May 22, 2026

The Invisible Chokepoint: Why Rare Earth Refining Is America's Most Urgent Industrial Vulnerability

Most discussions about rare earth supply chains fixate on mining, on who controls the ground and what lies beneath it. But the more strategically consequential bottleneck sits further down the production chain, in the furnaces, leaching circuits, and solvent extraction facilities where raw ore is transformed into the high-purity oxides that defence manufacturers actually require. It is at this refining stage, not the mining stage, where geopolitical vulnerability is most acute, and where the current dispute between the Pentagon and the White House over the Pentagon rare earths deal involving ReElement Technologies exposes something far more significant than a bureaucratic disagreement.

The clash is a symptom of a structural problem that no executive order, no billion-dollar announcement, and no interagency working group has yet solved: the United States does not have a coherent institutional framework for deploying public capital into pre-commercial industrial technology at the speed that national security demands, whilst simultaneously maintaining the financial discipline that taxpayer accountability requires.

When big ASX news breaks, our subscribers know first

The Refining Bottleneck: Where China's Leverage Actually Lives

Understanding why this dispute matters requires a clear-eyed look at the rare earth supply chain as it actually functions, not as it is often described in policy documents.

Rare earth elements are a group of 17 metals with unique magnetic, luminescent, and catalytic properties. The ones most relevant to defence and clean energy applications — particularly neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb) — are required inputs for the permanent magnets used in fighter jet actuators, guided missile systems, electric vehicle drive motors, wind turbine generators, and a broad range of consumer electronics.

The supply chain involves several distinct stages, each with different strategic characteristics:

| Supply Chain Stage | U.S. Domestic Capacity | China's Estimated Global Share | Strategic Risk Level |

|---|---|---|---|

| Mining / Extraction | Moderate (MP Materials, Lynas USA) | ~60% | Medium |

| Processing / Separation | Very Limited | ~85-90% | Critical |

| Magnet Manufacturing | Nascent | ~90%+ | Critical |

| Recycling / Secondary Refining | Emerging | ~70% | High |

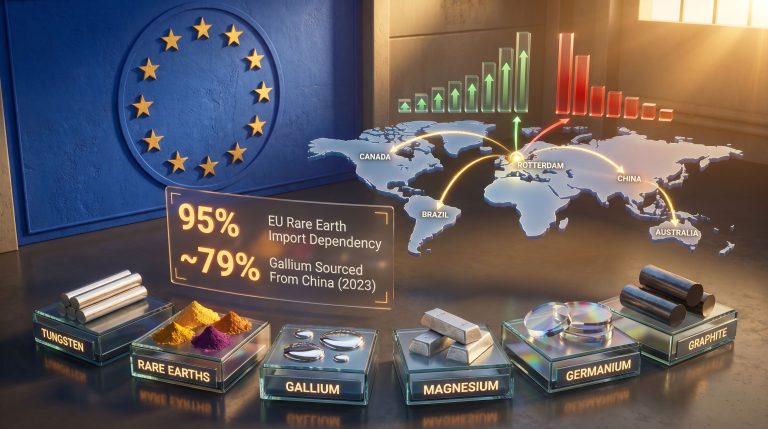

China controls approximately 70% of global rare earth mineral extraction and roughly 90% of global refining and separation capacity, according to widely cited industry estimates. This asymmetry is not accidental. It is the product of decades of deliberate industrial policy, subsidised processing infrastructure, and a tolerance for environmental externalities that Western regulatory frameworks do not permit.

Furthermore, the refining stage is particularly difficult to replicate quickly. Rare earth separation uses a technique called solvent extraction — a multi-stage chemical process that requires significant capital investment, specialised chemical inputs, precise process control, and environmental management infrastructure. Building a greenfield separation facility typically takes between five and ten years from initial planning to commercial operation, even with strong financial backing. This timeline reality is central to understanding why pre-revenue companies like ReElement represent both an important opportunity and a genuine diligence challenge, and it sits at the heart of broader rare earth processing challenges facing the West.

The $1.4 Billion Framework: What Was Actually Announced

In November of the prior year, the Pentagon's Office of Strategic Capital announced a conditional loan agreement with ReElement Technologies as part of a broader $1.4 billion critical minerals package that also included Vulcan Elements Inc. The structure was designed as a vertically integrated domestic supply chain: ReElement would produce high-purity rare earth oxides from electronic waste and decommissioned magnets, and Vulcan would convert those oxides into finished rare earth magnets for defence and commercial applications. The combined output target was stated as up to 10,000 metric tons of magnet materials over several years.

The ReElement component specifically involved an $80 million conditional loan from the OSC. The word conditional is important. The Pentagon's announcement was explicit that disbursement required ReElement to satisfy financial, legal, technical, and other due diligence requirements. No funds had been disbursed at the time the White House clash became public.

