July 8, 2026

When Major Miners Narrow Their Focus, Strategic Assets Find New Paths

The global mining industry is entering a period of concentrated portfolio discipline. The largest diversified miners are making deliberate choices about which commodities deserve their operational attention, shedding exposure to everything outside a tightly defined core. This consolidation of focus is not a retreat from value creation; it is a reallocation of it. Furthermore, when a project of genuine Tier 1 quality finds itself outside a major miner's revised strategic perimeter, the result is not abandonment — it is an opening for a more targeted, independent development pathway.

This is precisely the dynamic now playing out in the Rio Tinto Sovereign Malawi project, involving Sovereign Metals and the Kasiya rutile-graphite deposit in Malawi's Lilongwe District. Understanding what this shift means requires looking well beyond the headline.

When big ASX news breaks, our subscribers know first

The Geological Case for Kasiya: A Deposit That Stands Alone

Natural Rutile vs. Synthetic Alternatives: Why the Distinction Matters

Rutile is the highest-grade naturally occurring form of titanium dioxide, typically grading above 90% TiO2. Its synthetic equivalent, produced through energy-intensive chloride processing of ilmenite, requires significantly more processing and carries a substantially higher carbon footprint. For manufacturers of titanium metal and titanium dioxide pigment, natural rutile commands a consistent price premium over synthetic alternatives precisely because it reduces smelter costs and improves environmental performance metrics.

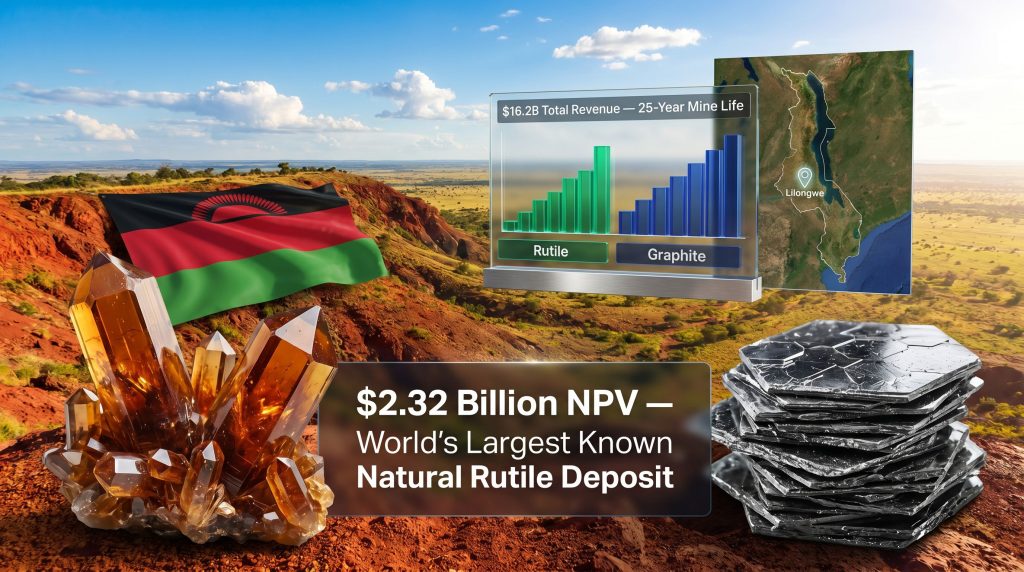

Kasiya holds the distinction of being the world's largest known natural rutile deposit, located in Malawi's Lilongwe District. Alongside this, it ranks as the second-largest known flake graphite deposit globally, making it one of only eleven Tier 1 mining discoveries recorded worldwide over the past decade. The coexistence of both commodities within a single, shallow, free-digging deposit is geologically uncommon and commercially significant.

The Dual-Commodity Advantage and the Monazite Wildcard

Most large-scale mining developments are built around a single primary commodity, with by-products providing incremental uplift. Kasiya inverts this structure: both rutile and graphite are primary revenue generators, and the project economics are supported by a confirmed monazite presence in the tailings stream.

