May 13, 2026

The Invisible Infrastructure Behind Western Rare Earth Ambitions

The global transition to electrified transport and renewable energy generation shares a dependency that rarely makes headlines: the availability of separated rare earth oxides produced outside of China. For most of the past two decades, this dependency was treated as a tolerable risk, managed through procurement diversification at the concentrate level rather than the separated oxide stage. That tolerance has eroded sharply. Western manufacturers, defence contractors, and the financial institutions backing them have shifted from passive acceptance to active restructuring of where and how they source the magnetic materials at the heart of modern industrial technology.

This shift is not theoretical. It is being encoded into commercial agreements, buffer inventory programmes, and project financing structures that reward rare earth developers capable of demonstrating credible, bankable supply commitments across multiple end-use regions simultaneously. The Arafura Traxys North America offtake term sheet, announced on 13 May 2026, is a direct expression of this structural realignment in action, reflecting the growing urgency around rare earth supply chains.

When big ASX news breaks, our subscribers know first

Why NdPr and DyTb Oxides Are Not Interchangeable Commodities

Before examining the commercial architecture of the Arafura Traxys North America deal, it is worth understanding precisely why neodymium-praseodymium (NdPr) oxide and dysprosium-terbium (DyTb) oxide attract the level of strategic attention they do. These are not generic industrial inputs. They are performance-critical materials with no commercially viable substitutes at the production scales demanded by modern manufacturing.

NdPr oxide is the primary feedstock for neodymium-iron-boron (NdFeB) permanent magnets, the highest-performance magnet category available. These magnets are embedded in every traction motor powering a modern electric vehicle, in the direct-drive generators of offshore wind turbines, and in the servo motors controlling industrial robotics. Their power-to-weight ratio is so superior to alternative magnet technologies that replacing them would require fundamental redesigns across entire product categories.

DyTb oxide addresses a different but equally critical performance parameter: thermal stability. NdFeB magnets lose coercivity (their resistance to demagnetisation) as operating temperatures rise. In EV drivetrains, motors can reach temperatures at which an undoped magnet begins to degrade. Adding dysprosium or terbium to the magnet alloy suppresses this thermal degradation, preserving magnetic performance across the operating range. This is why DyTb is particularly indispensable for automotive, aerospace, and defence applications where thermal management is a design constraint rather than an option.

The combination of both NdPr and DyTb oxide supply within a single offtake framework is genuinely uncommon in Western supply agreements, most of which have historically addressed only one oxide stream. This structural feature distinguishes the Arafura approach from the majority of competing rare earth supply agreements currently in negotiation or execution across the sector.

Furthermore, what makes Western ex-China supply of DyTb especially acute is that heavy rare earth elements, including dysprosium and terbium, are far more geographically concentrated in their ore deposits than light rare earths. Most Australian and North American rare earth deposits are light rare earth dominant, meaning projects capable of delivering meaningful DyTb volumes are structurally rare within the non-Chinese development pipeline. These rare earth processing challenges are precisely why dual-stream agreements of this nature command significant market attention.

