July 28, 2026

When the Pump Runs Dry: Understanding the Diesel Crunch Reshaping Global Markets

Fuel markets operate on razor-thin buffers. Unlike crude oil, which can be stored in supertankers anchored offshore for months as a financial instrument, refined diesel products must move from refinery to end user within tightly compressed timeframes. The physical infrastructure of modern industrial civilisation, from combine harvesters in the American Midwest to backup generators powering hospitals across Southern Europe, runs on distillate fuel that cannot be easily substituted, stockpiled in garages, or replaced by alternatives on short notice. When that supply chain fractures, the consequences are not confined to petrol station forecourts.

They travel upstream into food production costs, downstream into freight surcharges, and sideways into power grid stability across multiple continents simultaneously.

The Russia diesel export ban and global supply crunch that crystallised in July 2026 represents exactly this kind of systemic fracture, and understanding it requires looking well beyond Moscow's policy decision to the structural vulnerabilities that made global markets so dangerously exposed in the first place.

When big ASX news breaks, our subscribers know first

Why Diesel Demand Is Structurally Different From Other Fuels

Diesel occupies a unique position in the global energy economy because it is not primarily a consumer fuel. It is an industrial input. Petrol powers passenger vehicles in a market where consumers can delay discretionary journeys or shift travel modes. Diesel powers the systems that cannot wait: refrigerated food transport, long-haul freight, agricultural equipment during planting and harvest windows, mining operations, and emergency power generation.

This structural inelasticity means that when diesel prices spike, demand does not fall quickly enough to rebalance supply. Farmers cannot delay planting because diesel costs double. Freight companies cannot halt deliveries because crack spreads widen. The fuel simply must be purchased, at whatever price the market clears. This dynamic makes diesel the single most economically sensitive refined product, and its price signal travels faster and more broadly through headline inflation than almost any other commodity input.

Furthermore, the crude oil market dynamics of post-pandemic demand recovery accelerated this vulnerability. Refinery closures across Europe and North America during 2020 and 2021 permanently removed processing capacity that has not been rebuilt. Western nations sacrificed long-run refining resilience for short-term economic rationalisation during a period of suppressed demand, and those decisions created a structural deficit that has persisted ever since.

By early July 2026, US diesel inventories had fallen to 97.8 million barrels, approximately 6% below the five-year seasonal average, following a single-week draw exceeding 4.5 million barrels. Northwest European stocks had declined roughly 20% since the Iran war began, leaving virtually no inventory cushion against new supply disruptions.

"The Russia diesel export ban did not manufacture a supply crisis from thin air. It detonated a market that was already sitting on structural tinder, with depleted inventories, limited spare refining capacity, and simultaneous geopolitical stress across two major supply corridors."

The Mechanics Behind Russia's Export Halt

Russia's decision to suspend diesel exports until July 31, 2026 was not a geopolitical manoeuvre in the conventional sense. It was a defensive response to a domestic fuel emergency created by sustained Ukrainian drone campaigns targeting Russian oil processing infrastructure.

The cumulative damage from these strikes has been substantial. Analysts estimate that approximately 30% of Russia's domestic refining capacity has been impaired through the course of the campaign, reducing throughput across major processing facilities. The downstream consequence inside Russia was acute: fuel queues extending up to 18 hours at petrol stations, shortages of diesel for agricultural and industrial users, and a domestic distribution system under severe stress.

Moscow's response involved two parallel interventions: imposing a ban that applies directly to oil producers rather than simply to trading intermediaries (a structurally broader restriction than previous export controls), and simultaneously beginning to import diesel in July 2026 to compensate for domestic shortfalls. For the world's second-largest diesel exporter to become a net importer, even temporarily, represents a profound reversal with significant market implications.

Notably, pre-existing government-to-government supply agreements, such as arrangements with Mongolia, were explicitly carved out from the ban's scope. This suggests the policy was designed primarily as a domestic stabilisation measure rather than a broader geopolitical signal. In addition, the oil price shock reverberating through global markets has compounded the pressure on buyers scrambling for alternative supply.

The Collapse in Russian Export Volumes

The export data tells the full story of how dramatically Russian supply had already deteriorated before the formal ban was announced:

| Metric | Data Point |

|---|---|

| Russia's global seaborne diesel share (pre-crisis) | ~11% of global supply |

| 2025 average export volume | ~817,000 barrels per day |

| June 2026 export volume | ~426,000 barrels per day |

| July 1–10, 2026 export volume | ~234,000 barrels per day |

| Reduction from 2025 average to early July 2026 | ~71% decline |

This trajectory reveals that the formal export ban was, in some respects, the official codification of a collapse that was already well underway. Russian exporters had already lost nearly half their monthly volume before the ban took effect, meaning markets had absorbed a significant supply withdrawal before the announcement created its additional psychological and logistical shock.

