June 24, 2026

The Hidden Shift Reshaping the World's Largest Mining Portfolios

For most of the past century, the economics of large-scale mining were relatively straightforward: dig iron ore, smelt copper, ship coal. The commodity mix that powered industrial civilisation rewarded scale, logistics mastery, and geological luck. However, the energy transition has introduced a structural disruption that cannot be absorbed through operational efficiency alone. The input requirements of a battery-powered economy are fundamentally different from those of a fossil-fuel economy, and the miners who fail to reposition their portfolios risk becoming legacy operators in a market that is rapidly rewriting its own hierarchy.

Lithium sits at the centre of this realignment. Once considered a niche specialty chemical used in ceramics, lubricants, and mood-stabilising medication, lithium carbonate and lithium hydroxide have become the electrochemical backbone of the electric vehicle revolution. The scale of this transformation has been rapid enough to force diversified mining giants into uncomfortable strategic territory: competing directly with agile, purpose-built lithium producers for market share, customer relationships, and long-term relevance.

Rio Tinto's articulation of lithium as its fastest-growing division is one of the clearest signals yet that the institutional recalibration of mining portfolios is no longer theoretical. It is operational. The Rio Tinto lithium growth strategy represents a defining shift for one of the world's most powerful miners.

When big ASX news breaks, our subscribers know first

From Iron Ore Dependence to Battery Metal Ambition

Rio Tinto built its modern financial identity on iron ore. The Pilbara operations in Western Australia generate enormous cash flows and have historically subsidised the company's exploration and diversification efforts. Copper has played a secondary but increasingly important role as decarbonisation drives demand for electrical infrastructure. Both commodities, however, face structural growth ceilings that lithium, at its current stage of adoption, does not.

Global electric vehicle penetration continues to climb. Each battery electric vehicle requires roughly 5 to 15 kilograms of lithium depending on battery chemistry and pack size, compared to near-zero lithium consumption in a combustion engine vehicle. Grid-scale energy storage systems compound this demand trajectory further. The mathematical relationship between EV adoption forecasts and lithium consumption growth creates a demand curve that few bulk commodities can match.

It is precisely this asymmetry that has driven Rio Tinto's internal classification of lithium as its highest-priority growth segment, distinct from its established but more mature iron ore and copper divisions.

The Arcadium Acquisition: Counter-Cyclical Capital Deployment at Scale

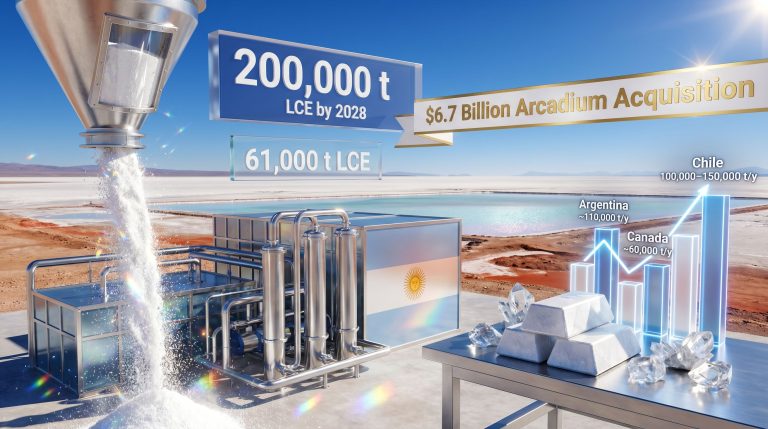

The $6.7 billion acquisition of Arcadium Lithium, completed in March 2025, was the defining strategic move that transformed Rio Tinto from a lithium bystander into a credible large-scale producer almost overnight. The transaction provided something that organic exploration rarely delivers on a useful timeline: an immediately operational, geographically diversified asset base.

What Arcadium brought to the table extended well beyond mineral reserves:

- Producing mines and processing facilities across four continents

- An established commercial customer network that includes Tesla and other major battery and EV manufacturers

- Proprietary knowledge in direct lithium extraction (DLE) technology, which Rio Tinto identified as a central strategic rationale for the transaction

