June 9, 2026

The Rare Earth Supply Crisis That Makes North American Deposits Worth Examining Carefully

The global rare earth industry operates under a structural imbalance that has persisted for decades and is now intensifying rather than resolving. A single country controls the overwhelming majority of both mining output and processing capacity, leaving Western manufacturers of electric vehicles, wind turbines, and defence systems exposed to supply chain risks they cannot easily hedge. For investors tracking the critical rare earth supply chain, this backdrop creates a specific analytical lens through which development-stage projects must be evaluated: not just on their geological merits, but on whether they can realistically bridge the gap between resource in the ground and product in a separation facility.

Against this framework, the updated Preliminary Economic Assessment (PEA) released by Mont Royal Resources (ASX:MRZ) for its Ashram Rare Earths and Fluorspar Project in Nunavik, Québec represents a meaningful data point. The question is not simply whether the numbers look attractive. The more useful question is what the numbers actually unlock in terms of strategic conversations, funding pathways, and the probability of a development timeline that doesn't quietly stall between study phases.

When big ASX news breaks, our subscribers know first

Why Ashram Sits at the Intersection of Geology and Geopolitics

The North American Rare Earth Supply Gap

China accounted for approximately 77% of global rare earth mine production and roughly 90% of global separation capacity as of 2025, according to industry estimates. That concentration creates a structural vulnerability that Western governments have been attempting to address through both policy and direct capital deployment. Furthermore, the challenge is that building a competing supply chain requires more than intent. It requires deposits of sufficient scale, in jurisdictions with credible permitting regimes, and with mineralogy that can actually be processed economically.

North America's development pipeline for rare earths remains thin relative to the demand projections being driven by EV adoption curves, offshore and onshore wind buildout, and defence procurement modernisation. In addition, most projects in the pipeline face one or more disqualifying constraints: insufficient grade, complex mineralogy, remote location without infrastructure, or high-sovereign-risk jurisdictions. The rare earth geopolitical risks inherent in this landscape make jurisdictional credibility a critical differentiator for any development-stage project.

What Makes the Ashram Deposit Structurally Different

The Ashram deposit addresses several of those constraints simultaneously, which is why it warrants closer examination than many of its peer projects.

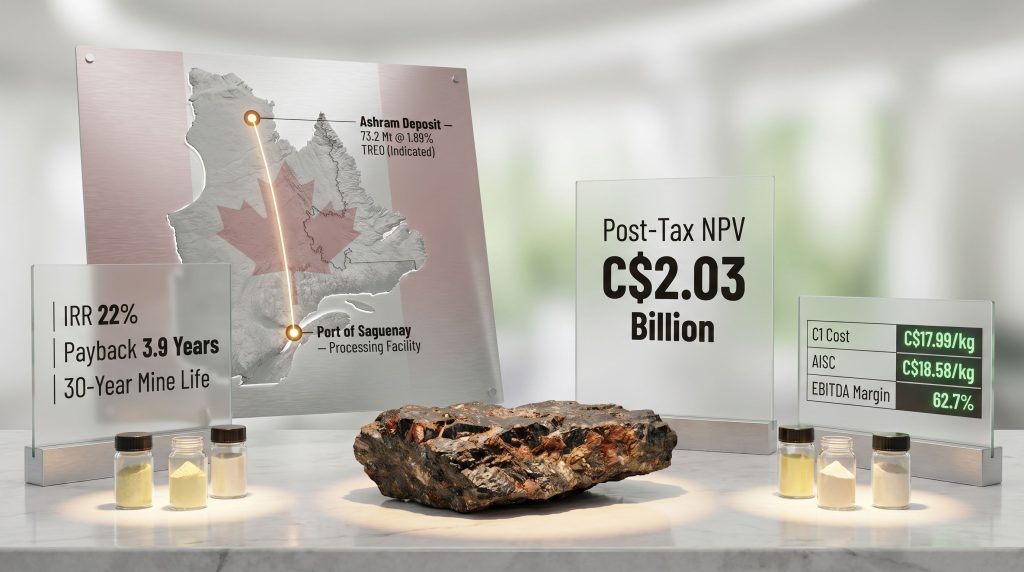

- Scale: Classified as one of North America's largest monazite-hosted rare earth deposits, with an updated April 2024 mineral resource estimate of 73.2 Mt at 1.89% TREO and 6.6% CaF₂ (Indicated) plus 131.1 Mt at 1.91% TREO and 4.0% CaF₂ (Inferred)