How Prices Responded: Record Spreads and Flushed Sellers

The price reaction to the Russia diesel export ban and global supply crunch was immediate and severe across both major trading hubs.

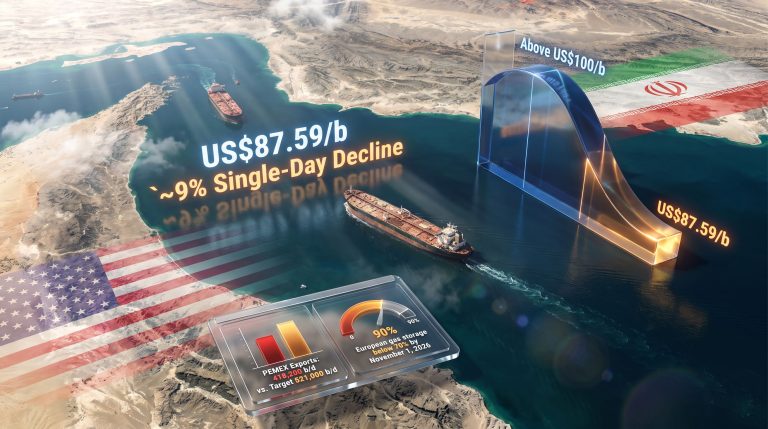

US ultra-low sulphur diesel futures surged 11% in a single session on the announcement day, reaching $154 per barrel. That figure represented an $80 per barrel premium over WTI crude, a crack spread of extraordinary width that signals genuine physical scarcity rather than financial speculation. When the spread between crude and refined product reaches those levels, it typically reflects refinery margins being overwhelmed by spot demand for the finished product itself.

European low-sulphur gasoil futures simultaneously reached an all-time record premium to Brent crude of $60.77 per barrel, a figure with no historical precedent in the post-pandemic energy market era. Consequently, the trade war impact on oil prices was further layered onto an already fractured supply environment, amplifying volatility across global energy benchmarks.

The timing amplified the shock considerably. Within hours of Russia's export ban announcement, fresh US military strikes on Iran were reported, reactivating fears around vessel movements through the Strait of Hormuz. The convergence of simultaneous supply threats from two geographically distinct but economically interconnected corridors created the conditions for a forced liquidation of short positions across distillate markets.

Gulf Oil adviser Tom Kloza characterised the environment as one where "Persian Gulf headlines, Russian supply cessation, and a stark US Energy Information Administration inventory report all arrived simultaneously, effectively forcing distillate sellers out of the market in a compressed timeframe." This captures a key mechanism in commodity markets: when bearish positioning meets multiple simultaneous supply shocks, the unwinding of short positions accelerates price moves beyond what fundamental supply-demand arithmetic alone would predict.

The Global Ripple Effect: Who Bears the Highest Exposure

One of the most instructive aspects of the current situation is how the Russia diesel export ban affects countries that have not purchased Russian diesel for years. This counterintuitive dynamic reveals how global commodity markets actually function.

Europe: Second-Order Exposure Through Cargo Competition

EU sanctions imposed following Russia's invasion of Ukraine mean European buyers stopped purchasing Russian diesel directly. Yet European gasoil prices hit all-time record premiums on the day of Russia's export ban. The mechanism is indirect but powerful.

Russia's traditional export customers, including Brazil, Turkey, and various North African importers, previously sourced a significant share of their diesel requirements from Russian cargoes. With those barrels removed from global supply, those buyers must now compete aggressively for cargoes from alternative origins: US Gulf Coast refiners, Middle Eastern exporters, and Indian refining hubs. Europe competes in that same pool for the same barrels, and fewer total barrels available means higher clearing prices everywhere, regardless of bilateral trading relationships.

Amsterdam-Rotterdam-Antwerp (ARA) hub inventories, the benchmark storage region for Northwest European refined products, are already described by market participants as well below historical seasonal ranges, leaving European buyers with minimal inventory cushion and maximum price exposure.

The United States: Swing Supplier Under Simultaneous Pressure

The US emerged as Europe's primary diesel replacement source when Middle East supply corridors came under pressure earlier in 2026. That role now creates a zero-sum allocation problem. According to Reuters analysis of Putin's diesel export ban, the risk of a prolonged fuel shock extending well into the second half of 2026 is considered significant by several senior commodity analysts.

