June 2, 2026

The Processing Gap at the Heart of the Rare Earth Crisis

The global conversation around rare earth supply chain importance tends to fixate on mining. Where are the deposits? Who controls the reserves? Yet the more consequential bottleneck sits one step downstream, inside the processing and separation infrastructure that converts raw ore into the high-purity oxides that manufacturers actually need. This distinction matters enormously, because it reframes the entire strategic challenge facing Western industry.

China's dominance in rare earth separation capacity is not an accident of geology. It is the product of decades of deliberate industrial policy. Estimates consistently place China's share of global rare earth separation and refining capacity at above 85%, meaning that even ore extracted from mines in Australia, Canada, or Brazil has historically been shipped to China for processing before re-entering global supply chains. For European manufacturers of electric vehicles, wind turbines, and defence systems, China's rare earth restrictions create an exposure that sits well beyond the reach of any individual company's procurement strategy.

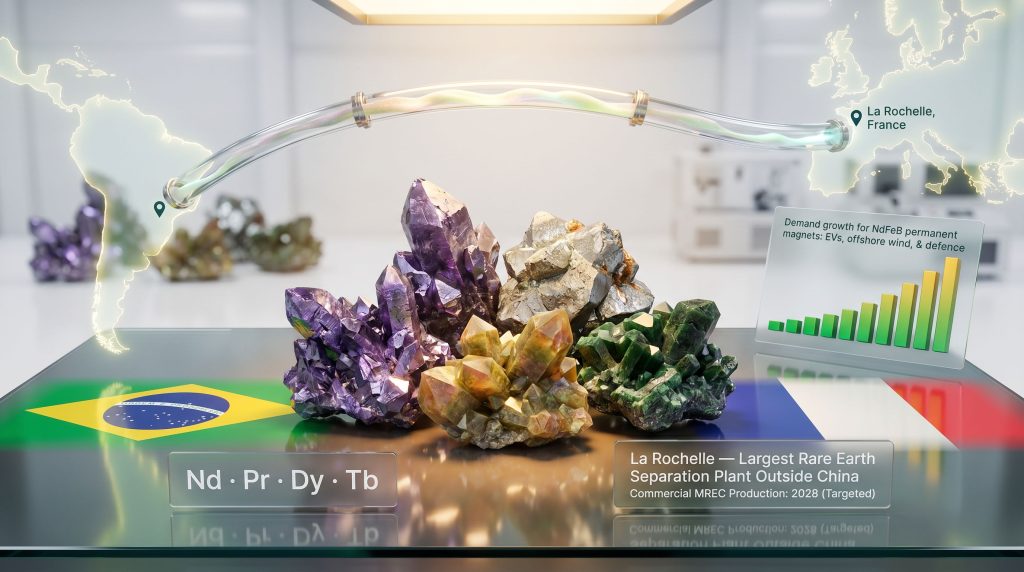

The Solvay and Viridis rare earth supply agreement, formalised through a non-binding Letter of Intent in June 2026, is one of the more structurally significant responses to this challenge to emerge from the European industrial sector. It is not simply a supply deal. It is an attempt to wire together two missing links in a non-Chinese rare earth value chain: a Brazilian feedstock source and a French separation facility with the technical capability to convert that feedstock into market-ready oxides.

When big ASX news breaks, our subscribers know first

Understanding the Four Magnet Rare Earths That Drive This Agreement

Before analysing the commercial architecture of the Solvay and Viridis rare earth supply agreement, it is worth understanding precisely which materials are at stake and why they command such strategic attention.

The four primary rare earth elements identified in the agreement are neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). These are the core inputs for neodymium-iron-boron (NdFeB) permanent magnets, which are embedded in virtually every electric vehicle drivetrain and offshore wind turbine generator currently in production. A single electric vehicle requires approximately 1 to 2 kilograms of NdPr oxide for its traction motor, while a large offshore wind turbine can require several hundred kilograms of magnet material depending on its generating capacity.

Dysprosium and terbium perform a different but equally critical function. At elevated operating temperatures, NdFeB magnets lose their coercivity — their ability to resist demagnetisation. Adding small quantities of Dy and Tb restores this performance characteristic, making them indispensable for automotive and defence applications where thermal stability is non-negotiable. These heavy rare earths are significantly scarcer than their light counterparts, concentrated in ion-adsorption clay deposits in southern China and Myanmar, making their supply chain exposure even more acute.

