June 5, 2026

The Concentrated World of PGM Supply and Why a Single Project Can Move Markets

Platinum group metals occupy a peculiar position in the global commodities hierarchy. Unlike gold or silver, which benefit from broad retail and investment demand, PGMs derive their pricing power almost entirely from industrial necessity. Palladium cleans exhaust emissions from petrol engines. Platinum serves hydrogen fuel cells, jewellery, and diesel catalysts. Rhodium, iridium, and ruthenium underpin specialised electronics and chemical processing. The result is a market where supply constraints in PGMs are extreme, demand is structurally inelastic in the short term, and the addition of a single large project can meaningfully shift the global supply curve.

That dynamic is now playing out in real time as the Russian Platinum Arctic mine launch moves toward a November 2025 commencement at its Arctic polymetallic operation on Russia's Taymyr Peninsula, a development that carries implications for palladium pricing, industrial procurement strategy, and the competitive dynamics of global PGM production.

When big ASX news breaks, our subscribers know first

Understanding the Chernogorskoye Deposit and Its Place in the PGM World

The geological foundation of this project matters enormously to understanding its long-term significance. The Chernogorskoye deposit, along with licences covering the southern portion of the Norilsk-1 zone, sits within the same Taymyr Peninsula geological province that hosts Nornickel's world-class Norilsk operations. The ore type is copper-nickel sulphide, the same formation responsible for some of the richest PGM accumulations on Earth.

Copper-nickel sulphide systems are geologically distinct from the layered igneous intrusions that host South Africa's Bushveld Complex deposits. Where Bushveld ores are mined in thin, consistent reef horizons, sulphide-hosted deposits like those at Norilsk and Chernogorskoye tend to present as larger, more irregular ore bodies amenable to bulk underground or open-pit extraction. The practical implication is that processing costs per tonne can be lower, but metallurgical complexity in separating co-products adds operational nuance.

Key Deposit Metrics at a Glance

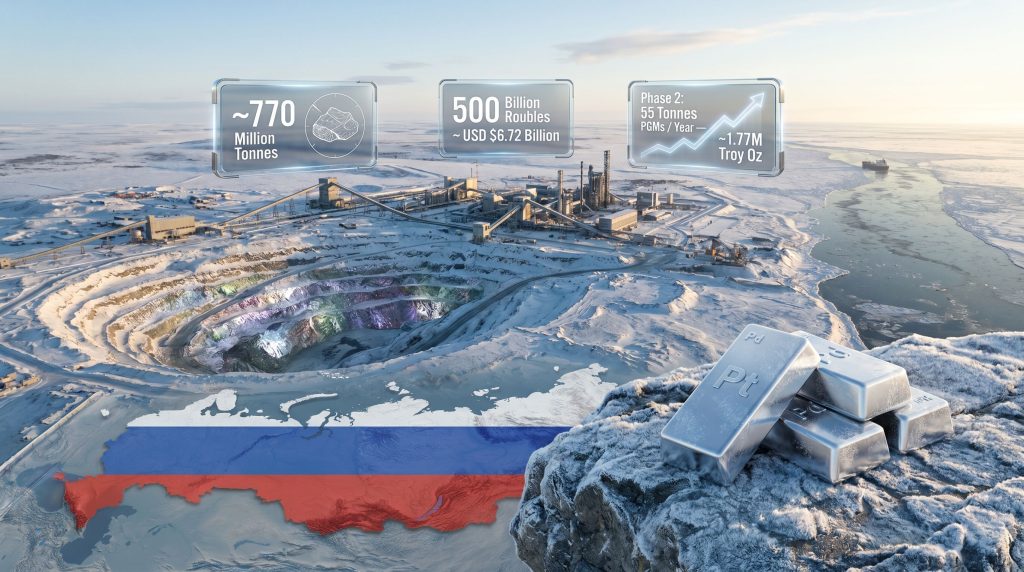

- Total ore resource: Approximately 770 million tonnes

- Primary PGM output: Palladium and platinum, with nickel and copper as significant co-products

- Phase 1 processing rate: 7 million tonnes of ore per year

- Operational life at Phase 1 rates: Approximately 55 years

- Phase 2 target throughput: 15 million tonnes of ore per year

- Phase 2 PGM output target: 55 tonnes annually, equivalent to roughly 1.77 million troy ounces

- Logistics pathway: Northern Sea Route for concentrate export

The co-product revenue structure deserves particular attention. Unlike pure-play PGM mines, where revenue is almost entirely dependent on palladium and platinum pricing, Chernogorskoye's copper and nickel output provides meaningful cash flow diversification. Furthermore, nickel's industrial importance means that in periods of PGM price weakness, base metal revenues act as a partial hedge against operating losses, improving the project's resilience across commodity cycles.

