June 7, 2026

The Arabian Shield and the $2.5 Trillion Question: What Saudi Arabia's Mining Surge Really Signals

Few geological formations on Earth have attracted as little commercial attention as the Arabian Shield relative to their true potential. Spanning roughly 670,000 square kilometres across western Saudi Arabia, this ancient Precambrian basement rock hosts mineral systems that geologists have long recognised as analogous to productive terrains in West Africa and the Pilbara region of Western Australia. For decades, however, the economic logic of the Kingdom pointed firmly toward hydrocarbons, leaving much of this geological endowment in a state of deliberate dormancy. That calculus is now shifting with measurable velocity.

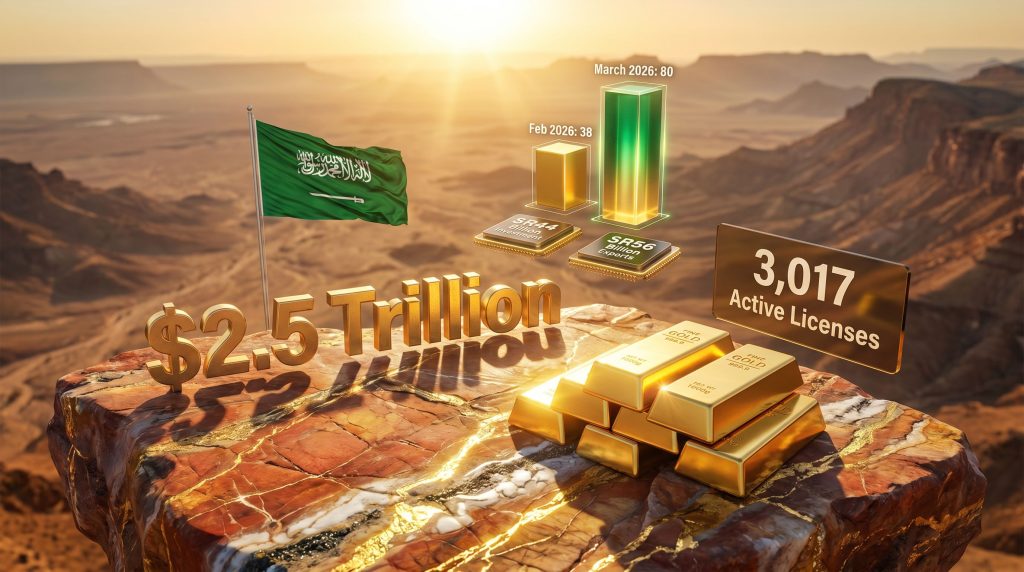

The issuance of Saudi Arabia mining licenses — 80 new licenses during March 2026 — is not simply an administrative milestone. It represents the visible surface of a much deeper institutional transformation, one designed to convert dormant geological potential into a functioning third economic pillar alongside oil and petrochemicals.

When big ASX news breaks, our subscribers know first

Why the Arabian Shield Is Geologically Unique and Commercially Underexplored

The Arabian Shield's mineralisation profile is far more varied than most outside the industry appreciate. It hosts orogenic gold systems, volcanogenic massive sulphide (VMS) deposits, and sedimentary phosphate sequences of global significance. VMS deposits, for context, are formed at ancient seafloor spreading centres and typically contain polymetallic assemblages of copper, zinc, lead, gold, and silver in a single geological body.

The Mahd Ad Dahab gold mine, which translates roughly as the Cradle of Gold, has been in operation since the 1930s and represents only the most visible expression of what the Shield may contain across its full extent. Furthermore, the Arabian Shield geochemical survey data continues to reveal mineralisation patterns that reinforce the region's long-term commercial promise.

What Is Exploration Maturity and Why Does It Matter?

What makes this geologically significant from an investor and policy perspective is the concept of exploration maturity. Established mining jurisdictions like Nevada in the United States or the Eastern Goldfields of Western Australia have been systematically drilled, mapped, and geochemically sampled over many decades. The Arabian Shield, by contrast, remains at an early stage of systematic modern exploration, meaning the statistical probability of meaningful new discoveries at surface or near-surface depths remains comparatively high.

