June 7, 2026

Saudi Aramco cuts oil supply to Asia represents a significant strategic shift in global energy trade patterns, fundamentally altering supply chain dynamics across the Asia-Pacific region. When critical shipping routes face geopolitical pressures, energy companies must rapidly recalibrate operational models that have been optimised for decades around predictable logistics patterns. The challenge becomes particularly acute in Asia-Pacific markets, where refining complexes have been engineered around specific crude slate assumptions and established import pathways. Furthermore, these disruptions create ripple effects that extend far beyond immediate price volatility, reshaping strategic frameworks across entire industries.

Understanding the Strategic Infrastructure Realignment in Middle Eastern Energy Distribution

The fundamental architecture of global oil trading has experienced significant structural adjustments as Saudi Arabia redirects its export strategy through alternative port facilities. Saudi Arabia has reduced crude exports to Asian markets by approximately 2.753 million barrels per day, declining from 7.108 million bpd in February 2026 to 4.355 million bpd in March 2026, representing a 38.6% month-over-month contraction. This represents one of the most substantial supply route modifications in recent energy trading history.

These Saudi export realignments reflect broader strategic considerations beyond immediate operational constraints. The reconfiguration affects not only volume flows but also the fundamental pricing mechanisms that have governed Asian crude procurement for decades.

Technical Capacity Assessment of Alternative Export Infrastructure

The operational pivot toward Red Sea export facilities demonstrates both the flexibility and limitations of existing energy infrastructure. Yanbu port has achieved record volume operations during March 2026, with loading schedules concentrated exclusively on Arab Light crude specifications. This grade represents a lighter, lower-sulfur crude type compared to the typical diverse slate that Saudi Arabia normally provides to Asian refineries.

China's Sinopec has arranged 24 million barrels of Saudi crude loading from Yanbu during March 2026, illustrating how major Asian refiners are adapting procurement strategies to accommodate the infrastructure shift. However, this concentration on a single export route creates new bottleneck risks that were previously distributed across multiple shipping pathways.

The technical specifications of Arab Light crude present both advantages and constraints for Asian refining operations. This crude grade typically yields higher proportions of lighter petroleum products, which may not align with the product slate optimisation that many Asian refineries have developed around heavier crude blends.

Security Vulnerabilities in Alternative Route Operations

Infrastructure security concerns became immediately apparent when a drone incident temporarily disrupted operations at Saudi Aramco's SAMREF refinery on March 23, 2026. This incident highlighted that alternative routing strategies, while providing operational flexibility, introduce new risk vectors that require comprehensive security protocols.

The concentration of increased volumes through Yanbu creates a single-point-of-failure scenario that differs from the distributed risk profile of multi-route export strategies. Consequently, energy security planners must now evaluate whether route diversification genuinely reduces overall system vulnerability or simply shifts risk concentration to different geographic areas.

When big ASX news breaks, our subscribers know first

Asian Refinery Adaptation Strategies and Operational Constraints

The supply adjustment has created what industry sources characterise as tight supply conditions for Asian refineries, directly constraining refined product output capabilities. This tightness reflects not just volume reductions, but also the complexity of adapting refining operations to different crude specifications than originally planned. In addition, these constraints demonstrate how geopolitical developments can rapidly transform geopolitical market risks into operational realities.

Crude Slate Optimisation Under Supply Constraints

Asian refining complexes face several technical challenges when transitioning to Arab Light-only procurement from Yanbu:

- Yield optimisation complications: Refineries configured for processing heavier crude blends must adjust distillation and conversion unit operations

- Product slate mismatches: The lighter crude may produce different ratios of petrol, diesel, and other refined products than market demand requires

- Blending limitations: Reduced crude variety constrains refiners' ability to optimise feedstock combinations for maximum economic returns

- Processing unit utilisation: Some heavy oil processing equipment may operate below optimal capacity when processing lighter crudes exclusively

Regional Procurement Strategy Modifications

Sinopec's large-scale March arrangements demonstrate how major Asian refiners are securing alternative supply channels, but this approach requires significant logistical coordination and potentially higher procurement costs due to reduced supply source diversity.

The restriction to Yanbu-sourced Arab Light crude forces refineries to either:

- Accept constrained crude slate flexibility and adjust operations accordingly

- Seek alternative suppliers from other Middle Eastern or global sources to maintain desired crude blend ratios

- Modify product output targets to align with the yields achievable from available crude types

Inventory Management Protocol Adjustments

The supply constraint environment necessitates more conservative inventory management approaches across Asian refining operations. Refiners must balance the competing priorities of maintaining operational flexibility whilst avoiding excessive inventory costs during uncertain supply conditions.

