May 13, 2026

The Hidden Architecture of Critical Mineral Scarcity

Rare earth supply chains are routinely discussed in terms of volume, market share, and Chinese dominance. What receives far less attention is the compositional reality sitting beneath those headline figures: the operations that collectively supply the majority of the world's rare earths are, by and large, not supplying the rare earths that matter most to Western defence, aerospace, and advanced semiconductor manufacturing. The strategic importance of rare earths becomes clear when you consider that the elements commanding the highest prices, subject to active export controls, and embedded in the most strategically sensitive supply chains are precisely the ones missing from Western rare earth output.

Understanding why this gap exists, and why a rutile project in Malawi sits directly inside it, requires looking past production volume statistics and into the mineralogical fundamentals that shape what each operation actually produces.

When big ASX news breaks, our subscribers know first

Light Versus Heavy Rare Earths: Why the Distinction Changes Everything

Most rare earth production discussions conflate two categorically different markets. Light rare earths, including lanthanum and cerium, are abundant within major ore bodies, command relatively modest prices, and find their primary applications in catalysts and polishing compounds. Heavy rare earths, including dysprosium, terbium, and yttrium, occur at much lower concentrations in major deposits, command significantly higher prices, and underpin applications with direct defence and national security implications.

The pricing differential between these two categories is not incremental. European market pricing for terbium stands at approximately US$3.6 million per tonne, while dysprosium trades at approximately US$850,000 per tonne. These figures reflect scarcity, irreplaceability, and concentrated supply control simultaneously.

The end-use profile of heavy rare earths reinforces their strategic significance:

- Dysprosium and terbium are core components of high-temperature permanent magnets used in fighter aircraft, precision-guided weapons, and naval propulsion systems

- Yttrium is essential for thermal barrier coatings on aerospace turbine blades, where no functional substitute exists

- Yttrium also appears in radar and laser systems, next-generation semiconductor manufacturing, and alloy strengthening applications

- The United States currently imports 100% of its yttrium requirements, with no domestic commercial production pathway

Critically, all three elements — dysprosium, terbium, and yttrium — are subject to China's rare earth export restrictions introduced in April 2025. The strategic and commercial case for non-Chinese sources of these specific elements is not theoretical. It is an active market condition.

Why Chinese Supply Dominance Is More Absolute for Heavy Than Light Rare Earths

Chinese control over light rare earth supply is significant but not total. For heavy rare earths, dominance approaches comprehensive. The geological reality underpinning this is that heavy rare earth concentrations are not evenly distributed across rare earth deposit types. Ion adsorption clays in southern China, which are uniquely enriched in heavy rare earths, have historically been the primary global source of dysprosium, terbium, and yttrium. No comparable deposit type with equivalent heavy rare earth grades has reached commercial production outside China at meaningful scale.

This is not a regulatory or political phenomenon, though regulation and export controls amplify its effects. It is a mineralogical baseline that the world's largest non-Chinese rare earth operations were never designed to overcome. Furthermore, the rare earth geopolitical impact of this imbalance continues to reshape industrial policy across Western nations.

How Kasiya's Monazite Heavy Rare Earth Profile Compares to Global Operations

Against this backdrop, the compositional profile of Kasiya's monazite concentrate becomes analytically significant. Kasiya monazite heavy rare earths present at concentrations that have no equivalent in the current Western supply base.

The following table draws a direct comparison between Kasiya and the five largest global rare earth producing operations, which collectively account for more than 70% of global rare earth output:

