June 22, 2026

Regulatory Architecture for Strategic Mineral Independence

Western democracies face a fundamental challenge in their approach to critical mineral supply chains, particularly when breaking china's rare earth monopoly becomes essential for economic security. Traditional market mechanisms, designed for competitive environments, prove insufficient when confronting state-directed resource strategies that span decades of coordinated industrial policy. The regulatory frameworks governing rare earth elements and strategic minerals must evolve beyond reactive trade measures toward comprehensive industrial architecture that addresses mining, processing, manufacturing, and recycling across integrated value chains.

This transformation requires understanding how regulatory policy can create sustainable alternatives to concentrated supply sources while maintaining economic efficiency and international trade compliance. The challenge extends beyond simple diversification toward building resilient industrial ecosystems capable of withstanding economic warfare tactics and supply chain weaponisation. Furthermore, mining permitting challenges create additional complexity for developing alternative sources.

When big ASX news breaks, our subscribers know first

Understanding the Strategic Mineral Dependency Crisis

Quantifying China's Market Control Across Critical Elements

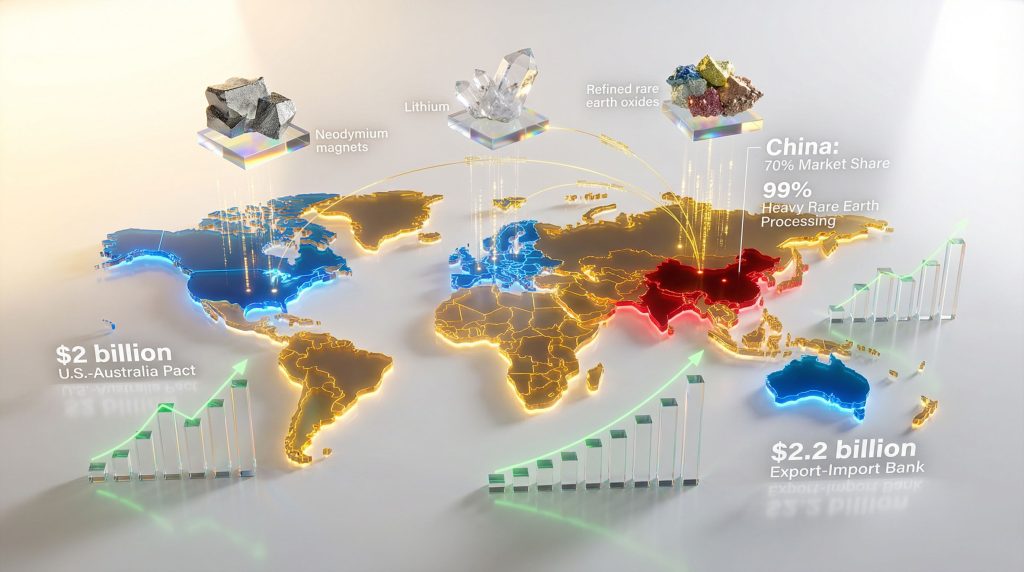

Current market concentration in strategic minerals represents an unprecedented level of single-nation control over industrial inputs essential to modern technology. According to International Energy Agency assessments, China maintains refining capacity between 47% and 87% across lithium, cobalt, graphite, copper, and rare earth elements. This processing dominance creates bottlenecks that extend far beyond raw material extraction, highlighting the urgent need for critical minerals energy security.

The scope of this concentration becomes clear when examining specific mineral categories:

• Light rare earth elements: China controls approximately 85% of global separation capacity

• Heavy rare earth elements: Near-total Chinese processing monopoly through 2023

• Rare earth magnets: Over 90% of permanent magnet production occurs in China

• Battery minerals: Dominant refining positions in lithium carbonate and cobalt sulfate

Malaysia's 4% share of rare earth processing capacity illustrates the concentrated nature of value-added manufacturing. While multiple countries extract rare earth ores, the complex chemical separation processes required to produce usable materials remain geographically concentrated in China due to decades of state investment in industrial infrastructure.

Economic Vulnerabilities in Western Supply Chains

The economic implications of supply chain concentration extend across sectors critical to national security and economic competitiveness. Defence applications require high-purity rare earth elements for guidance systems, communications equipment, and advanced materials. The automotive industry's electric vehicle transition depends on neodymium-iron-boron magnets for motor efficiency.