This is precisely why the dominance of exploration licenses in the March 2026 data carries strategic weight. In addition, Saudi exploration licences are increasingly attracting international attention as the Kingdom positions itself as a credible emerging mining jurisdiction.

Breaking Down Saudi Arabia's 80 New Mining Licenses: What Was Actually Issued?

The March 2026 licensing data reveals a sector that is deliberately sequencing its development across multiple value chain stages simultaneously.

| License Type | Licenses Issued (March 2026) | Share of Total |

|---|---|---|

| Exploration Licenses | 49 | 61.3% |

| Building Materials Quarry Licenses | 20 | 25.0% |

| Small-Scale Mining Exploitation Licenses | 8 | 10.0% |

| Reconnaissance Licenses | 2 | 2.5% |

| Surplus Mineral Ore Licenses | 1 | 1.3% |

| Total | 80 | 100% |

What each category signals about the sector's current maturity level deserves careful unpacking:

-

Exploration licenses (49): The commanding majority position of exploration permits confirms Saudi Arabia is still operating predominantly in an upstream discovery mode. Exploration licenses grant the holder the right to conduct systematic geological surveys, geochemical sampling, and drilling within a defined tenure area, but do not yet permit commercial extraction.

-

Building materials quarry licenses (20): These are directly tied to the Kingdom's domestic construction pipeline. Giga-projects including NEOM, the Red Sea Project, and Diriyah Gate collectively require enormous volumes of aggregate, limestone, and construction-grade rock, and local quarrying reduces costly import dependency.

-

Small-scale mining exploitation licenses (8): This category is perhaps the most commercially meaningful signal in the dataset. Exploitation licenses permit actual extraction and represent the conversion of geological knowledge into revenue-generating activity.

-

Reconnaissance licenses (2): These are the earliest-stage permits in the mining value chain, authorising regional geophysical surveys and remote sensing analysis before any ground-based work begins.

-

Surplus mineral ore licenses (1): A niche but strategically logical permit type that allows secondary processing of mineralised waste streams from existing operations, improving resource efficiency.

Total Active License Portfolio as of March 2026

| License Category | Active Licenses |

|---|---|

| Building Materials Quarry Licenses | 1,571 |

| Exploration Licenses | 1,075 |

| Small-Scale Mining Licenses | 285 |

| Reconnaissance Permits | 76 |

| Surplus Mineral Ore Licenses | 10 |

| Total Active Licenses | 3,017 |

The ratio of exploration licenses to exploitation licenses across the active portfolio reflects a sector that has accumulated substantial upstream positions but is only beginning to convert those positions into commercial production. This conversion lag is normal in mining, but the pace at which Saudi Arabia is compressing that timeline through regulatory reform is atypical for an emerging jurisdiction.

Moreover, the full breakdown of Saudi mining licences by category underscores how methodically the Kingdom is building its regulatory architecture across the entire mining value chain.

The 110% Month-on-Month Jump: Reading the Acceleration Signal

The February 2026 baseline of 38 licenses compared against March's 80 represents a month-on-month acceleration exceeding 110%. To contextualise why this matters beyond the headline number, consider that licensing throughput in any jurisdiction is constrained by regulatory bandwidth, application quality, and institutional processing capacity. A doubling within a single month therefore implies one or more of the following dynamics are at work:

- A deliberate policy directive to accelerate approval timelines through digital permitting systems and streamlined assessment criteria.

- A surge in qualified applications from domestic and international mining companies responding to favourable fiscal terms.

- A backlog clearance event, where applications lodged in prior periods were approved in batch during March.

- Coordinated institutional capacity building within the Ministry of Industry and Mineral Resources that has increased throughput velocity sustainably.

The most likely explanation is a combination of factors two and four. Consequently, the broader 2025 sector performance data suggests genuine demand growth rather than administrative anomaly. For further context, recent reporting from Arab News provides additional detail on how Saudi Arabia's regulatory institutions are responding to this surge in applications.