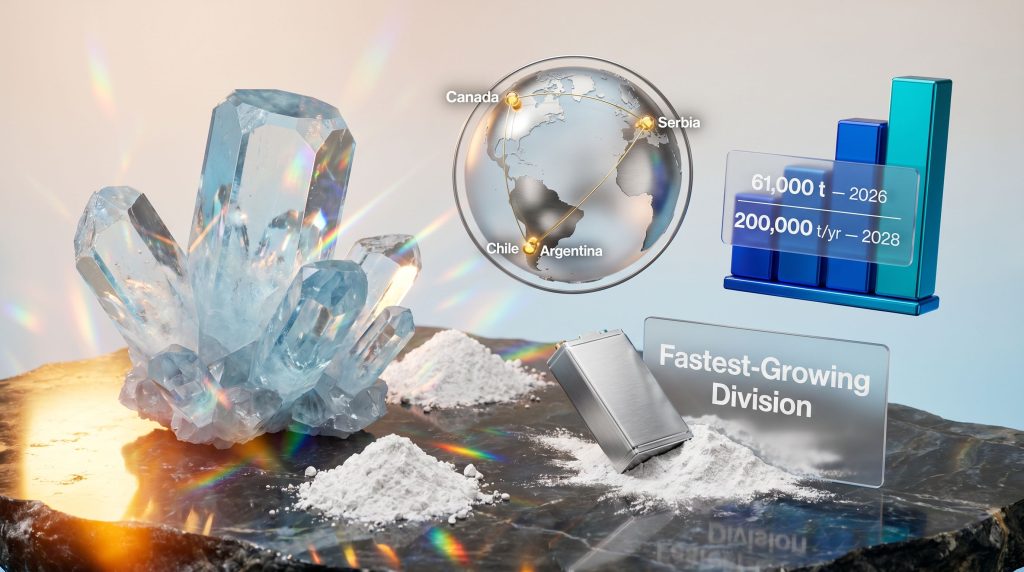

- A development pipeline spanning Argentina, Canada, Chile, and other jurisdictions

The timing of the acquisition is worth examining closely. The lithium market downturn had already forced a wave of industry layoffs, project deferrals, and asset write-downs across the sector. Rio Tinto moved into this environment with conviction, acquiring at a point of market stress rather than market euphoria. This counter-cyclical approach — paying for assets when the commodity is temporarily out of favour — is a well-established playbook among major diversified miners, and the Arcadium deal fits squarely within that tradition.

The Arcadium acquisition illustrates a fundamental truth about large-scale mining M&A: the best entry points rarely feel comfortable at the time. Buying into a distressed market requires institutional conviction that the long-term demand thesis will outlast the short-term price cycle.

Organisational Structure and the Philosophy of Operational Delivery

Lithium's placement within Rio Tinto's Aluminium and Lithium business unit reflects a deliberate organisational logic. Both commodities share characteristics relevant to the energy transition, both require sophisticated processing infrastructure, and both serve end markets that are increasingly shaped by decarbonisation policy. The combined divisional structure is designed to extract operational efficiencies across shared functions.

Leading this division is Jérôme Pécresse, a former General Electric executive who joined Rio Tinto in 2023 and sits on the company's executive committee. His stated operational mandate is unambiguous: deliver projects on time and on budget. In an industry where cost overruns and schedule delays have historically eroded shareholder value at the project level, this focus on execution discipline is both commercially rational and strategically essential.

Pécresse has indicated that execution discipline currently occupies the overwhelming majority of his operational focus, underscoring how seriously Rio Tinto is treating the delivery challenge embedded in its growth ambitions.

The Four-Continent Asset Portfolio: Where the Production Will Come From

| Geography | Asset / Project | Operational Stage | Capacity Potential |

|---|---|---|---|

| Argentina | Rincon Project | Starter plant operational at 3,000 t/yr | Up to 110,000 t/yr potential |

| Canada | Greenfield development | Advancing toward production | ~60,000 t/yr targeted by 2028-2030 |

| Chile | Salar de Maricunga / Salares Altoandinos (JV with Codelco/ENAMI) | Development phase | To be confirmed |

| Serbia | Jadar Project | Care and maintenance | Suspended pending permitting resolution |

The Argentina and Canada assets are currently the primary growth drivers. Furthermore, both have been specifically identified by Rio Tinto's leadership as projects designed to remain economical even if lithium prices experience another significant downturn. This emphasis on low-cost, resilient economics reflects a maturity of approach that differentiates Rio Tinto from producers whose viability depends on sustained high spot prices.

What Role Does Chile Play?

Chile's lithium resources represent a significant component of Rio Tinto's longer-term production ambitions. The joint venture with Codelco and ENAMI at Salar de Maricunga positions Rio Tinto within one of the world's most lithium-rich jurisdictions, adding geographic resilience to the overall portfolio.

