June 24, 2026

The Hidden Physics Behind Every Sound Your Smartphone Makes

Most people never think about what happens in the fraction of a second between tapping play and hearing music emerge from their phone. The process involves electromagnetic forces, precision metallurgy, and a carefully engineered chain of materials stretching from mines on multiple continents to an assembly line where magnets smaller than a fingernail are fitted into acoustic modules with micrometer-level tolerances. At the centre of this process sit rare earth elements, and understanding their role reveals something important: the audio quality of modern smartphones is, at its most fundamental level, a materials science story.

The performance gap between the tinny earpiece of an early 2000s handset and the stereo output of a 2026 flagship is not primarily the result of better software or more powerful processors. It is the result of a shift in what magnets can do at a given size, and rare earths in smartphone speakers are the reason that shift happened at all.

When big ASX news breaks, our subscribers know first

Why Magnetic Strength Is the Defining Variable in Miniature Speaker Design

Inside every smartphone speaker sits a voice-coil driver, a deceptively simple mechanism that converts fluctuating electrical signals into physical motion. A coil of wire is suspended in the magnetic field produced by a permanent magnet. When current flows through the coil, it experiences a force proportional to the strength of that magnetic field, pushing or pulling a diaphragm that displaces air and produces sound.

The critical variable is flux density in the gap between the magnet poles and the voice coil. Higher flux density means more force per ampere of current, which translates directly into louder output from the same electrical input, lower distortion at high volumes, and less wasted energy as heat. Every engineering objective in a compact speaker motor, whether loudness, efficiency, or acoustic clarity, traces back to that single magnetic field measurement.

This is precisely why neodymium-iron-boron (NdFeB) magnets became the dominant choice for smartphone audio. According to the U.S. Geological Survey's Mineral Resources Programme, NdFeB magnets achieve the highest energy product (BHmax) of any commercially available permanent magnet. Energy product is the volumetric measure of how much magnetic energy a material can store, and it directly determines the minimum magnet size required to achieve a target flux density. For smartphone designers working in millimetres of available space, that figure is not an abstract data point. It determines whether a stereo speaker configuration physically fits inside a device.

A smaller speaker motor frees internal space for a larger battery cell, expanded camera module architecture, and improved water-resistance sealing. The miniaturisation that high-energy-product NdFeB magnets enable creates a cascade of design freedoms that make the modern smartphone form factor possible.

Element-by-Element: What Is Actually Inside a Smartphone Speaker Magnet

The term rare earths in smartphone speakers covers a specific and well-defined set of elements, each contributing differently to magnet performance and durability.

| Rare Earth Element | Symbol | Primary Function | Thermal Role |

|---|---|---|---|

| Neodymium | Nd | Core magnetic phase in NdFeB; delivers peak energy product | Moderate heat sensitivity without additives |

| Praseodymium | Pr | Partial substitute for Nd; present in most commercial NdFeB | Improves performance under temperature fluctuation |

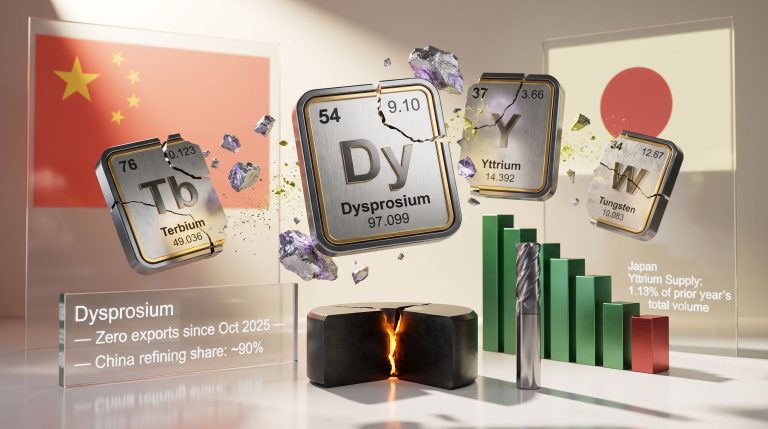

| Dysprosium | Dy | Raises coercivity to resist demagnetisation under sustained heat | Critical for high-temperature speaker operation |

| Terbium | Tb | Boosts coercivity at lower concentrations than Dy | Enables heat-stable output in thinner geometries |

| Samarium | Sm | Core phase in SmCo magnets for niche high-temperature uses | Superior thermal ceiling but higher material cost |

| Cerium & Lanthanum | Ce / La | Polishing compounds for acoustic mesh finishing | Indirect role in surface quality consistency |

