June 25, 2026

The Hidden Mechanics of Rare Earth Refining — And Why Location Matters More Than Ever

Most industrial supply chains are invisible until they break. The rare earth supply chains sector is a textbook example of this phenomenon. For decades, manufacturers across Japan, Europe, and North America quietly absorbed Chinese-processed rare earth materials without examining the structural fragility embedded in that arrangement. The events of 2025 and 2026 have forced that examination upon them with extraordinary urgency.

Understanding why the Shin-Etsu Chemical rare earths refinery in Japan represents far more than a single corporate capital decision requires stepping back from the headlines and examining what rare earth refining actually involves at a technical level, why it is so geographically concentrated, and what the real cost of supply rupture looks like when zero shipments arrive across four consecutive months.

When big ASX news breaks, our subscribers know first

Why Rare Earth Refining Is Structurally Different From Other Commodity Processing

Rare earth elements are not actually rare in terms of crustal abundance. Cerium, lanthanum, and neodymium exist in the Earth's crust at concentrations comparable to copper. The challenge is that they occur in mineralogically complex deposits, often intermixed with radioactive thorium and uranium, and separating individual elements from each other requires an exceptionally sophisticated hydrometallurgical process known as solvent extraction.

Solvent extraction for rare earths involves hundreds of sequential mixer-settler stages, highly specific organic solvents, and exacting pH control across the entire production circuit. The rare earth processing challenges inherent to this method are considerable. The process is:

- Chemically intensive, requiring large volumes of acid and alkali reagents

- Technically demanding, with purity tolerances measured in parts per million

- Environmentally complex, generating acidic wastewater streams that require careful management

- Capital-intensive, with large-scale separation circuits requiring years to design, permit, and commission

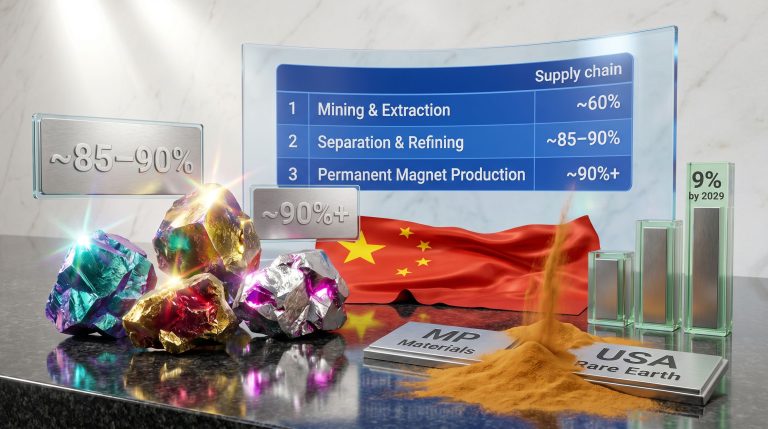

This is precisely why China commands an estimated 85–90% of global rare earth separation and refining capacity despite not holding a proportionate share of global reserves. The country built this infrastructure incrementally over three decades, accepting the environmental costs and investing in the chemical engineering expertise that most other nations declined to develop.

The consequence is a supply chain architecture where even if a mining company in Australia or Canada produces rare earth concentrate, that material almost invariably travels to China for the separation and refining steps before re-entering global trade as usable oxide or metal.

How China's Export Controls Created a Zero-Shipment Reality

China's export restrictions on medium and heavy rare earth categories — covering materials including dysprosium oxide, terbium oxide, and the high-performance permanent magnets incorporating them — were introduced in April 2025. However, what was underestimated was the speed and completeness of the supply cessation.

Trade data from early 2026 reveals the severity of the disruption. Chinese shipments of dysprosium and terbium oxide to Japan recorded zero volume across January, February, March, and April of the current year. This is not a reduction or a slowdown. It is a complete halt.

The significance of this data point is difficult to overstate. Dysprosium and terbium are not interchangeable with any other material in their primary application. They function as coercivity enhancers within neodymium-iron-boron (NdFeB) permanent magnets, allowing those magnets to maintain their magnetic strength at elevated operating temperatures. Without adequate dysprosium or terbium additions, an NdFeB magnet used in an EV drivetrain motor will begin to demagnetise irreversibly when the motor heats up under load.