Strategic inventory decisions now must account for:

- Extended lead times for alternative crude sourcing if primary supply routes remain constrained

- Quality specification variations between different crude sources that may require blending adjustments

- Storage capacity limitations that restrict the ability to stockpile diverse crude types simultaneously

Geopolitical Risk Framework Development for Energy Trade Routes

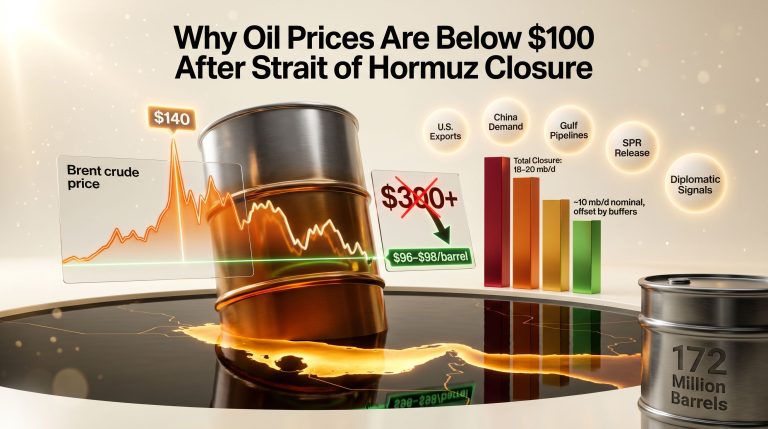

The current supply disruption stems from what has been characterised as conflicts affecting the Strait of Hormuz shipping corridor, through which approximately 20% of global oil trade typically transits. This percentage represents roughly 21 million barrels per day of crude oil and petroleum products under normal operating conditions.

Moreover, these developments illustrate broader patterns of OPEC tariff impacts on global energy trade relationships. The strategic implications extend beyond immediate supply logistics to encompass long-term alliance structures and trade agreements.

Strategic Chokepoint Vulnerability Analysis

The Strait of Hormuz represents one of several critical maritime chokepoints in global energy logistics, alongside the Suez Canal, Strait of Malacca, and Bab el-Mandeb strait. When any of these passages experiences operational constraints, alternative routes must absorb displaced volumes, often exceeding their optimal capacity limits.

Current disruption impacts extend beyond crude oil to include:

- Liquefied natural gas shipments from Qatar and other Gulf producers

- Refined petroleum products exported from Gulf refining centres

- Petrochemical feedstocks and finished chemical products

- Strategic reserve coordination between importing nations and their suppliers

The International Energy Agency has documented more than 40 severely damaged energy assets in the region, indicating that infrastructure vulnerability extends beyond shipping routes to production and processing facilities themselves.

Emergency Response Coordination Mechanisms

Strategic petroleum reserve deployment protocols become critical during extended supply disruptions. The IEA maintains emergency response capabilities designed to coordinate reserve releases among member nations, though the timing and scale of such interventions depend on the severity and expected duration of supply constraints.

Emergency response considerations include:

- Reserve release volumes sufficient to offset supply gaps without creating market oversupply once normal operations resume

- Coordination timing between multiple importing nations to maximise market stabilisation effects

- Commercial inventory incentives to encourage private sector stockpile utilisation before government reserve deployment

- Transport logistics for moving strategic reserves from storage locations to refineries requiring feedstock

Market Pricing Mechanism Evolution During Supply Route Disruptions

Crude oil pricing benchmarks face recalibration pressures when normal supply patterns experience significant disruptions. The Dubai crude benchmark, which serves as a key pricing reference for Asian oil imports, must account for quality and timing adjustments when supply sources shift dramatically.

Quality Assessment Protocol Modifications

Platts, a major price assessment agency, has suspended quality adjustments for Murban crude within the Dubai benchmark during March 2026, indicating that normal pricing mechanisms require modification during supply disruption periods. This suspension reflects the complexity of maintaining accurate price discovery when crude availability and specifications change rapidly.

Pricing mechanism adjustments typically address:

| Assessment Category | Normal Operations | Disruption Period Modifications |

|---|---|---|

| Quality differentials | Based on sulphur content, gravity, and yield characteristics | Simplified assessments due to limited crude variety |

| Loading timing | Flexible scheduling across multiple ports | Concentrated on available port capacity |

| Volume weightings | Distributed across major trade flows | Adjusted for actual available volumes |

| Geographic adjustments | Multiple origin points | Limited to operational export facilities |

Forward Curve Implications for Procurement Planning

Energy procurement strategies must account for both immediate supply constraints and expectations regarding the duration of current disruptions. Forward price curves during supply disruption periods often exhibit elevated volatility and wider bid-ask spreads due to increased uncertainty about future supply availability.

