June 15, 2026

The Hidden Economics Behind Dual-Commodity Critical Mineral Development

Most investors scanning the critical minerals landscape focus on grade, tonnage, and commodity price exposure. Fewer stop to examine the structural logic that separates projects with genuine economic resilience from those that look compelling only under favourable assumptions. The mechanics of how a development team chooses to sequence production, design its processing circuit, and manage environmental liability often reveal more about long-term viability than any single headline metric.

Against that backdrop, the recently completed Preliminary Economic Assessment (PEA) for the Resouro Tiros rare earths and titanium project in Minas Gerais, Brazil, offers a case study in deliberate project architecture. The economics are striking, but the reasoning behind the project's design choices is where the real substance lies.

When big ASX news breaks, our subscribers know first

Why Titanium and Rare Earths Together Creates a Different Risk Equation

Single-commodity exposure is one of the most persistent vulnerabilities in junior mining. When a project's revenue is tied entirely to one market, price cycles in that market become existential risks rather than manageable headwinds. The Resouro Tiros rare earths and titanium project PEA is built around a deliberate dual-revenue architecture that addresses this structural weakness from the outset.

Titanium dioxide is a globally traded industrial commodity consumed primarily in pigment manufacturing for paints, coatings, and plastics, with growing demand from aerospace and defence applications where titanium metal is increasingly valued for its strength-to-weight properties. The rare earth carbonate stream operates in an entirely different demand cycle, driven by permanent magnet production for electric vehicle motors and wind turbine generators.

What makes this pairing strategically interesting is that the demand drivers for each commodity are largely uncorrelated. TiO₂ pigment demand is sensitive to construction cycles and manufacturing activity. Rare earth demand, particularly for magnet materials such as neodymium, praseodymium, dysprosium, and terbium, is driven by energy transition capital expenditure and automotive production volumes. Furthermore, a project that can generate revenue from both streams simultaneously carries a materially different risk profile than one anchored to a single price signal, making critical minerals demand dynamics especially relevant here.

The growing disconnect between Chinese rare earth production policy and Western demand requirements has created structural supply gaps that new non-Chinese producers are increasingly positioned to address, particularly those offering commercially recognised intermediate products such as mixed rare earth carbonates.

Tiros Project Resource Scale: Understanding the Staged Development Logic

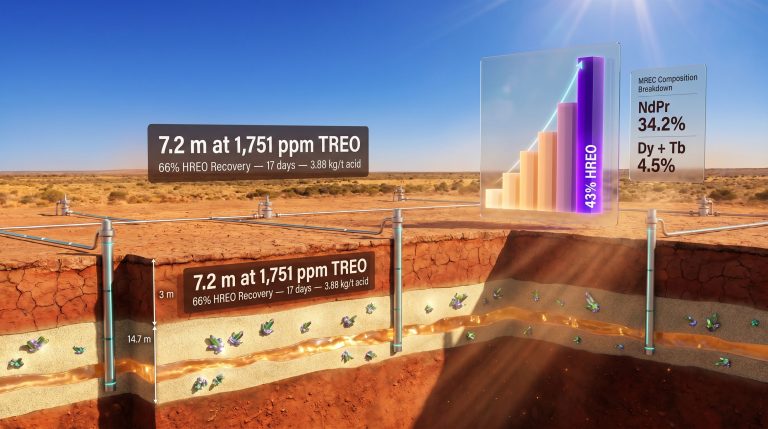

The Tiros project hosts a total mineral resource of approximately 1.9 billion tonnes across 497 km² spanning 28 mineral concessions in Minas Gerais. That scale places it among the largest combined titanium and rare earth resource inventories currently in development anywhere in the world. However, the PEA does not attempt to process that entire resource. It targets something far more surgical.

The starter operation focuses on a high-grade measured and indicated domain containing approximately 104 million tonnes at a feed grade of 26.3% TiO₂ and 10,832 ppm TREO, with a strip ratio of 2.7:1. This zone represents less than 1% of the total resource base.

| Resource Category | Tonnage | TiO₂ Grade | TREO Grade |

|---|---|---|---|

| Total Mineral Resource | ~1.9 billion tonnes | ~12% TiO₂ | ~3,900-4,000 ppm |

| High-Grade Domain (M&I) | ~136 million tonnes | ~23% TiO₂ | ~8,860 ppm |

| PEA Starter Zone (M&I) | ~104 million tonnes | ~23% TiO₂ | ~9,100 ppm |

The deliberate selection of this high-grade starter zone reflects a staged development philosophy that is increasingly favoured in the current financing environment. Rather than attempting to justify a large capital raise on the basis of a resource that has yet to demonstrate processing performance at scale, the team has chosen to validate metallurgical assumptions, establish product specifications, and generate early cash flow from a comparatively modest initial footprint.