Neodymium and Praseodymium: The Foundational Pair

In practice, commercial NdFeB magnet production rarely uses pure neodymium. Praseodymium is chemically similar and often substituted in part because it improves thermal stability in the resulting Pr-Fe-B crystal phase and is frequently extracted alongside neodymium during chemical separation. The two elements are so interlinked in processing that market pricing typically tracks them as a combined oxide, abbreviated Nd-Pr oxide.

This is an important and underappreciated detail: when analysts discuss neodymium supply tightness, they are almost always describing a supply picture that includes praseodymium as an inseparable commercial reality. Furthermore, rare earth supply chains for these two elements are increasingly scrutinised by governments and industry alike as demand grows.

Dysprosium and Terbium: The Thermal Stability Problem They Solve

NdFeB magnets lose coercivity — their resistance to demagnetisation — as temperature rises. The Curie temperature of pure NdFeB is approximately 312 degrees Celsius, but performance degradation begins at far lower temperatures. During sustained gaming sessions, video playback, or wireless charging, a smartphone can reach internal temperatures that cause meaningful coercivity loss in an unmodified NdFeB magnet.

The symptom is progressive volume reduction that reverses once the device cools, a behaviour sometimes mistakenly attributed to software throttling when the actual cause is thermal demagnetisation in the speaker motor itself. Dysprosium and terbium additions address this by substituting for neodymium at specific sites in the crystalline lattice, raising coercivity substantially.

Terbium is particularly efficient, achieving comparable coercivity enhancement at lower additive concentrations than dysprosium. This matters commercially because both elements are classified as heavy rare earths, extracted predominantly from ion-adsorption clay deposits concentrated in southern China, and are structurally scarcer and more expensive than light rare earths like neodymium and praseodymium.

The International Energy Agency has repeatedly flagged heavy rare earth availability as a supply concern distinct from the light rare earth picture. Dysprosium and terbium supply cannot simply scale with neodymium production because they originate from different deposit types with entirely different geological distribution patterns.

SmCo, Ferrite, and Where NdFeB Has No Viable Competitor

Samarium-cobalt (SmCo) magnets offer a higher Curie temperature and inherent corrosion resistance that eliminates the need for protective coatings. However, their material cost and the cobalt supply chain's own concentration risks make them impractical for consumer electronics at scale. Ferrite magnets are inexpensive and corrosion-resistant but deliver a fraction of the energy product of NdFeB, requiring significantly larger physical volumes to match performance. For the thinnest, highest-output speaker modules in flagship smartphones, neither alternative is a competitive substitute.

The Supply Chain From Rock to Speaker: Where the Vulnerabilities Concentrate

The journey from rare-earth-bearing ore to the finished magnet inside a phone involves seven distinct and technically demanding stages:

- Mining and concentration of rare-earth-bearing ore at the source deposit

- Chemical separation using solvent extraction circuits to isolate individual rare earth oxides at magnet-grade purity

- Metal reduction and alloying to combine Nd, Pr, Fe, B, and heavy REE additives into the correct composition

- Powder metallurgy and sintering where alloy is milled, magnetically pressed, and heated under pressure to form a dense solid

- Precision machining and coating to cut magnets to tolerance and apply corrosion-resistant surface treatments

- Acoustic module assembly integrating the magnet with voice coil, diaphragm, and gasketed mesh grilles

- Quality validation verifying flux consistency and acoustic output against IEC and ISO standards

The most structurally constrained stage is chemical separation. Building a new separation facility requires years of permitting, environmental compliance work, and engineering. The International Energy Agency has described this midstream bottleneck as a systemic constraint that cannot be resolved rapidly regardless of how much investment is committed upstream at the mining stage. Consequently, rare earth processing challenges remain one of the most discussed topics among industry analysts and policymakers.