- Mineralogy: Monazite is a rare earth phosphate mineral with well-understood processing chemistry, meaning it responds to established separation flowsheets without requiring novel or unproven metallurgical techniques

- By-product potential: The co-occurrence of fluorspar (calcium fluoride, CaF₂) at grades exceeding 6% in the Indicated resource introduces a potential secondary revenue stream that most rare earth deposits simply do not carry

- Jurisdiction: Nunavik, Québec sits within a Tier-1 mining jurisdiction with transparent permitting processes and direct access to Hydro-Québec's low-cost electricity network

- Infrastructure leverage: The revised project configuration routes processing through the Port of Saguenay, utilising existing deep-water export infrastructure rather than requiring purpose-built port construction

One detail that is underappreciated in most coverage of monazite-hosted deposits is that the processing chemistry, while well-established, involves handling thorium and uranium as minor by-products of the rare earth extraction process. This radioactive by-product management requirement adds a regulatory dimension to permitting that does not apply to ionic clay or carbonatite-hosted deposits. Québec's regulatory framework accommodates this; however, it is a variable that separates monazite projects from simpler deposit types in terms of permitting complexity.

The Mont Royal Resources Ashram PEA: What the Numbers Actually Say

Core Economic Parameters

The updated Mont Royal Resources Ashram PEA delivers a return profile that clears the threshold for serious strategic partner engagement. The headline metrics are presented below:

| Metric | Value |

|---|---|

| Post-Tax NPV (8% discount rate) | C$2.03 billion |

| Post-Tax IRR | 22% |

| Mine Life | 30 years |

| Average Annual REO Production | 17,466 tonnes |

| Annual NdPr Output | ~4,035 tonnes |

| Initial Capital Expenditure | C$1.23 billion |

| Total Life-of-Mine Capital | C$1.6 billion |

| Payback Period | 3.9 years |

| Life-of-Mine EBITDA Margin | 62.7% |

| C1 Cash Cost per kg Saleable REO | C$17.99 |

| AISC per kg Saleable REO | C$18.58 |

| Strip Ratio | 0.4:1 |

| Refundable Canadian Tax Credits | ~C$342 million |

A 22% post-tax IRR on a 30-year asset with a sub-4-year payback period is a return profile that institutional investors and strategic partners evaluate seriously. The 62.7% EBITDA margin is underpinned by two structural cost advantages: a low strip ratio of 0.4:1, which means very little waste rock needs to be moved per tonne of ore processed, and monazite mineralogy that responds efficiently to established processing flowsheets.

The Configuration Changes That Made These Numbers Possible

The revised economics did not emerge from improved commodity price assumptions alone. Two structural decisions fundamentally changed the project's capital intensity:

- Processing facility relocation: Moving the plant to the Port of Saguenay eliminated the need for an integrated remote processing complex, dramatically reducing both construction complexity and ongoing logistics costs

- Southern access road adoption: The new corridor replaced a more capital-intensive northern logistics solution that had burdened earlier study iterations

These configuration changes are reported to have reduced projected capital intensity by more than half compared to earlier studies. Consequently, this is a critical point for understanding why the current PEA represents a genuine step-change rather than an incremental update. The project being evaluated today is architecturally different from the one that produced prior cost estimates.

Analytical Note: When comparing historical PEA estimates to the current study, investors should treat them as different projects. The relocation of the processing facility and the southern access road together define a new economic architecture, not merely revised input assumptions applied to the same design.

Resource Quality and Mine Schedule Confidence

The current 30-year mine plan uses approximately 25% of the total global resource base, with a critically important quality metric: 93% of the scheduled mine tonnes sit in the Indicated resource category rather than Inferred. This distinction matters considerably more than it might appear to non-technical investors.