This approach compresses the capital requirement, shortens the timeline to first production, and reduces the environmental and social footprint during the project's most sensitive regulatory phase. It also preserves the expansion optionality embedded in the remaining 99% of the resource, which represents a long-term development runway that few comparable projects can match. Careful attention to cut-off grade economics is central to how this starter zone was identified and defined.

Breaking Down the PEA Economics: What a 44.2% IRR Actually Means

The headline numbers from the Resouro Tiros rare earths and titanium project PEA are genuinely compelling, but understanding what they represent in a broader market context requires some calibration.

Key PEA Economic Metrics at a Glance:

- After-Tax NPV: US$714.9 million

- After-Tax IRR: 44.2%

- Annual Processing Rate: 500,000 tonnes per annum

- Initial Mine Life: 20 years

- Total Run-of-Mine Feed: 9.5 million tonnes

- Feed Grade: 26.3% TiO₂ and 10,832 ppm TREO

- Strip Ratio: 2.7:1

An after-tax internal rate of return above 40% is exceptional by the standards of the mining industry. Most mid-tier critical mineral development projects are considered economically viable at IRRs in the 15-25% range, and projects achieving returns above 35% at the PEA stage are rare enough to attract serious attention from project financiers and potential strategic partners.

The after-tax NPV of US$714.9 million is particularly significant when considered alongside the scale of the starter operation. This economic value is being generated from less than 1% of the total resource. The implied valuation of the broader 1.9-billion-tonne resource base, assuming comparable or even lower-grade economics across the expanded deposit, is a figure that warrants serious attention from investors with a long time horizon.

A PEA is an early-stage technical and economic evaluation. The estimates it produces carry inherent uncertainty and are not equivalent to a Pre-Feasibility Study or definitive feasibility study. Investors should treat PEA economics as directional indicators rather than confirmed project parameters, and capital allocation decisions should account for the meaningful range of outcomes that remain possible at this stage of development.

How the Processing Flowsheet Works: A Technical Walkthrough

One of the less-discussed but critically important elements of any critical mineral project is the processing route. Flowsheet selection determines capital intensity, operating costs, reagent consumption, and ultimately product quality. The Tiros flowsheet is built around a sulphuric acid digestion pathway that is well-established in industrial titanium processing and has been adapted to enable simultaneous rare earth recovery.

The processing sequence operates as follows:

- Grinding and Sizing Beneficiation – Initial particle size reduction and classification to prepare the ore for downstream separation.

- Magnetic Separation and Electrostatic Separation – Mineral sorting exploits differences in magnetic susceptibility and electrical conductivity to concentrate target minerals and reject gangue.

- Gravity Separation – Density-based concentration separates heavy minerals from lighter waste material.

- Acid Leach – Chemical dissolution begins the liberation of target elements from the mineral matrix.

- Sulphation and Water Leach – Sulphuric acid digestion converts titanium and rare earth compounds into soluble forms that can be selectively recovered from solution.

- Hydrolysation – Titanium dioxide is precipitated from solution through controlled hydrolysis.

- Precipitation and Solid-Liquid Separation – Final product recovery separates the mixed rare earth carbonate from solution, with tailings management occurring at this stage.

| Product Stream | Recovery Rate | Product Form |

|---|---|---|

| Titanium Dioxide (Coarse) | Combined 68.7% | Coarse TiO₂ concentrate |

| Titanium Dioxide (Fine) | Combined 68.7% | Fine TiO₂ concentrate |

| Rare Earth Elements | 67% | Mixed rare earth carbonate |

A combined TiO₂ recovery of 68.7% and a rare earth recovery of 67% are operationally meaningful figures, though it is worth noting that recovery rates at PEA stage require confirmation across a broader range of ore types before they can be treated as bankable parameters.