2025 Sector Performance: The Foundation Beneath the 2026 Surge

Understanding why Saudi Arabia's 80 new mining licenses in March 2026 matter requires grounding the analysis in what 2025 actually delivered commercially.

| Performance Indicator | 2025 Result |

|---|---|

| Total Mining Sector Investment | SR44 billion (~$11.7 billion USD) |

| Mining Exports | SR56 billion |

| Export Shipment Volume | ~29 million tonnes |

| Exploitation License Growth (Year-on-Year) | +220% |

| Exploration Spending Growth (Year-on-Year) | +110% |

The 220% year-on-year growth in exploitation licenses is the figure that most warrants attention. In mining economics, exploration spending creates optionality but exploitation creates cash flow. The fact that exploitation licenses grew more than three times faster than exploration spending in percentage terms suggests the sector has reached an inflection point where early exploration work is now converting into productive tenements at an accelerating rate.

This dynamic — where exploration activity from prior cycles begins to generate exploitation outcomes — is sometimes called the discovery-to-development lag compression, and it typically signals sector maturity beginning to take hold. Saudi Arabia appears to be entering this phase roughly a decade after the regulatory reforms that enabled modern foreign participation in its mining sector first took hold.

Critical Minerals, Battery Supply Chains, and the Geopolitical Dimension

Beyond gold, phosphate, and zinc, the mineral categories attracting the most strategic attention globally involve lithium, cobalt, manganese, and rare earth elements, all of which feed into battery cathode and anode manufacturing for electric vehicles and grid-scale energy storage. The broader critical minerals demand trajectory is fundamentally reshaping how nations assess the strategic value of their geological endowments.

Saudi Arabia's geological surveys have identified rare earth occurrences within the Arabian Shield, though the grade and tonnage data required to assess commercial viability remains largely in the pre-resource stage. However, what makes Saudi Arabia's positioning particularly significant for global supply chain architects is the combination of:

-

Geographical neutrality: Unlike the Democratic Republic of Congo for cobalt or Australia for lithium, Saudi Arabia is not yet perceived as a partisan actor in the East-West industrial competition for battery materials, giving it potential diplomatic flexibility in supplying both Asian and European battery manufacturing hubs.

-

Sovereign capital depth: The ability to deploy state-directed investment through vehicles like the Public Investment Fund means Saudi Arabia can absorb the long lead times and capital intensity of mining development without the return-timeline pressures that constrain private equity-backed operators.

-

Integrated industrial logic: Saudi Arabia's existing petrochemical processing infrastructure provides a template for developing downstream mineral processing capacity, potentially enabling value-added export of refined battery materials rather than raw ore.

Saudi Arabia's position among the world's global phosphate reserves deserves particular attention. The Kingdom's phosphate deposits, centred on the Ma'aden operation in the north of the country, place it among a small group of nations capable of influencing global fertiliser supply chains. As food security concerns intensify globally, phosphate's strategic value extends well beyond its role in battery chemistry.

The next major ASX story will hit our subscribers first

What the Licensing Velocity Means in Scenario Terms

If the March 2026 pace of 80 licenses per month were sustained across a full calendar year, the Kingdom would issue approximately 960 new licenses annually. Against the current active base of 3,017, this implies a portfolio expansion rate approaching 32% per year — a figure without precedent among major established mining jurisdictions.

The more instructive question, however, is what proportion of newly issued exploration licenses will ultimately convert to exploitation permits. Industry benchmarks from comparable emerging mining jurisdictions suggest conversion rates in the range of 10% to 25% over a five to ten year horizon, depending on geological success rates, commodity price cycles, and infrastructure accessibility.

Applying a conservative 15% conversion assumption to the current exploration license base of 1,075 active permits would imply approximately 160 additional exploitation operations entering the pipeline over the next decade. This number would represent a substantial structural shift in Saudi Arabia's non-oil production economy if realised. Furthermore, Saudi Arabia's 80 new mining licenses issued in March are already being cited as a landmark signal of the sector's accelerating trajectory.

Structural Risks That Sophisticated Investors Must Weigh

No credible analysis of Saudi Arabia's mining expansion can ignore the structural constraints that could compress actual outcomes below the trajectory implied by licensing volumes.

