June 13, 2026

The Quiet Accumulation That Can No Longer Be Ignored

Every industrial system carries within it a hidden accounting problem. For the aluminium sector, that problem has been building for over a century, one tonne at a time, in vast storage ponds and sprawling impoundment facilities across six continents. The numbers have now grown large enough to demand a different kind of attention.

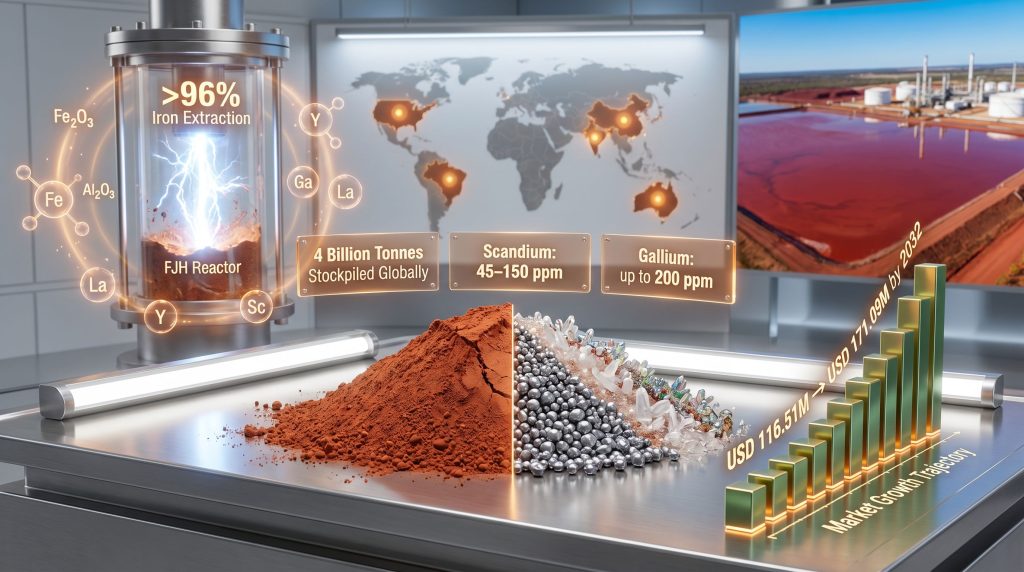

Global alumina output reached approximately 141 million tonnes in 2023, climbing to an estimated 154 million tonnes in 2025. For every tonne of alumina that refineries produce through the Bayer process, up to 1.5 tonnes of highly alkaline bauxite residue is generated as a byproduct. The arithmetic of that ratio, compounded across decades of industrial output, has produced a cumulative global stockpile now estimated at approximately 4 billion tonnes, with annual additions exceeding 150 million tonnes. If current trajectory holds, projections suggest that figure could approach 8 billion tonnes by 2040.

What changed is not the chemistry. What changed is the geopolitical and economic context surrounding it. Red mud as aluminium industry resource frontier is no longer a speculative concept from an academic paper. It is a structural reorganisation in motion.

When big ASX news breaks, our subscribers know first

Why the Industry's Largest Liability Is Being Reconsidered as an Asset

The material itself, commonly referred to as red mud or bauxite residue, has historically been characterised by two properties that made it difficult to handle and economically unattractive to process. The first is its extreme alkalinity, with pH levels typically ranging from 10 to 13, presenting genuine contamination risks to groundwater systems and requiring continuous monitoring of storage facilities. The second is its sheer volume, which has consistently made the capital investment required for processing appear disproportionate relative to the recoverable value.

That calculus is shifting due to several converging forces that are redefining the economic case simultaneously:

- Critical mineral scarcity has placed gallium, scandium, and rare earth elements at the centre of energy transition supply chain debates, dramatically increasing the perceived value of trace concentrations in residue.

- Regulatory pressure on residue storage is intensifying across multiple jurisdictions, increasing the ongoing liability cost of continued accumulation.

- Technological advancement has compressed extraction timelines and improved recovery rates to commercially viable thresholds that simply did not exist a decade ago.

- Geopolitical realignment of supply chains for strategic minerals has created policy incentives, particularly in the United States and Europe, for domestic processing alternatives.

The 2010 Ajka disaster in Hungary, where a red mud dam failure killed 10 people and caused widespread chemical burns across surrounding communities, marked a critical regulatory inflection point that has progressively tightened storage standards globally. That tragedy transformed what was once a permitting and disposal conversation into a liability management imperative.

