June 4, 2026

The Strategic Economics Behind Rhenium Supply Chains

Global supply chain vulnerabilities have emerged as defining features of modern economic statecraft, where single minerals can determine national security outcomes. The ongoing negotiations between the U.S. approaches Chile for critical mineral supply demonstrate how rare earth dependencies reshape international relations beyond traditional trade frameworks. Furthermore, these developments highlight the interconnected nature of critical minerals energy security in the modern economy.

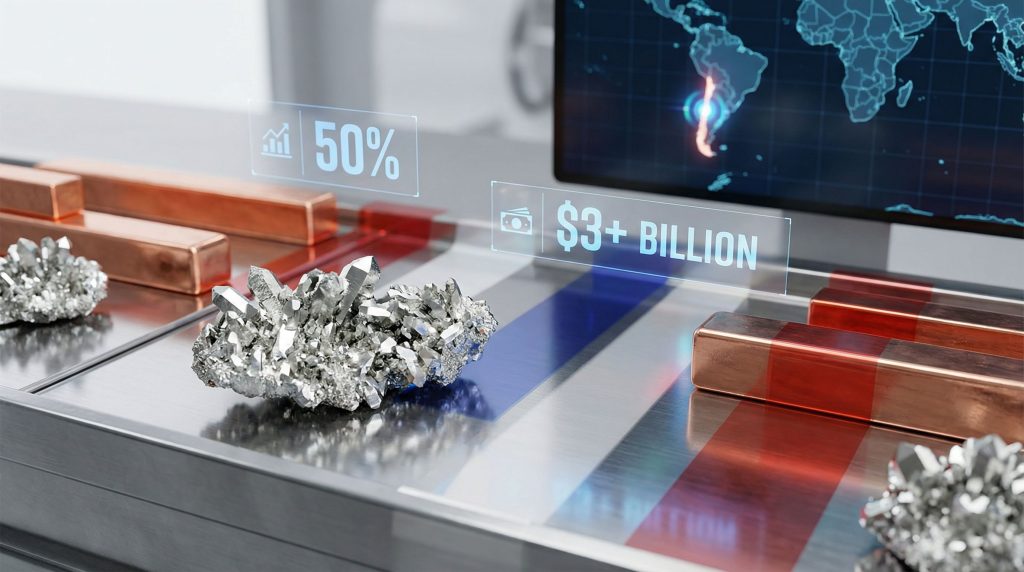

Rhenium occupies a unique position within critical mineral discussions due to its absolute strategic necessity. With a melting point exceeding 3,180°C, this element enables military and aerospace systems to function under extreme conditions where no alternatives exist. Chile's dominance of approximately 50% of global rhenium production creates what economists classify as a strategic chokepoint in defense manufacturing supply chains.

The mineral's extraction as a copper mining byproduct introduces additional complexity into supply planning. Unlike primary mining operations where production can scale according to demand, rhenium availability depends entirely on copper extraction volumes. This dual dependency means that fluctuations in copper markets directly impact defense-critical rhenium supplies, regardless of military procurement requirements.

Key Economic Factors:

- Chile controls 50% of global rhenium production through copper mining operations

- No commercial substitutes exist for high-temperature aerospace applications

- Price elasticity becomes irrelevant due to absolute material requirements

- Defense contractors cannot pivot to alternative materials without system redesigns

What Makes Rhenium Different from Other Critical Minerals?

Traditional critical mineral discussions often focus on supply concentration risks that can theoretically be addressed through substitution or technological innovation. Rhenium represents a fundamentally different category of strategic dependency where material science limitations eliminate substitution pathways entirely.