The Sulphation Route: Why Processing Chemistry Matters for Project Economics

The choice of sulphuric acid digestion as the core extraction mechanism is not merely a technical detail. It has meaningful economic consequences that are not always immediately apparent to non-specialist investors.

Sulphation-based processing is the dominant industrial route for ilmenite-type titanium feedstocks. Its chemistry is well understood, and the engineering parameters for plant design are based on decades of commercial operational data. This reduces technical risk relative to novel or emerging processing approaches that require more extensive metallurgical development work.

The integration of rare earth recovery within the same acid circuit is an important efficiency feature. Rather than operating two entirely separate processing trains, the flowsheet captures REE value as a co-product of the titanium extraction process, reducing the incremental capital and operating cost associated with the rare earth revenue stream. This kind of processing integration is less common than it might appear and represents genuine technical sophistication in the flowsheet design.

Acid consumption is, however, a meaningful cost variable. Sulphuric acid pricing is sensitive to global sulphur markets and industrial supply chains, and reagent cost assumptions embedded in any PEA-stage operating cost model carry uncertainty that investors should factor into their analysis.

The next major ASX story will hit our subscribers first

Dry-Stack Tailings: Environmental Design as a Financing Prerequisite

The decision to design the Tiros operation around dry-stack tailings management is worth examining in detail, because it reflects a broader shift in what project financiers and international development institutions require from new mining operations.

Conventional wet tailings storage facilities have been responsible for some of the most catastrophic environmental failures in modern mining history. Brazil itself experienced the Mariana dam failure in 2015 and the Brumadinho collapse in 2019, events that fundamentally altered the regulatory and social expectations placed on new mining projects in the country. In this context, a project that eliminates wet tailings storage from its design is not merely demonstrating environmental sensitivity; it is responding to a concrete regulatory and social licence reality.

Dry-stack tailings management involves dewatering the processed tailings material to a point where it can be stacked and compacted without requiring a water-retaining dam structure. The approach carries higher upfront capital costs than conventional wet storage, but significantly reduces long-term environmental liability. Consequently, it substantially improves the project's prospects for community acceptance and regulatory approval, and is increasingly recognised as central to mining sustainability transformation across the sector.

For project finance purposes, this design choice is increasingly viewed as a prerequisite rather than a differentiator. Institutional lenders and export credit agencies have progressively tightened their environmental, social, and governance requirements for mining project financing, and wet tailings facilities in geologically or seismically sensitive areas are increasingly difficult to finance through conventional channels.

Minas Gerais as a Jurisdiction: Infrastructure, Logistics, and Regulatory Context

The location of the Tiros project in Minas Gerais is not incidental. The state is Brazil's most established mining jurisdiction, with a history of large-scale mineral extraction that has produced the supporting infrastructure networks, regulatory capacity, and skilled workforce that greenfield projects elsewhere must build from scratch.

Key jurisdictional advantages include:

- Existing road and rail infrastructure capable of supporting industrial-scale mineral extraction and product transport.

- Proximity to Atlantic export facilities, which supports cost-competitive delivery of titanium dioxide and rare earth carbonate products to European and North American markets.

- An established regulatory framework for environmental licensing and mine permitting, with agencies that have direct experience processing applications for large-scale mineral development.

- A regional workforce with demonstrated mining sector skills, reducing the training and accommodation cost assumptions that inflate operating cost estimates for more remote projects.

Brazil's mining code, while subject to ongoing legislative debate, provides a relatively stable legal framework for mineral tenure compared to many frontier exploration jurisdictions. The country's existing export relationships with major industrial economies also provide a foundation for offtake discussions that projects in less commercially connected jurisdictions cannot easily replicate.

Ausenco's Involvement and What Third-Party Technical Credibility Signals

The engagement of Ausenco as lead technical consultant for the PEA carries significance beyond the quality of the engineering work itself. Ausenco is an internationally recognised firm with a proven track record across mineral processing and hydrometallurgical project development globally. Their involvement functions as a form of technical credibility signal to the investment community.

For a project at the PEA stage, the identity and reputation of the engineering consultant matters to institutional investors and potential project financiers. Third-party validation from a credentialled firm reduces the perception of technical risk and supports the credibility of the economic parameters disclosed to the market. As the project advances toward pre-feasibility, the continuity of engagement with an established engineering partner will become increasingly important to financing conversations.