Geographic concentration amplifies the risk. China controls a dominant share of both rare earth chemical separation capacity and sintered magnet manufacturing. According to both the IEA and the U.S. Geological Survey, this concentration affects every NdFeB-dependent industry simultaneously, meaning that consumer electronics, electric vehicles, wind turbines, and industrial automation all compete for supply from the same constrained processing infrastructure. Indeed, China's rare earth export restrictions have heightened these concerns significantly through 2025 and into 2026.

Quantifying the Demand: What One Billion Devices Mean for Rare Earth Markets

| Metric | Data Point | Source |

|---|---|---|

| Global smartphone shipments (2025) | Exceeded 1 billion units | IDC / Counterpoint Research |

| Stereo speaker adoption | Majority of mid-range and above devices | GSMA Intelligence |

| Typical NdFeB magnet weight per micro-speaker | Sub-1 gram per motor | TechInsights teardown data |

| Nd-Pr oxide pricing (2025-2026) | Volatile; tight supply from EV, wind, and electronics demand | Benchmark Mineral Intelligence |

At sub-gram magnet weights, individual smartphone speakers seem trivial from a materials perspective. The aggregate picture is different. Multiplied across more than one billion devices per year, with a growing share incorporating dual stereo setups that double the magnet count per handset, the total consumption of Nd-Pr oxide attributable to consumer audio is commercially meaningful.

This demand stream competes directly with electric vehicle traction motors, which use NdFeB magnets measured in kilograms per unit, and offshore wind turbines, which may contain hundreds of kilograms of magnet material each. The critical minerals demand driven by the global energy transition therefore intersects directly with the materials underpinning everyday consumer audio technology.

The price volatility that results from this multi-sector competition flows through to component costs. Benchmark Mineral Intelligence reported that Nd-Pr oxide pricing remained under sustained pressure through 2025 and into 2026, reflecting competing demand rather than any single supply disruption.

The Geopolitical Dimension: Policy Risk and Supply Diversification

Export controls, industrial policy, and environmental regulation in major producing countries can shift magnet costs faster than product development cycles can accommodate. This asymmetry is particularly challenging for smartphone OEMs, whose design cycles often lock in component specifications twelve to eighteen months before a device ships.

Policy attention to this vulnerability has intensified considerably. The U.S. Department of Energy's critical materials programme, the European Commission's Critical Raw Materials Act, and equivalent frameworks in Japan and South Korea have all increased focus on magnet manufacturing resilience, recycling infrastructure, and the qualification of alternative suppliers outside the current concentration zone.

New chemical separation capacity is being developed in Australia, the United States, and Europe, however commissioning timelines are measured in years, not quarters. Building an alternative rare earth supply chain outside China is a multi-cycle transition, not a near-term solution for the smartphone industry.

The next major ASX story will hit our subscribers first

On-Device AI and the Emerging Thermal Budget Problem

A development that will increasingly affect rare earth magnet specifications in smartphones is the sustained power draw associated with on-device artificial intelligence workloads. Real-time translation, computational photography, and AI-assisted audio processing keep the processor operating at elevated temperatures for longer periods than earlier usage patterns. This narrows the thermal margin available to every other component in the device, including the speaker motor.

Where previous smartphone generations might have encountered speaker thermal stress only under edge-case conditions like prolonged gaming, future devices running continuous AI inference will generate elevated internal temperatures as a baseline. This pushes coercivity requirements for speaker magnets upward, making dysprosium and terbium additions less of an optional enhancement and more of a baseline design requirement.

The engineering response to this challenge is already visible in the broader magnet industry. Grain-boundary diffusion technology, which concentrates heavy rare earth additions precisely at crystal grain boundaries rather than distributing them uniformly through the magnet volume, achieves substantially improved coercivity while consuming significantly less dysprosium or terbium. Commercial adoption of this technique has been expanding in magnet manufacturing facilities in Japan and China, with broader qualification underway among suppliers targeting the consumer electronics sector.

NdFeB vs. SmCo vs. Ferrite: The Performance Comparison That Explains Industry Choices

| Magnet Type | Energy Product | Heat Tolerance | Corrosion Resistance | Relative Cost | Typical Application |

|---|---|---|---|---|---|

| NdFeB (with Dy/Tb) | Highest available | Good with additives | Requires protective coating | Moderate | Mainstream smartphones |

| SmCo | High | Excellent | Excellent, no coating needed | High | Niche and specialised designs |

| Ferrite | Low to moderate | Good | Excellent | Low | Entry-level or space-tolerant designs |

The table above illustrates why NdFeB remains the default choice despite its supply chain vulnerabilities. No commercially available alternative combines its energy density with acceptable cost at the volumes smartphone manufacturing requires. For a broader overview of critical minerals used across smartphone components, the audio module represents just one of many rare-earth-dependent systems within a single device.

