June 24, 2026

The Race to Build a Western Rare Earth Supply Chain Nobody Can Disrupt

For decades, the global rare earth permanent magnet industry operated as if geography were destiny. China's dominance across every stage of the value chain, from ore extraction through to finished neodymium-iron-boron magnets, was not accidental. It was the product of sustained industrial policy, patient capital deployment, and a willingness to operate at margins that discouraged Western competition. The result is a supply architecture so concentrated that a single export restriction decision in Beijing can send shockwaves through automotive assembly lines, defence procurement offices, and wind turbine manufacturing plants across three continents.

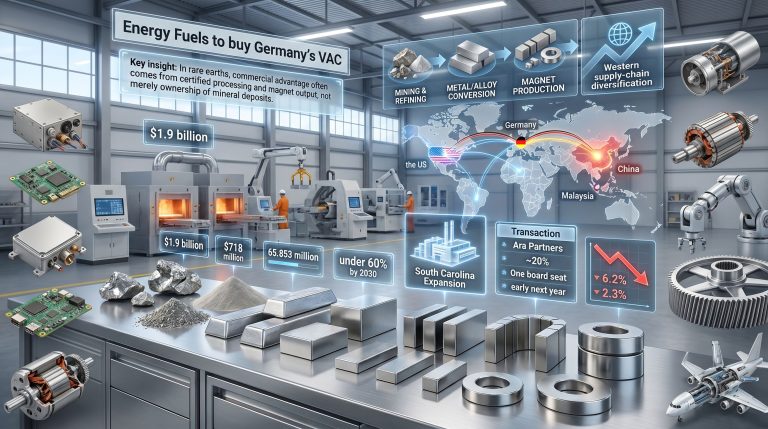

That structural vulnerability is now driving the most consequential wave of supply chain consolidation the Western critical minerals demand sector has ever seen. The Energy Fuels acquisition of VAC, Vacuumschmelze GmbH & Co. KG, announced in June 2026 for approximately $1.9 billion, represents the most complete attempt yet by a Western company to replicate China's integrated rare earth model on Western soil and under Western ownership.

When big ASX news breaks, our subscribers know first

Why Vertical Integration Is the Only Credible Western Response

Understanding why this deal matters requires understanding what makes the rare earth supply chain so difficult to replicate. Unlike most industrial supply chains, where individual nodes can be substituted or sourced independently, the rare earth-to-magnet pathway requires highly specialised capabilities at every stage that compound upon each other.

Producing neodymium-praseodymium oxide is not enough if you lack the metallurgical expertise to convert it into alloys. Producing alloys is not enough without the precision sintering and pressing capabilities needed to manufacture finished NdFeB magnets that meet automotive or defence specifications. Furthermore, manufacturing magnets is meaningless without the upstream feedstock certainty that prevents supply disruptions from undermining customer commitments.

China has spent more than three decades building these interlocking capabilities simultaneously. Western challengers attempting to replicate that system piecemeal, one node at a time, face not just a technical gap but a compounding integration deficit that grows at each stage.

The Energy Fuels acquisition of VAC is significant precisely because it closes that integration deficit in a single transaction, adding the one downstream capability the company was missing after years of methodical supply chain construction.

What VAC Brings to the Table: More Than Just a Magnet Factory

A Century of Proprietary Magnetics Knowledge

Founded in 1923 in Hanau, Germany, VAC is not a recently constructed greenfield facility racing to prove commercial viability. It is one of the oldest continuously operating advanced magnetics manufacturers in the world, carrying more than 400 patents across permanent magnet technology, soft magnetics, and specialty advanced materials. The company has been producing rare earth permanent magnets for more than 50 years, a depth of experience that genuinely cannot be shortcut by new entrants regardless of capital availability.

This institutional knowledge matters enormously in the NdFeB magnet sector. Magnet performance is not simply a function of raw material purity. It depends on precise control of microstructure during sintering, grain boundary engineering to optimise coercivity, and post-processing treatments that determine how a magnet responds to thermal cycling in real-world applications. These are rare earth processing challenges that are embedded in VAC's manufacturing protocols and workforce expertise, accumulated over generations.

VAC's U.S. Manufacturing Footprint and Scalability

VAC's North American subsidiary, eVAC Magnetics LLC, commenced production at its Sumter, South Carolina facility in 2025. This plant holds a significant distinction: it is currently the largest NdFeB permanent magnet facility of its scale operating in the United States.

| Facility Metric | Current State | Expansion Target |

|---|---|---|

| Annual NdFeB Capacity | 2,000 metric tonnes | 12,000 metric tonnes |

| Scale Multiplier | Baseline | 6x current capacity |

| Operational Status | Producing since 2025 | Phased expansion pathway |

The sixfold expansion pathway is particularly significant. Most Western magnet manufacturing announcements describe future capacity targets that require years of construction and permitting before any production begins. The Sumter facility is already producing, meaning expansion capital is deployed against proven infrastructure rather than greenfield risk.

