June 11, 2026

The Structural Forces Behind China's Rare Earth Processing Supremacy

Global supply chain vulnerabilities in critical minerals extend far beyond simple resource scarcity. The concentration of rare earth element processing capabilities represents a textbook case of how technical complexity, capital intensity, and strategic planning converge to create sustainable competitive advantages that transcend geological endowments.

Understanding why china controls rare earth processing requires examining the intersection of nuclear physics, industrial chemistry, and geopolitical strategy. While rare earth elements occur abundantly across multiple continents, their transformation from raw ore into commercially viable products involves mastering one of the most technically demanding separation processes in modern metallurgy.

When big ASX news breaks, our subscribers know first

What Makes Rare Earth Processing So Strategically Complex?

The fundamental challenge in rare earth processing stems from the co-occurrence principle that governs these elements in nature. Unlike traditional commodities where valuable minerals exist in relatively pure concentrations, rare earth elements appear together in the same mineral structures with nearly identical chemical properties.

The Co-Occurrence Problem

Rare earth elements do not exist as economically viable monometallic deposits. According to research published in the Handbook on the Physics and Chemistry of Rare Earths, these elements occur as mixed associations within single mineral phases, primarily bastnäsite, monazite, and xenotime. This co-occurrence creates a fundamental constraint: processing facilities must extract all 15 lanthanides plus yttium and scandium simultaneously, making selective extraction impossible.

The Oddo-Harkins rule demonstrates additional complexity in natural abundance patterns. Even-numbered atomic elements like neodymium and gadolinium occur in significantly higher concentrations than odd-numbered neighbors such as praseodymium and terbium. This nuclear stability principle means that the most strategically valuable elements for high-performance magnets, particularly dysprosium and terbium, exist in naturally scarce concentrations.

| Element Category | Natural Abundance | Separation Difficulty | Strategic Applications | Processing Concentration |

|---|---|---|---|---|

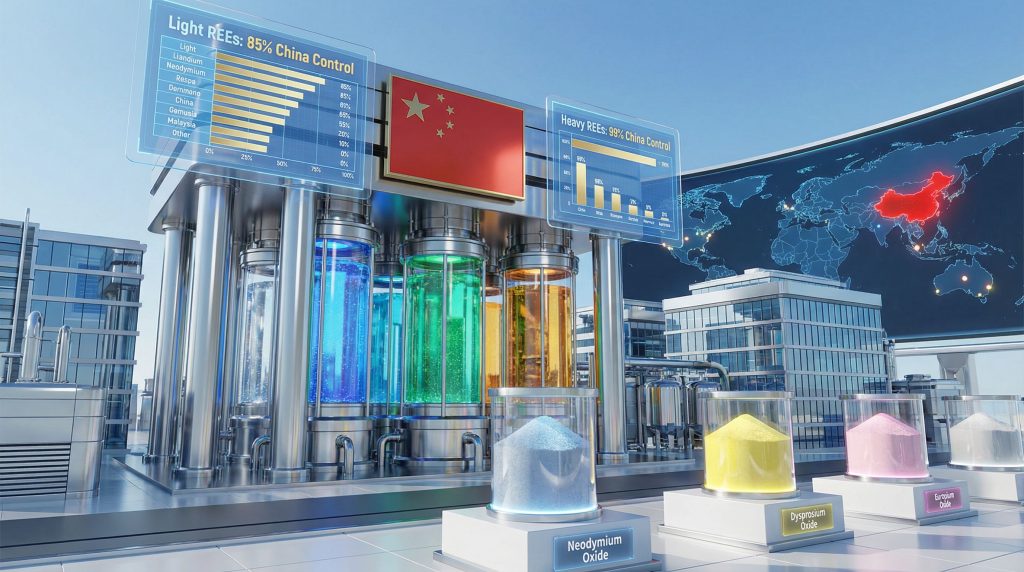

| Light REEs (La-Sm) | 98-99% of total REO | Moderate complexity | Catalysts, glass additives | 85% China-controlled |

| Heavy REEs (Eu-Lu) | <1% of total REO | Extreme complexity | Permanent magnets, defense | 95%+ China-controlled |

| Critical pairs | Variable by deposit | Maximum difficulty | Semiconductors, aerospace | 99% China-controlled |

Purity Requirements and Technical Barriers

Commercial rare earth applications demand extraordinary purity levels that magnify processing complexity. Aerospace and defense specifications require 99.9%+ purity for standard applications, while advanced uses like superconductors demand 99.99%+ purity. Contamination levels exceeding 0.1% can render entire production batches unsuitable for critical applications.

