May 21, 2026

Understanding Resource Nationalism in Battery Metal Supply Chains

Zimbabwe lithium export ban conditions represent a sophisticated approach to resource governance that fundamentally challenges traditional commodity trading models. Resource-rich nations across Africa increasingly recognise the strategic disadvantage of exporting unprocessed materials whilst importing value-added products. This fundamental asymmetry in global commodity trade has prompted sophisticated policy responses targeting higher value capture within domestic borders.

Battery metals, particularly lithium, represent a critical intersection where traditional mining industry evolution meets modern energy transition imperatives. The global lithium supply chain operates through distinct stages, each capturing progressively higher margins.

Raw spodumene concentrate extraction represents approximately 5-10% of final product value, whilst intermediate chemical processing captures 20-40% value addition. This economic reality drives policy frameworks designed to shift value creation upstream to producing nations rather than downstream processing centres.

Zimbabwe's recent regulatory framework exemplifies this strategic repositioning, establishing conditions that fundamentally alter traditional commodity export models in favour of domestic industrial development. Furthermore, the policy represents a calculated approach to resource governance that balances immediate revenue needs with long-term economic transformation objectives.

When big ASX news breaks, our subscribers know first

Zimbabwe's Phased Regulatory Framework for Lithium Value Capture

Zimbabwe implemented a comprehensive suspension of lithium concentrate exports on February 26, 2026, affecting Africa's largest lithium production sector. The halt followed concerns about operational transparency and revenue leakage within the sector. However, underlying motivations reflect broader continental trends toward resource beneficiation policies.

The regulatory conditions for export resumption establish a sophisticated multi-phase approach combining immediate compliance requirements with long-term processing commitments. In addition, this framework operates through several integrated mechanisms that create unprecedented zimbabwe lithium export ban conditions.

Immediate Compliance Requirements:

• Financial Transparency: Mandatory publication of annual financial statements

• Operational Standards: Adherence to enhanced labour, safety, and environmental regulations

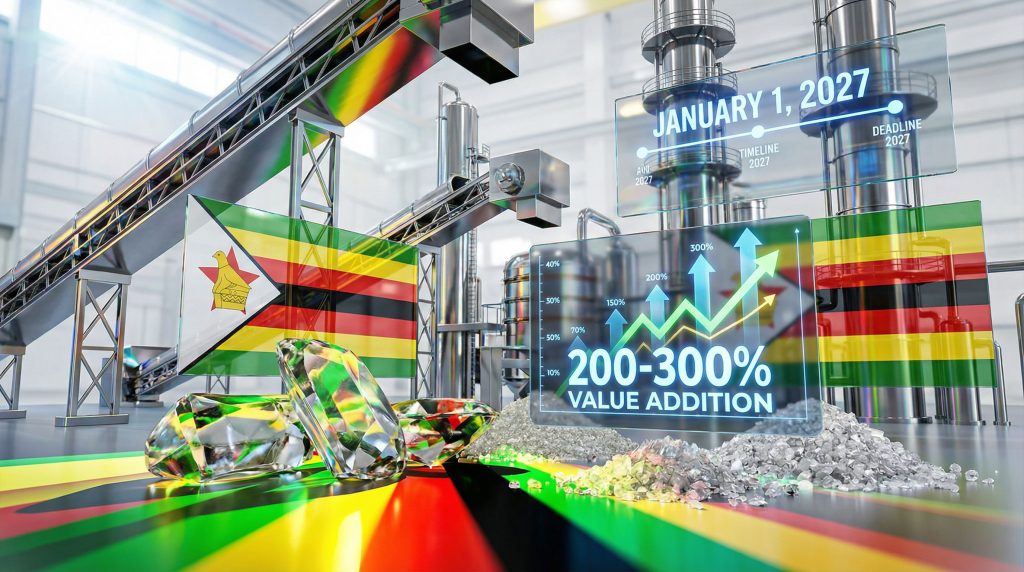

• Export Taxation: 10% levy on concentrate exports until January 2027

• Quota Allocations: Individual export limits per producer (specific volumes communicated separately)

Long-Term Processing Mandates:

• Infrastructure Commitments: Written agreements for lithium sulphate plant construction before January 1, 2027

• Complete Export Ban: Full prohibition on concentrate shipments effective January 1, 2027

• Processing Requirements: Mandatory conversion to intermediate chemical products for export eligibility

The nine-month implementation window from the April 2, 2026 announcement to the January 2027 deadline creates significant operational pressure. Consequently, this timeline reflects careful calibration between regulatory enforcement and practical implementation constraints.