ReElement's position in this framework is noteworthy for several reasons:

- The company was a subsidiary of Nasdaq-listed American Resources Corp. until relatively recently, and was described in an October 2025 filing as being in a "pre-revenue development stage"

- It had previously received a $2 million, two-year investment through the Pentagon's Industrial Base Analysis and Sustainment (IBAS) programme, suggesting a prior relationship with defence industrial planners

- In January, the company announced $200 million in strategic equity from Transition Equity Partners, which explicitly cited ReElement's government collaboration as a factor in the investment decision

- The State Department referenced this private capital raise at a critical minerals summit in February, describing it as an example of government signalling having "crowded in" private investment

That crowding-in dynamic is precisely what makes the current uncertainty so consequential. If government confidence in ReElement is openly contested, the downstream effects on private co-investors who made commitments partly on the strength of that signal cannot be dismissed.

Two Institutions, Two Mandates, One Conflict

The public dimension of the Pentagon rare earths deal White House clash emerged when Peter Navarro, the White House Senior Counsellor for Trade and Manufacturing, independently reached out to Bloomberg News to criticise the Pentagon's handling of the ReElement review. His criticism was directed at the OSC's due diligence team, which he characterised as applying private equity frameworks unsuited to a national security emergency requiring rapid action.

Pentagon spokesman Sean Parnell responded by defending the OSC team as highly qualified professionals capable of balancing speed with rigorous vetting. The programme is overseen by Deputy Defence Secretary Stephen Feinberg, the co-founder of Cerberus Capital Management, one of the world's largest private equity firms.

The institutional tension here runs deeper than a single deal:

| Institution | Primary Mandate | Position on ReElement |

|---|---|---|

| White House (Navarro) | Accelerate domestic industrial buildout at national security speed | Advocates for fast deployment; views OSC scrutiny as disproportionate |

| Pentagon OSC | Deploy capital with financial discipline and milestone accountability | Conducting active due diligence; raised concerns about technology scalability and revenue forecasts |

| Pentagon Leadership (Feinberg) | Balance strategic urgency with institutional accountability | Overseeing process without publicly taking sides |

| ReElement (CEO Jensen) | Secure financing; advance Indiana facility | Confirmed ongoing government collaboration; declined to address loan status |

The core disagreement reflects a genuine policy dilemma that industrial policy programmes in other countries have also encountered. When government capital is deployed into emerging technology companies at a pre-commercial stage, standard financial due diligence tools — built for evaluating companies with revenue histories, comparable industry benchmarks, and established customer relationships — are genuinely poorly calibrated for the task.

A pre-revenue rare earth refiner using a novel recycling-based feedstock model does not map neatly onto the financial analysis frameworks developed for evaluating established industrial borrowers. The uncertainty bands on revenue forecasts are structurally wide, not because of poor management, but because the commercial model has not yet been demonstrated at scale.

This is not an argument for abandoning due diligence. It is, however, an argument for designing due diligence frameworks that are appropriate to the asset class being evaluated.

ReElement's Technology Model: The Secondary Refining Opportunity

What makes ReElement's proposed approach strategically interesting — and simultaneously difficult to evaluate using conventional metrics — is its focus on secondary refining, the extraction of rare earth oxides from electronic waste and end-of-life magnets rather than from virgin ore.

This circular economy model targets a segment of the rare earth supply chain that is genuinely underinvested domestically. The United States generates substantial volumes of rare earth-bearing waste streams, from decommissioned military equipment and industrial motors to consumer electronics and wind turbine components. The rare earth content of these materials is recoverable, but the processing technology required to extract high-purity oxides from mixed secondary feedstocks is technically complex and not yet commercially proven at scale in the United States.

Key characteristics of the secondary refining model relevant to assessing ReElement's approach include:

- Feedstock variability is a significant technical challenge. Unlike virgin ore from a single deposit with consistent mineralogy, secondary feedstocks vary in composition, contamination levels, and rare earth concentration. Process chemistry must be adaptable.

- Separation purity requirements for defence-grade magnet materials are stringent. Neodymium-iron-boron (NdFeB) magnets require rare earth oxides of very high purity — typically 99%+ for individual rare earth elements — to achieve the magnetic performance specifications required by defence applications.

- Scale-up risk is the key variable. Bench-scale and pilot-scale demonstrations of rare earth recycling technology do not automatically translate to commercial-scale economics. Chemical consumption, waste stream management, and throughput rates all shift at larger scales.

- The Indiana facility ReElement is developing represents a genuine step toward demonstrating commercial viability, but as of late 2025, the company had not yet produced oxides at commercial scale.