In Canada's NI 43-101 classification system (which governs how mineral resources are categorised and reported), Indicated resources have been defined with sufficient geological confidence to support feasibility-level studies. Inferred resources carry considerably higher uncertainty. A mine schedule built predominantly on Indicated tonnes reduces the geological risk embedded in the economic model and is a prerequisite for government funding applications and serious offtake negotiations.

NdPr: Why the Product Mix Defines Ashram's Strategic Positioning

The Magnet Rare Earths Demand Architecture

Not all rare earth oxides carry equal commercial or strategic weight. The product category that Western buyers are most urgently seeking outside of Chinese supply chains is NdPr, or neodymium-praseodymium oxide. This is the primary feedstock for neodymium-iron-boron (NdFeB) permanent magnets, which are essential components in:

- EV traction motors, where magnet performance directly affects range and efficiency

- Direct-drive wind turbine generators, which avoid gearboxes entirely by using high-field permanent magnets

- Military guidance, propulsion, and actuation systems across air, land, and naval platforms

The critical minerals demand surge driven by these sectors is reshaping how governments and manufacturers think about supply security. Ashram's base case projects annual NdPr output of approximately 4,035 tonnes, a volume directly relevant to Western magnet supply chain ambitions at industrial scale. A new North American source producing over 4,000 tonnes of NdPr annually would represent a material addition to Western supply.

The product mix also includes terbium (Tb) and dysprosium (Dy), the heavy rare earths used to enhance the high-temperature performance of NdFeB magnets. These elements command significant price premiums over light rare earths and are even more concentrated in Chinese supply chains than NdPr. Their presence in Ashram's projected output adds a layer of strategic value that basket price calculations may understate.

Cost Competitiveness Against Non-Chinese Peers

C1 cash costs of C$17.99/kg and AISC of C$18.58/kg of saleable REO position Ashram competitively within the global non-Chinese developer cohort. The low strip ratio and favourable mineralogy structurally underpin these estimates rather than relying on aggressive throughput or recovery assumptions.

Sensitivity analysis in the PEA reportedly demonstrates project profitability is preserved under downside REO basket price scenarios. This is an important credibility marker: a project whose economics collapse under moderate price stress cannot attract the long-duration capital that a 30-year mine requires. The rare earth processing challenges facing many peer projects, by contrast, introduce cost uncertainties that make comparable margin projections far less reliable.

Three Capital Pathways and the Probability Framework

Scenario 1: Canadian Tax Credits as Non-Dilutive Capital

The C$342 million in refundable Clean Technology Manufacturing Investment Tax Credits is a structural feature of the Ashram economics that deserves careful attention. Unlike speculative government grants, these credits are codified in Canadian federal tax law as refundable instruments. This means they are recoverable regardless of the project's taxable income position in early operating years, providing genuine non-dilutive capital that directly reduces the effective upfront cost of the project.

For a development-stage company, the difference between a discretionary grant and a codified refundable tax credit is substantial. Grants require political alignment, application approval, and ongoing compliance. Refundable tax credits, however, are structurally guaranteed once the qualifying expenditure is incurred.

Scenario 2: Strategic Partner or Joint Venture Structure

The C$1.23 billion initial capex requirement substantially exceeds what a small-cap ASX-listed developer can raise through equity markets without severe dilution. This mathematical reality makes strategic partnership not a preference but a necessity if the project is to advance on an acceptable timeline for existing shareholders.

The most structurally efficient pathways include:

- Offtake-linked project financing: A committed downstream buyer provides debt or equity capital in exchange for long-term supply agreements at predetermined pricing. This aligns the interests of capital provider and project developer while reducing demand risk for the lender

- Joint venture with a major mining company: A partner with a strong balance sheet and rare earth processing interest takes an equity position in the project in exchange for contributing capital toward the PFS and development costs

- National strategic reserve or procurement body: Government-adjacent entities in North America, Europe, or Japan that have mandates to secure rare earth supply outside Chinese control could structure long-dated offtake arrangements that serve as the foundation for project financing

Scenario 3: Equity Markets as a Last Resort

Returning to equity markets at scale before strategic capital is secured carries significant dilution risk given the gap between current market capitalisation and project requirements. The PEA's most important function in the current phase is to establish a defensible negotiating floor, giving management a credible valuation reference when engaging institutional investors or offtake counterparties.

