July 24, 2026

The Quiet Commodity Reshaping Western Defence Supply Chains

Few industrial metals carry as much strategic weight per tonne as tungsten. It is not traded on mainstream exchanges with the visibility of copper or gold, and it rarely features in retail investor conversations. Yet inside the defence establishments of NATO nations, aerospace engineering facilities, and the procurement offices of U.S. industrial manufacturers, tungsten has quietly moved to the centre of a supply chain crisis that has been building for years.

The mechanism driving this crisis is straightforward. One country produces roughly 80% of the world's tungsten supply, controls the processing infrastructure, and has the policy leverage to restrict access at will. When Beijing introduced new export restrictions in 2025, reducing the number of authorised tungsten exporters to just 15 entities for the 2026–2027 cycle, the downstream consequences were immediate and structural. Western buyers who had relied on Chinese-origin tungsten for decades suddenly found themselves without a reliable primary source for one of their most strategically irreplaceable inputs.

Into this vacuum, a small landlocked nation in Central Africa has emerged as an unlikely solution. Rwanda tungsten exports to the United States represent one of the most consequential new trade relationships in the global critical minerals landscape.

When big ASX news breaks, our subscribers know first

Tungsten's Unique Physical Properties Make It Irreplaceable

Understanding why this supply disruption matters requires understanding what tungsten actually does. With the highest melting point of any pure metal at approximately 3,422°C, a density nearly twice that of lead, and hardness properties that enable precision cutting at tolerances impossible with alternative materials, tungsten's strategic importance in materials science is without parallel.

These properties translate into specific, mission-critical applications:

- Defence sector: Armour-penetrating munitions, missile guidance components, and high-performance aerospace alloys

- Automotive manufacturing: Tungsten carbide tooling used in precision machining for engine components, transmission parts, and body fabrication

- Electronics: Heat-resistant contacts, filaments, and semiconductor components

- Aerospace: Radiation shielding, high-temperature structural components, and turbine blade coatings

- Electric vehicles: Emerging drivetrain applications driven by the precision manufacturing requirements of EV powertrains

No commercially viable substitute currently exists for tungsten in high-temperature and high-density defence applications. This creates an inelastic demand floor that persists regardless of price. When supply tightens, prices rise and procurement becomes urgent, but demand does not diminish.

How Ammonium Paratungstate Became the Market's Pressure Gauge

Most commodity markets use a primary traded form as their pricing benchmark. For tungsten, that benchmark is ammonium paratungstate, commonly abbreviated as APT. This intermediate processing product sits between raw wolframite ore and the refined powders used by manufacturers, and its price serves as the global reference point for the entire tungsten value chain.

In late April 2026, APT prices surpassed $3,000 per tonne, a threshold that reflects one of the sharpest rallies in recent memory. The price acceleration had been building since the start of 2026, driven by a convergence of supply-side restrictions and accelerating critical minerals demand from sectors restocking after years of drawdown.

When APT prices rise, the signal transmits backward through the supply chain in real time, affecting concentrate-level pricing at mining operations and ultimately influencing investment decisions about production expansion.

The key drivers behind this price rally are not temporary. They reflect structural shifts that analysts believe will define tungsten markets for the remainder of this decade:

| Driver | Impact Level | Time Horizon |

|---|---|---|

| Chinese export restrictions (2025) | High | Near-to-medium term |

| Reduced Chinese mining quotas | High | Medium term |

| Defence sector restocking | Medium-High | 2026–2028 |

| Automotive sector demand growth | Medium | Ongoing |

| Western supply chain diversification | Medium-High | Long term |

Military and defence applications currently represent approximately 12% of total tungsten consumption, with projections from consultancy Project Blue forecasting growth to 15% by 2027–2028 as NATO-aligned nations and allied states rebuild depleted stockpiles. The automotive sector remains the largest single end-use market, accounting for 25–30% of global demand according to Argus, the commodity analysis firm. These figures are grounded in documented procurement programmes and observable production trends.