Renewable energy infrastructure relies on permanent magnets for wind turbine generators and rare earth phosphors for energy-efficient lighting. However, breaking china's rare earth monopoly requires coordinated action across multiple sectors simultaneously.

G7 nations collectively represent approximately 60% of global demand for processed rare earth materials, creating significant leverage for coordinated action. However, this demand concentration also represents vulnerability when supply sources remain geographically concentrated. Import dependency ratios vary significantly across Western nations:

• United States: 80% rare earth import dependency on China

• European Union: 75% combined dependency on Chinese rare earth processing

• Japan: Reduced from 90% to 58% following post-2010 diversification efforts

• South Korea: Maintains high dependency despite domestic technology capabilities

Cost implications of supply disruptions cascade through manufacturing sectors. The 2010 export restrictions demonstrated how rapid price increases for rare earth oxides created production bottlenecks in electronics, automotive, and renewable energy industries.

What Historical Precedents Reveal About Breaking Resource Monopolies?

Japan's Post-2010 Diversification Blueprint

Japan's response to Chinese export restrictions provides the most comprehensive case study of successful supply chain diversification in strategic minerals. Following the diplomatic dispute that triggered export controls, Japan implemented a coordinated strategy combining government investment, private sector partnerships, and diplomatic initiatives across multiple countries and technologies.

The centrepiece of Japan's approach involved the $250 million rescue package for Lynas Corporation in 2011. This investment prevented the collapse of the only significant rare earth producer outside China and secured long-term supply agreements for Japanese manufacturers. The Lynas facility in Malaysia now provides over one-third of Japan's rare earth imports.

Japan's comprehensive approach included multiple components:

• Overseas mining investments: Partnerships with Australian, Canadian, and African rare earth projects

• Technology development: Research into substitution materials and recycling processes

• Industrial cooperation: Joint ventures with processing companies in Southeast Asia

• Strategic stockpiles: Government reserves to buffer against future supply shocks

The quantified results validate this comprehensive strategy. Within a decade, Japan reduced Chinese import dependency from 90% to 58%, while maintaining industrial competitiveness in rare earth-intensive sectors.

Lessons from Previous Resource Diplomacy Conflicts

Historical analysis of resource-based economic conflicts reveals patterns relevant to current strategic mineral challenges. The 1973 oil embargo demonstrated both the vulnerability of concentrated supply chains and the potential for alternative arrangements to emerge under sufficient economic pressure.

However, oil markets possessed characteristics that do not apply to rare earth elements: multiple producing regions, substitutable grades, and established spot trading mechanisms. Consequently, the rare earth market structure presents unique challenges for supply diversification.

Unlike oil or traditional commodities, rare earth elements require specialised processing infrastructure that takes years to construct and commission. Environmental permitting for separation facilities involves complex regulatory processes due to radioactive byproducts in rare earth ores.

Economic impact assessments from the 2010 rare earth embargo reveal the speed with which supply disruptions translate into price volatility. Neodymium prices increased over 1,000% within months, while dysprosium prices rose 2,000%. These price spikes created immediate production constraints for manufacturers dependent on rare earth inputs.

Current Policy Mechanisms for Supply Chain Diversification

Multilateral Financial Frameworks and Investment Commitments

Contemporary policy responses to strategic mineral concentration emphasise coordinated financial commitments across allied nations. The U.S.-Australia critical minerals pact, announced in October 2025, represents the most significant bilateral commitment to date, with each nation pledging $1 billion within six months to accelerate rare earth and battery mineral projects.

In addition to these commitments, the initiative includes a strategic antimony investment component that addresses broader critical mineral dependencies.

| Initiative | Investment Amount | Timeline | Participating Nations | Focus Areas |

|---|---|---|---|---|

| U.S.-Australia Pact | $2 billion | 6 months | Bilateral | Mining, Processing |

| U.S. Export-Import Bank | $2.2 billion | Project pipeline | U.S.-Australia | Project financing |

| Australia Strategic Reserve | $8.5 billion | Multi-year | Australia + Partners | Reserve development |

| G7 Coalition Framework | TBD | Ongoing | 7+ nations | Coordination mechanism |

The Export-Import Bank's $2.2 billion in letters of interest provides financing mechanisms for Australian rare earth and battery metal projects, creating pathways for private sector participation in supply chain development.