VAC's Customer Base and Revenue Exposure

VAC serves more than 1,000 customers globally, with production facilities across North America, Europe, and Asia. The customer pipeline across target end markets represents over $2 billion in potential annual revenue.

| End Market | Strategic Relevance |

|---|---|

| Automotive (EV motors) | High-volume NdFeB demand anchor |

| Aerospace and Defence | Premium specifications, long-term contracts |

| Robotics and Automation | Rapidly expanding demand segment |

| Hyperscale Data Centres | Emerging high-performance magnet application |

| Semiconductors and Electronics | Precision magnetics requirements |

Transaction Structure: How the Deal Is Financed

Breaking Down the $1.9 Billion Consideration

The Energy Fuels acquisition of VAC is structured as a combination of cash and newly issued equity, with additional debt assumption forming part of the overall transaction value.

| Deal Component | Value or Detail |

|---|---|

| Total Implied Equity Value | ~$1.9 billion |

| Cash Payment | $718 million |

| Shares Issued | 65.853 million new Energy Fuels shares |

| Reference Share Price | $16.12 (June 22, 2026 closing) |

| VAC Adjusted Net Debt Assumed | ~$140 million (as of March 31, 2026) |

| Goldman Sachs Financing | $250 million term loan commitment |

| Seller | Ara Partners (private equity, industrial decarbonisation) |

| Expected Closing | Early 2027 |

Ara Partners, which acquired VAC in 2023, will not exit the story entirely after the transaction closes. The firm is expected to retain a 19.9% equity stake in Energy Fuels and will have the right to nominate one director to the Energy Fuels board, along with certain veto rights over an independent board nominee. VAC will operate as a wholly owned subsidiary while retaining its brand identity and its headquarters in Hanau, Germany.

The $250 million Goldman Sachs term loan provides the near-term liquidity bridge needed to fund the cash component of the acquisition while Energy Fuels continues advancing its other capital commitments. The involvement of Goldman Sachs at this scale signals institutional confidence in the combined entity's revenue prospects and asset quality.

How Energy Fuels Built Its Platform Before the VAC Deal

The "Middle-Out" Strategy: Starting Where Others Don't

One of the most analytically interesting aspects of Energy Fuels' supply chain construction is the sequence in which it was assembled. Rather than starting at the mine and working downstream, or starting at the magnet and working upstream, the company entered the value chain at its technical midpoint: processing and separation.

This approach was made possible by an asset that most pure-play rare earth developers lack. The White Mesa Mill in southeastern Utah, originally built as a uranium processing facility, provided the solvent extraction infrastructure, licensed facility status, and chemical processing expertise needed to handle rare earth feedstocks without starting from scratch. Converting an existing licensed processing facility to rare earth separation is a dramatically faster and lower-capital pathway than constructing a new hydrometallurgical plant from a blank site.

Monazite: The Feedstock Choice That Defines the Strategy

Energy Fuels' decision to anchor its rare earth business around monazite sand rather than conventional bastnäsite or ionic clay deposits reflects a sophisticated understanding of rare earth economics that deserves closer examination.

Monazite is a phosphate mineral that occurs as a byproduct of heavy mineral sand mining operations targeting titanium and zirconium. Because it is a co-product rather than a primary target, the cost structure for monazite feedstock supply can be significantly lower than ore mined specifically for its rare earth content. The Energy Fuels-Chemours partnership, established in 2021, exploits exactly this dynamic: monazite generated from Chemours' titanium and zirconium operations in Georgia and Florida is effectively an undervalued byproduct that Energy Fuels transforms into high-value separated rare earth oxides.

Critically, monazite tends to carry higher concentrations of heavy rare earth elements (HREEs), including terbium (Tb) and dysprosium (Dy), compared to many primary rare earth deposits dominated by light rare earths. This is not a minor distinction. Terbium and dysprosium are added to NdFeB magnets to enhance coercivity and heat resistance, enabling magnets to maintain performance at the elevated temperatures found inside electric vehicle motors, wind turbine generators, and defence guidance systems.

These elements are far scarcer than neodymium and praseodymium, trade at substantially higher prices per kilogram, and are subject to the tightest Chinese export controls. A supply chain with structural access to HREE-enriched feedstock is consequently building on fundamentally more defensible ground.