Monazite is a rare earth phosphate mineral containing concentrations of neodymium and praseodymium — the critical inputs for permanent magnets used in electric vehicles and wind turbines. Consequently, the role of rare earth supply chains in projects like Kasiya is becoming increasingly strategic. According to the Definitive Feasibility Study, monazite recovery from Kasiya tailings could generate an additional ~$60 million per year in EBITDA with minimal incremental capital expenditure. This is not speculative optionality; it is a recoverable by-product from material that would otherwise be discarded.

The production profile at steady state is substantial:

- ~222,000 to 246,000 tonnes of natural rutile annually

- ~265,000 to 288,000 tonnes of natural graphite annually

- Long-term graphite ramp-up potential exceeding 500,000 tonnes per year

Kasiya's Financial Architecture: DFS Metrics in Full

The Definitive Feasibility Study, completed in early 2026 under the oversight of the Sovereign-Rio Tinto Technical Committee, produced financial metrics that validate the project's Tier 1 economics. The table below summarises the headline figures:

| Metric | Estimated Value |

|---|---|

| Pre-Tax Net Present Value (NPV) | $2.32 billion |

| Total Revenue Over Mine Life | $16.2 billion |

| Estimated Annual Earnings | ~$476 million |

| Pre-Production Capital Expenditure | ~$597 to $727 million |

| Mine Life | 25 years |

| Annual Rutile Production (Steady-State) | ~222,000 to 246,000 tonnes |

| Annual Graphite Production (Steady-State) | ~265,000 to 288,000 tonnes |

| Long-Term Graphite Ramp-Up Potential | >500,000 tonnes/year |

These figures represent estimates derived from the completed DFS. All projections remain subject to financing, regulatory approvals, and final investment decisions. Investors should not treat DFS outputs as guarantees of future financial performance.

As confirmed by the DFS, a feature that meaningfully strengthens the credibility of these estimates is the pilot mining and rehabilitation programme executed prior to DFS completion. Unlike most projects at a comparable development stage, Kasiya entered its DFS process with real-world operational data already incorporated. The pilot programme generated actual mining rates, processing behaviour, and rehabilitation parameters from the operating environment itself — not from laboratory or desktop extrapolations. This is an unusual level of pre-development validation, and it directly strengthens the reliability of the DFS cost assumptions.

Rio Tinto Sovereign Malawi Project: Decoding the Strategic Exit

Portfolio Concentration Is Not the Same as Project Rejection

Rio Tinto has publicly committed to concentrating its growth capital across four commodity pillars: iron ore, copper, aluminium, and lithium. A strategic review of its iron and titanium business concluded that assuming operational control of Kasiya no longer aligned with this revised mandate. The company's formal notice to Sovereign Metals confirmed explicitly that this decision does not reflect any change in the project's fundamentals, economics, or strategic importance.

This distinction is not a formality. It is the most analytically important element of the entire development. A major miner that had lost confidence in a project's economics would not retain an ~18.2% equity position and maintain board representation rights. Rio Tinto's behaviour here resembles a portfolio manager reducing sector concentration, not an informed insider exiting a deteriorating asset.

What Rio Tinto Invested and What It Kept

Rio Tinto's initial entry into the Kasiya partnership occurred in July 2023 via an A$40.4 million investment for a 15% equity stake in Sovereign Metals. Subsequent option exercises contributed a further A$18.5 million, lifting total ownership to approximately 19.76% before settling at the current ~18.2% post-announcement level. Total committed capital exceeded A$60 million, deployed over a period of active technical collaboration.

The following table clarifies which rights have been relinquished and which have been retained:

| Right | Status Following Decision |

|---|---|

| Operatorship of Kasiya | Relinquished |

| Product Marketing Rights (40% of output) | Relinquished |

| Consent and Pre-Emption Rights | Ceased |

| ~18.2% Equity Shareholding | Retained |

| Right to Appoint Nominee Director (at or above 15% holding) | Retained |

| Right to Notification of Future Equity Issues (at or above 10% holding) | Retained |

The structural logic is clear. Rio Tinto exits the operational and commercial obligations while preserving the financial upside of its equity stake. The project's technical legacy from the partnership — including the pilot mining dataset and DFS contributions from the Technical Committee — remains embedded in Kasiya's development foundation regardless of who holds the operator title.