| Operation | Location | Avg. DyTb (%) | Avg. Yttrium (%) | Avg. NdPr (%) |

|---|---|---|---|---|

| Mt Weld | Australia | ~0.4 | ~1.7 | ~19.4 |

| Mountain Pass | USA | 0.0 | 0.0 | High |

| Bayan Obo | China | Low | Low | Dominant |

| Weishan | China | Low | Low | Dominant |

| Maoniuping | China | Low | Low | Dominant |

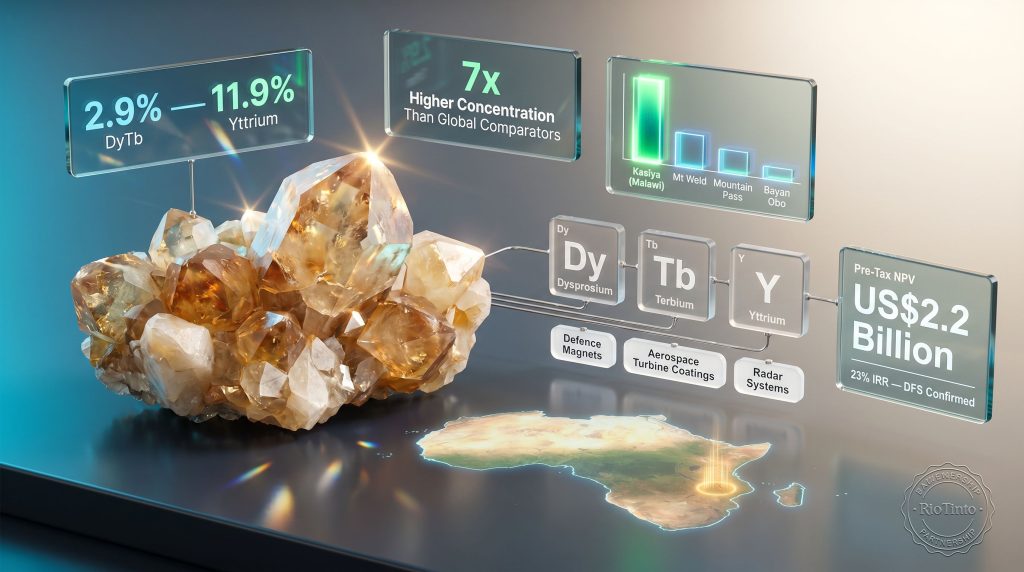

| Kasiya (monazite) | Malawi | 2.9% avg (up to 3.9%) | 11.9% avg (up to 17.3%) | 21.8% |

The numbers require context to be fully understood. Mountain Pass, operating within the United States and representing the country's primary domestic rare earth source, records 0.0% dysprosium-terbium and 0.0% yttrium. This is not a processing limitation or an economic decision. The ore body does not contain these elements at concentrations that make their recovery viable within the existing flowsheet. The gap between Mountain Pass and Kasiya is therefore not a matter of degree. It is categorical.

Kasiya's monazite averages 2.9% combined dysprosium-terbium, reaching up to 3.9% in higher-grade zones, and 11.9% yttrium, reaching up to 17.3%. Relative to the five-operation average of 0.4% DyTb and 1.7% yttrium, these figures represent approximately a 7x concentration advantage across both element groups.

The neodymium-praseodymium (NdPr) content of 21.8% is broadly in line with the global comparator average of approximately 19.4%. What makes this significant is the bundling: where competing operations deliver NdPr without meaningful heavy rare earth content, Kasiya's monazite delivers NdPr alongside heavy rare earth concentrations that have no current equivalent in the Western supply base.

Monazite Recovery at Kasiya: Turning Process Waste Into a Strategic Product

Understanding the cost structure of Kasiya's monazite stream requires understanding its position within the existing processing flowsheet. Monazite is not extracted through a dedicated rare earth circuit. It is recovered from material the primary rutile processing circuit already treats as waste.

The recovery sequence operates as follows:

- Heavy mineral gravity concentrate is produced within the existing rutile processing circuit

- Electrostatic separation isolates the conductor fraction, which is rutile, and generates a non-conductor tailings stream

- That non-conductor tailings stream, which would ordinarily be discarded, is subjected to additional gravity separation

- Magnetic separation follows, yielding monazite concentrate as the output product

- No parallel rare earth circuit is constructed, and no dedicated capital is required for the monazite stream

The consequence of this architecture is a near-zero incremental cost structure for monazite production. Conventional rare earth miners bear the full cost of ore extraction, comminution, and parallel rare earth processing circuits. Kasiya's monazite production carries none of those costs. The capital and operating expenditure that supports the near-zero incremental cost figure is the primary rutile circuit, which already exists in the project design regardless of whether monazite is recovered.