How Phase 1 Output Stacks Up Against Global PGM Production

Nornickel's own market analysis concluded that Russian Platinum's Phase 1 operations could contribute approximately 500,000 ounces of palladium and 200,000 ounces of platinum to Russia's annual output. To contextualise those numbers, global palladium mine supply has historically ranged between 6.5 and 7 million ounces per year, meaning Phase 1 alone would represent a supply addition of roughly 7 to 8 percent of current global output.

| Metric | Nornickel (Current) | Russian Platinum Phase 1 Target |

|---|---|---|

| Palladium market share | ~40% globally | ~500,000 oz/year incremental |

| Platinum output contribution | Significant | ~200,000 oz/year incremental |

| Operational status | Active, multi-decade producer | November 2025 target launch |

| Processing infrastructure | Fully integrated | Concentrate via offtake agreement |

While Phase 1 volumes are unlikely to trigger an immediate price collapse, they introduce a structural supply increment at a time when the platinum and palladium dynamics have been navigating a complex transition. Palladium demand from internal combustion engine catalytic converters, which historically drove the metal's extraordinary price performance between 2016 and 2022, faces a medium-term structural headwind as electric vehicle penetration accelerates across key automotive markets.

The Financing Architecture: What 500 Billion Roubles Really Means

The capital commitment behind this project is one of its most striking features. Total expenditure has reached 500 billion roubles, which at the exchange rate of approximately 74.35 roubles per US dollar translates to roughly USD $6.72 billion. That figure places the Russian Platinum Arctic operation among the largest single-asset mining capital commitments globally in the current decade.

For reference, major greenfield PGM projects in more capital-accessible jurisdictions have historically required substantially less:

| Project | Jurisdiction | Estimated Capex (USD) | Annual PGM Output Target |

|---|---|---|---|

| Russian Platinum Arctic (Phase 1) | Russia (Arctic) | ~$6.72 billion | ~700,000 oz combined PGMs |

| Waterberg Project | South Africa | ~$1.5 billion | ~420,000 oz 4E PGMs |

| Flatreef (Ivanhoe Mines) | South Africa | ~$1.6 billion | ~476,000 oz PGMs |

Note: Figures are indicative and sourced from public project disclosures. Comparisons should account for differences in ore grade, processing complexity, Arctic infrastructure requirements, and currency effects.

The elevated capital intensity relative to South African comparables reflects several factors unique to Arctic development: permafrost engineering, remote logistics, energy infrastructure construction, and the need to domestically source equipment that would ordinarily be procured from Western suppliers. Following the collapse of international capital market access under Western sanctions, financing was secured through Russian state-linked institutions VTB and VEB.RF, embedding the project firmly within Russia's state-directed financial architecture.

This transition from an internationally financed joint venture model to a state-bank-funded independent operation represents a fundamental restructuring of the project's risk profile, not simply a funding substitution. The project's resilience to further Western financial pressure has increased, but institutional dependencies of a different character have emerged.

The Timeline That Tells the Story: From Alliance to Independent Development

The path to the Russian Platinum Arctic mine launch has been anything but linear. Understanding the timeline helps explain both the current ownership structure and the commercial relationship with Nornickel:

- 2018: A cooperation framework was established between Russian Platinum and Nornickel aimed at developing Arctic PGM resources jointly.

- 2020: The proposed alliance collapsed after Rusal, one of Nornickel's major shareholders, opposed the partnership terms.

- 2021: Rather than pursuing equity co-ownership, both parties entered five-year offtake agreements allowing concentrate from the Chernogorsky processing plant to flow to Nornickel's Global Palladium Fund.

- 2024 (original target): Production was scheduled to begin but was delayed due to restricted access to specialised mining and processing equipment under Western sanctions regimes.

- 2025: At the St Petersburg Economic Forum, company owner Musa Bazhaev confirmed November 2025 as the first-output milestone, backed by domestically sourced equipment and state financing.

The shift from a joint venture to an offtake structure created a commercial relationship that is simultaneously cooperative and competitive. Russian Platinum gains a guaranteed downstream processing route through Nornickel's infrastructure; Nornickel gains incremental supply for its Global Palladium Fund without taking on equity risk or capital exposure. Both parties effectively de-risked their relationship while preserving optionality for future partnership discussions, which Bazhaev indicated remain possible.

What Phase 2 Would Mean for the Global PGM Supply Curve

If Phase 1 represents a meaningful but manageable market addition, Phase 2 operates in an entirely different order of magnitude. The southern Norilsk-1 zone targets 15 million tonnes of ore per year and annual PGM output of 55 tonnes, equivalent to approximately 1.77 million troy ounces.

A single project delivering 1.77 million ounces of PGMs annually would represent a supply addition of roughly 25 percent relative to current global palladium mine production. That is not a marginal increment. It is a structural shift in the global supply curve with multi-decade pricing consequences.

The timing of Phase 2 matters considerably. No confirmed commencement date has been publicly stated. However, the interaction between Phase 2 supply and automotive sector transition dynamics creates a scenario of unusual complexity:

- If Phase 2 production ramps up while internal combustion engine vehicles still dominate global fleets, the supply addition would likely compress palladium price premiums significantly.

- If hydrogen fuel cell vehicle adoption accelerates, platinum demand could rise to partially offset the supply addition, though the net effect on pricing remains uncertain.

- If electric vehicle penetration displaces ICE production faster than currently modelled, Phase 2 supply could arrive into a structurally weaker demand environment, amplifying downward price pressure.