The Colossus feedstock also contains three additional heavy rare earth elements with distinct end-market applications:

| Rare Earth Element | Primary Application | End Market |

|---|---|---|

| Neodymium (Nd) | NdFeB permanent magnets | EVs, wind turbines |

| Praseodymium (Pr) | NdFeB permanent magnets | EVs, wind turbines |

| Dysprosium (Dy) | High-temperature magnet performance | Automotive, defence |

| Terbium (Tb) | High-temperature magnet performance | Automotive, defence |

| Samarium (Sm) | Samarium-cobalt magnets | Aerospace, defence |

| Gadolinium (Gd) | MRI contrast agents, neutron shielding | Medical, nuclear |

| Yttrium (Y) | Phosphors, ceramics, electronics | Electronics, aerospace |

Samarium-cobalt magnets, while less common than NdFeB in consumer applications, are preferred in defence and aerospace contexts because of their superior performance at extreme temperatures and their resistance to corrosion. Their presence in the Colossus feedstock adds meaningful optionality to the commercial proposition.

The Colossus Project and Why Brazil Matters

Viridis Mining and Minerals' Colossus Rare Earth Project in Brazil is the designated upstream feedstock source under the LOI framework. Brazil represents an underappreciated node in the global rare earth landscape. The country hosts substantial rare earth mineral endowment, yet its contribution to processed rare earth supply has historically been minimal relative to its geological potential.

From a geopolitical standpoint, Brazilian supply carries a neutrality that is difficult to replicate with alternatives. Australian supply chains, while well-developed through operators like Lynas Rare Earths, are subject to their own bilateral trade sensitivities. African projects face infrastructure and governance challenges that complicate financing timelines. Brazil's regulatory environment for mining, while not without complexity, provides a degree of political stability and institutional predictability that supports long-term project development.

The LOI targets commercial production of mixed rare earth carbonate (MREC) from the Colossus project by 2028, with a final investment decision anticipated in the second half of 2026. These timelines are ambitious for a development-stage project, but they align with a projected demand acceleration in the NdPr market as electric vehicle penetration rates increase across European and North American markets in the latter half of the decade.

Furthermore, rare earth processing challenges remain central to understanding why this arrangement carries such strategic weight. Mixed rare earth carbonate is an intermediate product, produced through hydrometallurgical processing of rare earth ore. It contains a mixture of rare earth oxalates or carbonates that must undergo solvent extraction and further refining to yield individual separated oxides. The commercial logic of the Solvay agreement is that La Rochelle performs precisely this conversion step.

La Rochelle: Europe's Most Consequential Rare Earth Asset

Solvay's processing facility at La Rochelle in western France occupies a singular position in the European rare earth landscape. It is described as one of the largest rare earth separation plants operating outside China, and its technical capabilities span the full range of rare earth oxide separation from mixed carbonate feedstocks.

The facility's strategic importance extends beyond its current output. In a supply chain architecture where China controls the separation stage, La Rochelle represents one of the few Western-located assets capable of converting upstream feedstock into the high-purity oxides that European automotive and defence manufacturers need. Maximising its throughput is therefore both a commercial imperative for Solvay and a contribution to Europe's critical minerals supply chain resilience.

The processing margin that Solvay captures is material. MREC trades at a significant discount to separated rare earth oxides, with the conversion process adding substantial value per kilogram of output. This margin structure underpins the commercial rationale for Solvay to actively seek and support new upstream supply sources, even when those sources require developmental capital and technical assistance to reach production.

The Non-Chinese Supply Chain: Where Does This Deal Fit?

The Solvay and Viridis rare earth supply agreement sits within a broader competitive landscape of Western supply chain development initiatives. The following table contextualises the deal against comparable efforts:

| Initiative | Origin Country | Processing Location | Target Materials | Status |

|---|---|---|---|---|

| Solvay–Viridis LOI | Brazil | France (La Rochelle) | Nd, Pr, Dy, Tb + heavy REEs | LOI signed; FID targeted H2 2026 |

| MP Materials | USA | USA | NdPr | Operational |

| Lynas Rare Earths | Australia | Malaysia / USA | NdPr, heavy REEs | Operational, expanding |

| Pensana / Saltend | Angola | UK | NdPr | Development stage |

| Vital Metals | Canada | Canada | Mixed REEs | Early stage |

What distinguishes the Solvay-Viridis arrangement is the combination of a development-stage mining asset with an already-operational, high-capacity separation facility. The MP Materials model in the United States is entirely vertically integrated but geographically limited to North America. Lynas operates across two continents but relies on Malaysian processing infrastructure with ongoing political sensitivities. The Solvay-Viridis configuration, if it reaches commercial production, would represent the first functioning South America-to-Europe rare earth supply chain at scale.