Key Context: The near-zero incremental cost is a function of flowsheet architecture, not an approximation or a target. It derives directly from the fact that monazite production adds no primary processing load to a circuit already designed and costed for rutile recovery. This structural advantage has no direct equivalent among primary rare earth developers.

What remains to be determined through the ongoing evaluation programme includes:

- Detailed mineralogical characterisation of the monazite concentrate at commercial scale

- Recovery rate assessment at the proposed throughput levels

- Formal economic evaluation of the by-product stream's financial contribution

Preliminary laboratory recovery at Sovereign's Lilongwe facility has confirmed both mineral presence and separability. The transition from laboratory confirmation to a fully quantified commercial by-product stream requires completing these three workstreams. Mining Technology's coverage of the Kasiya project provides further detail on the technical development pathway.

The Saprolite Mineralisation Advantage and Its Connection to Cost

Kasiya's ore body is hosted in soft saprolite, a deeply weathered geological material that requires no drilling, blasting, crushing, or milling. This free-dig extraction architecture is unusual at the scale Kasiya operates and directly supports the DFS-published operating cost of US$450 per tonne of product FOB Nacala. The saprolite host also means that the material entering the processing circuit is already in a suitable physical state for gravity and electrostatic separation, which is the same material from which monazite is subsequently recovered. The geological characteristics that lower primary rutile extraction costs thus also lower the effective cost of generating the non-conductor tailings stream from which monazite is isolated.

Kasiya's Baseline Economics: The DFS Foundation Before Monazite

The economic foundation for Kasiya exists entirely independently of its monazite potential. The DFS-confirmed metrics cover primary rutile and graphite production only:

| Metric | Value |

|---|---|

| Pre-Tax NPV (8% discount rate) | US$2.2 billion |

| Pre-Tax IRR | 23% |

| Capital to First Production | US$727 million |

| Total Life-of-Mine Development Capital | US$1,239 million |

| Sustaining Capital | US$431 million |

| Operating Cost | US$450/tonne of product (FOB Nacala) |

| Steady-State Throughput | 24 million tonnes per annum |

| Annual Rutile Production (steady-state) | 222,000 tonnes |

| Annual Graphite Production (steady-state) | 275,000 tonnes |

| Life of Mine | 25 years (initial) |

| Total Resource | 2.1 billion tonnes |

The project develops in two phases. Phase 1 operates at 12 million tonnes per annum throughput across Years 1 to 4. Phase 2 scales to 24 million tonnes per annum from Year 5 onwards. Sovereign Metals (ASX: SVM | AIM: SVML | OTCQX: SVMLF) carries Rio Tinto as a 19.9% strategic investor, with non-binding memoranda of understanding in place with Mitsui & Co. for rutile offtake and Traxys North America for graphite.

Critical Distinction for Investors: The published US$2.2 billion pre-tax NPV8% and 23% pre-tax IRR include no monazite revenue, no by-product credit from the rare earth stream, and no associated cost allocation. Any economic contribution established through the ongoing evaluation programme represents value that is additive to, not embedded within, the current published valuation baseline.

How China's Export Controls Created an Active Market Condition

The demand environment that Kasiya's monazite stream would enter did not exist two years ago. It was created in April 2025, when China introduced export controls specifically targeting dysprosium, terbium, and yttrium. These three elements are precisely those in which Kasiya monazite heavy rare earths are most concentrated, at approximately 7x the global comparator average.

The timeline of escalating restrictions is instructive:

| Date | Action | Market Effect |

|---|---|---|

| April 2025 | China introduces export controls on dysprosium, terbium, and yttrium | Supply disruption begins across Western and Japanese manufacturing sectors |

| January 6, 2026 | Controls tightened specifically against Japan | Acute shortages concentrated on the largest non-Chinese heavy rare earth consumer |

Japan's exposure illustrates the structural depth of this dependency. Despite more than 15 years of active supply diversification efforts following the 2010 supply shock, Japan remains approximately 60% dependent on Chinese rare earth imports overall, with dependency approaching 100% for heavy rare earths specifically. The January 2026 tightening targeted the market with the least viable diversification pathway.