Asian refiners face several forward curve challenges:

- Contango structures may encourage inventory building if storage capacity permits

- Backwardation patterns could signal market expectations of rapid supply normalisation

- Basis risk expansion between different crude grades as availability patterns change

- Time spread volatility reflecting uncertainty about disruption duration

Supply Chain Resilience Enhancement Strategies

The current supply disruption demonstrates both the vulnerabilities and adaptive capabilities inherent in global energy supply chains. Companies with diversified procurement portfolios and flexible logistics arrangements have shown greater operational resilience compared to those dependent on single-source supply strategies.

However, these disruptions also highlight the interconnected nature of modern energy security insights across multiple commodity markets and geographic regions.

Multi-Source Procurement Framework Development

Effective supply diversification strategies require:

- Geographic distribution across multiple producing regions to reduce concentration risk

- Crude quality diversity to maintain refining flexibility under various supply scenarios

- Contract term variations including spot market access, term agreements, and optional volume arrangements

- Transportation route alternatives to avoid single chokepoint dependencies

Sinopec's ability to arrange 24 million barrel loadings from Yanbu suggests that major refiners maintain procurement relationships that can be activated quickly when primary supply routes face constraints. However, the scale of this arrangement also indicates the significant coordination required to implement alternative sourcing strategies.

Technology Integration for Supply Visibility

Advanced supply chain monitoring technologies become increasingly valuable during disruption periods. Real-time shipping tracking, port congestion monitoring, and predictive analytics for route optimisation help companies anticipate and respond to supply chain challenges before they impact operations.

Key technology applications include:

- Satellite-based vessel tracking for monitoring crude oil tanker movements and potential delays

- Port congestion analytics to predict loading schedule impacts and optimise shipping timing

- Weather routing optimisation to minimise transit times whilst avoiding operational risks

- Inventory optimisation algorithms to balance carrying costs against supply security benefits

Contract Flexibility Enhancement Protocols

Traditional term crude purchase agreements often include force majeure provisions that become relevant during geopolitical supply disruptions. However, the practical application of these contractual mechanisms requires careful coordination between buyers and sellers to maintain long-term commercial relationships.

Contract modification considerations encompass:

- Volume flexibility clauses allowing temporary quantity adjustments during supply constraints

- Quality substitution provisions permitting alternative crude grades when preferred specifications are unavailable

- Shipping route alternatives with associated cost adjustments for longer transit times or alternative ports

- Pricing mechanism adjustments to account for supply route changes and associated cost impacts

Energy Transition Acceleration Under Supply Security Pressures

Supply disruptions in traditional energy markets often accelerate consideration of alternative energy sources and enhanced energy security measures. While immediate responses focus on managing current supply constraints, longer-term strategic planning may incorporate lessons learned about supply vulnerability into future energy portfolio decisions.

Furthermore, these disruptions often catalyse interest in renewable energy strategies as part of comprehensive energy security frameworks.

Renewable Energy Investment Decision Frameworks

Energy security considerations potentially influence renewable investment through:

- Supply independence benefits of domestically generated renewable electricity compared to imported fossil fuels

- Price volatility reduction as renewable generation costs become more predictable over project lifetimes

- Infrastructure security advantages of distributed generation compared to centralised fossil fuel logistics

- Strategic reserve implications as battery storage technologies provide alternative emergency energy supplies

However, the timeline for renewable energy deployment typically extends beyond the duration of most fossil fuel supply disruptions, limiting the immediate relevance of clean energy alternatives for addressing current supply constraints.

Hybrid Energy Security Framework Development

Modern energy security strategies increasingly incorporate:

| Energy Source Category | Security Advantages | Implementation Timeline | Supply Chain Dependencies |

|---|---|---|---|

| Strategic petroleum reserves | Immediate availability during disruptions | Existing infrastructure | Crude oil import requirements |

| Natural gas storage | Seasonal demand management | Moderate infrastructure requirements | Pipeline and LNG import dependencies |

| Battery storage systems | Grid stability and backup power | 2-5 year deployment cycles | Critical mineral supply chains |

| Renewable generation | Long-term supply independence | 5-10 year development cycles | Manufacturing and material supply chains |

Critical Mineral Supply Chain Parallels

The current focus on energy supply chain resilience parallels growing attention to critical mineral supply chain security for renewable energy technologies. Lithium, cobalt, rare earth elements, and other materials essential for battery storage and renewable generation equipment face their own geographic concentration risks and potential supply disruptions.

Energy security planning increasingly must account for these interconnected supply chain vulnerabilities across both traditional and renewable energy systems.

The next major ASX story will hit our subscribers first

Regional Cooperation Mechanisms for Energy Security Enhancement

The current supply disruption highlights the importance of coordinated responses between energy importing nations and international organisations. Regional cooperation frameworks provide mechanisms for sharing both emergency supplies and market stabilisation costs during extended disruption periods.