The separation process involves liquid-liquid extraction using organic compounds dissolved in kerosene, operating on selective partition coefficients where different rare earth elements display varying affinities for organic versus aqueous phases. Processing requires:

- pH control maintained within ±0.1 units using hydrochloric acid or sodium hydroxide

- Temperature regulation at 45-55°C for optimal extraction kinetics

- Multiple contact stages requiring 15-50 extraction and back-extraction cycles

- Precise organic-to-aqueous phase ratio control to optimise throughput

Radioactive Waste Management Constraints

Rare earth ore processing generates radioactive waste streams that create additional technical and regulatory barriers. Monazite processing produces thorium-232 contaminated residues with a 14-billion-year half-life, while phosphatic rare earth ores generate uranium-238 bearing waste requiring specialised long-term containment.

These radioactive byproducts demand geological stability and regulatory frameworks capable of managing 100+ year containment timescales. This constraint significantly limits viable processing locations, particularly in jurisdictions with stringent environmental standards. Furthermore, effective mining waste management solutions become crucial for sustainable operations.

How Did China Build Its Processing Ecosystem Advantage?

China's dominance in rare earth processing emerged through a deliberate, multi-decade strategy focused on controlling midstream value-added operations rather than merely exporting raw materials. This approach created sustainable competitive advantages that extend far beyond cost leadership.

Phase 1: Technology Acquisition and Foundation Building (1980s-1990s)

During this initial phase, China systematically acquired Western processing technologies through licensing agreements with companies including Rhône-Poulenc and Molycorp. Chinese enterprises recruited approximately 150+ senior scientists and engineers from Western rare earth processing facilities, transferring critical technical knowledge.

State investment during this period totalled an estimated $200-500 million RMB equivalent, funding pilot-scale facilities that provided the foundation for later industrial expansion. Processing capacity grew from approximately 5,000 tons annually in 1980 to 50,000 tons by 1995.

Phase 2: Scale Development and Industry Consolidation (2000s-2010s)

The Chinese government implemented a consolidation strategy that reduced licensed rare earth operations from 70+ independent entities to 8-10 major integrated complexes by 2010. This consolidation enabled:

- Direct coordination between ore production and processing input requirements

- Strategic inventory management reducing market volatility

- Integrated planning for downstream magnet and alloy production

- Coordinated environmental waste management across operations

Combined processing capacity expanded from 75,000 tons in 2000 to over 150,000 tons annually by 2010. Vertical integration simultaneously expanded mining operations at Bayan Obo and international deposits while developing downstream manufacturing capabilities.

Phase 3: Market Control and Export Management (2010s-Present)

By 2015, China controlled approximately 85-90% of global rare earth separation capacity. Heavy rare earth processing concentration reached 95-99%, with dysprosium and terbium effectively monopolised by Chinese processors. This dominance continues to influence critical minerals energy security considerations globally.

Export quota systems implemented between 2010-2015 restricted international access to processed materials, forcing price premiums of 200-400% above Chinese domestic pricing. This policy demonstrated China's ability to use processing control as a strategic leverage tool.

Cost Leadership Through System Integration

Chinese rare earth oxide production costs averaged $3-5 per kilogram during 2018-2020, compared to $8-15 per kilogram for equivalent Western production at comparable scales. This cost differential resulted from:

- Environmental compliance expenditures: 40-50% lower than Western equivalents

- Labour costs: 30-40% below Western facility requirements

- Scale economies: Chinese facilities operate at 10,000-50,000 ton annual capacity versus Western facilities at 1,000-5,000 ton capacity

Why Do Alternative Processing Centres Struggle to Compete?

The barriers to establishing competitive rare earth processing capabilities extend beyond simple capital requirements. Multiple structural factors create sustained advantages for existing processors while discouraging new market entrants.

Capital Intensity and Timeline Constraints

Establishing commercially viable rare earth processing requires $500 million to $2 billion in initial investment, with development timelines spanning 7-10 years before reaching operational efficiency. These capital requirements create natural barriers favouring established players with access to patient capital.

The Mountain Pass facility in California exemplifies these challenges. Despite containing approximately 15 million tons of indicated rare earth resources, environmental compliance requirements added an estimated $200-350 million in infrastructure costs compared to equivalent Chinese facilities operating under different regulatory frameworks.