In early 2026, China compounded the situation by specifically targeting Japan through restrictions prohibiting the export of dual-use items to Japanese military-affiliated end users. Furthermore, any entities assessed as capable of enhancing Japan's defence capabilities were included. The cumulative impact on ex-China spot prices for heavy rare earth oxides has been substantial, with premiums rising to exceptionally elevated levels relative to historical benchmarks tracked by commodity price reporting agencies including Fastmarkets.

Shin-Etsu's Refinery: Project Parameters and Strategic Rationale

Against this backdrop, the announcement of the Shin-Etsu Chemical rare earths refinery in Japan takes on a clarity that extends well beyond routine capacity planning. The facility, to be located in Fukui Prefecture in western Japan, represents a deliberate attempt to domesticate the most vulnerable segment of the rare earth supply chain: the separation and refining step that currently has almost no non-Chinese capacity at meaningful industrial scale.

| Parameter | Detail |

|---|---|

| Facility Location | Fukui Prefecture, western Japan |

| Estimated Capital Investment | Over ¥35 billion (approximately USD $218 million) |

| Government Subsidy Component | Approximately 50% of total investment |

| Existing Regional Footprint | Two existing manufacturing plants in Fukui Prefecture |

| International Processing Operations | Rare earths processing facility in Vietnam |

| Current Domestic Refining Capability | 16 out of 17 rare earth elements |

Several aspects of this project merit closer examination than a straightforward capacity announcement would suggest.

The Vertical Integration Advantage

Shin-Etsu is currently the only manufacturer globally that controls the complete rare earth magnet production process within a single integrated operational framework, from initial ore separation and element refinement through alloy production and finished magnet casting. This matters because each handoff point in a disaggregated supply chain represents a potential disruption node. Shin-Etsu's integration eliminates those nodes entirely.

The Fukui Clustering Logic

Locating the new refinery adjacent to two existing Shin-Etsu manufacturing plants in Fukui Prefecture is not merely a matter of convenience. Industrial clustering in rare earth processing generates genuine cost advantages, including shared reagent handling infrastructure, consolidated waste treatment, and reduced logistics complexity for intermediate products moving between process stages.

The Vietnam Feedstock Pathway

Shin-Etsu's existing rare earths processing operation in Vietnam provides a geographically diversified input source that does not depend on Chinese-origin raw materials. Vietnam possesses significant rare earth mineral deposits, and Shin-Etsu's established presence there creates a feedstock pipeline that bypasses Chinese-controlled supply routes entirely.

The Hydrometallurgical Gap: Why Building This Refinery Takes Time

One of the less discussed dimensions of the Shin-Etsu refinery announcement is the inherent complexity of the construction timeline. Unlike a simple warehouse or assembly facility, a rare earth separation plant requires:

- Detailed process engineering design, typically requiring 12–18 months for a facility of this complexity

- Specialised equipment procurement, including mixer-settler banks, solvent recovery systems, and acid-handling infrastructure with long lead times

- Regulatory approvals for chemical processing facilities, which in Japan involve multiple agency consultations

- Commissioning and process optimisation, which for solvent extraction circuits can take 6–12 months after mechanical completion

- Workforce training, as experienced rare earth hydrometallurgists represent a scarce human resource outside China

Based on comparable rare earth refinery construction timelines observed globally, a facility of this scale and technical complexity would typically require three to five years from groundbreaking to full operational capacity. This timeline underscores a critical point: the Shin-Etsu investment is a long-duration strategic bet, not a near-term supply remedy.

The gap between announcement and first production output is a structural feature of rare earth refinery development that investors and supply chain planners must account for explicitly. Companies and governments making commitments today are positioning for the supply landscape of 2029–2031, not 2026.

Target Elements: Why Dysprosium, Terbium, and Yttrium Were Chosen

The selection of dysprosium, terbium, and yttrium as the primary focus elements for the new Shin-Etsu Chemical rare earths refinery in Japan reflects a deliberate commercial and strategic calculation.