Sovereign Metals' Independent Strategy: The US-Focused Pivot

Why the United States Is the Natural Commercial Target

Western economies face a concentrated vulnerability in critical minerals trade and supply chains. China currently controls an estimated 70 to 80% of battery-grade graphite anode material globally, according to assessments from the International Energy Agency and the US Geological Survey. Titanium feedstock supply chains exhibit a similar structural dependence on Chinese processing capacity. For policymakers and industrial manufacturers in the United States and allied economies, this is not a theoretical risk; it is an active procurement problem.

Kasiya's projected output would represent a material non-Chinese supply addition in both commodity categories simultaneously. Its combination of natural rutile, natural graphite, and monazite within a single development addresses three distinct supply chain gaps within one project. Indeed, the growing critical minerals demand from Western nations makes Kasiya's timing particularly compelling.

Sovereign Metals has confirmed it intends to pursue a US-centric commercial strategy, deepening engagement with US government agencies and industry stakeholders and prioritising offtake and partnership efforts where Kasiya's strategic value receives the highest recognition.

Existing Commercial Relationships: The MOU Pipeline

Sovereign currently holds non-binding memorandums of understanding with two established counterparties:

- Mitsui and Co: A major Japanese trading house with extensive exposure to critical mineral supply chains across both the titanium and battery sectors

- Traxys North America: A specialist commodities trader whose existing MOU covers an initial 40,000 tonnes per year of graphite, with scalability to 80,000 tonnes per year, specifically structured to support US strategic mineral reserve objectives

Converting these MOUs into binding offtake agreements is now a primary near-term commercial priority. The removal of Rio Tinto's consent and pre-emption rights simplifies Sovereign's ability to negotiate and execute these agreements on its own terms and timetable.

The IFC Partnership: Development Finance With Geopolitical Alignment

Sovereign holds a collaboration agreement with the International Finance Corporation (IFC), the private-sector lending arm of the World Bank Group. As highlighted in Sovereign's IFC partnership, the US government holds the single largest shareholder position in the World Bank, creating a natural geopolitical alignment between Sovereign's US-focused commercial strategy and its development finance partner.

This relationship positions Sovereign to access development finance institution capital and export credit agency financing from the US and allied economies — structures that are particularly well-suited to projects of Kasiya's scale, strategic profile, and geographic location. Furthermore, advances in critical mineral processing technologies continue to improve the economic viability of projects at this scale.

Competitive Positioning: How Kasiya Compares to Peers

| Comparison Dimension | Kasiya (Sovereign Metals) | Typical Competing Projects |

|---|---|---|

| Deposit Classification | World's largest natural rutile; 2nd-largest flake graphite | Smaller, single-commodity deposits |

| Production Profile | Dual-commodity plus monazite upside | Typically single-commodity |

| Carbon Footprint | Low CO2 processing profile | Higher for synthetic rutile alternatives |

| Geopolitical Alignment | Non-Chinese, allied-nation supply | Often Chinese-controlled or processed |

| DFS Completion Status | Completed early 2026 | Many peers at pre-feasibility stage |

| Major Miner Equity | Rio Tinto (~18.2%) retained | Few peers carry major miner equity backing |

The next major ASX story will hit our subscribers first

Key Risks and Critical Path Items for Investors

No DFS-stage project is without execution risk, and Kasiya carries several gating items that investors should track closely:

- Mining licence approval: The Environmental and Social Impact Assessment submission remains on the critical path to licence grant in Malawi. Regulatory timelines in sub-Saharan Africa can be variable and are not fully within the developer's control.

