July 15, 2026

When the Map Gets Redrawn: Rutile's Supply Crisis and What It Means for New Discoveries

The titanium minerals market operates on a structural tension that most investors never fully appreciate. Natural rutile, the highest-purity feedstock for titanium dioxide pigment and aerospace-grade titanium metal, is not simply a commodity that can be substituted at will. Its chemical properties, particularly its elevated TiO₂ content relative to synthetic alternatives like chloride slag or upgraded ilmenite, place it in a category of its own for applications where purity is non-negotiable.

Global natural rutile production is heavily concentrated. A small number of operating mines, primarily in Sierra Leone, Australia, and Kenya, account for the overwhelming majority of annual supply. When those operations face depletion curves, production disruptions, or mine life limitations, the market has limited flexibility to absorb the shortfall through synthetic feedstocks alone, because chloride-process pigment plants are specifically engineered around natural rutile's characteristics.

New large-scale discoveries in stable jurisdictions are exceptionally rare, which is precisely why southern-central Africa has attracted intense geological attention over the past several years. Furthermore, the ongoing rutile price assessment landscape adds another layer of complexity to how market participants value new supply entrants.

It is within this supply-constrained backdrop that the Fortuna Metals Mkanda rutile resource deserves analysis, not simply as a company announcement, but as a data point in a much larger mineral systems story.

When big ASX news breaks, our subscribers know first

Understanding the Mkanda Rutile-Graphite Project: Geology, Scale, and Setting

What Kind of Deposit Is This and Why Does the Style Matter?

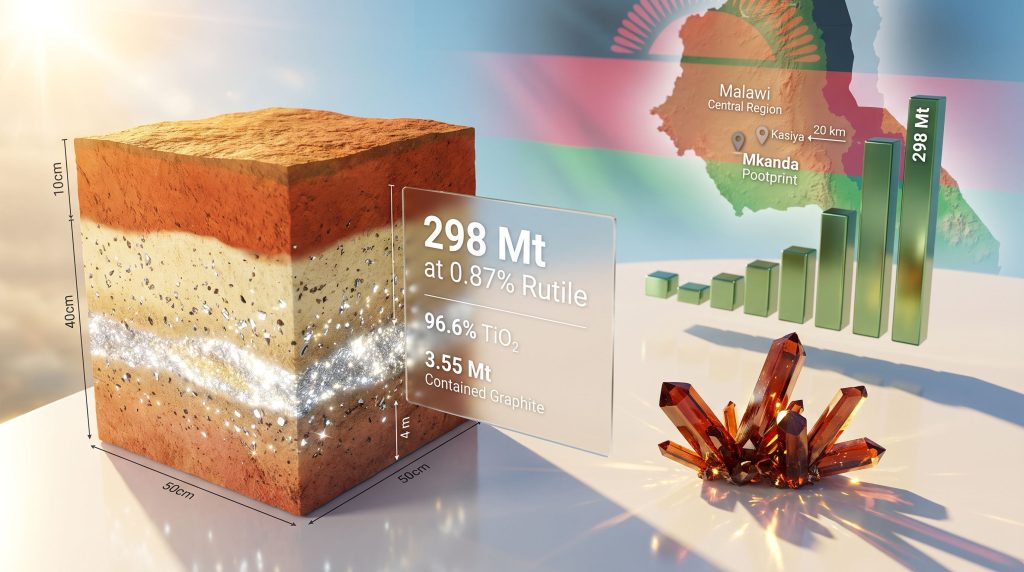

Mkanda is a regolith-hosted, near-surface rutile and graphite deposit situated within a 658 km² landholding in Malawi, positioned approximately 20 kilometres south of Sovereign Metals' Kasiya project. The regolith-hosted style is analytically important for reasons that go beyond simple geology.