Qilin Tam, head of refining at consultancy FGE NexantECA, articulated the dilemma clearly: the US became the reliable diesel source for European and British buyers when Hormuz disruptions struck, but every barrel now redirected toward Latin American buyers represents a barrel unavailable to European importers. This competition is unfolding against a backdrop of US diesel inventories already sitting materially below five-year seasonal averages.

Freight cost inflation is an additional layer. Higher cargo demand on transatlantic diesel trade routes pushes up shipping rates, adding a logistics premium on top of the commodity price increase itself. Analysts expect elevated freight costs to persist through at least Q4 2026 as rebalancing plays out over months rather than weeks.

Turkey and Mediterranean Power Generation

Turkey occupies a structurally important but often overlooked position in Mediterranean diesel flows. As both a refiner and re-exporter, Turkish output supplements diesel supply across the broader Mediterranean basin. Vortexa analyst Mick Strautmann has specifically flagged the risk that Turkish refiners may redirect production toward domestic consumption rather than export during peak summer demand periods.

The consequence would be the removal of diesel volumes that Mediterranean countries depend on for power generation during summer peak load. Diesel-fired generation remains significant backup and primary generation infrastructure across parts of Southern Europe and North Africa, and peak summer demand coincides precisely with current market stress.

Asia: China's Uncertain Safety Valve

China partially relaxed its fuel export restrictions in July 2026, theoretically providing some relief to global markets. However, Qilin Tam cautions that renewed Middle East tensions make continuation of Chinese export liberalisation into August far from guaranteed. China's export policy remains contingent on domestic demand dynamics and geopolitical calculation, neither of which provides reliable forward visibility for global buyers banking on Asian supply as an offset to Russian losses.

Downstream Consequences: From Farm Fields to Freight Invoices

The economic transmission channels from diesel price inflation to broader consumer costs are well-established but worth tracing explicitly, because they operate across multiple timescales simultaneously.

Agricultural costs are the most time-sensitive channel. The current price shock arrives as the Southern Hemisphere approaches its planting season and the Northern Hemisphere enters harvest. Brazilian farmers and US Midwestern producers compete for the same shrinking global pool of diesel supply, with higher fuel costs feeding directly into input cost structures for food production. Higher farm-gate costs eventually become higher food prices, with a lag of weeks to months depending on crop type and supply chain length.

Freight surcharges are the most structurally embedded channel. Diesel is the primary fuel for road freight across virtually every major economy. Sustained price elevation typically triggers contractual fuel surcharge resets, with industry analysts expecting US shippers to reset surcharge formulas by September 2026. Those surcharges then flow through to the cost of every product moved by truck, which in practice means almost everything consumers purchase.

Power generation vulnerability is the least visible but potentially most acute channel in specific geographies. Regions that depend on diesel-fired generation for either baseload or backup power, including parts of the Middle East, Sub-Saharan Africa, and Southern Europe, face both elevated fuel costs and potential supply availability concerns if the global crunch deepens. The broader commodity price impacts rippling from this disruption are already being tracked closely by institutional investors monitoring downstream cost exposure.

The next major ASX story will hit our subscribers first

Comparing 2026 to the 2022 Sanctions Shock

Markets have navigated Russian diesel supply disruptions before, most notably during the 2022 EU sanctions imposed following Russia's full-scale invasion of Ukraine. However, the structural characteristics of the two episodes differ in ways that make 2026 potentially more severe.

| Factor | 2022 EU Sanctions | 2026 Export Ban |

|---|---|---|

| Trigger | Political response to invasion | Military infrastructure damage |

| Mechanism | Demand-side withdrawal | Supply-side removal |

| Advance warning | Months of diplomatic signalling | Days of market preparation |

| Inventory buffer at shock | Moderate | Near-critically low |

| Simultaneous geopolitical stressors | Moderate | High (Iran war, Hormuz risk) |

| Expected duration | Permanent structural shift | Temporary (until July 31, 2026) stated |

The 2022 sanctions allowed market participants months to reroute procurement relationships, build alternative supply chains, and accumulate buffer inventories. The 2026 ban arrived with minimal preparation time into a market already operating at depleted inventory levels. The dual-shock dynamic — Russian supply removed from the west while Hormuz tensions threaten flows from the east — has no clear historical precedent in post-pandemic energy markets.

Scenarios for Post-July 31 Markets

Three distinct pathways are plausible once Russia's stated ban expiry date passes, each carrying materially different implications for global diesel markets through the remainder of 2026.

Scenario 1: Clean Resolution. Russian refineries complete repairs, domestic shortages ease, and exports resume close to pre-ban levels by early August. Markets partially retrace price spikes, though inventory rebuilding takes months. Assessment: Low-to-moderate probability given uncertain refinery repair timelines and ongoing drone campaign risk.