Recycling Reality and the Long Road to Circular Supply

Smartphone magnets present one of the most structurally challenging recycling problems in the rare earth supply chain. The magnets are tiny, bonded into assemblies with adhesives, dispersed across billions of devices globally, and difficult to demagnetise and recover at the purity levels magnet manufacturing requires.

Near-term recycled NdFeB supply is expected to flow predominantly from electric vehicle motors and industrial equipment, where individual magnet masses are large enough to make recovery economically straightforward. Smartphone magnet recycling will improve as collection infrastructure, automated disassembly technology, and hydrometallurgical processing methods mature, but the contribution to overall supply will remain limited through the late 2020s.

Disclaimer: Projections regarding recycling contributions and supply timelines reflect current industry assessments and are inherently uncertain. Actual outcomes will depend on policy developments, technology commercialisation rates, and market conditions that cannot be predicted with precision.

Frequently Asked Questions About Rare Earths in Smartphone Speakers

Do wireless earbuds use the same rare earth magnets as smartphone speakers?

Both typically rely on NdFeB motors because the performance-per-volume advantage is equally relevant at earbud scale. Smartphone speakers may face stricter thermal and sealing constraints that increase the value of higher-coercivity heavy REE additions.

Which single rare earth element has the greatest impact on speaker loudness?

Neodymium contributes most directly to the energy product that determines flux density and therefore acoustic output. Praseodymium is commercially inseparable from neodymium in most magnet production and contributes comparably.

Can a smartphone speaker degrade over time due to magnet weakening?

Yes. Repeated thermal cycling can cause incremental coercivity loss in magnets not adequately protected by dysprosium or terbium additions. The effect is typically slow under normal use conditions but can accelerate in high-temperature environments or devices with inadequate thermal management.

Why can't manufacturers use larger ferrite magnets to avoid rare earth dependency?

Ferrite magnets require substantially greater volume to achieve equivalent flux density. In a smartphone chassis measured in fractions of a millimetre, that volume is not available without sacrificing battery capacity, structural integrity, or water-resistance architecture.

How do export restrictions on rare earths from China affect smartphone pricing?

Supply restrictions translate into price increases for separated rare earth oxides and finished magnets, which flow through to acoustic component costs. Given that speaker module costs represent a fraction of total bill-of-materials for a flagship device, the direct per-unit impact is modest but becomes meaningful at billion-unit volumes across the industry.

Key Takeaways: Rare Earths and the Future of Smartphone Audio

- Neodymium and praseodymium deliver the magnetic energy density that makes sub-gram speaker motors acoustically viable at smartphone scale, and they are commercially interlinked in virtually all NdFeB magnet production

- Dysprosium and terbium are not performance enhancements but thermal stability requirements, and their heavy rare earth classification means supply constraints are structurally independent from the neodymium supply picture

- Global smartphone shipments exceeding one billion units annually create aggregate REE demand that competes directly with electric vehicle and wind energy supply chains for the same midstream processing capacity

- Chemical separation bottlenecks and heavy REE scarcity are the two most structurally significant constraints in the magnet supply chain, and neither can be resolved quickly regardless of upstream mining investment

- Grain-boundary diffusion technology represents the most commercially mature pathway to reducing dysprosium and terbium intensity without sacrificing coercivity performance at elevated temperatures

- On-device AI workloads are raising baseline device operating temperatures, which will increase coercivity requirements for speaker magnets across future device generations

- Supply diversification across Australia, the United States, and Europe is progressing but will require multiple product cycles before materially reducing dependence on current concentration points

Readers seeking to deepen their understanding of rare earth supply chains, market dynamics, and the policy landscape shaping critical materials availability can explore further analysis and industry coverage at Rare Earth Exchanges.

Want to Be First to Spot the Next Major Rare Earth Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant rare earth and critical mineral discoveries before the broader market reacts — explore historic discovery returns to understand what early positioning can mean, then begin your 14-day free trial at Discovery Alert to secure your market-leading edge.