The scarcity of terbium and dysprosium in non-Chinese supply chains is arguably a greater long-term risk to Western magnet manufacturing than neodymium supply alone. Energy Fuels' monazite-anchored strategy directly addresses this often-overlooked vulnerability.

White Mesa Expansion: Adding Terbium and Dysprosium Separation

Energy Fuels initially focused White Mesa production on neodymium-praseodymium (NdPr) oxide, the primary rare earth input for NdFeB magnets. The company is now expanding its separation capabilities to include terbium and dysprosium, completing the full suite of magnet-critical rare earth outputs. When combined with the ASM metals conversion step and VAC's magnet manufacturing capabilities, this means the integrated platform will be capable of producing high-performance, high-temperature-grade NdFeB magnets without relying on any Chinese-controlled processing node.

Diversifying Feedstock Supply Beyond Chemours

The Chemours partnership anchors near-term feedstock supply, but Energy Fuels has built a diversified pipeline to support White Mesa's long-term throughput ambitions.

| Project | Location | Energy Fuels' Position |

|---|---|---|

| Donald Project | Victoria, Australia | Up to 49% JV interest with Astron Ltd. |

| Vara Mada Project | Madagascar | 100% owned |

| Bahia Project | Brazil | 100% owned |

This geographic diversification is strategically important. By sourcing monazite-rich feedstocks from multiple jurisdictions across different regulatory environments, Energy Fuels reduces the single-point-of-failure risk that has historically afflicted America's rare earth supply chain.

The ASM Acquisition: Filling the Metals and Alloys Gap

Why the Metals Conversion Step Is Frequently Underestimated

Between rare earth oxide production and permanent magnet manufacturing sits a conversion step that receives far less public attention than mining or magnet making: the production of rare earth metals and alloys. This stage involves reducing rare earth oxides to metallic form and then alloying them in precise ratios to create the neodymium-iron-boron feedstock from which magnets are pressed and sintered. It is a technically demanding process with significant energy requirements and very few non-Chinese practitioners at commercial scale.

In January 2026, Energy Fuels announced plans to acquire Australian Strategic Materials Ltd. (ASM) in a cash-and-shares transaction expected to close in early July 2026 subject to conditions. ASM's Korean Metals Plant is already operational, providing an immediate, revenue-generating metals conversion capability that bridges the gap between White Mesa's oxide output and VAC's magnet manufacturing input.

ASM's planned American Metals Plant would eventually add a fully domestic U.S. metals production node, further reducing the supply chain's geographic risk exposure.

Pentagon Financing: Context and Significance

Energy Fuels received a conditional commitment from the U.S. Office of Strategic Capital for a 20-year loan of up to $725 million to accelerate White Mesa Mill expansions and support construction of the proposed American Metals Plant. This commitment reflects the U.S. government's broader recognition that rare earth processing and conversion infrastructure represents a national defence priority, given the deep dependence of military systems on NdFeB permanent magnets for motors, actuators, guidance systems, and communications hardware.

It is important to note that this financing commitment is conditional and subject to further due diligence and documentation. Investors should not treat it as a finalised funding arrangement until all conditions have been formally satisfied.

The next major ASX story will hit our subscribers first

The Complete Mine-to-Magnet Architecture

How the Integrated Value Chain Functions

Upon completion of both the ASM and VAC acquisitions, Energy Fuels will have assembled a rare earth value chain spanning five distinct processing stages, each previously dependent on Chinese-controlled intermediaries for Western manufacturers.

Monazite Feedstock Sourcing

(Chemours / Donald / Vara Mada / Bahia)

↓

Rare Earth Processing and Separation

(White Mesa Mill, Utah)

↓

Metals and Alloys Conversion

(ASM Korean Metals Plant + planned American Metals Plant)

↓

NdFeB Permanent Magnet Manufacturing

(VAC Sumter SC + European facilities)

↓

End Markets: Automotive, Defense, Robotics,

Aerospace, Data Centers, Semiconductors

Comparing Western Mine-to-Magnet Strategies

| Company | Entry Point | Integration Direction | Stage Reached |

|---|---|---|---|

| Energy Fuels | Processing and Separation | Both upstream and downstream | Near-complete with VAC |

| MP Materials | Mining | Downstream toward magnets | Magnet production underway |

| USA Rare Earth | Magnet manufacturing | Upstream toward supply | $1.6B in federal funding secured |

Each approach carries different risk and reward profiles. MP Materials' upstream-first strategy delivers feedstock security but required years before downstream revenue materialised. USA Rare Earth's downstream-first approach built customer relationships early but depends on third-party oxide and metal supply in the interim. Energy Fuels' middle-out architecture is arguably the most complex to execute but offers the advantage of early revenue generation at the processing stage while expanding outward simultaneously.