Why Defence Metal Shortages Are Accelerating Western Action

Furthermore, defense metal shortages across multiple critical inputs have intensified urgency within Western procurement offices. Tungsten is not an isolated case but part of a broader pattern of supply chain vulnerability that policymakers are now racing to address.

Rwanda's Industrial Advantage Over Every Other African Producer

Central Africa contains two meaningful tungsten-producing nations: Rwanda and the Democratic Republic of Congo. However, comparing their production profiles reveals a gap so large that they are effectively operating in different industries.

| Metric | Rwanda (2024) | DRC (2025) |

|---|---|---|

| Tungsten export volume | 2,383.9 tonnes | 94.5 tonnes (wolframite) |

| Export value | $35.76 million | $1.3 million |

| Production method | Industrial (mechanised) | Entirely artisanal |

| Primary ore type | Wolframite | Wolframite |

| U.S. supply chain integration | Established | Not yet established |

| Volume differential | Rwanda exports approximately 25x DRC volume | Baseline |

The DRC's tungsten sector produces 213 tonnes of wolframite annually through entirely artisanal methods, of which only 94.5 tonnes reach export markets. To put that in context, the DRC exported 46,251 tonnes of cassiterite (tin ore) in the same period, valued at $652 million. Tungsten is barely a rounding error in Kinshasa's mineral economy at present, whilst tin remains a commanding revenue driver.

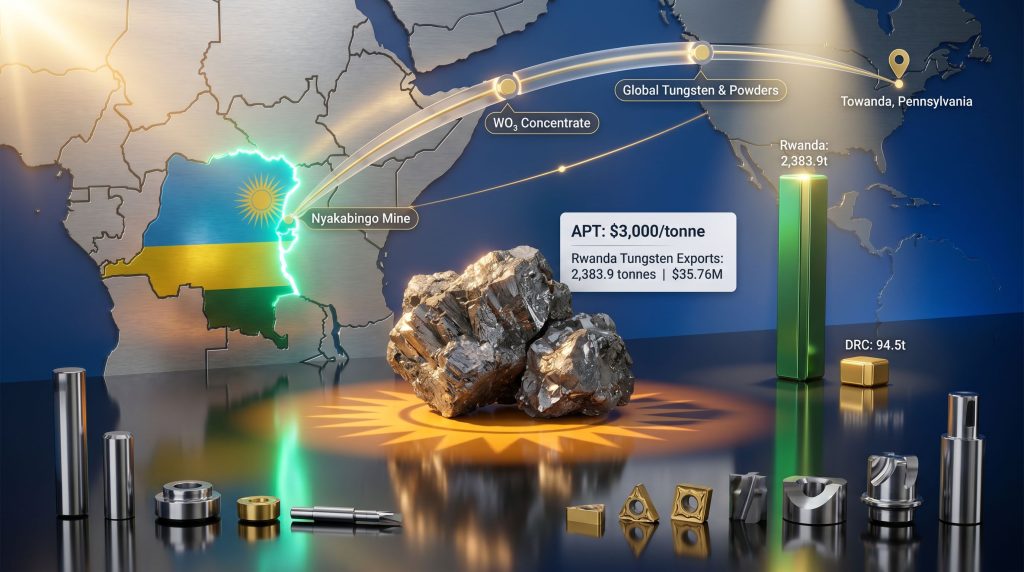

Rwanda, in contrast, operates on a fundamentally different model. Official data shows the country exported 2,383.9 tonnes of tungsten in 2024, generating $35.76 million in declared export value — an implied average realised price of approximately $15,000 per tonne at the concentrate level. This makes Rwanda Africa's leading tungsten supplier by a substantial margin.