The Production Roadmap: What 200,000 Tonnes Actually Means

Rio Tinto has set two key production milestones that define the near-to-medium term trajectory of the Rio Tinto lithium growth strategy:

- At least 61,000 tonnes of lithium production targeted for 2026

- 200,000 tonnes per year of capacity to be established by 2028, contingent on sufficient market demand

The conditional language attached to the 2028 target is significant. The distinction between installed capacity and actual output is not semantic. Rio Tinto is signalling that it will build infrastructure capable of producing at scale, but will calibrate actual production volumes to match market conditions rather than flooding an oversupplied market to chase volume rankings.

This positions Rio Tinto among the upper tier of global lithium producers. For context, Albemarle, the current world leader in lithium production, serves as the benchmark against which all other producers are measured. Notably, Rio Tinto's broader strategic focus makes clear that displacing Albemarle from the top position is not the primary objective.

Rio Tinto's divisional leadership has made clear that the company's ambition is not to achieve a specific production ranking, but to build a portfolio of assets large enough to maintain genuine long-term relevance with major customers. This represents a fundamentally different growth philosophy from pure-play producers who compete primarily on volume.

The next major ASX story will hit our subscribers first

Direct Lithium Extraction: The Technology Bet That Could Redefine the Cost Curve

Of all the elements within Rio Tinto's lithium strategy, Direct Lithium Extraction (DLE) may carry the greatest long-term implications, both for the company and for the broader lithium industry.

Conventional brine extraction relies on pumping lithium-rich subsurface water into large evaporation ponds, where solar energy slowly concentrates the brine over periods of 12 to 24 months. The process is land-intensive, water-consumptive in some configurations, and delivers lithium recovery rates of roughly 50%. In regions like the Atacama Desert, where water scarcity is an environmental and social flashpoint, these limitations are not merely operational — they are existential for project social licence.

DLE fundamentally changes this equation:

| Factor | Conventional Evaporation | Direct Lithium Extraction |

|---|---|---|

| Processing Timeframe | 12 to 24 months | Days to weeks |

| Water Consumption | Very high | Significantly reduced |

| Lithium Recovery Rate | Approximately 50% | Up to 90% or higher |

| Surface Area Required | Extensive | Compact footprint |

| Deployment Flexibility | Geographically constrained | More adaptable across brine types |

DLE uses selective adsorption, ion exchange, or membrane-based processes to extract lithium directly from brine with dramatically higher efficiency and speed. The technology effectively unlocks resource potential that evaporation ponds cannot economically access, particularly in brines with lower lithium concentrations or challenging co-ion compositions.

Rio Tinto views DLE as central to developing competitive, low-environmental-impact operations across its South American portfolio, with at least one DLE project expected to reach commercial launch within a few years of 2026.

How Does DLE Affect Hard-Rock Producers?

A less frequently discussed implication of DLE's advancement is the competitive pressure it could place on spodumene extraction operations, primarily concentrated in Western Australia. Spodumene processing requires energy-intensive conversion to lithium hydroxide and carries higher operating costs per tonne of recoverable lithium. If DLE reaches cost competitiveness at scale, it could structurally compress the economics of hard-rock lithium over the medium term.

In addition, underground lithium mining operations in Australia face a different set of cost and recovery challenges compared to brine-based DLE projects, further highlighting why Rio Tinto's technology investment carries such significant strategic weight.

Capital Discipline in a Volatile Market

Rio Tinto's broader strategic reset under current leadership has introduced tighter capital allocation frameworks across all divisions. Lithium is not exempt from this discipline. The financial architecture of the company's growth strategy reflects a clear set of targets:

| Financial Metric | Target Detail |

|---|---|

| EBITDA Growth | 40 to 50% increase targeted by 2030 |

| Production Volume Growth | Approximately 20% copper-equivalent increase |

| Capital Expenditure Trajectory | Below US$10 billion per year from 2028 onward |

| Lithium Production in 2026 | Minimum 61,000 tonnes |

| Lithium Capacity Target in 2028 | 200,000 tonnes per year |

Lithium investment is benchmarked against the returns available from iron ore and copper development. Projects that cannot demonstrate credible low-cost economics, even under adverse price scenarios, will not receive capital allocation. This framework guards against the speculative overcommitment that damaged many lithium producers during the 2022 to 2024 price cycle.

Rio Tinto has also stated that it is not currently pursuing additional lithium acquisitions beyond the Arcadium integration, signalling confidence that the existing asset base is sufficient to achieve scale targets without diluting capital discipline.

The Jadar Suspension: A Masterclass in Geopolitical Risk

The Jadar lithium project in Serbia, valued at approximately $2.4 billion, represents Rio Tinto's most prominent permitting setback and one of the most instructive case studies in sovereign permitting risk in recent mining history. The Serbian government's cancellation of permits forced Rio Tinto to place the project in care and maintenance, effectively freezing one of Europe's largest identified lithium deposits indefinitely.