What the Chemistry of Red Mud Actually Contains

Understanding why bauxite residue has attracted such sustained research interest requires looking closely at its compositional profile, which varies considerably by geography but consistently contains a suite of recoverable materials spanning bulk commodities and high-value critical minerals.

| Region | Iron Oxide (Fe₂O₃) Content | Alumina Content | Notable Characteristics |

|---|---|---|---|

| Australia | 28.5% to 56.9% | 15% to 24% | High iron variability; metallurgical recovery focus |

| India (Damanjodi) | ~53% Fe₂O₃ | ~18% | Positioned for iron and scandium co-recovery |

| China (Sintering) | Moderate iron | Variable | Up to 41.6% CaO; direct cement integration pathway |

| United States (Gramercy, Louisiana) | Moderate | ~20% | REE concentrations of 3,000 to 4,000 ppm |

Critically, the variability in residue composition that once deterred investors and processors is increasingly being treated as a feedstock differentiation factor rather than a barrier. High-iron residues in Australia and India lend themselves to metallurgical pathways, while Chinese sintering-derived residues, containing up to 41.6% calcium oxide and 32.5% silica, are being routed directly into cement manufacturing streams where pre-treatment costs are minimal.

Trace Elements and the Strategic Metals Argument

Beyond the bulk mineral fractions, bauxite residue consistently carries concentrations of strategically significant trace elements that have become central to the economic reappraisal:

- Scandium: 45 to 150 ppm, exceeding double the Earth's average crustal abundance

- Gallium: up to 200 ppm, a critical input for semiconductors and compound materials

- Vanadium: up to 800 ppm, relevant to battery storage and steel alloying

- Rare earth elements: cerium, lanthanum, terbium, gadolinium, and yttrium in commercially significant concentrations

- REE totals at Gramercy, Louisiana: estimated at 3,000 to 4,000 ppm across approximately 30 million tonnes of stockpiled material

The significance of these concentrations becomes clear when viewed through a supply chain lens. Gallium is essential for the production of gallium arsenide and gallium nitride semiconductors, which are foundational to both defence electronics and renewable energy infrastructure. China currently controls the vast majority of global gallium refining capacity. The presence of gallium at up to 200 ppm in widely distributed bauxite residue stockpiles represents an alternative sourcing pathway that Western economies are only beginning to seriously evaluate.

Furthermore, understanding the role of gallium in semiconductors helps contextualise why recoverable gallium concentrations in red mud are attracting such intense strategic interest from governments and technology manufacturers alike.

Flash Joule Heating: The Technology That Changed the Extraction Timeline

Among the suite of emerging processing technologies, Flash Joule Heating with chlorination has attracted the most attention due to the radical compression it achieves in processing time and the extraction efficiencies it demonstrates at pilot scale.

Developed as a commercial application at Rice University and being advanced through the spinoff company Flash Metals USA under Metallium Ltd., the process works through a precise and rapid sequence:

- Red mud feedstock is loaded into the FJH reactor chamber

- A high-intensity electrical pulse is applied for approximately 60 seconds

- Iron is extracted at rates exceeding 96%, while aluminium is retained in the purified stream at approximately 99%

- Sodium is simultaneously removed and toxic metals are volatilised in the same reaction step

- Residual material can be converted into ceramic tiles, bricks, or construction-grade inputs, creating a near-zero-waste processing chain

The significance of achieving 96% iron extraction in 60 seconds cannot be overstated in the context of refinery economics. Conventional pyrometallurgical approaches involve multi-stage roasting, multiple energy inputs across hours of processing time, and significantly higher capital infrastructure requirements. FJH compresses that operational footprint dramatically while simultaneously addressing the toxic metal removal challenge that has added cost and regulatory complexity to competing systems.

How Competing Technologies Stack Up

FJH is not the only extraction pathway advancing toward commercial viability. A broader technology landscape is emerging, with each approach offering different trade-offs across recovery rate, capital cost, processing time, and maturity level.

| Technology | Iron Recovery Rate | REE Recovery | Capital Cost | Processing Time | Maturity Level |

|---|---|---|---|---|---|

| Flash Joule Heating (FJH) | >96% | Retained in stream | High (emerging) | ~60 seconds | Pilot to Commercial |

| Hydrometallurgical Leaching | ~90% | Up to 80% | Moderate | Multi-stage | Industrial |

| Bioleaching | Moderate | 84 to 91% (Ce, Y) | USD 30 to 50M/Mt | 3+ days | Emerging commercial |

| Combined Roasting (China) | >93% | Variable | High | Multi-hour | Industrial scale |

| On-site Metallurgical (WPI) | >80% waste reduction | High purity | Moderate | Continuous | Pilot stage |

Hydrometallurgical systems using staged acid leaching now achieve approximately 90% recovery of both iron and aluminium. A 2025 breakthrough published in Frontiers in Materials applying ammonium sulfate roasting has meaningfully improved scandium extraction selectivity while keeping iron dissolution below 0.12%, a technically significant improvement that allows operators to target trace element recovery without sacrificing bulk metal yield.