Regolith mineralisation forms through the deep weathering of primary crystalline rocks over geological timescales. In this process, titanium-bearing minerals concentrate within the laterised weathering profile, producing soft, loose material that is typically amenable to low-energy extraction methods. The practical consequence is that strip ratios and processing costs for this deposit style tend to be structurally lower than hard-rock equivalents, which matters enormously when pre-feasibility economics are eventually modelled.

At Mkanda, the average mineralised depth across the hand auger dataset is approximately 4.1 metres, which is exceptionally shallow even by regolith-hosted standards. This shallow profile, while limiting the vertical extent of current resource knowledge, also signals minimal overburden and potentially favourable mining geometries.

The mineralised footprint covers a high-grade rutile core of approximately 17.8 km², embedded within a broader anomalous zone of around 37 km². More than 675 drill holes have been completed across the project, and the mineralised system remains open along strike and at depth — an important distinction for understanding where the resource stands in its definitional lifecycle.

A deposit that is still geometrically open after more than 675 drill holes is not a fully characterised system. It is a resource in active expansion, and the next round of data will carry disproportionate interpretive weight.

One statistical signal that deserves attention: 85% of shallow samples in the 0 to 2 metre horizon exceed the cut-off grade. That level of consistency across the near-surface zone is a meaningful indicator of deposit continuity, reducing the risk that the mineralisation is patchy or structurally controlled in ways that would complicate bulk mining assumptions.

Malawi's Geological Credentials: More Than Just a Kasiya Neighbourhood

Malawi's emergence as a rutile exploration frontier is anchored in the Proterozoic basement geology running through the country's central region. The same geological belt that hosts Kasiya also underpins Mkanda's landholding, and while geological analogy is not a resource estimate, it does meaningfully reduce exploration risk when the mineralisation style, host geology, and weathering profile are demonstrably similar.

Sovereign Metals' Kasiya discovery effectively validated the regional prospectivity at a scale that redrew the global rutile map. Before Kasiya reached its current resource size of approximately 1,800 million tonnes, the conventional wisdom in mineral exploration circles was that world-class natural rutile deposits of this type were largely exhausted. Kasiya challenged that assumption directly, and Mkanda's proximity to that established system materially de-risks the geological thesis at the exploration stage.

Infrastructure, regulatory, and sovereign risk considerations for Malawi are legitimate factors in any project-level assessment. The country has an established mining code, and the Ministry of Natural Resources has administered exploration and mining licences across several commodity verticals. That said, Malawi is not a mature mining jurisdiction in the way that Western Australia or Quebec are, and investors should factor in permitting timelines, community engagement requirements, and export logistics as variables that will influence project advancement schedules.

The Maiden MRE at a Glance: Unpacking the Numbers Behind the Fortuna Metals Mkanda Rutile Resource

Headline Metrics and What They Actually Represent

The maiden Inferred Mineral Resource Estimate for the Fortuna Metals Mkanda rutile resource delivers figures that are substantial even by global standards at first publication. The project's mineral deposit tiers positioning becomes particularly relevant when benchmarking against established peers.

| Parameter | Value |

|---|---|

| Total Resource Tonnage | 298 million tonnes (Mt) |

| Rutile Grade (0.7% cut-off) | 0.87% rutile |

| Total Graphitic Carbon (TGC) | 1.19% TGC |

| Contained Graphite | ~3.55 Mt |

| Higher-Grade Slice (0.8% cut-off) | 159 Mt at 0.98% rutile |

| Resource Classification | Inferred |

| Drill Spacing | ~400m x 400m |

| TiO₂ Product Purity (bulk sample) | 96.6% TiO₂ |

The distinction between the full resource at the 0.7% cut-off and the higher-grade slice at 0.8% is analytically useful. At the elevated cut-off, 159 Mt of material grades at 0.98% rutile, demonstrating that a meaningful proportion of the total tonnage carries above-average grade. This is not a deposit where the headline average is propped up by dilutive low-grade tonnes at the margins.