Geological risk remains the primary variable. A licence is an administrative instrument, not a geological guarantee. The Arabian Shield's mineral systems, while geologically promising, have not been systematically tested at the drill-hole density required to establish confidence in reserve size and grade continuity. Grade continuity — meaning the consistency of mineralisation between drill intercepts — is one of the most frequently underestimated risks in early-stage exploration programmes globally.

Water scarcity represents a constraint that is uniquely severe in the Saudi context. Mineral processing, particularly for base metals and phosphate, requires substantial volumes of water. In an environment where freshwater is scarce and desalination expensive, water sourcing for processing plants adds a cost layer not present in most competing jurisdictions.

Infrastructure access in remote Shield terrain requires road, power, and communications networks that must in many cases be built from scratch. The capital intensity of this enabling infrastructure is often underestimated in early project economics.

Skilled labour localisation presents a medium-term challenge. Technical mining roles — including mine geologists, metallurgists, and mine planners — require years of specialised training. Saudi Arabia's domestic talent pipeline in these disciplines, while growing, has not yet reached the scale the sector's ambition demands.

Frequently Asked Questions: Saudi Arabia Mining Licenses 2026

How many mining licenses did Saudi Arabia issue in March 2026?

Saudi Arabia's Ministry of Industry and Mineral Resources issued 80 new mining licenses in March 2026, comprising five distinct permit categories including exploration, quarrying, small-scale exploitation, reconnaissance, and surplus mineral ore licenses.

How does the March 2026 figure compare to previous months?

The March 2026 issuance of 80 licenses represents more than double the 38 licenses granted in February 2026, reflecting a significant acceleration in the Kingdom's regulatory throughput for the mining sector.

How many total active mining licenses does Saudi Arabia hold?

As of the end of March 2026, Saudi Arabia held 3,017 active mining licenses across all categories, with building materials quarry licenses (1,571) and exploration licenses (1,075) representing the two largest segments.

What minerals is Saudi Arabia targeting through its expanded licensing programme?

The Kingdom's mining strategy prioritises gold, zinc, phosphate, and a range of critical minerals essential to battery manufacturing and clean energy supply chains, drawing on an estimated $2.5 trillion in untapped geological reserves across the Arabian Shield.

What was the total value of Saudi Arabia's mining sector investment in 2025?

Saudi Arabia's mining sector attracted SR44 billion (approximately $11.7 billion USD) in total investment during 2025, with exploitation licenses growing 220% year-on-year and exploration spending rising 110%.

Is Saudi Arabia's mining sector open to foreign investors?

Yes. The Kingdom has implemented regulatory frameworks designed to attract international mining companies and joint ventures, with the Ministry of Industry and Mineral Resources overseeing licensing, land access, and fiscal terms for foreign participants.

Key Takeaways: What the Data Actually Tells You

-

Saudi Arabia issued 80 new mining licenses in March 2026, more than doubling February's figure of 38

-

The license mix, led by 49 exploration permits, confirms the sector remains heavily upstream, with substantial discovery pipeline growth still ahead

-

Total active licenses reached 3,017, weighted toward quarrying and exploration, with exploitation representing a growing but still minority share

-

The 2025 commercial baseline of SR44 billion in investment, SR56 billion in exports, and 29 million tonnes in shipments establishes that the sector has already moved beyond pilot-scale activity

-

The $2.5 trillion mineral reserve estimate is geologically credible given the Arabian Shield's known mineralisation profile, though significant systematic exploration remains required to convert that estimate into bankable resources

-

Structural constraints including water availability, infrastructure gaps, and technical workforce depth remain material variables that will determine the pace at which licensing velocity translates into production growth

Readers seeking ongoing coverage of Saudi Arabia's mineral sector development can follow Arab News' dedicated Mining section at arabnews.com/main-category/mining for continuing updates on licensing, investment, and production milestones.

This article contains forward-looking analysis, scenario projections, and statistical extrapolations. These do not constitute financial advice. Investors should conduct independent due diligence and consult qualified advisers before making investment decisions related to the mining sector.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market Catches On?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors — explore historic examples of exceptional discovery outcomes to understand the potential at stake, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.