The Arafura Traxys North America Offtake Term Sheet: Core Commercial Terms

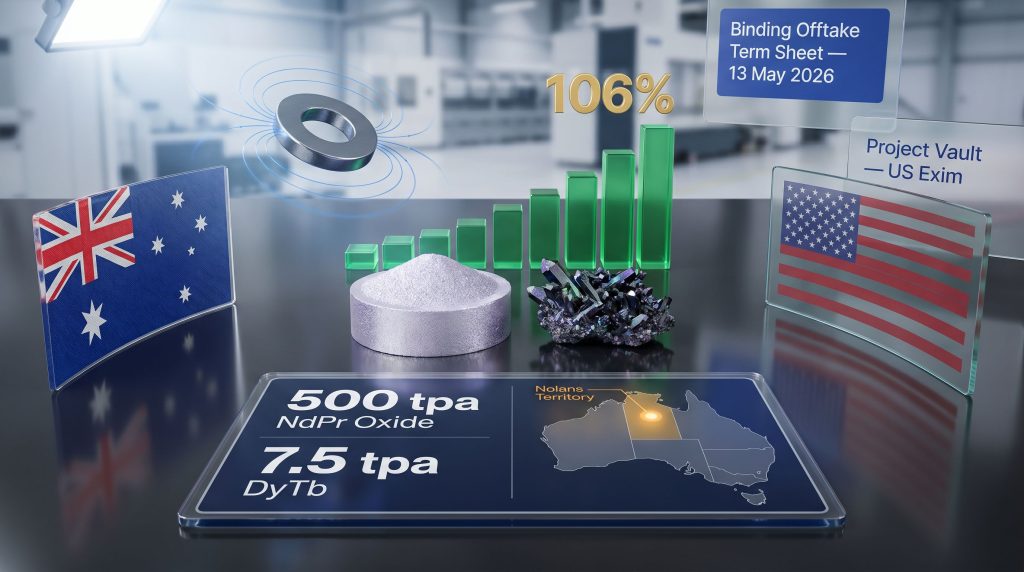

The binding offtake term sheet executed between Arafura Rare Earths and Traxys North America on 13 May 2026 establishes the foundational commercial parameters for a supply arrangement covering both NdPr and DyTb oxide streams from the Nolans project in Australia's Northern Territory. According to the official announcement on Listcorp, the key terms are as follows:

| Parameter | Detail |

|---|---|

| Agreement Type | Binding Offtake Term Sheet |

| Counterparty | Traxys North America |

| NdPr Oxide Volume | 500 tonnes per annum |

| DyTb Oxide Volume | 7.5 tonnes per annum |

| Initial Term | 5 years |

| Extension Option | 2 years by mutual agreement |

| Pricing Currency | US Dollars |

| Pricing Benchmark | Global seaborne index (Benchmark Minerals Intelligence or S&P Global Platts North America) |

| Long-Form Agreement Deadline | 6 months from term sheet execution |

| Announcement Date | 13 May 2026 |

How the Pricing Mechanism Serves Multiple Stakeholders

The decision to tie pricing to independently published global seaborne indices rather than bilaterally negotiated fixed prices is a deliberate structural choice with significant implications beyond the two parties to the agreement.

For debt providers and export credit agencies, index-linked pricing provides an auditable, transparent price discovery framework that can be stress-tested in financial models. Lenders evaluating project finance proposals for large-scale mining developments require confidence that offtake revenue projections are based on observable market data rather than opaque bilateral arrangements.

For buyers, index pricing provides protection against seller-side pricing leverage and ensures alignment with the prevailing market. For Arafura, it preserves exposure to upside in a rare earth oxide market that structural supply-demand analysis suggests will tighten as EV adoption curves steepen through the latter half of the 2020s.

The specific mention of both Benchmark Minerals Intelligence indices and S&P Global Platts North America pricing reflects the relative novelty of transparent seaborne pricing infrastructure for rare earths. Unlike base metals traded on the London Metal Exchange, rare earth oxide price discovery has historically been opaque and dominated by Chinese domestic reference prices. The emergence of credible Western seaborne indices represents an important maturation of the market infrastructure that makes large-scale project financing viable.

Project Vault: What It Is and Why It Matters

One of the most strategically significant features of the Traxys North America arrangement is the intended channelling of a portion of Arafura's oxide production into Project Vault, a programme managed by the US Export-Import Bank (Exim).

Project Vault functions as a tactical buffer inventory designed to insulate American manufacturers and defence contractors from sudden rare earth supply disruptions. The programme operates on the principle that maintaining strategic stockpiles of critical mineral inputs at accessible points within the supply chain reduces vulnerability to export restrictions, geopolitical shocks, or production disruptions affecting dominant supplying nations.

The involvement of a US government-managed buffer programme within a commercial offtake structure creates a layered demand framework:

- Baseline commercial demand from Traxys's downstream trading and distribution activities across North American manufacturing

- Buffer inventory demand from Project Vault's strategic accumulation objectives

- Potential defence-industrial demand as US procurement frameworks tighten sourcing requirements for rare earth inputs used in guided weapons systems, radar, and military vehicle drivetrains

It is important to note that while Traxys North America has indicated its intention to supply into Project Vault from Arafura's production, this does not constitute confirmed government backing or designated project support for Arafura's Nolans development specifically. The connection represents Traxys's downstream distribution strategy, not a direct Arafura-US government commercial relationship.