The Nyakabingo Mine: Scale, Resources, and Operational Trajectory

The engine behind Rwanda's tungsten output is the Nyakabingo mine in northern Rwanda, operated by Trinity Metals and widely recognised as the largest tungsten project on the African continent. The mine's operating metrics provide a useful lens for understanding both its current scale and its expansion potential:

- Monthly production capacity: 100–110 tonnes of wolframite concentrate

- Annualised production: Minimum 1,200 tonnes per year at current run rates

- Recoverable resource base: Over 115,000 tonnes, providing a multi-decade production runway

- Post-acquisition output growth: Trinity Metals tripled production following its acquisition of the asset in 2022, demonstrating substantial operational leverage from targeted capital investment

- Strategic investor: TechMet, a critical minerals investment firm with U.S.-linked backing, holds a stake in Trinity Metals

The 115,000-tonne recoverable resource figure is particularly significant for long-term supply chain planning. At current production rates of approximately 1,200–1,320 tonnes per year, the Nyakabingo resource base represents a production horizon exceeding 85 years. This eliminates resource depletion as a near-term risk and positions the asset as a durable, long-term anchor for Western procurement programmes.

A detail not widely understood in broader market discussions is what Trinity Metals' tripling of output post-2022 actually signals. The resource was not expanded; the geology was already there. What changed was capital allocation, management capability, and processing infrastructure. This pattern of operational leverage suggests that further production expansion from the same geological base remains achievable without the discovery of new mineralization.

Rwanda's Broader Mineral Economy: Context Behind the Numbers

Total mineral export revenues reached $1.7 billion in 2024, compared with $373 million in 2017, representing more than a fourfold increase over seven years. Forward projections place annual mineral export revenues at approximately $2.2 billion by 2029.

Tungsten sits alongside tin and coltan as one of the "3T" critical metals forming the backbone of Rwanda's extractive economy. The country has invested substantially in mineral traceability frameworks and conflict-free certification systems, strengthening its critical minerals supply chains appeal in an era of increasingly stringent downstream due diligence requirements.

An important nuance that current revenue forecasts have not fully captured: the impact of rising APT prices on Nyakabingo's future revenue profile remains unquantified in official projections. If current price levels are sustained or extended, the gap between stated 2024 revenue figures and what the same volumes would generate in a $3,000+ APT price environment represents material unrecognised upside.

From Agreement to Shipment: How Rwanda Became a U.S. Tungsten Supplier

Rwanda tungsten exports to the United States did not emerge spontaneously from market forces. They are the product of deliberate diplomatic and commercial architecture constructed over several years and formalised in 2025.

The sequence of events establishing this supply chain is instructive:

- Commercial partnership formation: Trinity Metals concluded a supply agreement with Global Tungsten & Powders (GTP), a subsidiary of Austria's Plansee Group, alongside offtake partner Traxys, creating the commercial framework for direct U.S.-bound shipments

- Bilateral trade framework: Rwanda and the United States signed a trade agreement in August 2025, establishing the diplomatic foundation for formal supply chain integration

- First industrial-scale shipment: The initial delivery of Rwandan wolframite concentrate arrived at GTP's processing facility in Towanda, Pennsylvania, in September 2025, marking a historic first in the bilateral trade relationship

- U.S. government financial involvement: TechMet, Trinity Metals' principal investor, has received financial backing from the U.S. International Development Finance Corporation (DFC), creating a formal link between U.S. strategic capital and Nyakabingo's operational continuity

Prior to this framework, the bilateral tungsten trade was negligible. UN COMTRADE data recorded only $480,460 in Rwandan tungsten exports to the United States in 2018, with no comparable volumes in subsequent years. The September 2025 shipment therefore represents not an incremental increase but a categorical shift in the trade relationship.

The involvement of the U.S. International Development Finance Corporation as a financial backer of TechMet signals a formal U.S. government interest in securing Rwandan tungsten for American industrial and defence supply chains.

The Commercial Actors Enabling This Supply Chain

The physical flow of tungsten from a mine in northern Rwanda to a manufacturing facility in Pennsylvania involves a specific constellation of commercial actors, each fulfilling a distinct function:

| Entity | Role | Headquarters |

|---|---|---|

| Trinity Metals | Mine operator at Nyakabingo | Rwanda / UK |

| TechMet | Strategic investor in Trinity Metals | Ireland / USA |

| U.S. DFC | Government-backed financial supporter of TechMet | United States |

| Global Tungsten & Powders (GTP) | Offtake buyer and downstream processor | USA (Plansee Group, Austria) |

| Traxys | Offtake partner and commodity trading intermediary | Luxembourg / Global |

GTP's Towanda, Pennsylvania facility is one of the few locations in the United States capable of processing raw wolframite concentrate into the refined tungsten powders and intermediates required by defence contractors and industrial manufacturers. The Plansee Group, GTP's Austrian parent, is a globally recognised tungsten processing specialist, providing the downstream technical capability that completes the supply chain from Rwandan mine to American end-user.