The 96.6% TiO₂ result from bulk sample metallurgical testwork is commercially significant. Chloride-process pigment plants typically require a minimum rutile feedstock purity of around 95% TiO₂, with premium pricing available above that threshold. Fortuna Metals produced high-purity rutile results that already sit comfortably in commercially competitive territory relative to Sierra Rutile and Kwale concentrate specifications — a gating question that exploration-stage projects often leave unanswered for years.

Why the JORC Classification Matters More Than the Tonnage Ranking

Fortuna has placed Mkanda inside the top six largest contained rutile deposits globally based on peer comparison data. That ranking has genuine geological merit, but it comes with a caveat that the company itself highlights: every higher-ranked peer carries Indicated or Measured tonnes, while Mkanda's entire resource sits at the Inferred classification level.

Under the JORC Code 2012, the primary framework used by ASX-listed mining companies, resource classifications carry specific meanings:

- Inferred: The lowest confidence tier, based on limited geological data and drill spacing, typically 400m x 400m or wider. Geological continuity is assumed but not statistically demonstrated.

- Indicated: Intermediate confidence, requiring infill drilling to approximately 200m x 200m spacing and more rigorous geostatistical validation of grade continuity.

- Measured: The highest confidence tier, underpinning feasibility-level economic studies and typically requiring 100m x 100m or closer drill spacing.

The practical implication is that Inferred tonnes cannot be used directly in the economic modelling that underlies scoping or feasibility studies. The path from today's 298 Mt Inferred resource to a bankable project requires a substantial infill drilling campaign to upgrade at least a portion of the tonnes to Indicated classification.

Investors who focus exclusively on the tonnage ranking without understanding the classification hierarchy risk misinterpreting where Mkanda sits in its development lifecycle. A top-six ranking built on Inferred tonnes is a geological achievement, not a production-ready asset.

The Aircore Signal: Why the Next Drilling Phase Could Reshape the Entire Resource

Hand Auger vs. Aircore: A Technical Distinction With Material Consequences

The entire maiden MRE at Mkanda is built on hand auger drilling data, with an average hole depth of approximately 8.4 metres. Hand auger is a well-established technique for sampling shallow regolith mineralisation, and it is the industry-standard method for initial characterisation of this deposit type. However, it provides no information about what exists below the near-surface weathering profile.

| Drilling Method | Average Depth | Contribution to Maiden MRE |

|---|---|---|

| Hand Auger | ~8.4 metres | 100% of the 298 Mt maiden resource |

| Aircore (initial 14 holes) | ~27 metres | Not included; assays pending H2 2026 |

The 14 initial aircore holes completed at Mkanda average 27 metres in depth, representing more than three times the penetration depth of the hand auger dataset underpinning the current resource. Crucially, none of the aircore data has been incorporated into the maiden MRE, meaning the current 298 Mt number reflects only the near-surface component of what may be a substantially thicker mineralised system.

In regolith-hosted rutile deposits, the weathering profile can extend to significant depth depending on the intensity and duration of the laterisation process. Where mineralisation is driven by primary crystalline sources that have been deeply weathered, the grade-bearing horizon can continue well below the hand auger sampling window. Aircore drilling is specifically designed to test this deeper zone, and its results will determine whether the near-surface resource reflects the full mineralised system or merely its upper expression. Understanding proper drill results interpretation is therefore essential when assessing the significance of the pending aircore assays.

The Kasiya Precedent: Instructive but Not Predictive

The comparison between Mkanda and Sovereign Metals' Kasiya is analytically unavoidable given the 20-kilometre separation between the two projects and their shared geological setting. At Kasiya, the transition from hand auger to aircore drilling contributed to a resource expansion from approximately 644 Mt to roughly 1,800 Mt — a scale change that fundamentally repositioned the project's global significance.

This historical trajectory is worth understanding at the methodological level. Kasiya's hand auger resource underestimated the total mineralised system because the weathering profile extended considerably deeper than initial shallow sampling revealed. Aircore drilling exposed that depth extension, and the resource grew accordingly.