Technical Knowledge and Operational Expertise

Rare earth processing involves mastering complex technical domains that require years of operational experience to optimise:

- Solvent extraction chemistry requiring precise chemical reagent management

- Quality control systems meeting aerospace-grade purity specifications

- Radioactive waste stream management with long-term containment planning

- Environmental compliance in developed regulatory frameworks

Chinese processors developed proprietary improvements to licensed separation technologies over 15-20 year periods, reducing per-unit processing costs by 15-25% through:

- Modified extraction column designs improving liquid-liquid contact efficiency

- Optimised back-extraction chemistry reducing reagent consumption by 20-30%

- Integrated thermal recovery systems capturing waste heat for process applications

- Automated control systems reducing operator error and process variance

Market Risk and Competitive Response

New processing entrants face constant threats of Chinese price competition designed to protect market share. Historical precedent demonstrates Beijing's willingness to use pricing pressure to discourage Western processing development, as occurred with Molycorp's Mountain Pass operations.

Molycorp operated Mountain Pass with 14,000 tons annual rare earth oxide capacity but exited processing in 2015 due to inability to compete with Chinese pricing. Post-closure analysis indicated Western processing facilities require government subsidies or trade protection measures to remain economically viable against Chinese competition.

How Does Technology Impact Processing Competition?

The evolution of the mining industry evolution includes significant technological advances that could reshape competitive dynamics. Modern processing facilities increasingly deploy AI-driven mining efficiency systems to optimise separation processes and reduce operational costs.

Moreover, broader economic factors such as the US–China trade impact continue to influence rare earth supply chains and processing location decisions. These geopolitical tensions create both challenges and opportunities for alternative processing centres.

What Are the Geopolitical Implications of Processing Concentration?

The concentration of rare earth processing capabilities in China creates multiple strategic vulnerabilities across defence, energy transition, and technology sectors. These dependencies extend beyond simple supply disruption risks to encompass broader economic and security implications.

Defence Sector Dependencies

Modern military systems require significant quantities of processed rare earth materials that cannot be easily substituted:

- F-35 fighter aircraft: 920 pounds of rare earth materials per unit

- Virginia-class submarines: 9,200 pounds of rare earth components

- Patriot missile defence systems: Critical dysprosium dependencies for guidance systems

- Electronic warfare platforms: Processed rare earth elements essential for sensor and communication systems

These dependencies create operational risks during geopolitical tensions, as demonstrated by China's export restrictions during trade disputes in 2010-2012 and 2018-2020.

Clean Energy Transition Vulnerabilities

The global transition to renewable energy systems depends heavily on rare earth-intensive technologies controlled by Chinese processing:

- Wind turbine generators: Permanent magnets requiring neodymium and dysprosium

- Electric vehicle motors: Rare earth magnet dependencies for efficiency and power density

- Solar panel inverters: Processed rare earth components essential for grid integration

- Energy storage systems: Battery technologies incorporating multiple rare earth elements

Supply disruptions to processed rare earth materials could significantly delay clean energy deployment timelines and increase transition costs across multiple sectors.

Technology Sector Systemic Risks

Information technology infrastructure depends on Chinese-processed rare earth materials throughout the supply chain:

- Smartphone production: Multiple rare earth elements in displays, speakers, and vibration systems

- Data centre infrastructure: Permanent magnet motors and magnetic storage systems

- 5G network equipment: Rare earth components essential for signal processing and amplification

- Semiconductor manufacturing: Processed materials required for specialised applications

How Might Processing Diversification Scenarios Unfold?

Several potential pathways could reshape the global rare earth processing landscape over the next decade. Each scenario involves different combinations of technological innovation, government policy, and market dynamics.

Scenario 1: Gradual Western Capacity Development (2025-2035)

Probability Assessment: Moderate

This scenario assumes sustained government support for processing infrastructure development in the United States, European Union, and allied nations. Key characteristics include:

- Combined US and EU investment exceeding $10 billion in processing infrastructure

- Australia developing integrated mine-to-magnet operations reducing Chinese dependency

- Japan expanding urban mining and recycling technologies to supplement primary supply

- China maintaining 60-70% global market share while losing monopoly pricing power

Under this scenario, processing diversification occurs slowly due to capital intensity and technical learning curves. Alternative supply chains emerge but operate at higher costs than Chinese facilities, requiring government support or trade protection measures.