Early results from these initiatives show promise for broader international participation. Australia reports increasing interest from European, Japanese, and other Asian partners in collaborative supply chain arrangements.

Price Floor Mechanisms and Market Stabilisation Tools

The U.S.-Australia agreement includes provisions for price floor protections designed to prevent Chinese market manipulation tactics. These mechanisms address the fundamental challenge facing new rare earth projects: the risk of Chinese producers flooding markets with below-cost materials to eliminate competition.

Price floor mechanisms operate through several potential structures:

• Government purchase agreements: Guaranteed offtake at minimum prices for domestic producers

• Import tariffs: Protective barriers against below-cost foreign materials

• Strategic stockpile purchases: Government buying to support price levels

• Production subsidies: Direct support to maintain domestic capacity

Economic rationale for price floors acknowledges that rare earth markets do not function according to traditional competitive models. The combination of high capital requirements, long development timelines, and potential for predatory pricing creates market failures that justify government intervention.

Furthermore, export control measures provide additional tools for addressing unfair trade practices in strategic mineral markets.

Why Mining Alone Cannot Solve the Monopoly Problem

Value Chain Integration Requirements

Breaking china's rare earth monopoly requires understanding that raw material extraction represents only the first stage of complex value chains. Rare earth ores contain multiple elements in varying concentrations, requiring chemical separation processes to produce individual rare earth oxides. These separated materials then undergo further processing into alloys, magnets, and finished components for end-use applications.

Value creation analysis reveals that mining typically represents 10-15% of total rare earth value chains, while processing and manufacturing account for the majority of economic value. China's strategic advantage stems from integrated facilities that combine separation, alloy production, and magnet manufacturing at single industrial sites.

Critical gaps in Western processing infrastructure create bottlenecks that limit the effectiveness of new mining projects. The Mountain Pass rare earth mine in California, for example, ships ore concentrates to China for processing due to the absence of domestic separation facilities.

Magnet manufacturing capacity deficits compound processing limitations. Rare earth magnets require precise alloy compositions and specialised manufacturing techniques developed over decades. Chinese magnet manufacturers benefit from proximity to rare earth processing facilities and integrated supply chains.

Industrial Policy Coordination Across Supply Stages

Successful supply chain independence requires coordinated industrial policy addressing multiple stages simultaneously. Mining exploration and permitting must accelerate to identify and develop new sources of rare earth ores. However, these efforts prove ineffective without corresponding investments in downstream processing and manufacturing capabilities.

Regulatory coordination becomes essential when addressing environmental and safety requirements for rare earth processing. Separation facilities must manage radioactive byproducts inherent in rare earth ores, requiring specialised waste handling and long-term storage solutions.

Strategic stockpile management provides buffer capacity against supply disruptions while supporting market development. Government stockpile purchases can provide guaranteed demand for new producers during market establishment phases.

Technology development initiatives must address both immediate supply chain needs and long-term substitution possibilities. For instance, recent developments in battery recycling breakthrough technologies can recover rare earth elements from end-of-life products, reducing primary supply requirements.

Regulatory Frameworks for Comprehensive Industrial Strategy

Export Control and Technology Transfer Policies

Contemporary export control regimes reflect the increasing recognition of strategic minerals as critical to national security. China's implementation of export controls on rare earth processing technology and equipment creates barriers to Western attempts at building domestic processing capabilities.

Western response mechanisms focus on protecting and developing domestic technological capabilities while limiting dependence on Chinese technical expertise. Export licensing requirements for critical mineral processing technology aim to prevent inadvertent technology transfer to potential competitors.

Intellectual property protection becomes crucial when government investments support private sector technology development. Public-private partnerships in rare earth processing require clear frameworks for protecting proprietary technologies while ensuring government investors receive appropriate returns.

Investment screening mechanisms evaluate foreign participation in critical mineral projects to prevent strategic assets from falling under hostile control. These reviews examine both direct investment and technology transfer arrangements that could compromise supply chain independence objectives.