The comparison with other strategic materials reveals rhenium's unique vulnerability profile:

| Mineral | Substitution Potential | Production Concentration | Strategic Risk Level |

|---|---|---|---|

| Lithium | Sodium-ion alternatives emerging | 70% Australia/Chile/China | Moderate |

| Rare Earth Elements | Limited alternatives for some uses | 65% China dominance | High |

| Cobalt | Partial nickel substitution possible | 65% Democratic Republic of Congo | High |

| Rhenium | Zero substitution available | 50% Chile control | Absolute |

Unlike lithium battery applications where sodium-ion technology offers emerging alternatives, or rare earth permanent magnets where design modifications can reduce dependence, rhenium applications in jet engines and military turbines cannot utilize substitute materials without fundamental system redesigns costing hundreds of billions across military fleets.

Technical Performance Requirements:

- Rhenium-tungsten alloys maintain structural integrity above 2,500°C operating temperatures

- Alternative materials like molybdenum alloys degrade significantly above 1,500°C in oxygen environments

- Ceramic matrix composites require 10-15 year development cycles before military deployment approval

- Existing military aircraft fleets totaling over 5,000 combat aircraft designed around rhenium specifications

The F-22 Raptor's Pratt & Whitney F119-PW-100 engines exemplify this dependency, requiring rhenium alloys to achieve afterburner temperatures of 2,200°C during supersonic flight operations. SpaceX Raptor 3 engines similarly depend on rhenium components rated for 3,500+ combustion cycles in space launch applications.

Why Is the U.S. Prioritising Latin American Mineral Partnerships?

The Trump administration's mineral diplomacy represents a systematic response to China's processing dominance across critical material supply chains. Rather than competing directly in processing capacity where China maintains decade-long operational advantages, the strategy focuses on developing parallel supply networks with democratic allies. Additionally, this approach aligns with the defence-critical materials strategy being implemented globally.

The $3 billion U.S.-Australia critical minerals agreement established precedent for these partnerships, potentially accessing $53 billion in theoretical mineral wealth through direct investment in extraction and processing infrastructure. This model now extends to Latin American negotiations, where geographic proximity and political alignment offer additional strategic advantages.

Regional Mineral Production Context:

| Country | Primary Resources | Global Market Share | Strategic Applications |

|---|---|---|---|

| Chile | Copper, Lithium, Rhenium | 28% lithium, 50% rhenium | Defence, Energy Storage, Aerospace |

| Peru | Copper, Silver, Zinc | 10% copper, 21% silver | Industrial Manufacturing, Electronics |

| Bolivia | Lithium, Silver | 11% lithium reserves | Battery Technology, Electronics |

| Brazil | Iron Ore, Niobium | 20% iron ore, 70% niobium | Steel Production, Aerospace Alloys |

Investment Architecture and Economic Benefits

Latin American partnerships offer structural advantages over Asian supply chains through reduced transportation costs and aligned governance frameworks. Western Hemisphere sourcing cuts logistics expenses by 40-50% compared to Asian alternatives while providing greater supply security through democratic institutions and rule of law protections.

The proposed supply chain architecture encompasses:

- Raw Material Extraction – Chilean, Peruvian, and Bolivian mining operations

- Regional Processing Facilities – Western Hemisphere processing to reduce transport costs

- Technology Transfer Programmes – U.S. firms licensing advanced extraction technologies

- Long-term Offtake Agreements – Government commitments for defined mineral quantities

- Strategic Integration – Priority access for defence applications before commercial markets

Consequently, these partnerships represent a big pivot in critical minerals sourcing strategy, moving away from traditional Chinese-dominated supply chains.

How Do Strategic Mineral Reserves Impact Economic Security?

President Trump's announcement of a $12 billion strategic reserve for critical metals and minerals represents economic insurance against supply chain disruptions that could cripple defence manufacturing and industrial production. This approach mirrors the Strategic Petroleum Reserve concept but extends across multiple critical materials including rare earths, lithium, cobalt, nickel, and graphite.

Strategic reserves fundamentally alter market dynamics by creating artificial demand floors that reduce price volatility and encourage domestic production investment. The reserve system also provides negotiating leverage in bilateral agreements by demonstrating reduced vulnerability to supply manipulation. However, the US-China trade war impact continues to influence these strategic calculations.