Step-by-Step: The Physical Journey of Rwandan Tungsten

For those unfamiliar with how a mining supply chain actually functions, the journey from geological resource to industrial application involves several discrete and technically demanding stages:

- Extraction at Nyakabingo, where wolframite ore is mined from the deposit at a rate of 100–110 tonnes of concentrate per month

- On-site beneficiation, where raw ore is upgraded into high-grade tungsten trioxide (WO₃) concentrate through gravity separation and processing equipment

- Export logistics, where concentrate is transported through Rwanda's infrastructure to international shipping channels — a process complicated by the country's landlocked geography

- Receipt at Towanda, where GTP's Pennsylvania facility accepts the concentrate for further processing into tungsten metal powders and chemical intermediates

- End-use manufacturing, where processed tungsten powders are supplied to U.S. defence contractors, aerospace manufacturers, electronics producers, and EV component suppliers

One operational factor that deserves more attention than it typically receives is step three. Rwanda's landlocked status is a genuine structural cost disadvantage relative to coastal producing nations. Export logistics costs represent a real constraint on competitiveness, particularly as volumes scale.

The DRC's Potential and Current Limitations

The Democratic Republic of Congo occupies the same geological region as Rwanda and shares similar wolframite ore body characteristics. Its current tungsten sector output, however, reflects a fundamentally different state of industrial development.

With 213 tonnes of total wolframite production in 2025, all of it from artisanal sources, and exports of just 94.5 tonnes valued at $1.3 million, the DRC is decades behind Rwanda in terms of supply chain readiness for Western industrial buyers. The scale differential — roughly 25 times lower export volumes — is not primarily a geological limitation but an operational and governance one.

| Factor | Rwanda | DRC |

|---|---|---|

| Production scale | Industrial mechanised | Entirely artisanal |

| Governance framework | Established, conflict-free certification | Developing |

| U.S. trade agreement | Signed August 2025 | Under discussion |

| DFC-backed investment | Operational (TechMet/Trinity Metals) | Indirect/emerging |

| Supply chain readiness for Western buyers | Operational | Pre-commercial |

| Near-term export potential to U.S. | High | Low-to-medium |

Consequently, US critical minerals production policy is increasingly focused on partnerships with established, governance-compliant producers like Rwanda, rather than relying on markets still developing their industrial frameworks. Should the DRC successfully formalise and industrialise its tungsten sector, competitive pressure on Rwanda's market position could intensify over the medium term.

The next major ASX story will hit our subscribers first

What the APT Price Rally Means for Future Revenue Projections

Rwanda exported 2,383.9 tonnes of tungsten in 2024 at an implied average realised price of approximately $15,000 per tonne for a total declared value of $35.76 million. That calculation reflects market conditions before the current APT rally. Furthermore, record tungsten prices have positioned Rwanda further ahead of regional competitors and more prominently on the U.S. supply radar than at any previous point.

With APT prices now exceeding $3,000 per tonne at the intermediate benchmark level, the revenue implications at the concentrate level have not yet been formally quantified by analysts covering either Trinity Metals or Rwanda's broader mineral sector. Several factors amplify the potential upside:

- The 115,000-tonne recoverable resource at Nyakabingo means production can be scaled without the capital and timeline risk of new resource discovery

- The multi-year offtake agreement with GTP provides contractual revenue certainty that reduces commercial risk during price cycles

- Defence sector demand growth from approximately 12% to a projected 15% of global consumption between 2027 and 2028 represents hundreds of additional tonnes of annual demand entering Western procurement channels

- Rwanda's conflict-free mineral certification carries increasing commercial value as U.S. and European procurement frameworks tighten around provenance requirements

Risk Factors That Could Alter This Trajectory

While Rwanda's structural positioning in the Western tungsten supply chain appears durable, several material risk factors warrant monitoring by investors and policymakers tracking this sector.