Investment Incentive Structures and Risk Mitigation

Government investment incentives address the high capital requirements and extended payback periods characteristic of rare earth projects. Tax incentives can include accelerated depreciation for processing facilities, investment tax credits for strategic mineral projects, and reduced corporate tax rates.

Risk-sharing mechanisms help attract private capital to projects that serve strategic objectives but face uncertain commercial prospects. Loan guarantees reduce financing costs for large-scale mining and processing investments.

Public-private partnership structures balance government strategic objectives with private sector efficiency and innovation. Joint ventures allow governments to participate in strategic projects while leveraging private sector technical expertise and market knowledge.

Development banks and export credit agencies provide financing tools specifically designed for large-scale infrastructure projects in strategic sectors. These institutions can offer longer-term financing than commercial banks while maintaining project evaluation standards.

The next major ASX story will hit our subscribers first

How Effective Are Current International Cooperation Models?

G7+ Coalition Coordination Mechanisms

The emergence of coalitions representing approximately 60% of global rare earth demand creates potential for coordinated action that could reshape supply chain structures. However, translating demand concentration into effective supply chain alternatives requires sophisticated coordination mechanisms.

Decision-making structures must balance national sovereignty with collective action effectiveness. Consensus requirements ensure all participants support major initiatives but can create gridlock when national interests diverge.

Resource allocation frameworks become critical when multiple nations contribute to joint projects. Burden-sharing agreements must reflect both capacity to contribute and benefits received from enhanced supply security.

Dispute resolution mechanisms address inevitable conflicts over project priorities, technology sharing, and market access. International arbitration provides neutral forums for resolving disagreements while maintaining coalition unity.

Technology Sharing and Joint Development Programs

Collaborative research and development initiatives offer pathways for sharing the costs and risks of developing alternative technologies and supply sources. Joint R&D programs can accelerate technology development while preventing duplication of efforts across multiple nations.

Substitute material research coordination addresses long-term supply chain independence through technological alternatives to current rare earth applications. Collaborative programs can pool research resources and share development costs.

Shared facility development models offer potential for achieving economies of scale while distributing investment risks and political vulnerabilities. Multinational processing facilities can serve multiple national markets while reducing individual nation investment requirements.

Technical expertise sharing addresses the critical shortage of rare earth processing knowledge outside China. Training programmes and technical exchanges can develop domestic capabilities while strengthening international cooperation.

What Does Success Look Like: Measuring Progress Against Chinese Dominance

Key Performance Indicators for Supply Chain Resilience

Effective measurement of progress toward supply chain independence requires comprehensive metrics that capture both quantitative market share changes and qualitative improvements in supply chain resilience. Import dependency ratios provide baseline measurements of progress but must be supplemented with indicators of supply chain robustness.

Critical performance indicators include:

• Source diversification: Number of countries providing significant supply shares

• Processing capacity: Domestic and allied processing as percentage of demand

• Strategic reserves: Stockpile coverage in months of typical consumption

• Technology independence: Domestic capability for critical processing stages

• Market resilience: Price stability during supply disruption scenarios

Processing capacity development represents a particularly important indicator given China's dominance in value-added manufacturing stages. Metrics should track both absolute capacity development and relative market share changes over time.

Strategic reserve adequacy requires balancing storage costs against supply security benefits. Reserve levels should reflect consumption patterns, supply disruption scenarios, and alternative source development timelines.

Timeline Expectations for Meaningful Market Share Shifts

Realistic timeline expectations acknowledge the complexity and capital intensity of developing alternative rare earth supply chains. Mining projects typically require 7-10 years from discovery to production, while processing facilities need 3-5 years for construction and commissioning.

Short-term objectives (2-3 years) focus on project initiation and financial commitments rather than production results. Key milestones include mining project permitting, processing facility site selection, and technology development partnerships.

Medium-term goals (5-7 years) target operational capacity development and initial production from new sources. Processing facility commissioning and mine production ramp-up provide concrete measures of progress.

Long-term targets (10+ years) envision competitive market alternatives that can function without permanent government support. Sustainable supply chains require private sector viability and market-driven efficiency rather than ongoing subsidisation.