The United States carries a parallel vulnerability. With 100% of yttrium requirements met through imports and no domestic commercial production pathway, the US faces a measurable and immediate supply security gap for a mineral embedded throughout its defence and semiconductor manufacturing base.

What distinguishes the current market condition from prior rare earth supply anxieties is that the controls are operational, the shortages are active, and the consuming nations most affected have not yet identified alternative supply sources at commercially relevant scale. The demand case for Kasiya's monazite heavy rare earth stream is therefore not a forecast about future policy scenarios. It describes conditions that exist today.

The next major ASX story will hit our subscribers first

What Three Workstreams Will Determine About Kasiya Monazite's Commercial Value

The monazite evaluation programme underway at Kasiya will resolve three open variables that separate the confirmed compositional advantage from a formally quantified commercial contribution:

- Volume recoverable at commercial scale: Laboratory recovery at Sovereign's Lilongwe facility has confirmed separability, but scaled recovery rates at 24 million tonnes per annum throughput remain under assessment

- Economic value attributable to that volume: Formal economic evaluation of the by-product stream is pending and will establish the revenue contribution against current and forward market pricing for dysprosium, terbium, and yttrium

- Flowsheet integration outcomes at full throughput: Detailed mineralogical characterisation will determine how the monazite stream performs within the primary circuit at commercial operating conditions

What is already determined and not subject to revision includes the near-zero incremental cost structure, the compositional profile showing 2.9% DyTb and 11.9% yttrium averages, and the DFS baseline economics of US$2.2 billion NPV8% against which any monazite contribution would be incremental.

At European market pricing of approximately US$850,000 per tonne for dysprosium and US$3.6 million per tonne for terbium, even modest annual monazite production volumes at Kasiya's confirmed compositional grade would represent material incremental value relative to the current DFS baseline. The evaluation programme's function is to convert that theoretical observation into a formally quantified number. For broader context on how this fits within the energy transition, the critical minerals demand narrative continues to accelerate across Western industrial policy.

Kasiya's Position in the Western Critical Mineral Supply Architecture

Kasiya sits at a confluence of factors that are independently significant but collectively unusual. The project offers:

- A DFS-confirmed economic foundation worth US$2.2 billion pre-tax NPV8% from primary production alone

- A by-product monazite stream recoverable at near-zero incremental cost from an existing processing circuit

- Heavy rare earth concentrations approximately 7x the global comparator average across dysprosium-terbium and yttrium

- A supply offering for three elements simultaneously subject to active Chinese export controls

- A Malawian jurisdiction that sits outside the geopolitical risk profile of Chinese, Russian, and other constrained supply sources

Western industrial policy frameworks, including the US Inflation Reduction Act and the European Critical Raw Materials Act, prioritise supply chain diversification toward politically stable, non-adversarial source jurisdictions. The critical raw materials for the green transition framework further underscores why a Malawian source of heavy rare earths at Kasiya's compositional grade would represent a structurally meaningful addition to the non-Chinese supply base. No claim is made here that these frameworks constitute project-specific support or that any government funding, designation, or accelerated permitting has been confirmed for Kasiya.

The monazite evaluation programme remains in progress, its commercial conclusions pending. However, the market conditions it is being evaluated against — including active Chinese export controls, near-total Japanese heavy rare earth import dependency, and 100% US yttrium import reliance — are not assumptions or projections. They are the present operating environment into which Kasiya's third mineral stream, if commercially confirmed, would deliver product. Crux Investor's analysis of Kasiya's monazite recovery offers additional perspective on the value layer sitting outside the current DFS.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Investors should conduct their own due diligence. Forecasts, projections, and forward-looking statements involve inherent uncertainty and may not reflect actual outcomes.

Want to Stay Ahead of the Next Major Critical Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors. Explore why major mineral discoveries can generate exceptional returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.