Scenario 2: Technology Breakthrough Acceleration (2025-2030)

Probability Assessment: Low-Moderate

Technological innovations could compress diversification timelines through breakthrough improvements in separation chemistry or alternative materials:

- Advanced separation technologies reducing capital requirements for processing facilities

- Recycling innovations achieving economic viability for urban mining operations

- Alternative magnet chemistries reducing rare earth dependencies in critical applications

- Synthetic production methods enabling domestic rare earth element manufacturing

This scenario would shift competitive advantages toward technology leaders rather than resource controllers, potentially diminishing China's structural advantages in traditional processing methods.

Scenario 3: Geopolitical Fragmentation (2025-2040)

Probability Assessment: High

Escalating strategic competition leads to deliberate supply chain separation along geopolitical alignments:

- Trade bloc formation creating separate rare earth processing ecosystems

- China prioritising domestic consumption over export availability

- Western alliance development of redundant but higher-cost processing capacity

- Regional market fragmentation with limited cross-bloc material flows

Under this scenario, economic efficiency becomes subordinated to supply chain security considerations. Multiple parallel processing systems emerge with higher costs but reduced interdependency.

The next major ASX story will hit our subscribers first

What Investment Strategies Address Processing Concentration Risk?

Investors seeking exposure to rare earth processing diversification can pursue several strategic approaches, each involving different risk profiles and timeline considerations.

Upstream Integration Investment Strategy

This approach focuses on mining companies developing integrated processing capabilities:

Lynas Rare Earths (ASX: LYC)

- Operating Malaysian processing facility handling Australian concentrates

- Expanding capacity and developing US processing partnerships

- Risk factors: Regulatory dependencies in Malaysia, capital intensity for expansion

MP Materials (NYSE: MP)

- Developing integrated processing at California Mountain Pass facility

- Planning magnet production capabilities for vertical integration

- Risk factors: Environmental compliance costs, market competition with Chinese pricing

Rare Element Resources (OTCQB: REEMF)

- Advancing Wyoming heavy rare earth project with processing focus

- Potential for critical dysprosium and terbium production

- Risk factors: Development stage uncertainty, financing requirements

Technology Innovation Investment Focus

Supporting companies developing alternative processing technologies or rare earth substitutes:

- Urban mining and recycling technology developers

- Advanced separation chemistry research and commercialisation

- Alternative permanent magnet technologies reducing rare earth requirements

- Synthetic rare earth production methods and equipment manufacturers

Strategic Alliance and Government Partnership Opportunities

Investment in companies benefiting from government processing initiatives:

- US Department of Defence rare earth processing grant recipients

- European Union Critical Raw Materials Act implementation projects

- Japan-Australia rare earth cooperation agreement participants

- Allied nation strategic material reserve development programmes

Portfolio Risk Management Considerations

Effective rare earth investment strategies should account for:

- Timeline mismatches between processing development and market needs

- Technology substitution risks affecting demand for specific elements

- Geopolitical scenario planning for trade restriction impacts

- Environmental compliance cost variations across jurisdictions

How Do Environmental Factors Influence Processing Location Decisions?

Environmental compliance requirements create significant location-dependent cost variations that influence the viability of rare earth processing projects across different jurisdictions.

Regulatory Compliance Cost Disparities

Western rare earth processing facilities operate under environmental standards that add 20-40% to operational costs compared to Chinese equivalents. Major compliance areas include:

- Radioactive waste disposal: Long-term containment requirements for thorium and uranium byproducts

- Water treatment systems: Advanced purification to meet discharge standards for processing chemicals

- Air quality controls: Emissions monitoring and control for volatile organic compounds

- Community impact management: Stakeholder engagement and local benefit sharing requirements

The Lynas Rare Earths Malaysian facility exemplifies these challenges. Despite choosing Malaysia for lower compliance costs compared to Australia, the operation faced shutdown orders in 2011-2012 due to radioactive waste management concerns, demonstrating ongoing environmental and political risks.

Social Licence and Community Acceptance Variables

Public acceptance of rare earth processing varies significantly across regions, affecting project timelines and political sustainability:

- United States: Mixed reception with strong support in mining-dependent communities but resistance in populated areas

- European Union: High environmental standards and extensive public consultation requirements extending development timelines

- Australia: Generally supportive regulatory environment with established mining industry acceptance

- Canada: Provincial variation in approval processes and indigenous consultation requirements

Long-term Waste Management Infrastructure

Processing location decisions must account for geological suitability and regulatory frameworks capable of managing radioactive waste streams over century-long timescales. This constraint significantly limits viable processing locations to areas with:

- Stable geological formations suitable for long-term containment

- Established regulatory frameworks for radioactive material management

- Political and social acceptance of long-term waste storage responsibilities

What Are the Long-Term Strategic Implications?