Development Pathway: From PEA to Production Decision

| Milestone | Typical Timeline | Key Deliverables |

|---|---|---|

| Preliminary Economic Assessment (PEA) | Completed | Economic parameters, flowsheet selection |

| Pre-Feasibility Study (PFS) | 12-24 months | Refined capital and operating cost estimates |

| Definitive Feasibility Study (DFS) | 24-36 months | Bankable engineering, environmental approvals |

| Project Financing | Concurrent with DFS | Offtake agreements, debt/equity structuring |

| Construction Decision | Post-DFS | Final investment decision |

The immediate priorities following PEA completion centre on advancing metallurgical test work across a broader range of ore types to confirm recovery rates and product specifications. This work is essential for initiating meaningful offtake discussions, as potential buyers of titanium dioxide concentrate and mixed rare earth carbonate will require product specification data before entering commercial negotiations.

Environmental and social baseline studies must also progress in parallel with technical development. Brazilian environmental licensing for mining operations involves multiple stages of assessment and community consultation, and the timeline for regulatory approvals is a material variable in any production schedule. Furthermore, the global context of rare earth supply chains continues to evolve rapidly, adding urgency to projects that can demonstrate near-term development momentum.

Frequently Asked Questions: Resouro Tiros PEA

What is the total resource size of the Tiros project?

The Tiros project contains a total mineral resource of approximately 1.9 billion tonnes across 497 km² in Minas Gerais, Brazil, representing one of the largest combined titanium and rare earth resource inventories currently in development globally.

What products will the operation produce?

The proposed flowsheet is designed to produce two forms of titanium dioxide concentrate (coarse and fine grades) and a mixed rare earth carbonate, creating a dual-revenue structure across two distinct commodity markets.

What are the headline PEA economics?

The PEA indicates an after-tax NPV of US$714.9 million and an after-tax IRR of 44.2%, based on a 500,000 tonne per annum starter operation with a 20-year initial mine life. For additional context on these results, Stockhead's coverage of the Tiros PEA highlights the billion-dollar potential underpinning these figures.

Why target less than 1% of the total resource initially?

The staged approach minimises upfront capital requirements, reduces the environmental footprint during the project's most sensitive development phase, and accelerates the pathway to production while building the operational track record needed to support financing for larger-scale expansion.

What is the strip ratio for the starter operation?

The PEA models a strip ratio of 2.7:1, consistent with a shallow, open-pit operation targeting near-surface high-grade mineralisation that requires minimal pre-stripping to access economic ore.

What stage of development is the project at?

As of mid-2026, the Tiros project has completed its Preliminary Economic Assessment. The next development milestones would typically include a Pre-Feasibility Study followed by a Definitive Feasibility Study before any final investment decision.

Key Takeaways: What the Economics Really Reveal

- The PEA confirms a high-grade, near-surface starter operation capable of generating compelling economic returns from less than 1% of the total resource inventory.

- A 44.2% after-tax IRR and US$714.9 million after-tax NPV position the Tiros project among the more economically robust critical mineral developments at the PEA stage anywhere in the world.

- The dual-revenue model across titanium dioxide and rare earth carbonate reduces single-commodity price dependency in a way that single-product projects structurally cannot replicate.

- Dry-stack tailings design reflects both environmental responsibility and a pragmatic response to the financing and social licence realities of operating in post-Brumadinho Brazil.

- The 1.9-billion-tonne total resource base provides an expansion platform of exceptional scale, with the starter operation functioning as the proof-of-concept phase for a much larger long-term development.

- Minas Gerais jurisdiction delivers infrastructure, regulatory experience, and export logistics advantages that meaningfully reduce development execution risk relative to competing critical mineral projects in less established locations.

Readers seeking broader context on titanium and rare earth market dynamics, critical mineral project development economics, or Brazil's mining sector may find value in reviewing publicly available resources from Resouro Strategic Metals, which provides ongoing updates across the Tiros project's development.

Want to Track the Next Major Critical Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths, titanium, and more than 30 other commodities — turning complex data into actionable investment insights for traders and long-term investors alike. Explore how historic discoveries have generated exceptional returns and begin your 14-day free trial today to secure a genuine market-leading edge.