Economic Security Benefits:

- Price Stabilisation – Buffer stocks reduce market volatility during supply disruptions

- Industrial Continuity – Manufacturing operations continue during international supply interruptions

- Negotiating Power – Reduced dependency strengthens bilateral trade negotiations

- Investment Incentives – Guaranteed government purchases encourage domestic production development

The reserve system addresses scenarios where hostile nations could weaponise critical mineral exports to coerce policy changes or disrupt military operations. By maintaining strategic stockpiles, the U.S. can sustain defence production and industrial operations through extended supply disruptions.

Market Impact and Industrial Policy Integration

These mineral partnerships represent convergence between trade policy, national security strategy, and industrial development objectives. Unlike traditional trade agreements focused primarily on economic efficiency, these frameworks prioritise strategic considerations alongside market dynamics. Moreover, these changes reflect the broader mining industry evolution occurring globally.

The integration spans multiple policy areas:

- Defence Procurement – Military specifications ensuring strategic material availability

- Clean Energy Transition – Battery and renewable energy technology material requirements

- Advanced Manufacturing – Semiconductor and aerospace industry material dependencies

- Technological Sovereignty – Reducing foreign control over critical technology inputs

What Are the Long-Term Economic Implications?

The U.S.-Chile rhenium negotiations signal broader restructuring of global commodity markets away from Chinese-dominated processing toward diversified partnerships with democratic allies. This shift creates new investment flows into Western Hemisphere mining while potentially reducing Chinese market leverage over strategic materials. Furthermore, U.S. innovators are actively boosting critical mineral supply through technological advancement.

Projected Market Changes:

- Increased foreign direct investment in Latin American mining infrastructure

- Development of alternative processing capabilities outside China

- Enhanced bilateral trade relationships with mineral-rich democratic nations

- Reduced Chinese ability to use export restrictions as geopolitical leverage

Regional Economic Development Opportunities

Chile's mineral wealth positions the nation as a critical partner in U.S. economic security strategy, creating opportunities for enhanced bilateral cooperation beyond traditional trade relationships. The partnership model could expand across Latin America, creating an integrated Western Hemisphere mineral supply network competing directly with Chinese influence. In fact, Chile and the US are already eyeing collaboration on critical minerals in various sectors.

Development Benefits:

- Technology Transfer – Advanced extraction and processing technologies from U.S. partners

- Infrastructure Investment – Port, railway, and transportation corridor development

- Workforce Development – Training programmes for advanced mining and processing operations

- Economic Diversification – Reduced dependence on single-commodity exports

Challenges and Risk Assessment

While reducing Chinese dependency, these partnerships create new forms of economic interdependence requiring careful management to avoid replacing one vulnerability with another. Market efficiency may be sacrificed for security benefits, potentially increasing costs for end consumers while providing strategic advantages.

Critical Risk Factors:

- Political Stability – Changes in Latin American governments could affect partnership agreements

- Environmental Regulations – Mining expansion faces increasing environmental scrutiny

- Infrastructure Development – Processing facilities require years of construction and operational ramp-up

- Cost-Security Trade-offs – Strategic partnerships may increase material costs compared to market alternatives

The success of these partnerships depends on balancing economic efficiency with strategic security while maintaining bipartisan political support through changing administrations. Congressional backing and long-term commitment will be essential for attracting private investment in alternative supply chains.

Investment Disclaimer: The analysis presented in this article is for informational purposes only and should not be considered as investment advice. Commodity markets, including critical minerals, involve significant risks and volatility. Investors should conduct their own research and consult with qualified financial advisors before making investment decisions. Geopolitical developments and supply chain disruptions can significantly impact mineral prices and related investments.

Are You Tracking Critical Mineral Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including critical minerals essential to defence and clean energy applications. With supply chain vulnerabilities reshaping global markets, subscribers gain immediate access to actionable investment opportunities as major discoveries are announced. Begin your 14-day free trial today to position yourself ahead of evolving mineral market dynamics.