- Price volatility: Tungsten markets have experienced significant cycles historically. A reversal in APT prices, potentially triggered by a Chinese decision to increase export authorisations or release strategic reserves, could compress margins at Nyakabingo and delay expansion timelines

- Landlocked logistics costs: Rwanda's geography imposes a structural cost disadvantage that limits competitive pricing flexibility relative to coastal producing nations

- Geopolitical dependencies: The Rwanda–U.S. bilateral relationship that underpins the commercial supply agreement remains subject to broader diplomatic dynamics

- DRC formalisation: Should the DRC successfully formalise and industrialise its tungsten sector, competitive pressure on Rwanda's market position could intensify over the medium term

- Chinese policy reversal: Beijing retains full capacity to adjust export authorisations, potentially increasing supply to global markets if it determines that the current price environment or geopolitical dynamics warrant a different approach

Disclaimer: The revenue projections and price forecasts discussed in this article are based on current market conditions and analyst estimates as of mid-2026. Tungsten markets are historically cyclical, and actual future prices and revenues may differ materially from projections. Nothing in this article constitutes investment advice.

Key Questions About Rwanda Tungsten Exports to the United States

What exactly does Rwanda export to the United States?

Rwanda exports high-grade wolframite concentrate, processed on-site at the Nyakabingo mine into tungsten trioxide (WO₃), which is then shipped to Global Tungsten & Powders' facility in Towanda, Pennsylvania. At Towanda, the concentrate is refined into tungsten metal powders and intermediates for use in defence, aerospace, electronics, and electric vehicle manufacturing applications.

When did the first direct tungsten shipment from Rwanda reach the United States?

The first industrial-scale shipment arrived in September 2025, one month after Rwanda and the United States signed a bilateral trade agreement in August 2025. Prior to this arrangement, UN COMTRADE data recorded only $480,460 in Rwandan tungsten exports to the U.S. in 2018, with no comparable volumes in any subsequent year.

Why is the U.S. sourcing tungsten from Rwanda specifically?

China controls approximately 80% of global tungsten production and introduced restrictive export policies in 2025 that limited authorised exporters to just 15 entities for the 2026–2027 cycle. This created immediate sourcing constraints for Western defence and industrial buyers. Rwanda, with its industrialised Nyakabingo operation, established conflict-free certification framework, and bilateral trade relationship with Washington, represents a commercially viable and strategically aligned non-Chinese alternative.

What is the scale of Rwanda's annual tungsten production?

Rwanda exported 2,383.9 tonnes of tungsten in 2024 at a total declared value of $35.76 million. The Nyakabingo mine produces between 100 and 110 tonnes of wolframite concentrate per month, with a recoverable resource base exceeding 115,000 tonnes providing a multi-decade production horizon.

Why does the APT price matter to Rwanda's tungsten revenues?

Ammonium paratungstate serves as the global benchmark intermediate in tungsten processing, and its price sets the reference point for concentrate-level transactions throughout the supply chain. With APT surpassing $3,000 per tonne in late April 2026, the revenue impact on Nyakabingo's concentrate pricing has not yet been formally quantified, suggesting that current revenue projections may understate the financial benefit of the current price environment.

Is Rwandan tungsten certified as conflict-free?

Rwanda operates a formal mineral traceability and certification framework, and the country's tungsten exports — including material from Nyakabingo — are classified as conflict-free and compliant with international due diligence standards. This certification carries significant commercial value for U.S. defence and industrial procurement programmes operating under increasingly stringent mineral provenance requirements.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

As tungsten and other strategic commodities reshape Western defence supply chains, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts on significant mineral discoveries — instantly translating complex geological data into actionable investment insights for traders and long-term investors alike. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself ahead of the broader market.