trajectory aligns with broader energy transition security initiatives worldwide.

Similar demand growth characterises wind energy development, where global installed capacity expansion from 1,100 gigawatts to over 2,000 gigawatts by 2030 requires 2,000-3,000 additional tonnes of permanent magnet materials annually.

Which Companies Will Benefit from Australia's First Common-Use Processing Facility?

| Facility Aspect | Details |

|---|---|

| Operator | Australian Nuclear Science and Technology Organisation (ANSTO) |

| Opening Date | 2026 |

| Facility Type | Common-use, taxpayer-financed |

| Primary User | Australian Rare Earths (Koppamurra project) |

| Processing Focus | Clay-hosted rare earth deposits |

Australian Rare Earths' Koppamurra Project Profile

Australian Rare Earths' Koppamurra project represents Australia's first large-scale ion-adsorption clay rare earth development proposal. Located in South Australia's Wrattonbully region, the project received scoping study approval in December 2025, marking a significant regulatory milestone despite lacking final mining licences.

The project's technical characteristics align with ANSTO's processing facility capabilities. Moreover, Koppamurra's clay-hosted mineralisation requires hydrometallurgical processing rather than conventional hard-rock concentration methods. This technical fit positions Australian Rare Earths as the logical inaugural user for validating facility operations and establishing processing protocols.

Resource estimates and production capacity projections remain subject to detailed feasibility studies following scoping study completion. The company's development timeline depends heavily on ANSTO facility commissioning, community consultation outcomes, and final environmental approvals for mining operations.

Open Infrastructure Model Benefits

The common-use facility model provides cost advantages unavailable through dedicated processing infrastructure. Junior exploration companies can access hydrometallurgical testwork capabilities without constructing bespoke facilities costing $20-50 million for clay processing or $500 million to $2 billion for hard-rock operations.

Standardised testing protocols across multiple projects enable comparative analysis and benchmarking between different clay deposit sources. This systematic approach reduces technical risk for both explorers and potential investors by establishing consistent quality control and processing parameters.

Risk reduction through shared infrastructure extends beyond capital cost savings:

- Technical validation: Multiple projects using identical equipment provide operational data for process optimisation

- Regulatory precedent: Successful facility operations establish environmental and safety compliance frameworks

- Market development: Consistent processing creates reliable supply for downstream purchasers

The infrastructure sharing model mirrors successful precedents in other mining sectors where common-use facilities enable industry development despite individual project constraints. For instance, similar approaches have been implemented in the European CRM facility development programmes.

What Are the Technical Capabilities of Australia's New Processing Plant?

Processing Technology Specifications

ANSTO's facility design incorporates modular hydrometallurgical equipment optimised for ion-adsorption clay processing. Initial capacity targets 100-500 kilograms per day for testwork phases, with pilot-scale expansion to 5-10 tonnes daily throughput capability.

The processing circuit includes specialised equipment for each separation stage:

- Acid leaching vessels: Corrosion-resistant tanks with agitation systems for ammonium sulfate or hydrochloric acid treatment

- Filtration systems: Filter presses and centrifuges for solid-liquid separation of clay residues

- Precipitation equipment: Sequential vessels for impurity removal and rare earth concentration

- Calcination furnaces: High-temperature systems operating at 800-1,000°C for oxide production

Quality assurance protocols incorporate inductively coupled plasma mass spectrometry and X-ray fluorescence analysis for real-time composition monitoring. These analytical capabilities ensure consistency with international specifications for magnet-grade rare earth oxides requiring 99.5-99.9% purity levels.

Integration with Existing Australian Operations

ANSTO's facility complements rather than competes with existing Australian rare earth processing infrastructure. Lynas Rare Earths operates the Kalgoorlie Rare Earths Processing Facility, which processes hard-rock concentrates through solvent extraction methods unsuitable for clay deposits.

Iluka Resources' planned Eneabba refinery development focuses on heavy rare earth production from monazite processing, creating a differentiated product portfolio from ANSTO's anticipated light rare earth emphasis. However, this technical specialisation enables facility coexistence rather than direct competition.

The complementary relationship extends to feedstock sources and processing methodologies. ANSTO's clay processing capabilities fill a technical gap in Australia's rare earth processing ecosystem, enabling development of ion-adsorption deposits that cannot utilise existing hard-rock infrastructure. This advancement reflects broader trends in mining industry innovation across Australia.

How Do Agricultural Concerns Impact Clay Rare Earth Development?

Landholder Resistance in South Australia

Agricultural communities in the Wrattonbully region express significant concerns about rare earth mining impacts on productive farmland. The area's reputation for premium wine grape production and livestock operations creates tension between mining development and established agricultural identity.