The geological setting at Mkanda shares key characteristics with Kasiya: similar host geology, comparable weathering profiles, and the same broad mineralisation style. Whether those similarities translate into a proportionally similar depth extension outcome is a question that only drill results can answer.

Speculative parallel: If Mkanda's mineralisation follows a comparable depth extension pattern to Kasiya, the 298 Mt maiden resource could represent a fraction of the total system. This is a hypothesis, not a forecast, and it should be treated as optionality rather than expectation.

Beyond Rutile: The Multi-Commodity Dimension of Mkanda's Economic Thesis

Graphite, Zircon, and Monazite as Value Multipliers

One of the less-discussed structural features of regolith-hosted rutile deposits in this geological belt is their propensity to carry multiple heavy mineral species within the same mineralised matrix. At Mkanda, graphite, zircon, and monazite are present alongside rutile, and each carries distinct economic implications.

The 3.55 Mt of contained graphite at 1.19% TGC in the maiden MRE is a number that deserves context. At Kasiya, graphite by-product credits uplift the rutile equivalent grade from approximately 0.96% to 1.51% — a differential that substantially alters project-level economics when modelled through a discounted cash flow framework. A comparable uplift at Mkanda, if metallurgical recoveries confirm economic graphite extraction, would meaningfully shift the project's economic attractiveness.

Zircon is a well-established co-product in heavy mineral sand operations globally and typically commands a stable price point that improves the overall revenue basket of multi-product operations. Its characterisation work at Mkanda is ongoing through H2 2026.

Monazite carries a different strategic dimension entirely. As a phosphate mineral that concentrates heavy rare earth elements (HREEs) including dysprosium and terbium, monazite is directly relevant to permanent magnet supply chains that underpin electric motor technology. The global scarcity of HREE supply sources outside China gives monazite-bearing deposits a strategic significance that extends beyond simple commodity economics.

| By-Product | Current Status | Potential Economic Impact |

|---|---|---|

| Graphite (3.55 Mt contained) | In maiden MRE; recovery unconfirmed | Significant rutile equivalent grade uplift |

| Zircon | Characterisation ongoing (H2 2026) | Additional revenue stream; margin improvement |

| Monazite (HREE-bearing) | Characterisation ongoing (H2 2026) | Potential strategic critical minerals exposure |

The important caveat across all three by-products is that presence in the resource does not equal economic recoverability. Metallurgical testwork must confirm that each mineral can be selectively separated, concentrated to a saleable specification, and recovered at a rate that justifies the additional processing complexity. None of this is confirmed at Mkanda, and investors should treat by-product optionality as a potential upside scenario rather than a base-case assumption.

Global Peer Benchmarking: Where Does Mkanda Fit?

Comparing Grade, Scale, and Product Quality Across Major Rutile Projects

| Project | Operator | Resource Scale | Rutile Grade | Classification | TiO₂ Product Purity |

|---|---|---|---|---|---|

| Kasiya | Sovereign Metals | ~1,800 Mt | ~0.96% Ru Eq | Indicated/Inferred | High purity |

| Sierra Rutile | Iluka Resources | Producing asset | Varies by zone | Measured/Indicated | ~95%+ TiO₂ |

| Kwale | Base Resources | Producing asset | Varies by zone | Measured/Indicated | ~95%+ TiO₂ |

| Mkanda | Fortuna Metals | 298 Mt | 0.87% | Inferred only | 96.6% TiO₂ |

The most instructive column in this comparison is TiO₂ product purity. At 96.6%, Mkanda's bulk sample result exceeds the commercial threshold and is competitive with concentrate grades from projects that are already in production. For an exploration-stage asset at the maiden resource stage, having early product quality validation removes a significant layer of technical uncertainty from the investment thesis.