Bioleaching, long dismissed as an experimental curiosity with limited commercial upside, is emerging as a low-capital alternative with specific advantages in rare earth recovery. Using bacterially catalysed sulfur oxidation with Sulfobacillus thermosulfidooxidans, trials have demonstrated:

- 89% aluminium recovery

- 84% cerium recovery

- 91% yttrium recovery

- 70% terbium recovery

- 60% gadolinium recovery

- Greater than 95% dealkalization rates for sodium, potassium, and calcium

- Capital costs as low as USD 30 to 50 million per million tonnes of processing capacity

The dealkalization performance is particularly noteworthy because sodium removal has historically been one of the costliest pre-treatment steps in any residue processing pathway. Achieving that at bioleaching capital cost levels, while simultaneously recovering REEs, positions the technology as viable for lower-grade deposits or operations where minimising upfront capital expenditure is a priority.

How Major Economies Are Approaching Valorisation Differently

The contrast in national approaches to bauxite residue processing is itself an instructive map of how different economies are prioritising the opportunity. No two major producing regions have reached the same strategic conclusion, which creates both diversity in technology development and complexity in benchmarking commercial progress.

India is building a hybrid co-recovery model. A 10-tonne-per-day pilot at Damanjodi is targeting simultaneous extraction of iron, alumina, and scandium while converting residual material into construction bricks at a projected rate of 1 million units annually. The economic logic is reinforced by India's domestic construction sector, which is projected to reach USD 1.4 trillion by 2047, providing powerful demand-side pull for locally produced construction materials derived from residue processing.

China is operating at a scale that makes all other national programmes look incremental by comparison. With over 100 million tonnes of residue generated annually, Chinese industry is advancing under government-set utilisation targets of 15% by 2027, rising to 25% by 2030, supported by multi-billion-yuan investment in cement clinker integration and combined roasting operations that are already delivering iron recovery rates above 93% alongside aluminium purity of 99.49%.

Europe is approaching the issue through its decarbonisation and circular economy frameworks. The ReActiv project has demonstrated that bauxite residue can substitute for up to 30% of cement clinker in construction applications, producing proportional reductions in process emissions while simultaneously diverting material from landfill. In addition, Europe's critical minerals supply chain strategy increasingly identifies bauxite residue valorisation as a mechanism for reducing import dependency on strategic materials.

The United States has adopted the most strategically framed approach, treating residue processing primarily as a national security and critical mineral independence initiative. Federal funding is being directed toward gallium and scandium recovery programmes, reflecting the acute awareness of US dependency on Chinese-controlled supply chains for these materials. The Gramercy, Louisiana deposit alone represents approximately 30 million tonnes of residue carrying REE concentrations of 3,000 to 4,000 ppm, a resource that sits largely untapped within US borders.

Brazil is at an advanced pilot stage, with a project scheduled for completion in mid-2026 designed to process 50,000 tonnes of residue annually, producing 9,000 tonnes of pig iron and 22,000 tonnes of construction materials as its primary output streams.

Secondary Applications and Full-Spectrum Valorisation

The most commercially resilient processing models are those that do not rely on a single revenue stream from a single extracted material. Full-spectrum valorisation, a model where each fraction of processed residue is directed toward a specific end market, is increasingly the target architecture for projects seeking commercial viability at scale.

Secondary applications beyond metal recovery include:

- Construction materials: bricks, ceramic tiles, and cement clinker substitution represent the highest-volume secondary use pathway, particularly attractive in markets with strong domestic construction demand

- Soil amendment: neutralised residue, once pH-adjusted and detoxified, has been trialled as an agricultural soil conditioner, though regulatory acceptance varies significantly by jurisdiction

- Pedersen Process applications: a cement and fertiliser co-production pathway that converts processed residue fractions into value-added agricultural and construction inputs simultaneously

- Road base and fill materials: lower-value but high-volume applications that absorb large quantities of processed residue in infrastructure applications

The Indian pilot model, combining metal recovery with brick production, is perhaps the clearest operational illustration of full-spectrum valorisation in practice. By targeting multiple simultaneous output streams from a single feedstock, the economic case for processing is strengthened and the residual waste fraction that still requires disposal is minimised.

The next major ASX story will hit our subscribers first

What the Market Economics Actually Look Like

The headline market size figures for red mud as aluminium industry resource frontier, while useful for calibrating the commercial landscape, significantly understate the embedded value proposition. The global red mud processing market was valued at approximately USD 116.51 million in 2024 and is projected to reach USD 171.09 million by 2032, growing at a compound annual rate of 4.92%. However, these figures reflect processing services and technology revenue rather than the full value of recoverable materials.