Comparable international experience is instructive. Lynas Rare Earths, now one of the most significant non-Chinese rare earth producers, required well over a decade of development, multiple rounds of government support across Australia, Malaysia, and the United States, and significant capital investment before achieving the production volumes that now make it strategically relevant. The timeline expectations embedded in the OSC's due diligence concerns are therefore not unreasonable, even if the urgency of the policy problem is genuine.

Governance Design and the Lessons of Prior Industrial Policy

The ReElement situation is not the first time U.S. industrial policy programmes have encountered the tension between strategic urgency and financial accountability. The Solyndra loan guarantee under the DOE's loan programmes office in 2011 produced significant political fallout when the company entered bankruptcy, shaping institutional risk appetite in federal lending programmes for years afterward. The lesson most commonly drawn from that experience — that pre-revenue technology companies require staged capital deployment with verified milestones — is precisely the approach the OSC's due diligence process appears to be applying to ReElement.

The broader structural issue is that the United States lacks a dedicated critical minerals development institution with a clear mandate to balance speed, risk tolerance, and accountability in a single organisational framework. Consequently, current mechanisms — including the OSC, the IBAS programme, the Development Finance Corporation, and DOE loan programmes — operate with different risk appetites, different timelines, and different accountability structures. The broader US critical mineral strategy has yet to resolve this fragmentation in any meaningful institutional sense.

| Program | Country | Key Lesson |

|---|---|---|

| DOE Loan Guarantee (Solyndra, 2011) | USA | Pre-revenue technology risk requires staged capital deployment |

| Lynas Rare Earths development | Australia / USA | Long timelines required even with strong government backing |

| Japan JOGMEC rare earth investments | Japan | State-backed entities with defined risk mandates outperform ad hoc programmes |

| Critical Minerals Facility (NAIF) | Australia | Dedicated mandates reduce institutional friction |

The next major ASX story will hit our subscribers first

The Allied Dimension: Why Institutional Credibility Matters Beyond U.S. Borders

The public nature of the Pentagon rare earths deal White House clash carries implications that extend beyond the ReElement loan itself. The United States has established bilateral critical minerals cooperation frameworks with Australia, Japan, and a growing number of other nations. In fact, the historic US-Australia critical minerals agreement signed between President Trump and Prime Minister Albanese underscores how central allied coordination has become to America's rare earth supply chain ambitions. Discussions have reportedly involved more than 50 countries around trade arrangements and pricing mechanisms designed to compete with Chinese market influence.

Allied governments and private sector co-investors evaluate U.S. institutional reliability as a factor in deciding whether to commit resources to shared supply chain frameworks. However, when senior White House officials publicly criticise the due diligence standards of the institution responsible for executing those frameworks, the signal received by external partners is not one of confident, coordinated industrial mobilisation. It is one of internal incoherence.

The credibility of U.S. programme governance is itself a strategic asset. Furthermore, protecting it requires resolving the institutional design problem at the heart of this conflict — not just managing individual deal disputes as they surface publicly. This is especially consequential given the ongoing pressure of China's export restrictions on critical materials, which continue to raise the strategic stakes for every Western-aligned nation.

What a More Coherent Strategy Would Require

Several structural reforms would reduce the likelihood of future institutional clashes whilst preserving both speed and accountability:

- Risk-tiered capital frameworks that explicitly distinguish between early-stage technology validation bets — where higher risk tolerance and longer timelines are appropriate — and near-commercial scale-up investments, where conventional due diligence is well-calibrated.

- Staged disbursement mechanisms that link capital release to verified technical and commercial milestones, reducing the binary dynamic of approving or cancelling large loan commitments before key uncertainties are resolved.

- Specialised technical review capacity for novel processing technologies, particularly recycling-based rare earth refining models, where traditional private equity due diligence frameworks have limited precedent to draw from.

- Interagency coordination protocols that keep internal disagreements about deal quality within institutional channels rather than surfacing them publicly in ways that destabilise private co-investment positions.

- Longer investment horizons for secondary refining and recycling programmes, which require extended development timelines but address the refining bottleneck that represents China's most durable point of strategic leverage.

Disclaimer: This article contains analysis, forecasts, and speculative assessments regarding pre-commercial companies, government policy programmes, and rare earth supply chain development. These views are based on publicly available information and should not be construed as investment advice. All forward-looking statements involve uncertainty, and outcomes may differ materially from those described. Readers should conduct independent research before making any investment decisions.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly converting complex mineral data across more than 30 commodities into clear, actionable insights — so subscribers are never last to act on a significant discovery. Explore historic examples of exceptional discovery returns and begin a 14-day free trial to position yourself ahead of the broader market.