Grade, however, tells only part of the story. The critical differentiator for project economics is the combination of grade, tonnage, depth of mineralisation (which influences strip ratio), processing complexity, and logistics costs. Mkanda's shallow, near-surface character at an average depth of 4.1 metres is a structural advantage on the first two of those variables, but the other three remain to be quantified through scoping and feasibility work. Furthermore, benchmarking against the largest global mines by resource scale underscores just how significant Mkanda's maiden tonnage is at this early stage.

The next major ASX story will hit our subscribers first

Key Milestones: The Catalyst Timeline That Will Define Mkanda's Trajectory

Near-Term Catalysts: H2 2026

- Aircore assay results: The single most consequential data release in Mkanda's near-term development. Determines whether 298 Mt represents a floor or an approximate ceiling for the resource.

- Zircon and monazite characterisation results: Defines whether the multi-commodity thesis has metallurgical support and whether the project's strategic minerals classification is materially enhanced.

- Additional drill hole assay completions: Hundreds of pending assay results from the continuing programme may contribute to a resource update ahead of a formal infill campaign.

Medium-Term Milestones: 2027 and Beyond

- Infill drilling campaign: Required to tighten drill spacing from 400m x 400m toward 200m x 200m and upgrade Inferred tonnes toward Indicated classification.

- Scoping study: The first structured economic framework for the project, dependent on a higher-confidence resource base and preliminary metallurgical test data.

- Prefeasibility and definitive feasibility studies: Sequential gateways toward a production decision, each conditional on the quality of the preceding work. A definitive feasibility study represents the final technical and financial gateway before any production decision can be made.

- WNDRCO strategic partner vesting condition: A background structural consideration that carries implications for ownership economics through to 2029.

How a Rutile Exploration Project Advances: Step by Step

- Maiden Inferred MRE completed at Mkanda, establishing tonnage and grade base.

- Aircore depth extension drilling tests mineralisation below the hand auger window.

- Resource expansion and confidence upgrade via infill drilling to Indicated classification.

- Scoping study provides first economic modelling framework.

- Prefeasibility study (PFS) delivers detailed technical and financial analysis.

- Definitive feasibility study (DFS) constitutes the final investment decision gateway.

- Project financing, offtake agreements, and construction follow a positive DFS outcome.

The Bull and Bear Framework: Weighing the Investment Case Objectively

Constructive Arguments for the Mkanda Story

- A maiden resource of 298 Mt places Mkanda in globally significant company on tonnage at first publication — a hurdle that took peer projects multiple drill campaigns to clear.

- The 96.6% TiO₂ product quality from bulk sample testwork provides early commercial credibility before metallurgical studies are formally complete.

- Aircore drilling results expected in H2 2026 represent genuine, unpriced optionality. If depth extension is confirmed, the resource base could expand materially from its current starting point.

- Multi-commodity exposure across graphite, zircon, and monazite creates multiple independent value pathways and potential economic uplift scenarios.

- Proximity to Kasiya, one of the most extensively drilled and validated rutile systems on the planet, de-risks the geological thesis in ways that a standalone greenfield project cannot match.

Cautionary Factors for Disciplined Assessment

- The full 298 Mt resource is Inferred — the lowest JORC confidence tier. Geological continuity at 400m x 400m spacing is assumed, not statistically demonstrated.

- No by-product credits are confirmed until metallurgical recoveries are validated at commercially representative scale.

- The path from Inferred resource to production decision involves years of additional work, multiple capital raises, and regulatory navigation in a developing jurisdiction.

- Peer comparisons using Indicated and Measured tonnes versus Mkanda's Inferred base should be read with interpretive discipline.

- The WNDRCO vesting condition introduces an ownership complexity layer that investors should understand independently before sizing a position.

Investor Reminder: Mineral resources at the Inferred stage are geological interpretations, not confirmed orebodies. All investment decisions should be made with reference to the full JORC disclosure, independent technical advice, and a realistic understanding of the timeline and capital intensity involved in advancing an exploration project toward production.