Risk Assessment: Potential Chinese Countermeasures and Policy Responses

Escalation Scenarios in Export Control Regimes

China's October 2025 implementation of enhanced export restrictions demonstrates the dynamic nature of supply chain competition and the potential for escalating economic warfare tactics. Temporary suspensions of rare earth exports to specific countries or companies illustrate how export controls can function as precision tools.

Potential escalation scenarios include expansion of export controls to additional mineral categories beyond rare earths. China's dominance in processing lithium, cobalt, and graphite creates similar leverage opportunities in battery supply chains.

Economic modelling of escalation scenarios suggests that comprehensive Chinese export restrictions could create immediate supply shortages for specific high-technology applications. However, escalation also accelerates Western diversification efforts.

Threshold analysis indicates that Chinese export restrictions become economically counterproductive when they trigger sustained Western investment in alternative supply sources. Gradual pressure maintains dependence while avoiding threshold responses.

Defensive Policy Frameworks Against Market Manipulation

Emergency stockpile activation protocols provide immediate response capabilities for supply disruption scenarios. Automatic triggers based on price movements or quantity restrictions can release strategic reserves without requiring lengthy political decision processes.

Alternative supplier cultivation strategies focus on building relationships with potential supply sources before crises occur. Advance purchase agreements and technical assistance programmes can maintain alternative supply options during normal market conditions.

Diplomatic coordination ensures unified responses to export restriction threats while maintaining international trade law compliance. Coordinated responses increase economic pressure on export-restricting nations while providing mutual support for affected countries.

Counter-escalation policies must balance firm responses with escalation control to prevent resource conflicts from expanding into broader economic warfare. Targeted responses that focus on specific sectors can provide deterrent effects while maintaining overall economic relationships.

Investment Implications and Market Opportunities

Emerging Market Dynamics in Alternative Supply Sources

Investment opportunities in rare earth supply chain development reflect both government policy commitments and long-term demand growth projections. Australia's $8.5 billion project pipeline represents the largest concentration of alternative supply development, driven by geological advantages and political stability.

Canadian rare earth prospects benefit from favourable geology and established mining regulatory frameworks. African projects offer potential for low-cost production but face infrastructure and political risk challenges.

Market dynamics reflect growing recognition that rare earth supply chains require premium pricing to sustain alternative sources. Traditional commodity market pricing models that focus on marginal cost production prove inadequate when supply security considerations justify higher-cost alternatives.

Venture capital and private equity interest in rare earth recycling technologies reflects both environmental objectives and supply chain independence goals. According to industry analysis on breaking china's rare earths monopoly, secondary supply development offers shorter development timelines than primary mining.

Private Sector Participation in Strategic Mineral Security

Government guarantee structures provide risk mitigation that enables private sector participation in strategic projects that might not meet traditional commercial investment criteria. Loan guarantees, purchase agreements, and political risk insurance reduce investment risks.

Market-making mechanisms create liquidity and price discovery for alternative supply sources during market development phases. Government purchasing programmes can provide guaranteed demand while spot trading platforms develop organic market activity.

Investment risk profiles for rare earth projects reflect unique characteristics that differ from traditional mining investments. Regulatory risks include environmental permitting challenges and potential policy changes.

Long-term investment returns depend on sustained government commitment to supply chain independence policies and continued demand growth for rare earth-intensive technologies. Electric vehicle adoption, renewable energy deployment, and defence modernisation programmes provide fundamental demand drivers.

However, breaking china's rare earth monopoly requires sustained commitment across multiple election cycles. Substitution technologies and recycling improvements could affect long-term demand projections, requiring investors to carefully evaluate technological developments alongside political commitments.

Investment decisions regarding rare earth and critical mineral projects involve substantial risks including commodity price volatility, regulatory changes, and geopolitical factors. This analysis is for informational purposes only and does not constitute investment advice. Potential investors should conduct thorough due diligence and consult qualified professionals before making investment decisions.

Looking to Capitalise on Strategic Mineral Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including critical minerals and rare earth element prospects that could benefit from the emerging regulatory frameworks and government investment initiatives. Access Discovery Alert's discoveries page to explore how major mineral discoveries have historically generated substantial returns for early investors, then start your 30-day free trial to position yourself ahead of this rapidly evolving market.