Farming community concerns focus on several technical and economic issues:

- Soil health impacts: Clay extraction and acid leaching effects on long-term agricultural productivity

- Water resource competition: Processing water requirements potentially affecting irrigation availability

- Land use conflict: Mining lease areas overlapping with productive agricultural zones

- Property value effects: Proximity to mining operations potentially affecting land valuations

These concerns reflect broader patterns observed in clay rare earth developments globally, where agricultural regions resist mining activities despite potential economic benefits. Social licence challenges often prove more difficult to resolve than technical or regulatory obstacles.

Regulatory Approval Process

Mining licence requirements for the Koppamurra project involve multiple regulatory stages beyond scoping study approval. Environmental assessment protocols specifically address clay deposit processing impacts, including groundwater effects, soil contamination risks, and waste management procedures.

Community consultation obligations under Australian mining law require extensive engagement with affected landholders and regional stakeholders. This process can extend project timelines significantly when social licence issues remain unresolved.

The regulatory framework must balance economic development objectives with environmental protection and community concerns. Successful project approval depends on demonstrating sustainable mining practices and addressing landholder concerns through compensation, rehabilitation guarantees, or operational modifications.

What Economic Impact Will Clay Processing Have on Australia's Resource Sector?

Value-Added Processing Economics

Processing rare earth concentrates domestically captures substantially higher economic value than raw material exports. Current pricing demonstrates the value differential, with rare earth oxides commanding $40-60 per kilogram compared to $8-15 for unprocessed concentrates.

At Australia's current production level of 19,000 tonnes rare earth oxide equivalent annually, domestic processing could generate additional revenue of $570-950 million based on value-added processing margins. This economic opportunity extends beyond immediate export revenues to include employment creation and industrial development.

Regional processing hubs generate employment across multiple skill levels:

- Technical operations: Chemical engineers, metallurgists, and process technicians

- Support services: Maintenance, logistics, and administrative personnel

- Indirect employment: Equipment suppliers, consulting services, and regional businesses

Economic modelling suggests each processing facility job creates 2-3 additional positions in supporting industries, multiplying the regional economic impact beyond direct employment. Furthermore, this aligns with Australia's critical minerals reserve development strategies.

Investment Implications for Resource Companies

Shared processing infrastructure reduces capital expenditure requirements for rare earth exploration companies, lowering the threshold for project development. Junior explorers can advance projects toward feasibility studies without committing to dedicated processing facilities costing tens or hundreds of millions of dollars.

Risk mitigation benefits extend beyond capital cost reduction. Access to proven processing infrastructure enables realistic economic modelling and reduces technical uncertainty for project financing. This improved risk profile potentially attracts broader investor participation in Australian rare earth development.

Market positioning advantages accrue to companies with access to Australian processing infrastructure. Supply chain security concerns drive consuming nations and manufacturers to diversify sourcing beyond Chinese processors, creating premium pricing opportunities for alternative suppliers.

The next major ASX story will hit our subscribers first

Which Rare Earth Elements Will Australia's Clay Processing Target?

Magnet-Grade Rare Earth Production Focus

ANSTO's facility design emphasises production of magnet-grade rare earth oxides, particularly neodymium and praseodymium compounds essential for permanent magnet manufacturing. These elements command premium pricing due to critical applications in electric motors and wind turbine generators.

Clay deposits typically contain favourable ratios of light rare earth elements compared to hard-rock sources. Ion-adsorption clays often yield 15-25% neodymium and praseodymium content within total rare earth oxide production, compared to 10-15% for conventional hard-rock concentrates.

Heavy rare earth element potential varies significantly between clay deposit sources. Some Australian clay prospects contain elevated dysprosium and terbium concentrations, which command substantially higher pricing than light rare earth elements due to supply constraints and critical applications. Research by the CSIRO's critical minerals hub demonstrates the potential for these strategic elements.

Strategic Elements for Clean Energy Transition

Electric vehicle motor requirements drive demand growth for specific rare earth combinations. Permanent magnet electric motors utilise neodymium-iron-boron alloys enhanced with praseodymium for temperature stability and dysprosium for coercivity improvement.

Wind turbine generator specifications similarly demand high-performance permanent magnets capable of reliable operation across temperature and magnetic field variations. Direct-drive wind turbines utilise 200-600 kilograms of permanent magnet material per megawatt of generating capacity.

Defence technology applications create additional strategic demand for rare earth elements, particularly for radar systems, guidance equipment, and electronic warfare systems. These applications often require higher purity specifications and supply chain security guarantees unavailable from conventional commercial sources.

How Does Australia's Processing Strategy Compare Globally?

International Clay Processing Developments

China maintains dominant market position in ion-adsorption clay processing through facilities in Ganzhou and Longnan regions processing over 60,000 tonnes annually. Chinese operations benefit from decades of experience, established supply chains, and lower operational costs ranging 20-35% below Western equivalents.