Comparative Analysis of Global Processing Mandate Policies

Zimbabwe's approach follows established patterns in resource-rich jurisdictions seeking value chain integration. Indonesian nickel growth challenges provide valuable lessons for understanding how export restrictions drive downstream processing investment whilst maintaining long-term resource sector viability.

Similar frameworks have emerged across strategic mineral producers, reflecting growing recognition that raw material exports perpetuate economic dependency. For instance, the Democratic Republic of Congo has implemented cobalt processing requirements, whilst Ghana and Tanzania have introduced export restrictions on bauxite and enhanced gold monitoring respectively.

Technical Processing Economics and Value Addition

Converting spodumene concentrate into lithium sulphate represents a critical intermediate step in the battery materials supply chain. This processing stage typically operates through acid leaching, impurity removal, and crystallisation processes that achieve 85-90% lithium recovery rates from concentrate feedstock.

The economic transformation achieved through intermediate processing is substantial. Furthermore, whilst raw spodumene concentrate trades at approximately $1,500-$2,500 per tonne, lithium sulphate intermediate products command significantly higher valuations, creating processing margins that justify infrastructure investment even under regulatory mandates.

Processing Infrastructure Investment Analysis:

| Investment Component | Capital Requirement | Operational Impact |

|---|---|---|

| Plant Construction | $300-500 million typical range | 24-36 month development timeline |

| Chemical Processing Equipment | 40-50% of total capex | Specialised acid leaching and crystallisation systems |

| Environmental Controls | 15-20% of total capex | Tailings management and emission control |

| Skilled Labour Development | Ongoing operational expense | Technical training and retention programmes |

Zhejiang Huayou Cobalt's $400 million lithium sulphate facility in Zimbabwe exemplifies how major operators are adapting to processing requirements. This investment demonstrates that regulatory compliance costs, whilst substantial, remain economically viable within current lithium market dynamics.

Chinese Supply Chain Dominance and Strategic Adaptation

Chinese companies control approximately 80% of Zimbabwe's lithium production capacity, reflecting broader Chinese strategic positioning in global battery metal supply chains. Major operators include Zhejiang Huayou Cobalt, Sinomine, Chengxin Lithium Group, Yahua, and Tsingshan Holding Group. In addition, zijin global expansion strategy demonstrates how Chinese mining companies are adapting to new regulatory environments.

In 2025, Zimbabwe exported 1.128 million tons of lithium-bearing spodumene concentrate to China, representing roughly 15% of China's total lithium concentrate imports. This significant supply relationship creates both leverage and vulnerability for Zimbabwean policy makers whilst forcing Chinese operators into fundamental strategic adaptations.

Operational Model Transformation Requirements

The regulatory framework forces Chinese operators to choose between maintaining market access through processing investment or exiting Zimbabwe operations entirely. Early evidence suggests most major players view processing requirements as navigable rather than prohibitive, with several announcing significant infrastructure commitments.

Confirmed Chinese Company Adaptations:

• Zhejiang Huayou Cobalt: $400 million lithium sulphate processing plant completed or under construction

• Sinomine: Processing facility investment announced (specific amounts not disclosed)

• Yahua: Similar processing infrastructure commitments confirmed

These adaptations represent fundamental shifts from pure extraction models toward integrated extraction-and-processing operations. Consequently, they require substantial additional capital deployment and operational complexity management.

Export Quota Strategy and Revenue Optimisation

Zimbabwe's export quota system serves multiple strategic functions within the broader regulatory framework. Individual quota allocations provide immediate revenue generation whilst creating controlled pressure for processing investment. This graduated approach allows companies transition time whilst ensuring Zimbabwe captures increasing value over the implementation period.

The 10% export tax on concentrates generates government revenue during the transition phase whilst creating economic incentives for processing investment. Companies can reduce their effective tax burden by shifting toward processing operations, aligning private sector incentives with national policy objectives.

The implementation of zimbabwe lithium export ban conditions creates a sophisticated balance between immediate revenue needs and long-term industrial development goals. Lithium industry tax breaks in other jurisdictions provide comparative context for understanding how fiscal incentives can drive sector development.

Market Positioning and Regional Competition

Zimbabwe competes with established lithium producers including Australia, Chile, and Argentina in global markets. By mandating intermediate processing, Zimbabwe aims to differentiate its market position from pure commodity exporters toward higher-value chemical intermediate suppliers.

This positioning strategy targets specific segments of the battery materials supply chain where Zimbabwe can capture enhanced margins whilst building domestic industrial capacity. However, the approach recognises that competing solely on raw material pricing offers limited long-term economic benefits compared to value-added product strategies.