Industrial consumers with long-horizon PGM procurement contracts, particularly in the automotive sector, should treat Phase 2 timeline developments as a key variable in strategic sourcing and hedging decisions.

The next major ASX story will hit our subscribers first

Key Risks That Could Affect the November 2025 Launch

Commissioning a large-scale greenfield operation in the Arctic, under sanctions conditions and with domestically substituted equipment, carries a risk profile that warrants careful assessment:

| Risk Category | Specific Factor | Probability | Potential Impact |

|---|---|---|---|

| Equipment access | Ongoing sanctions procurement restrictions | Medium | High: could push launch to 2026 |

| Financing continuity | State bank capital reallocation under fiscal pressure | Low-Medium | High: project already at $6.72B capex |

| Technical execution | Processing plant commissioning delays | Medium | Medium: common in greenfield startups |

| Geopolitical escalation | Expanded sanctions targeting mining sector | Medium | High: could affect offtake execution |

| Partnership uncertainty | Nornickel offtake renegotiation | Low | Medium: affects Phase 1 commercial pathway |

| Regulatory or environmental | Permitting or licence complications | Low | Medium |

One underappreciated risk specific to Arctic operations is the engineering complexity of working in permafrost conditions. Foundation instability, seasonal access constraints, and extreme cold weather commissioning challenges have historically caused delays at Russian Arctic industrial projects independent of sanctions or financing issues. These technical factors add a layer of execution risk beyond what comparable lower-latitude mining projects would face.

Geopolitical Dimensions: Sanctions, the Northern Sea Route, and Supply Chain Decoupling

The Russian Platinum Arctic mine launch does not occur in a geopolitical vacuum. Western sanctions imposed since 2022 have progressively restricted Russia's industrial sector from accessing foreign capital, technology, and precision equipment. The project's delay from 2024 to 2025 is a direct consequence of those restrictions, as procurement strategies required redesign around domestically available alternatives.

The reliance on the Northern Sea Route as the primary logistics corridor for concentrate exports reinforces a broader pattern of Arctic resource development serving Russian strategic interests. In addition, the broader geopolitical mining landscape shows that the route connects Siberian industrial output to Asian markets whilst bypassing Western-controlled shipping chokepoints entirely.

For Western industrial supply chains, the implications are layered:

- PGMs from Russian Platinum will not be directly accessible to buyers operating under sanctions compliance obligations.

- However, additional Russian supply entering global markets creates price effects that ripple through spot and futures pricing regardless of buyer geography.

- South African and Zimbabwean PGM producers, who have benefited from supply tightness and Russian supply uncertainty since 2022, face a medium-term competitive challenge if Russian output expands as projected.

- Industrial consumers who have invested in Russian supply diversification programs may find that diversification was well-timed not only for compliance reasons but also for supply security.

Nornickel's Strategic Position in a More Competitive Russian PGM Sector

Nornickel currently controls approximately 40 percent of global palladium supply, a dominance that has made it one of the most consequential single entities in any industrial metals market. The emergence of Russian Platinum as an independent domestic producer, operating on geologically adjacent ground, introduces a competitive dimension that did not exist when Nornickel was the sole Russian PGM producer.

Phase 1 volumes flowing through the existing offtake to Nornickel's Global Palladium Fund partially neutralise the competitive dynamic in the near term, as Nornickel effectively gains additional supply to manage commercial obligations. But if offtake agreements expire without renewal, or if Russian Platinum achieves independent commercial access as Phase 2 develops, Nornickel's market share position becomes more contestable than at any point in its recent history.

The openness to renewed partnership discussions signalled by Bazhaev suggests that a cooperative resolution remains on the table. From a market structure perspective, consolidation would preserve pricing discipline within Russian PGM supply more effectively than fragmented competition between two large domestic producers.

What the Market Should Watch Through 2026 and Beyond

The Russian Platinum Arctic mine launch is a supply-side event with a long tail of consequences. Near-term market participants should monitor several key indicators, particularly given the critical minerals demand surge reshaping procurement strategies globally:

- Commissioning confirmation: Whether November 2025 first output is achieved or further delayed.

- Phase 2 timeline disclosure: Any public statement on commencement timing for the Norilsk-1 southern zone would materially update market supply projections.

- Offtake agreement status: The 2021 five-year agreements are approaching their contractual limit, making renewal or renegotiation a live commercial question.

- Palladium futures positioning: As Phase 1 commissioning progresses, futures markets may begin pricing in incremental supply, particularly if automotive demand data simultaneously shows continued ICE vehicle production softness.

- South African producer responses: Any acceleration of cost-cutting, consolidation, or output reduction among South African PGM producers would signal that market participants are already adjusting to anticipated Russian supply growth.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or commodity trading advice. PGM market projections involve significant uncertainty, and past price behaviour is not indicative of future outcomes. Readers should conduct independent research and seek professional advice before making any investment or procurement decisions.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and commodity data into actionable investment insights — ideal for investors monitoring how single projects can reshape global supply dynamics. Explore historic discoveries and the extraordinary returns they generated, then begin your 14-day free trial at Discovery Alert to ensure you're positioned before the broader market reacts.