Myanmar's rare earth clay operations in Kachin and Shan states focus primarily on heavy rare earth production, achieving approximately 98% purity for dysprosium and terbium without complex solvent extraction systems. These operations demonstrate technical feasibility of simplified clay processing approaches.

Madagascar's emerging clay deposit developments represent potential competition for Australian processing initiatives. However, infrastructure limitations and political instability create supply security concerns for consuming nations seeking reliable alternative sources.

Competitive Positioning Analysis

Australia's processing strategy emphasises supply chain security and environmental standards rather than cost competition with established Asian processors. Western manufacturers increasingly prioritise supply reliability over minimum pricing, creating market opportunities for higher-cost but dependable suppliers.

Processing cost comparisons indicate Australian operations will likely exceed Chinese costs by 20-35% due to labour, environmental compliance, and capital costs. However, transportation savings, reduced political risk, and supply security premiums can offset these cost disadvantages for regional customers.

Environmental standards differentiation provides competitive advantages in markets emphasising sustainable sourcing. Australian processing facilities operate under stringent environmental regulations creating product differentiation for environmentally conscious consumers and manufacturers.

What Challenges Could Delay Australia's Clay Processing Ambitions?

Technical Processing Risks

Hydrometallurgical optimisation for different clay deposit types presents ongoing technical challenges. Each deposit source may require modified leaching parameters, impurity removal procedures, or precipitation sequences to achieve consistent product quality.

Waste management protocols for clay processing must address acid neutralisation, sulfate precipitation, and tailings storage under Australian environmental regulations. These requirements may prove more stringent than initially anticipated, potentially increasing operational costs or facility modifications.

Quality consistency challenges across different clay sources could complicate commercial operations. Variability in clay mineralogy, rare earth distribution, or impurity content may require facility modifications or processing parameter adjustments affecting operational efficiency.

Market and Regulatory Uncertainties

Global rare earth price volatility creates economic risk for processing facility operations. Price declines could render higher-cost Australian processing uneconomical compared to established Asian suppliers, potentially reducing facility utilisation rates.

Environmental permitting timeline risks could delay facility commissioning or operational expansion. Regulatory processes for new processing technologies may require additional environmental studies, community consultation periods, or permit modifications extending development schedules.

Community acceptance factors in project development areas remain significant uncertainty. Ongoing landholder resistance could prevent mining licence approvals, eliminating feedstock sources for processing facilities regardless of technical capabilities.

When Will Australia's Clay Processing Capacity Reach Commercial Scale?

Production Timeline Projections

ANSTO's 2026 facility commissioning schedule represents the initial milestone for Australian clay rare earth processing capabilities. However, commercial-scale production requires successful completion of testwork phases, process optimisation, and feedstock supply agreements.

Ramp-up period expectations for full capacity utilisation typically extend 12-24 months beyond initial commissioning. During this period, facility operators optimise processing parameters, resolve equipment issues, and establish consistent product quality meeting customer specifications.

Multi-project processing scenarios beyond Australian Rare Earths depend on successful demonstration of facility capabilities and economic viability. Additional clay projects require individual regulatory approvals, feasibility studies, and financing arrangements before committing to processing agreements.

Supply Chain Integration Milestones

Downstream processing capability development represents the next integration stage following successful oxide production. Australia currently lacks facilities for converting rare earth oxides into magnetic powders or finished permanent magnets, limiting value-added opportunities.

Export market establishment for processed oxides requires customer qualification, product certification, and supply agreement negotiations. These commercial relationships typically develop over 12-18 months involving sample testing, factory audits, and contract negotiations.

Strategic partnership opportunities with international buyers could accelerate market development through joint ventures, offtake agreements, or technology sharing arrangements. Such partnerships provide market access while reducing commercial risk for Australian processors. For instance, the Victory Metals North Stanmore project demonstrates how strategic partnerships can advance project development.

The Australian government's investment in the Australia clay rare earth processing plant infrastructure represents a calculated response to global supply chain vulnerabilities and domestic value-addition opportunities. Success depends on technical execution, community acceptance, and market development across multiple complex variables. While the 2026 facility commissioning timeline appears achievable, commercial viability and scaled operations face significant implementation challenges requiring sustained commitment and adaptive management strategies.

Disclaimer: This analysis contains forward-looking projections and market assessments based on current information and industry trends. Actual outcomes may differ significantly due to technical, regulatory, market, or geopolitical factors beyond current visibility. Readers should conduct independent research and consult qualified professionals before making investment or business decisions related to rare earth processing or mining operations.

Ready to Capitalise on Australia's Clay Rare Earth Processing Boom?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications when ASX-listed rare earth companies announce significant developments, from processing agreements to resource discoveries. Don't miss the next breakthrough in Australia's critical minerals revolution – start your 30-day free trial today to position yourself ahead of market movements in this rapidly evolving sector.