Financial and Investment Risk Considerations

Market Reaction and Dilution Dynamics

Energy Fuels shares (ticker: UUUU) declined approximately 2.2% to 3.4% in premarket trading following the acquisition announcement. This reaction is consistent with investor caution when a company in an early-to-mid development stage commits to a transaction at a scale that substantially reshapes its balance sheet and operational complexity.

The issuance of 65.853 million new shares represents meaningful dilution for existing shareholders. Combined with the Goldman Sachs term loan and the conditional Pentagon financing, the company is carrying a substantial capital commitment load that will require disciplined execution across multiple simultaneous integration workstreams.

Key risk factors investors should monitor closely include:

- Integration complexity across different industries, cultures, and geographies, combining a uranium processing background with a century-old German precision manufacturing business

- Execution timeline risk, as both the ASM and VAC transactions must close and integrate before the supply chain functions as a unified system

- Rare earth price volatility, with NdPr and heavy rare earth prices subject to significant fluctuation based on Chinese production policy and global EV demand cycles

- Regulatory closing uncertainty, with foreign investment reviews required across Germany, Australia, and the United States adding timeline risk

- Capital intensity, given the simultaneous demands of the Goldman Sachs term loan service, conditional Pentagon loan conditions, and ongoing White Mesa expansion capital

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Past performance and announced transaction terms do not guarantee future outcomes. Investors should conduct independent due diligence before making investment decisions.

The Geopolitical Dimension: Why Western Governments Are Paying Attention

NdFeB Magnets as Defence-Critical Infrastructure

The urgency driving the Energy Fuels acquisition of VAC is not purely commercial. NdFeB permanent magnets are embedded in systems that underpin modern military capability: precision guidance actuators, electric drive motors for naval vessels, radar cooling systems, drone propulsion units, and communications hardware all rely on high-performance rare earth magnets that currently flow overwhelmingly from Chinese-controlled supply chains.

China's share of global NdFeB magnet production capacity has historically exceeded 85%, and the country has progressively tightened its export control framework around rare earth processing technologies and certain magnet-related materials. This creates an asymmetric vulnerability: Western nations have advanced manufacturing capabilities across aerospace, defence, and automotive sectors but remain structurally dependent on a single geopolitical competitor for a foundational input material.

The Energy Fuels and VAC combination, alongside parallel efforts by MP Materials and USA Rare Earth, represents the Western industrial response to this vulnerability. However, whether these initiatives collectively achieve sufficient scale and reliability to genuinely reduce that dependency within a commercially meaningful timeframe remains an open question, and one that investors in the sector should approach with calibrated rather than uncritical optimism.

Frequently Asked Questions

What is VAC and what does it produce?

VAC, formally Vacuumschmelze GmbH & Co. KG, is a German advanced magnetics manufacturer founded in 1923. The company produces NdFeB rare earth permanent magnets, soft magnetics, and specialty advanced materials. Its U.S. facility in Sumter, South Carolina currently produces up to 2,000 metric tonnes of NdFeB magnets annually, with an expansion pathway to 12,000 metric tonnes per year.

How much is Energy Fuels paying for VAC?

The total implied equity value is approximately $1.9 billion, comprising $718 million in cash and 65.853 million newly issued Energy Fuels shares, valued at $16.12 per share based on the June 22, 2026 closing price. Energy Fuels will also assume approximately $140 million of VAC's adjusted net debt.

Who is selling VAC?

VAC is being sold by Ara Partners, a private equity firm focused on industrial decarbonisation that acquired VAC in 2023. Following transaction close, Ara Partners is expected to hold a 19.9% stake in Energy Fuels.

When is the deal expected to close?

Subject to foreign investment reviews, antitrust clearances, and other regulatory conditions, the Energy Fuels acquisition of VAC is expected to close in early 2027.

What other acquisitions is Energy Fuels pursuing?

Energy Fuels is separately acquiring Australian Strategic Materials Ltd. (ASM) in a cash-and-shares transaction targeting a close in early July 2026. ASM provides the metals and alloys conversion capability that bridges White Mesa oxide production and VAC's magnet manufacturing.

For ongoing coverage of rare earth supply chain developments, critical minerals policy, and technology metals, Metal Tech News provides detailed reporting across the full spectrum of the sector.

Want to Know Which ASX Companies Are Building Exposure to the Critical Minerals Boom?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths, critical minerals, and beyond — turning complex data into actionable investment insights before the broader market catches on. Explore Discovery Alert's discoveries page to see how historic ASX discoveries have generated substantial returns, and begin your 14-day free trial to position yourself ahead of the next major find.