Strategic Warning: The historical pattern in rare earth development is instructive. Most projects do not fail at the geological study stage. They stall at the transition from PEA to funded PFS, when the capital requirement becomes concrete but strategic commitments have not yet materialised. The 12 to 18 months following PEA release is the critical window.

Resource Optionality Beyond the Base Case

Upside Levers Deliberately Excluded From the Current Study

The current PEA is deliberately conservative in its resource utilisation. Several value levers were excluded from the base case, each of which could improve project economics in subsequent studies:

- Fluorspar recovery circuit: Additional metallurgical testing is underway to assess whether a dedicated fluorspar processing stream can be incorporated into future feasibility work. With CaF₂ grades of 6.6% in the Indicated resource, a by-product credit from fluorspar could meaningfully shift the project's cost position

- BD-Zone higher-grade material: A higher-grade zone was deliberately excluded from the current resource model, preserving it as an optionality lever for subsequent studies where grade-blending strategies could improve mill feed quality

- Mallard satellite target: An adjacent exploration target that could extend the resource envelope or support a standalone satellite development scenario

- Resource scale: The 30-year mine plan draws on approximately one quarter of total mineral resources, meaning production rates or mine life could be extended without new discovery

The fluorspar angle is particularly worth monitoring. Fluorspar (CaF₂) is itself a critical mineral used in the production of hydrofluoric acid, which is essential for lithium battery electrolyte manufacturing, semiconductor etching, and aluminium smelting. Furthermore, a project that produces both rare earth carbonate and fluorspar is serving two critical mineral demand categories simultaneously, which could be relevant to the structure of any government funding application.

The next major ASX story will hit our subscribers first

Development Timeline and Key Investor Milestones

From PEA to PFS: The Critical Path

| Milestone | Status / Target |

|---|---|

| Updated Mineral Resource Estimate | Completed April 2024 |

| Updated PEA Delivery | Completed 2026 |

| PFS Commencement | Targeted H2 2026 |

| Strategic Partner / Offtake Engagement | Ongoing, no commitments disclosed |

| Government Funding Application | Enabled by PEA completion |

| Permitting (Québec Tier-1 Regime) | Pre-application stage |

The PFS is the document that converts PEA-level interest into binding capital commitments. Government funding bodies and institutional offtake partners do not make financing decisions on the basis of PEA studies. The PFS will need to validate the revised processing plant location at Port of Saguenay, the southern access road configuration, the fluorspar circuit economics, and the project's social licence framework with Nunavik's Indigenous communities before development financing can be structured.

Any delay in PFS commencement beyond H2 2026 extends the timeline to a Final Investment Decision and increases the probability that Mont Royal must return to equity markets before strategic capital is in place. The rare earth market breakthrough potential of projects like Ashram ultimately depends on executing these transitional milestones within competitive timeframes.

Québec's Jurisdiction Advantage: More Than a Location Choice

Why the Mining and Infrastructure Environment Matters for Cost Economics

The choice of Québec as a project location carries structural cost implications that go beyond permitting predictability. Hydro-Québec provides electricity at some of the lowest industrial rates in North America, derived from the province's extensive hydroelectric generation capacity. For rare earth processing operations, which are energy-intensive by nature, this translates directly into operating cost advantages that competitors in other jurisdictions cannot replicate.

The Port of Saguenay infrastructure removes a capital burden that has undermined the economics of other remote rare earth projects. Deep-water port access for product export is a fixed cost that scales poorly for a single project to absorb. Leveraging existing infrastructure converts what would have been a capital cost into an operating cost, consequently improving the project's NPV at any given discount rate.

Québec's mining permitting regime is one of the most established in North America, with defined process timelines and a regulatory framework that has been tested across multiple large-scale mine developments. This reduces sovereign and regulatory risk relative to projects in jurisdictions where permitting outcomes are less predictable.