Implementation Timeline Analysis and Market Implications

The January 1, 2027 processing facility deadline creates significant operational pressure for compliance. Lithium sulphate plant construction typically requires 24-36 months from initial planning to operational status. Consequently, companies must accelerate development timelines or risk losing export access entirely.

Critical Implementation Milestones:

- Immediate Phase (April-December 2026): Quota-based exports with 10% taxation

- Transition Phase (January-December 2027): Processing facility construction and commissioning

- Full Implementation (January 2028+): Mandatory processing for all export activities

Market dynamics during this transition period will likely reflect supply chain uncertainty, potential price volatility, and investment flows toward processing infrastructure. Companies successfully meeting processing deadlines may gain competitive advantages through preferential access to Zimbabwe's lithium resources.

Furthermore, the development of battery-grade lithium refinery infrastructure in other regions provides valuable insights into the technical and financial requirements for successful implementation.

The next major ASX story will hit our subscribers first

Continental Mining Policy Convergence and Future Frameworks

Zimbabwe's lithium export conditions align with broader African Union initiatives promoting resource beneficiation and industrial development. This policy convergence suggests similar frameworks may emerge across other strategic mineral producers, potentially reshaping global supply chain structures for battery metals.

The success or failure of Zimbabwe's approach will likely influence policy development in other resource-rich African nations. Positive outcomes could accelerate adoption of similar processing mandates, whilst implementation challenges might prompt more graduated approaches to value addition requirements.

Regional Policy Development Indicators:

• Democratic Republic of Congo: Enhanced cobalt processing requirements under development

• Ghana: Bauxite export restrictions promoting domestic aluminium industry development

• Tanzania: Gold export monitoring and value addition initiatives

• Nigeria: Mineral processing incentives and export restriction evaluations

These zimbabwe lithium export ban conditions represent a sophisticated evolution in resource governance that other African nations are closely monitoring. The implementation outcomes will significantly influence continental mining policy development.

Investment Climate Implications and Risk Assessment

Zimbabwe's regulatory framework creates both opportunities and risks for mining sector participants. Companies investing in processing infrastructure gain preferential access to resources and higher-margin products. However, those unable to meet processing requirements face market exclusion.

Financial and Operational Risk Factors

The compressed implementation timeline creates execution risks for processing facility development. Construction delays, permitting challenges, or technical complications could result in temporary or permanent loss of export access for affected operators.

However, companies successfully navigating the transition may benefit from competitive moats through processing infrastructure ownership and preferential resource access. This dynamic creates strong incentives for early compliance whilst penalising delayed adaptation strategies.

Investment Evaluation Framework:

• Capital Requirements: $300-500 million typical processing facility investment

• Revenue Protection: Maintained access to Zimbabwe's lithium resources

• Margin Enhancement: Higher-value intermediate product sales versus raw concentrate

• Competitive Positioning: First-mover advantages in Zimbabwean processing sector

The conditions for lifting the ban outlined by mining authorities provide clear guidance for industry participants navigating compliance requirements. These conditions establish a comprehensive framework that balances immediate operational needs with long-term development objectives.

Global Battery Metal Supply Chain Resilience

Zimbabwe's processing requirements encourage geographic diversification of lithium intermediate production, reducing over-concentration in traditional processing centres. This diversification aligns with Western supply chain security objectives whilst creating alternative sources of battery-grade materials.

The policy framework also demonstrates how resource-rich nations can successfully leverage their mineral endowments for broader economic development rather than accepting commodity price exposure as the primary value capture mechanism.

Market participants must adapt to increasingly sophisticated resource governance frameworks that prioritise domestic value creation over traditional export-focused models. Furthermore, benchmark minerals analysis suggests these conditions represent a carefully calibrated approach to achieving balanced development outcomes.

This evolution requires fundamental reassessment of global supply chain strategies and investment allocation decisions across the battery materials sector. The successful implementation of these zimbabwe lithium export ban conditions could establish a new paradigm for resource governance across strategic mineral producing nations.

This analysis is provided for informational purposes and does not constitute investment advice. Commodity markets involve significant risks including price volatility, regulatory changes, and operational uncertainties. Readers should conduct independent research and consult qualified professionals before making investment decisions.

Are You Tracking Strategic Mineral Policy Changes That Could Impact Your Portfolio?

Zimbabwe's lithium export restrictions exemplify how resource nationalism is reshaping global supply chains, creating significant opportunities for investors who can identify companies adapting to new regulatory frameworks. Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on ASX mineral discoveries and policy developments, helping investors capitalise on market movements before they become mainstream news. Begin your 14-day free trial today to ensure you're positioned ahead of critical industry shifts that could affect your investment returns.