Dysprosium and terbium are classified as heavy rare earth elements (HREEs), sourced predominantly from ionic clay deposits in southern China's Jiangxi province. Unlike the light rare earth elements (LREEs) such as neodymium and praseodymium — which can be sourced from hard-rock deposits in Australia, the United States, and Canada — HREE deposits of comparable grade and extractability are genuinely scarce outside Chinese territory. This makes dysprosium and terbium the most strategically exposed elements within the NdFeB magnet system.

Yttrium occupies a different but equally critical niche. It is an indispensable material in:

- Yttria-stabilised zirconia coatings used in plasma-resistant components within semiconductor fabrication equipment

- Phosphors used in lighting and display applications

- Specialty ceramic formulations with high-temperature stability properties

Japanese manufacturers of semiconductor fabrication equipment hold significant global market positions, making yttrium supply security a direct industrial competitiveness issue for the country's technology sector.

The next major ASX story will hit our subscribers first

Japan's Processing-Centric Strategy in a Global Context

Japan's approach to rare earth supply security is structurally distinct from the strategies pursued by the United States and the European Union, reflecting the country's specific industrial geography: significant manufacturing capability but no domestic rare earth ore deposits.

| Country/Region | Strategic Approach | Key 2025–2026 Developments |

|---|---|---|

| Japan | Domestic refinery investment + recycling + diversified feedstock sourcing | Shin-Etsu Fukui refinery; Daikin magnet recycling partnership |

| United States | Mine-to-magnet vertical integration via acquisition | Energy Fuels acquires German magnet maker VAC for approximately $1.9 billion |

| European Union | Critical Raw Materials Act; domestic processing targets and investment mandates | Regulatory framework driving capital allocation requirements |

| Australia | Upstream mining expansion with downstream processing partnerships | Multiple rare earth projects advancing toward production stage |

Japan's processing-centric posture means the country is essentially betting on its ability to source ore and concentrate from diversified international suppliers whilst maintaining sovereign control over the value-added conversion steps. This is a rational strategy for a resource-constrained manufacturing economy. However, it does carry feedstock sourcing risk if alternative rare earth supply from allied-nation mining projects fails to deliver expected volumes on schedule.

The Recycling Dimension: Strategic Buffer, Not Structural Solution

Shin-Etsu's April 2026 partnership with Daikin Industries to recover and recycle rare earth magnets from end-of-life air conditioner compressors — with operations targeting commencement in 2027 — represents an important but frequently misunderstood element of Japan's rare earth strategy.

Understanding what recycling can and cannot realistically deliver is essential for accurate supply chain assessment:

- Recycled rare earth permanent magnets currently account for an extremely small proportion of global rare earth supply

- The overwhelming majority of existing magnet recycling infrastructure is concentrated in China, where most permanent magnets are produced

- Collection logistics present a significant challenge, as end-of-life compressors, motors, and electronics are distributed across vast and fragmented waste streams

- Demagnetisation of recovered magnets requires energy-intensive thermal or hydrogen-based processing before the alloy can be reintroduced into production

- Hydrometallurgical reprocessing of recycled magnet material involves many of the same technical complexities as primary refining

The Daikin partnership is strategically valuable precisely because it creates a closed-loop material flow between two entities that already have an established commercial relationship. Daikin uses Shin-Etsu magnets in its compressors; recovering those magnets at end-of-life and returning them to Shin-Etsu's production cycle reduces feedstock dependency and creates an auditable, traceable material stream that primary ore processing cannot easily replicate.

However, even optimistic projections for urban mining and recycling initiatives globally suggest that recycled rare earth supply is unlikely to displace more than a low single-digit percentage of primary production demand within the next decade. Consequently, recycling is best understood as a strategic buffer during acute supply disruption events rather than a structural solution to China's refining dominance.