Several lessons emerge from the Jadar experience that have relevance far beyond Rio Tinto's portfolio:

- Community opposition can override technical and economic merit: Jadar's resource quality was never in question. The project's suspension was driven by public resistance and political dynamics.

- Jurisdictional diversification is not optional: Over-concentration in a single country or regulatory environment creates binary risk that can materially alter a company's production outlook.

- Care and maintenance is not closure: Rio Tinto has maintained the project's optionality, leaving open the possibility of permitting resolution if the political environment shifts.

- European lithium supply remains elusive: Jadar's suspension illustrates the difficulty of establishing domestic battery metal supply chains within Europe, despite strong policy interest in reducing import dependence.

Competitive Landscape: How Rio Tinto Fits Among Lithium's Major Players

| Producer | Primary Strategic Approach | Key Asset Concentrations | Current Market Position |

|---|---|---|---|

| Rio Tinto | Acquisition-led, DLE-focused, contract-based pricing | Multi-continent Arcadium portfolio | Rapidly scaling post-acquisition |

| Albemarle | Pure-play diversified, global footprint | Chile, Australia, United States | World's largest lithium producer |

| SQM | Brine-dominant, Chilean concentration | Atacama, Codelco partnership | Major producer navigating transition |

| Glencore | Diversified miner, opportunistic exposure | Copper and cobalt primary, lithium secondary | Merger speculation with Rio Tinto noted |

The Glencore merger speculation adds a further dimension of uncertainty to the competitive landscape. A standstill regulation governing any potential combination expires in August 2026. Should discussions advance post-expiry, the implications for lithium supply concentration and competitive dynamics across critical minerals would be substantial. As industry analysts have noted, Rio Tinto's lithium strategy reflects broader challenges facing the industry as it scales. Rio Tinto's leadership has, however, declined to comment on the matter while the standstill remains active.

Long-Term Supply Contracts: The Pricing Architecture That Protects Both Sides

One of the less-discussed but strategically important elements of Rio Tinto's commercial approach is its preference for long-term supply contracts that incorporate price floors and price ceilings. This structure differs fundamentally from spot-market-exposed sales strategies.

For buyers — primarily battery manufacturers and EV producers — a price ceiling provides input cost predictability that supports manufacturing economics and product pricing. For Rio Tinto, a price floor provides revenue protection during market downturns, reducing the revenue volatility that spot-market dependence would introduce. The structure is essentially a shared risk arrangement that aligns producer and customer incentives over a multi-year horizon.

This commercial model may become increasingly standard as the lithium market matures and both producers and buyers seek to reduce exposure to the extreme price cycles that characterised the 2021 to 2024 period.

Key Risks Investors Should Monitor

No assessment of the Rio Tinto lithium growth strategy is complete without acknowledging the material risks that could impede execution. This section reflects analytical perspectives and should not be interpreted as financial advice.

- Prolonged price weakness: Chinese production overcapacity has already triggered one significant downturn. A recurrence could delay capacity activation even where infrastructure is complete.

- DLE commercialisation uncertainty: Moving from pilot-scale demonstration to full commercial production introduces engineering and cost risks that are not fully resolved at the current stage of the technology.

- Integration complexity: Absorbing Arcadium's multi-continent operational structure while maintaining capital discipline and cultural alignment is a management challenge of considerable scale.

- Sovereign and permitting risk: The Jadar precedent demonstrates that even fully funded, technically proven projects remain vulnerable to sudden regulatory reversal.

- Competitive pressure from low-cost producers: Australian spodumene producers and established brine operators in Chile may undercut Rio Tinto on spot pricing during periods of market oversupply.

What Rio Tinto's Lithium Ambitions Signal for the Broader Sector

The Rio Tinto lithium growth strategy is not merely a corporate repositioning story. It represents a data point in a much larger structural transition: the systematic reallocation of institutional mining capital toward battery metals and away from thermal energy commodities.

When the world's second-largest miner designates a single commodity as its fastest-growing internal division, anchors a multi-billion dollar acquisition around it, and commits to tripling production within three years, the signal to the broader critical minerals sector is unambiguous. The energy transition demand thesis has moved from investor narrative to operational mandate at the highest levels of mining leadership.

Whether Rio Tinto executes against its targets will depend on lithium price recovery, DLE technology validation, permitting stability across its asset portfolio, and the quality of its integration management. Consequently, what is not in doubt is the conviction behind the strategy or the scale of the institutional commitment behind it.

Want to Know When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including critical battery metals like lithium — so subscribers can act ahead of the broader market. Explore historic discoveries and their market-moving returns, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.