The Commercial Structure: What the LOI Actually Establishes

A Letter of Intent in the mining and chemicals industries performs a specific commercial function. It establishes agreed principles without creating binding obligations, allowing both parties to progress technical and financial workstreams in parallel while the terms of a definitive agreement are negotiated.

The LOI between Solvay and Viridis covers:

- Offtake arrangements: The volume and pricing framework under which Solvay will purchase MREC from the Colossus project

- Technical package: Solvay's contribution of separation expertise and processing technology to support Colossus's development milestones

- Commercial principles: Quality specifications, delivery logistics, and pricing mechanism structures

- Development milestones: The agreed pathway toward commercial MREC production by 2028

The inclusion of a technical package is particularly noteworthy. It signals that Solvay's role in this arrangement extends beyond that of a passive off-taker. By contributing processing expertise to accelerate Colossus's development, Solvay is effectively co-investing in the supply chain architecture it needs to sustain La Rochelle's long-term throughput. This structure is broadly comparable to other examples of a rare earth offtake agreement where technical collaboration accompanies commercial terms.

Key Milestones and Decision Gates

| Milestone | Target Timing |

|---|---|

| LOI signed | June 2026 |

| Definitive sourcing agreement | H2 2026 (targeted) |

| Final investment decision | H2 2026 |

| Commercial MREC production (Colossus) | 2028 (targeted) |

Stakeholders should note that completion of the transaction remains subject to finalisation of definitive documents, applicable regulatory compliance, and standard commercial conditions. No assurance has been provided that the agreement will be completed or that its ultimate terms will mirror those outlined in the LOI.

The next major ASX story will hit our subscribers first

Risks That Warrant Careful Monitoring

The structural logic of the Solvay and Viridis rare earth supply agreement is compelling, however several risk dimensions deserve analytical attention:

Development execution risk is the most immediate. Converting a development-stage Brazilian rare earth project into commercial MREC production within approximately two years of a final investment decision is an aggressive timeline. Permitting, infrastructure construction, processing plant commissioning, and workforce development all carry execution uncertainty, particularly in a jurisdiction where rare earth project development precedents are limited.

Rare earth commodity price risk introduces a second layer of complexity. The rare earth market has historically been characterised by extreme price volatility, with NdPr oxide prices experiencing swings of more than 300% between market troughs and peaks within single commodity cycles. If Chinese supply expands aggressively or demand growth disappoints relative to current EV adoption forecasts, the economics underpinning the LOI could deteriorate before Colossus reaches production.

Financing risk for a junior developer like Viridis is structurally significant. Long-term offtake agreements with creditworthy counterparties like Solvay are a prerequisite for securing project finance from institutional lenders. The LOI creates the commercial foundation for this financing, but a non-binding instrument does not guarantee that definitive terms will be agreed or that capital markets will be receptive at the time of the final investment decision.

Investors and analysts should treat all forward-looking timelines and commercial projections associated with development-stage mineral projects as subject to material uncertainty. Past project development timelines in the rare earth sector have frequently extended beyond initial estimates.

The Structural Shift Behind the Headlines

The broader significance of the Solvay and Viridis rare earth supply agreement lies not in its individual commercial terms but in what it represents about how the rare earth industry is restructuring. For decades, the dominant procurement model for rare earth consumers outside China was effectively spot-market dependency on Chinese processed material. The concentration of separation capacity made bilateral supply agreements upstream of the processing stage largely unnecessary.

That model is now breaking down. European industrial policy, reflected in instruments like the EU Critical Raw Materials Act, is creating structural pressure on manufacturers and processors to demonstrate upstream supply chain resilience. Consequently, this pressure is translating into a wave of long-term bilateral supply agreements, strategic investments in non-Chinese processing infrastructure, and technical partnerships between established processors and development-stage miners.

The Solvay-Viridis LOI is a product of this structural shift. Its value extends beyond the specific volumes of MREC it might eventually deliver to La Rochelle. It establishes a commercial and technical template for how European rare earth processors can cultivate upstream supply from geopolitically diversified sources, contributing processing expertise in exchange for feedstock security.

For the rare earth sector as a whole, the proliferation of such agreements is a leading indicator of a supply chain architecture that is slowly, incrementally, but meaningfully rebalancing away from single-source dependency. Whether the Colossus project delivers on its 2028 target will be a closely watched data point for every participant in that rebalancing process.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths and more than 30 other commodities — turning complex data into clear, actionable investment insights. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial to position yourself ahead of the broader market.