Frequently Asked Questions: Fortuna Metals Mkanda Rutile Resource

What is the total size of the Mkanda rutile resource?

The maiden Inferred Mineral Resource Estimate stands at 298 million tonnes at 0.87% rutile and 1.19% total graphitic carbon, using a 0.7% rutile cut-off. A higher-confidence grade slice at 0.8% cut-off contains 159 Mt at 0.98% rutile.

How does Mkanda rank globally among rutile deposits?

Based on peer comparison data published by Fortuna Metals, Mkanda ranks within the top six largest contained rutile deposits globally by tonnage. All higher-ranked peers carry Indicated or Measured classification, while Mkanda's resource remains entirely Inferred.

What is the TiO₂ product purity at Mkanda?

Bulk sample metallurgical testwork produced a rutile concentrate grading 96.6% TiO₂, which is commercially competitive with concentrate specifications from major producing operations and exceeds the threshold typically required by chloride-process pigment plants.

What drilling methods underpin the maiden MRE?

The maiden resource is based entirely on hand auger drilling at an average depth of approximately 8.4 metres. Fourteen initial aircore holes averaging 27 metres depth have been completed but are not included in the current resource. Their assay results are expected in H2 2026.

What by-products does Mkanda contain?

The project hosts 3.55 Mt of contained graphite at 1.19% TGC within the maiden MRE. Zircon and monazite (a heavy rare earth-bearing phosphate mineral) have also been identified, with characterisation work ongoing through H2 2026.

How does Mkanda compare to Sovereign Metals' Kasiya project?

Kasiya, located approximately 20 km north of Mkanda, currently stands as the world's largest rutile deposit at roughly 1,800 Mt. The two projects share similar geological settings and deposit styles. Kasiya's resource grew from approximately 644 Mt to 1,800 Mt following the transition from hand auger to aircore drilling — a trajectory that the ongoing aircore programme at Mkanda is now beginning to test. Independent analysis from Pitt Street Research further contextualises how Mkanda's JORC resource definition is shaping up relative to that precedent.

What are the most important upcoming catalysts for Mkanda?

The highest-priority catalyst is the aircore assay results expected in H2 2026, which will determine whether the current 298 Mt base case expands materially with depth. Secondary catalysts include zircon and monazite characterisation data and any additional resource updates from the continuing drill programme.

What 298 Mt Actually Means: Context, Caution, and the Path Forward

Positioning the Fortuna Metals Mkanda rutile resource within its correct analytical context requires holding two ideas simultaneously. The maiden MRE is a genuine geological achievement, establishing a globally competitive tonnage base at first publication and providing early product quality validation through bulk sample testwork. At the same time, it is precisely that: a first number, constructed from shallow hand auger data, classified at the lowest JORC confidence tier, and representing only the near-surface expression of a mineralised system that has not yet been tested at depth by a systematic aircore programme.

The H2 2026 aircore assay results will be the most consequential single dataset in Mkanda's development history to this point. If depth extension is confirmed at grade, the conversation shifts from a 298 Mt Inferred resource to something materially larger and more geologically credible. If mineralisation is shown to be thin or grade-depleted below the hand auger window, the resource definition work becomes more focused on lateral expansion and infill confidence.

Either outcome provides critical information. The market's job between now and those results is to appropriately price the optionality — neither dismissing the geological setting because the resource is Inferred, nor assuming that Kasiya-scale expansion is inevitable because the two projects share a geological address.

The rutile supply gap is structural, the product quality case at Mkanda is already established, and the geological framework is one of the most de-risked exploration addresses for this commodity on the planet. Whether those foundations support a top-tier global project will be answered progressively through 2026 and 2027, one drill result at a time.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across more than 30 commodities — delivering real-time alerts on significant mineral discoveries like the rutile and graphite systems reshaping global supply maps. Explore why historic ASX discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.