Comparing the Two Traxys Agreements: Europe Versus North America

The Traxys North America term sheet is structurally and commercially independent from the arrangement Arafura concluded with Traxys Europe in March 2025. Understanding the differences between these two agreements reveals the geographic and product-scope logic underpinning Arafura's offtake strategy. The earlier Traxys offtake agreement with the European arm established the framework that the North American arrangement has since extended and expanded.

| Feature | Traxys Europe (March 2025) | Traxys North America (May 2026) |

|---|---|---|

| Oxide Products Covered | NdPr oxide only | NdPr oxide + DyTb oxide |

| Annual Volume (NdPr) | Up to 300 tpa | 500 tpa |

| Annual Volume (DyTb) | Not included | 7.5 tpa |

| Target Market | European manufacturing | US manufacturing and strategic buffer |

| Project Vault Linkage | No | Yes (Traxys intention) |

| Contract Status | Signed definitive agreement | Binding term sheet (long-form within 6 months) |

The combined NdPr commitment across both agreements reaches 800 tonnes per annum, alongside 7.5 tonnes per annum of DyTb oxide exclusively for North America. This cumulative position represents a meaningful allocation within the non-Chinese supply segment, which remains significantly undersupplied relative to projected demand growth driven by accelerating EV penetration rates and expanding wind energy capacity across both regions.

The structural choice to engage the same parent trading group across two geographic markets through entirely separate commercial arrangements is notable. It suggests a coordinated distribution architecture rather than opportunistic trading, with Traxys acting as the primary Western distribution conduit for Nolans production across multiple target markets.

The Nolans Project: Why Vertical Integration Changes the Investment Thesis

Located in Australia's Northern Territory, the Nolans project is positioned as a vertically integrated rare earth operation, meaning it is designed to produce separated rare earth oxides rather than ore concentrates requiring third-party processing before they can be used by magnet manufacturers.

This distinction carries substantial commercial significance. A concentrate-only operation delivers an intermediate product that still requires hydrometallurgical processing to yield the separated oxides that magnet producers actually purchase. That additional processing step introduces supply chain complexity, additional cost, and additional geopolitical risk if the processing capacity is concentrated in a single jurisdiction.

By contrast, a project capable of delivering specification-grade separated NdPr and DyTb oxide directly to a trader like Traxys eliminates a critical vulnerability in the Western supply chain. It means that buyers in the US and Europe can source a production-ready input without depending on any intermediate processing step outside the project's own operational control.

Development Milestones and the Path to Final Investment Decision

The Arafura Traxys North America offtake term sheet explicitly supports the project's broader financing strategy. Arafura management has characterised advancing this agreement as achieving another milestone in delivering the company's long-term offtake and financing objectives in support of a future investment decision.

The sequencing of milestones from a project financing perspective follows a recognisable logic:

- Binding offtake agreements demonstrate committed revenue at projected production volumes

- Multiple regional counterparties signal geographic diversification of demand, reducing concentration risk

- Inclusion of strategic buffer programmes (Project Vault) adds an institutional demand layer beyond pure commercial trading

- Index-linked pricing provides lenders with transparent, auditable revenue modelling inputs

- Long-form agreement execution (targeted within 6 months of term sheet) converts preliminary commitments into definitive contractual obligations suitable for inclusion in debt financing packages

The next major ASX story will hit our subscribers first

What This Deal Signals for Western Rare Earth Supply Chain Architecture

Traxys as a Strategic Distribution Partner

Traxys operates as a global physical commodity trader with established downstream relationships across the rare earth processing and magnet manufacturing value chain. Its dual engagement across European and North American markets through separate Arafura agreements carries meaningful implications for how sophisticated market participants are positioning ahead of anticipated supply tightening.

For junior rare earth developers, securing a commercially sophisticated trader as an offtake counterparty has historically been one of the most persistent execution challenges. Traders with genuine downstream market access, credit standing, and institutional relationships can underwrite offtake commitments in a way that pure end-user agreements sometimes cannot, particularly in pre-production phases where project execution risk remains a buyer concern.

The involvement of a counterparty with the commercial sophistication and market access of Traxys materially reduces the offtake execution risk that has historically challenged developers at the pre-FID stage of rare earth project development.

Australia's Sovereign Risk Advantage in Rare Earth Supply

Australia occupies a structurally advantaged position in Western rare earth supply chain development for reasons that extend beyond geology. Its established mining regulatory framework, stable legal system, and deep trade relationships with both the United States and European Union create a preferred jurisdiction profile for Western end-users and financial institutions evaluating supply chain provenance.

The broader AUKUS security partnership and Five Eyes intelligence-sharing framework reinforce the geopolitical alignment that underpins commercial rare earth supply arrangements between Australian producers and Western buyers. Consequently, Australian-origin rare earth oxides carry an implicit sovereign risk profile that is distinctly different from supply sourced from jurisdictions with more complex geopolitical relationships with Western nations.