Downstream Industry Exposure: Who Needs This Refinery to Succeed

The commercial success of the Shin-Etsu Chemical rare earths refinery in Japan carries direct implications for multiple downstream industrial sectors:

Electric Vehicle Manufacturing: NdFeB permanent magnets are integral to the high-torque, high-efficiency traction motors used in battery electric and hybrid vehicles. Japanese automakers including Toyota, Honda, and Nissan face direct exposure to rare earth magnet supply constraints, with magnet availability already identified as a potential bottleneck for EV production scaling.

Industrial Robotics: Japan is a dominant global producer of industrial robots, with rare earth motors embedded across virtually all high-performance robotic systems. The country's robotics manufacturers are acutely sensitive to magnet supply reliability.

Semiconductor Equipment: Japanese manufacturers of plasma etch and deposition equipment used in semiconductor fabrication require yttrium-based ceramic components that must meet extremely demanding purity and dimensional stability specifications.

Air Conditioning Systems: Modern inverter-driven air conditioners, which dominate the global market, depend on compact, high-efficiency compressor motors built around rare earth permanent magnets. Daikin's partnership with Shin-Etsu directly acknowledges this dependency.

What This Investment Signals to the Broader Rare Earth Market

The decision by Tokyo to subsidise approximately 50% of the Shin-Etsu refinery's capital cost is perhaps the most instructive data point in the entire announcement. Government co-investment at this scale communicates unambiguously that rare earth processing capability has been elevated to the same policy priority tier as semiconductor manufacturing and energy security in Japan's industrial strategy framework.

China's rare earth strategy has, in effect, accelerated this shift by demonstrating the consequences of dependence on a single processing nation. For rare earth market participants, several implications follow from this:

- Upstream project developers supplying non-Chinese rare earth concentrate will find Japan a motivated customer, particularly for HREE-bearing feedstocks that can support dysprosium and terbium production

- Ex-China spot price premiums for heavy rare earth oxides are likely to remain structurally elevated until meaningful new non-Chinese refining capacity comes online, a process measured in years rather than months

- Allied-nation supply chain coordination between Japan, Australia, the United States, and Canada is likely to intensify, with the Shin-Etsu facility serving as a downstream anchor for upstream mining investments across those countries

- Competing refinery investments in the United States and Europe may accelerate as the Shin-Etsu announcement demonstrates both the commercial viability and the political appetite for domestic rare earth processing capacity

Disclaimer: This article contains forward-looking analysis based on publicly available information and market observations current as of the date of publication. Rare earth market conditions, pricing, and project timelines are subject to change. Nothing in this article constitutes financial or investment advice. Readers should conduct independent due diligence before making any investment decisions.

Key Takeaways for Industry Observers

The Shin-Etsu Chemical rare earths refinery in Japan is simultaneously a corporate capacity decision, a geopolitical statement, and a structural bet on the long-term reorganisation of global rare earth supply chains. Several conclusions stand out for those following this market closely:

- The zero-shipment data from China to Japan across four consecutive months represents one of the most significant documented rare earth supply disruptions since China's 2010 export quota restrictions

- Shin-Etsu's unique position as the sole globally integrated rare earth magnet producer — covering 16 of 17 elements and the full production chain — means this refinery investment compounds rather than creates an existing competitive advantage

- The three-to-five year construction horizon means the facility's contribution to supply security lies in the 2029–2031 window, requiring supply chain managers to identify bridge solutions in the interim

- Recycling, exemplified by the Daikin partnership, provides meaningful strategic optionality but cannot substitute for primary processing capacity at the volumes required by Japan's manufacturing economy

- The combination of new primary refining capacity, diversified Vietnamese feedstock, and emerging closed-loop recycling infrastructure represents a multi-layered supply resilience architecture that other non-Chinese rare earth stakeholders are now studying closely as a potential template

For ongoing rare earth market intelligence including price data, trade flow analysis, and supply chain developments, Fastmarkets provides specialised coverage of the global rare earth sector through its metals and mining rare earths news and price data platform.

Want To Catch the Next Major Rare Earth Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant rare earth and critical mineral discoveries and translating complex geological data into clear, actionable opportunities — explore historic examples of major mineral discoveries and their returns to understand what's at stake, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market as the rare earth supply chain reshapes itself beyond China's dominance.