The evolution of rare earth processing capabilities will fundamentally reshape global supply chains, industrial competitiveness, and strategic relationships over the next two decades.

Market Structure Transformation Patterns

The rare earth processing landscape will likely evolve from Chinese monopoly toward regional oligopoly by 2035. This transition involves:

- Regional processing hubs serving different geographic markets with limited cross-regional integration

- Technology specialisation where different regions develop advantages in specific separation technologies or applications

- Integration strategies linking processing with downstream manufacturing to capture additional value-chain segments

Each regional hub will likely serve 15-25% of global demand, with China maintaining the largest but not monopolistic market share.

Technology Integration and Automation Trends

Future competitive advantages in rare earth processing will increasingly depend on advanced technology integration:

- Artificial intelligence optimisation of extraction parameters and quality control systems

- Automated processing systems reducing labour costs and improving consistency

- Environmental technology integration minimising waste streams and regulatory compliance costs

- Modular facility designs enabling faster deployment and scale-up of processing capacity

These technological advances could compress the capital intensity and timeline barriers that currently protect established processors.

Resource Security Framework Development

Nations are developing strategic rare earth reserves and processing capacity as critical infrastructure, similar to strategic petroleum reserves:

- Strategic material stockpiles providing short-term supply security during disruptions

- Processing capacity reserves maintaining minimum domestic separation capabilities for critical applications

- Technology preservation programmes ensuring access to separation expertise and equipment manufacturing

- Alliance coordination mechanisms sharing processing capacity and technical knowledge among allied nations

Industrial Policy Coordination Requirements

Successful processing diversification will require unprecedented coordination between government policy, private investment, and international cooperation:

- Demand aggregation across allied nations to support economically viable processing facilities

- Technology sharing agreements accelerating capability development and reducing duplication

- Risk sharing mechanisms protecting private investment from Chinese competitive responses

- Standards harmonisation enabling cross-border processing and supply chain integration

Navigating the Processing Transition Landscape

China's rare earth processing dominance reflects the convergence of deliberate strategic planning, technical mastery, and structural advantages accumulated over multiple decades. The co-occurrence of rare earth elements and the extreme complexity of separation chemistry create natural barriers to competition that extend far beyond simple cost considerations.

Understanding why china controls rare earth processing requires recognising that geological resource distribution provides minimal competitive advantage without corresponding processing capabilities. The technical demands of achieving 99.9%+ purity separation, managing radioactive waste streams, and operating at commercial scale create sustained barriers to entry that favour established processors.

Furthermore, China's rare earth export controls have demonstrated Beijing's willingness to use processing dominance as a strategic tool. Additionally, recent analysis from China's rare earth processing monopoly highlights the structural challenges Western nations face in developing alternative capacity.

Diversification efforts currently underway in the United States, European Union, Australia, and allied nations face significant challenges including capital intensity, environmental compliance requirements, and competitive pricing pressure from Chinese facilities. However, strategic imperatives for processing independence continue to strengthen as rare earth applications expand across defence, clean energy, and technology sectors.

The transition toward processing diversification will likely unfold gradually over 10-15 year timescales, requiring coordinated government support, patient capital investment, and technological innovation across multiple countries simultaneously. Success depends on moving beyond mining-focused strategies toward integrated approaches linking ore production, separation chemistry, and downstream manufacturing capabilities.

For investors, policymakers, and industry participants, the rare earth processing landscape represents both significant risks and opportunities. While Chinese dominance will persist in the near term, the strategic value of alternative processing capabilities continues to grow as geopolitical tensions intensify and supply chain resilience becomes a national security priority.

Disclaimer: This analysis contains forward-looking assessments and scenario projections based on current market conditions and policy trends. Rare earth market dynamics involve significant uncertainties including technological developments, regulatory changes, and geopolitical factors that may materially affect actual outcomes. Investment decisions should be based on comprehensive due diligence and professional financial advice.

Want to capitalise on Australia's growing critical minerals sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in Australia's strategically important critical minerals space.