Frequently Asked Questions: Mont Royal Resources Ashram PEA

What does the Ashram PEA NPV of C$2.03 billion mean for investors?

The post-tax NPV of C$2.03 billion at an 8% discount rate represents the present value of projected future cash flows from the 30-year operation, after taxes and time-value-of-money adjustments. It establishes a valuation reference point for strategic partner negotiations and government funding discussions. It does not represent the current market value of Mont Royal Resources, and investors should treat it as a negotiating anchor rather than a market price.

What is the difference between a PEA and a Prefeasibility Study?

A PEA (Preliminary Economic Assessment) uses a combination of Indicated and Inferred mineral resources to outline early-stage project viability. A PFS (Prefeasibility Study) applies a higher standard of engineering accuracy, relies predominantly on Indicated resources, and is required before binding financing or offtake commitments can typically be secured from institutional counterparties.

Why does the C$342 million in Canadian tax credits matter structurally?

These credits are refundable instruments codified in Canadian federal tax law, meaning they are recoverable regardless of the project's taxable income position. Unlike discretionary grants, they do not require ongoing political approval after the qualifying expenditure is confirmed. This makes them a more reliable component of the capital structure than project-specific government support.

What is NdPr and why does it define Ashram's commercial value?

NdPr is neodymium-praseodymium oxide, the primary input for NdFeB permanent magnets used in EV motors, wind turbine generators, and defence systems. It commands a significant price premium over other rare earth oxides and is the product category most actively sought by Western buyers seeking supply diversification away from Chinese sources.

When is the Ashram PFS expected to begin?

Management has indicated PFS commencement is targeted for the second half of 2026. The study will incorporate the revised processing plant location at Port of Saguenay, the southern access road configuration, and potentially a fluorspar recovery circuit. For further detail on project milestones and investor communications, Mont Royal's investor news provides regularly updated announcements.

Key Risk Factors That Investors Should Monitor

Understanding the Mont Royal Resources Ashram PEA in full requires mapping the risks alongside the opportunities. The following represent the variables most likely to determine investor outcomes over the next 24 months:

- Capital gap risk: The distance between current market capitalisation and C$1.23 billion in initial capex is the single largest structural constraint. Without a named strategic partner or committed government funding, the project cannot advance to construction on a timeline that avoids material equity dilution

- REO price sensitivity: Rare earth basket prices are subject to significant volatility driven by Chinese export policy, demand fluctuations, and periodic oversupply cycles. Downside price scenarios could compress the 22% IRR toward or below hurdle rates for strategic investors

- Timeline execution risk: The PEA delivery timeline shifted from the originally targeted Q1 2026 to a later 2026 completion, indicating that execution risk exists in the study schedule. Similar delays in PFS delivery would extend the critical funding conversation window

- Permitting and community engagement: Nunavik's remote location and the requirements for meaningful engagement with Indigenous communities introduce timeline variables that are difficult to model precisely at the PEA stage

- Monazite radioactive by-product management: The thorium and uranium content in monazite processing introduces a regulatory dimension that adds complexity to permitting relative to simpler deposit types, even within a well-established jurisdiction like Québec

For investors seeking deeper context on how Ashram compares to other rare earth development projects in Canada, Proactive Investors' coverage of Mont Royal's advancing strategy offers useful third-party perspective on the project's positioning.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Projections, NPV estimates, IRR figures, and timeline targets referenced in this article are drawn from the company's PEA study and involve assumptions about future commodity prices, capital costs, and operating performance that may not be realised. Past performance of similar projects is not a reliable indicator of future outcomes. Readers should conduct their own independent research and consult a licensed financial adviser before making investment decisions.

Further analysis of ASX-listed rare earth companies and the broader critical minerals sector is available at Stocks Down Under.

Want to Be First When the Next Major Rare Earth Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including critical rare earths like NdPr — and delivering actionable alerts before the broader market has time to react. Explore historic examples of what major mineral discoveries can return and begin your 14-day free trial today to position yourself ahead of the next significant find.