- Project financing: Assembling $597 to $727 million in pre-production capital without a major miner as operational co-developer will require a robust DFI and export credit agency engagement strategy. The IFC relationship provides structural support, but financing at this scale takes time to structure.

- Offtake conversion: MOU-to-binding-agreement timelines for Mitsui and Traxys North America are subject to commercial negotiation and are not guaranteed to proceed at pace.

- Commodity price sensitivity: The DFS financial metrics reflect price assumptions that may not hold across a 25-year mine life. Rutile and graphite markets are subject to demand-side variability from both industrial and battery technology shifts.

- US policy environment: While Sovereign's US-focused strategy aligns with the broader direction of American critical mineral policy, policy settings can change between administrations and are not project-specific commitments.

Readers should treat all forward-looking statements and financial projections in this article as indicative estimates, not confirmed outcomes. Investment decisions should be informed by independent financial advice and direct reference to Sovereign Metals' ASX regulatory filings.

Frequently Asked Questions

What is natural rutile and why does it command a price premium?

Natural rutile is a high-grade titanium dioxide mineral typically containing more than 90% TiO2. It commands a consistent price premium over synthetic rutile and upgraded ilmenite because it requires less processing energy, produces lower emissions during smelting, and reduces overall production costs for titanium metal and pigment manufacturers.

Why did Rio Tinto exit operatorship of the Kasiya project?

Rio Tinto elected not to exercise its option to become operator following an internal strategic review of its iron and titanium business. The company has publicly narrowed its portfolio to four core commodity pillars: iron ore, copper, aluminium, and lithium. The decision was not attributed to any change in Kasiya's fundamentals, economics, or strategic importance.

Does Rio Tinto still hold equity in Sovereign Metals after this decision?

Yes. Rio Tinto retains approximately 18.2% equity in Sovereign Metals, along with the right to appoint a nominee director to the Sovereign board for as long as its shareholding remains at or above 15%.

What is flake graphite and how does it differ from other graphite types?

Flake graphite is a naturally occurring crystalline form of graphite extracted from metamorphic rock. It is distinct from amorphous graphite, which has lower carbon purity and fewer industrial applications. Large-flake, high-carbon graphite commands the highest market premiums and is the preferred feedstock for battery anode manufacturing after purification and spheronisation processing.

What does the IFC collaboration mean for project financing?

The IFC collaboration agreement positions Sovereign to access development finance institution lending and potentially export credit agency support from the US and allied economies. This type of financing architecture is particularly relevant for large-scale critical mineral projects in developing economies, where commercial bank appetite may be constrained by perceived country risk.

The Longer View: What This Transition Signals for Critical Mineral Development

The Rio Tinto Sovereign Malawi project evolution illustrates a recurring dynamic in the modern mining sector: large diversified miners provide technical credibility and early-stage capital to junior developers, then recalibrate their involvement as corporate strategy evolves. When the asset in question carries genuine Tier 1 economics and geopolitical relevance, the departure of a major miner from the operator role does not diminish the project. It repositions it for a more direct engagement with the financing and offtake structures that best reflect its strategic value.

For Kasiya, the next 12 to 24 months will test whether Sovereign Metals can convert the technical foundation built during the Rio Tinto partnership into binding commercial agreements and a credible financing structure. The role of energy transition minerals in shaping geopolitical alliances has never been more prominent, and Kasiya sits squarely at this intersection. The DFS is complete, the deposit's scale is confirmed, and the geopolitical rationale for non-Chinese titanium and graphite supply has never been stronger. What remains is execution, and the independent path Sovereign now walks offers both greater flexibility and greater accountability for the outcome.

Readers seeking additional context on critical mineral supply chain dynamics are encouraged to consult publicly available assessments from the International Energy Agency and the US Geological Survey. For project-specific disclosures, Sovereign Metals' ASX and AIM announcements represent the primary regulatory source.

Want to Identify the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across more than 30 commodities — including critical minerals like graphite, rutile, and rare earths — delivering real-time alerts on significant discoveries directly to subscribers; explore historic examples of major discovery returns to understand the scale of opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.