The underlying economics of recoverable material streams are considerably more compelling:

| Revenue or Savings Stream | Estimated Value |

|---|---|

| Iron recovery (bulk) | USD 90 to 120 per tonne |

| Alumina recovery | USD 250 to 400 per tonne |

| Avoided disposal costs | USD 5 to 15 per tonne |

| Carbon credits (CO₂ equivalent) | USD 20 to 60 per tonne |

| Gallium (strategic premium) | Variable; supply-constrained pricing |

| Scandium (strategic premium) | Variable; very limited global supply |

At scale, iron recovery from global residue stockpiles could theoretically yield 45 to 90 million tonnes annually at current iron prices. Alumina recovery adds another 15 to 30 million tonnes per year at significantly higher per-tonne values. Gallium output, though smaller in absolute volume, could reach up to 30,000 tonnes commanding strategic market premiums that no bulk commodity price captures.

The current recycling rate for bauxite residue sits at only 1 to 3% globally. That figure represents both a systemic failure of the current industrial model and the clearest possible quantification of the opportunity available to operators who can solve the processing economics at scale.

The persistence of such a low recycling rate despite the evident compositional value of the material reflects the structural reality that continued disposal, where storage facilities exist and regulatory penalties remain limited, still presents a lower short-term cost than capital investment in processing infrastructure. That calculation is changing as regulatory costs rise, storage capacity becomes constrained, and critical minerals security concerns intensify under mounting geopolitical pressure.

The Barriers That Still Need to Be Overcome

A realistic assessment of the red mud valorisation opportunity cannot ignore the genuine structural obstacles that have kept recycling rates at 1 to 3% despite decades of research interest. Understanding these barriers is essential for evaluating the credibility of projected timelines and commercial outcomes.

Margin pressure in aluminium refining is a persistent constraint on capital allocation. Alumina refining operates on margins that leave limited room for significant additional capital expenditure on ancillary processing infrastructure, particularly when disposal costs remain manageable and processing economics require scale to be viable.

The coordination problem is arguably the most underappreciated barrier. Transitioning from a disposal model to a valorisation model requires simultaneous alignment across refiners, technology providers, governments, logistics operators, and end-market buyers. No single actor can force that transition alone, and the economics of early movers bear costs that later adopters will not face.

Residue dam safety and legacy liability continue to absorb capital and management attention. The catastrophic consequences of the 2010 Ajka disaster remain the sector's most stark reminder of what inadequate residue management looks like at its worst. The ongoing cost of managing thousands of storage facilities globally, furthermore, represents a real drain on capital that might otherwise support processing investment.

Regulatory inconsistency across jurisdictions creates uncertainty for technology developers seeking to commercialise extraction processes. What is permissible at one refinery site may require entirely different approvals at another, adding cost and timeline risk to commercial deployment.

The Green Energy Transition Connection

The link between bauxite residue valorisation and the global clean energy transition is more direct than is commonly appreciated. The rare earth elements and critical minerals recoverable from red mud are not abstract commodities. They are physical inputs required in specific quantities to manufacture the technologies that the energy transition depends upon.

Scandium is a performance-enhancing alloying element for high-strength aluminium alloys used in aerospace and advanced manufacturing, and is also a component in solid oxide fuel cells. Consequently, the role of global bauxite production in generating recoverable critical mineral streams is becoming central to clean energy supply chain planning. The rare earth elements cerium, lanthanum, terbium, and gadolinium all have roles in permanent magnets, phosphors, and clean energy components.

With current recycling rates leaving 97 to 99% of stockpiled residue unprocessed, and new residue being added at over 150 million tonnes per year, the gap between available secondary supply and growing critical mineral demand is one that the industry cannot afford to leave unaddressed. The aluminium industry's assessment of red mud increasingly reflects this strategic urgency. The alignment with UN Sustainable Development Goals 7 and 12, covering clean energy access and responsible production respectively, is clear in principle. Converting that alignment into commercial reality is the challenge that defines the next decade of bauxite residue management, and the true measure of whether red mud as aluminium industry resource frontier can transition from compelling concept to operational reality.

Disclaimer: This article contains forward-looking projections, market estimates, and technology performance data drawn from publicly available industry sources and research publications. These projections involve inherent uncertainty and should not be treated as investment advice or guarantees of commercial outcomes. Readers should conduct independent due diligence before making any investment or business decisions related to the sectors or technologies discussed.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across gallium, scandium, rare earths, and more than 30 other commodities — precisely the materials driving the bauxite residue valorisation opportunity outlined above. Explore how historic mineral discoveries have delivered extraordinary returns, and begin your 14-day free trial today to ensure you're positioned ahead of the broader market when the next major critical minerals announcement lands.