Investor Considerations: How to Read This Development

The Mechanics of Valuation Re-Rating for Pre-Production Miners

For development-stage companies like Arafura, the market's valuation typically embeds a discount reflecting execution uncertainty, offtake uncertainty, and financing uncertainty. Each incremental binding commitment that resolves one of these uncertainties tends to compress that discount, enabling valuation re-rating.

The sequence of catalysts relevant to investors monitoring this development includes:

- Long-form offtake agreement execution (targeted within 6 months of 13 May 2026)

- Progress toward and announcement of a Final Investment Decision for Nolans

- Securing of project finance facilities supported by the assembled offtake stack

- Construction commencement milestones

ARU shares rose 6.1% intraday to 35 cents following the announcement, against a prior close of 33 cents. This single-session movement occurred within a broader context of 106% year-on-year share price appreciation, suggesting that the market had been progressively re-rating Arafura's commercial positioning as its offtake portfolio assembled. As reported by Motley Fool Australia, this trajectory reflects growing investor confidence in Arafura's ability to convert commercial commitments into a funded project.

Key Risk Factors Investors Should Monitor

Disclaimer: The following represents an analysis of disclosed risk factors based on publicly available information. Nothing in this article constitutes financial advice. Investors should conduct independent due diligence and consult a licensed financial adviser before making investment decisions.

Investors evaluating Arafura's trajectory should weigh the following risk considerations against the commercial progress represented by the Traxys North America term sheet:

- FID dependency: The long-form agreement remains conditional on progress toward a positive Final Investment Decision. If FID is delayed, offtake obligations may not crystallise into binding delivery commitments within expected timeframes

- NdPr and DyTb price volatility: Index-linked pricing exposes both parties to commodity price cycles. Historical NdPr pricing has demonstrated significant volatility, with periods of sharp price elevation followed by correction

- Construction and commissioning timeline risk: Any extension of the pre-production timeline would affect the delivery schedule underpinning offtake commitments, potentially triggering renegotiation or penalty provisions in long-form agreements

- Project financing completion risk: Assembling a complete project financing package sufficient to fund Nolans construction requires more than offtake agreements. Equity commitments, debt facilities, and potentially export credit agency support must all be secured and coordinated

- Heavy rare earth supply assumptions: The 7.5 tpa DyTb commitment, while strategically significant, depends on Nolans achieving the heavy rare earth yields projected in feasibility studies. Geological variability in heavy rare earth distribution within ore bodies is a known risk factor for any project combining light and heavy rare earth production

The Broader Realignment: Where Nolans Fits in the Non-Chinese Supply Pipeline

The Arafura Traxys North America offtake term sheet is not an isolated commercial event. It reflects a structural realignment in how Western nations, their industrial bases, and the financial institutions servicing them are approaching the critical minerals challenge. The critical minerals demand surge across both the US and Europe has made securing credible, non-Chinese supply an institutional priority rather than a peripheral strategic consideration.

The post-pandemic period has accelerated a shift from passive acceptance of supply chain concentration to active co-investment in diversification. Export credit agencies, defence departments, and multilateral development banks have moved from bystander roles to active participants in qualifying supply projects through financing, offtake facilitation, and buffer inventory programmes. Project Vault is one visible expression of this shift within the US institutional framework.

For the rare earth sector specifically, this realignment is creating a bifurcated competitive landscape:

- Projects with multiple binding offtake agreements across geographically diversified Western markets are advancing toward project financing with institutional support

- Projects relying on memoranda of understanding or single-buyer arrangements are finding it increasingly difficult to assemble the credible offtake stacks that lenders require

The Arafura Traxys rare earth deal across both European and North American markets, covering both light and heavy rare earth oxide streams, positions it firmly within the first category. The six-month window to execute a long-form North American agreement, and the anticipated FID timeline beyond that, represent the near-term catalyst sequence that will determine whether this commercial positioning translates into funded construction.

The trajectory of Western rare earth supply chain development ultimately depends on whether projects like Nolans can navigate the gap between commercial commitment and operational production. The Arafura Traxys North America offtake term sheet represents a credible and commercially substantive step in that direction.

Want To Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — from rare earths to critical minerals — turning complex market announcements into actionable investment insights the moment they hit the exchange. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.