Scenario 2: Partial Resumption. Russia restores exports at materially reduced volumes in the range of 400,000 to 500,000 barrels per day, reflecting persistent refinery impairment. Diesel markets remain in structural deficit through Q3 2026, with prices stabilising at elevated levels. Assessment: Moderate-to-high probability, most consistent with the observed trajectory of Russian export data through 2026.

Scenario 3: Extension or Escalation. Continued drone strikes prevent meaningful refinery recovery, and Moscow extends the ban beyond July 31 or imposes additional restrictions. Combined with Hormuz disruptions and below-average Western inventories, this pathway risks a sustained diesel price shock extending into Q4 2026. Assessment: Moderate probability, dependent on conflict trajectory in Ukraine and the direction of Iranian nuclear negotiations.

Investors and supply chain managers should note that Scenario 2 represents the base case for most market analysts, implying that elevated diesel prices are not a temporary spike to be traded through but a structural market condition requiring operational adjustment. This article contains forward-looking assessments based on current market data and analyst commentary. Commodity markets are inherently unpredictable, and actual outcomes may differ materially from scenarios described above.

Frequently Asked Questions: Russia Diesel Export Ban and Global Supply Crunch

Why does Russia's diesel export ban affect countries that stopped buying Russian diesel years ago?

Global diesel trades through a unified international pricing mechanism. When Russian supply is removed, countries that previously sourced from Moscow must compete with all other buyers for alternative barrels, bidding up prices universally regardless of whether a particular nation ever held a direct trading relationship with Russian exporters.

What is the crack spread, and why does it matter here?

The crack spread measures the price difference between crude oil and refined products like diesel. An unusually wide crack spread, such as the $80 per barrel premium of US diesel over WTI crude seen during this episode, signals that physical diesel is scarce relative to the crude needed to produce it, reflecting genuine supply stress rather than financial market noise.

How long will the ban last?

Russia's stated end date is July 31, 2026. Extension risk is real, contingent on refinery repair progress and the continuation of Ukrainian drone campaigns against Russian oil infrastructure. The US-China oil price tensions add a further layer of uncertainty to global energy markets during this period.

Which sectors face the most immediate cost exposure?

- Agricultural producers facing elevated input costs during planting and harvest seasons

- Road freight and logistics operators whose fuel surcharge formulas are linked to diesel benchmarks

- Power generators in diesel-dependent regions facing both price and availability risk

- Maritime shipping operators facing bunkering cost inflation on key trade routes

Could Indian or Middle Eastern refiners offset Russian supply losses?

Indian refiners have expanded diesel export capacity significantly since 2022 and represent a partial offset. However, Middle Eastern refinery output is itself subject to Hormuz transit risk, and Indian export volumes are constrained by domestic demand priorities, limiting the degree to which Asian supply can substitute for the scale of lost Russian barrels. Furthermore, Spartan Commodities' market outlook suggests that the pace of any rebalancing will depend heavily on whether geopolitical flashpoints stabilise in the coming weeks.

Key Takeaways

The Russia diesel export ban and global supply crunch of July 2026 is not an isolated policy event. It is the detonation point for structural vulnerabilities that have accumulated across global refined product markets since the pandemic refinery rationalisation cycle of 2020 to 2022.

- Russian diesel exports collapsed 71% from their 2025 average to early July 2026 levels before the formal ban was announced

- US diesel inventories stood 6% below the five-year seasonal average at the time of the shock, with European stocks similarly depleted

- European gasoil crack spreads reached all-time record premiums to Brent crude, reflecting genuine physical scarcity

- The simultaneous pressure from Russian supply loss in the west and Iranian corridor risk in the east creates a dual-shock scenario without modern precedent

- Downstream consequences for food inflation, freight costs, and power generation reliability mean this is a macroeconomic risk event, not merely an energy trading story

- Resolution requires either rapid Russian refinery restoration, meaningful inventory rebuilding across Western markets, or a reduction in competing geopolitical supply pressures — none of which are achievable within weeks

Readers seeking to track ongoing developments in global diesel market dynamics and energy supply chain conditions can find related reporting and data analysis at ETEnergyWorld.

Want to Track the Next Major Commodity Supply Shock Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying mineral discoveries and actionable investment opportunities across 30-plus commodities — because when supply chains fracture and commodity prices surge, being first to a discovery can be the difference that matters. Explore historic returns from major mineral discoveries and begin your 14-day free trial today to position yourself ahead of the broader market.