Strategic Reserve Coordination Protocols

International Energy Agency emergency response capabilities include:

- Coordinated reserve releases timed to maximise market impact whilst minimising individual country burden

- Market monitoring systems to track supply gaps and coordinate appropriate response scales

- Information sharing mechanisms to improve supply disruption assessment and response planning

- Commercial sector coordination to leverage private inventory capabilities alongside government reserves

The documentation of over 40 severely damaged energy assets indicates that current disruptions may require sustained rather than temporary response measures, potentially necessitating multiple coordination cycles between IEA member countries.

Alternative Supply Route Development

Regional infrastructure development priorities may include:

- Pipeline capacity expansion to reduce dependence on maritime shipping routes

- Strategic port facility enhancement to improve alternative route throughput capabilities

- Cross-border energy storage coordination to improve collective supply security

- Emergency sharing agreements for refined products and natural gas supplies

Long-term energy security planning requires balancing the costs of redundant infrastructure development against the economic impact of supply disruptions like the current situation affecting Asian refiners.

Investment Strategy Implications for Energy Infrastructure Development

The current supply disruption provides insights into infrastructure investment priorities that balance normal operational efficiency against emergency response capabilities. Capital allocation decisions must weigh the costs of maintaining excess capacity against the potential impact of supply route disruptions.

Port Infrastructure Investment Assessment

Yanbu port's record volume operations during March 2026 demonstrate both the potential and limitations of alternative export infrastructure. The ability to rapidly scale operations suggests that some excess capacity existed, but the concentration of volumes through a single facility creates new operational risks that require additional investment consideration.

Infrastructure investment priorities include:

- Loading terminal capacity expansion to accommodate surge volumes during route disruptions

- Storage facility enhancement to provide buffer capacity for supply timing mismatches

- Security infrastructure development to protect against the types of disruptions that affected SAMREF operations

- Redundant system installation to maintain operations if primary facilities face temporary constraints

Energy Trading and Logistics Technology Investment

Advanced analytics and monitoring systems become increasingly valuable during supply chain disruptions, potentially justifying accelerated investment in:

- Predictive supply chain analytics for anticipating and responding to potential disruptions before they impact operations

- Automated contract management systems for rapidly implementing alternative sourcing arrangements

- Real-time market intelligence platforms for optimising pricing and logistics decisions during volatile periods

- Risk management software integration for coordinating supply, financial, and operational risk exposures

Strategic Partnership Development

The scale of coordination required for arrangements like Sinopec's 24 million barrel Yanbu loadings suggests that strategic partnerships between major energy companies become increasingly important during disruption periods. Investment in relationship development and coordination capabilities may provide competitive advantages during future supply constraints.

Market Psychology and Behavioural Responses During Energy Supply Disruptions

Energy market participants often exhibit behavioural patterns during supply disruptions that can amplify or dampen the actual physical impact of supply constraints. Understanding these psychological factors becomes important for both market participants and policymakers attempting to manage disruption effects.

Inventory Hoarding and Demand Surge Dynamics

Supply constraint announcements typically trigger:

- Anticipatory purchasing by refiners seeking to secure supplies before further constraints develop

- Inventory building beyond normal operational requirements as companies prepare for extended disruptions

- Contract renegotiation urgency as buyers seek to secure alternative supply arrangements

- Price risk management activity through increased hedging and forward purchasing

These behavioural responses can create temporary demand surges that exceed the actual physical supply reduction, amplifying market tightness beyond what supply/demand fundamentals alone would suggest.

Information Processing and Market Reaction Patterns

Market participants must process complex, rapidly evolving information during disruptions:

| Information Type | Market Impact Timeline | Typical Response Pattern |

|---|---|---|

| Supply reduction announcements | Immediate (within hours) | Price volatility increase, volume surge |

| Alternative route capacity assessments | 24-48 hours | Volatility moderation, basis adjustment |

| Disruption duration estimates | Several days | Forward curve reshaping |

| Emergency response coordination | 1-2 weeks | Price stabilisation attempts |

Saudi Aramco's statement regarding commitment to meeting customer expectations whilst adjusting loading schedules demonstrates the importance of clear, timely communication in managing market psychological responses during supply disruptions.

Technical Crude Quality Analysis and Refining Implications

The concentration of Asian imports on Arab Light crude from Yanbu creates specific technical challenges for refining operations that have been optimised around different crude slate assumptions. Understanding these technical implications provides insight into the operational constraints facing Asian energy companies.

Arab Light Crude Specifications and Processing Characteristics

Arab Light crude typically exhibits:

- API gravity: Approximately 32-34 degrees (lighter than many Asian refinery design crudes)

- Sulphur content: Moderate levels requiring standard desulphurisation processing

- Yield patterns: Higher petrol and middle distillate yields compared to heavier crudes

- Processing requirements: Compatible with most refining configurations but may not optimise all unit utilisations

Refining Economics Under Constrained Crude Availability

Asian refiners processing exclusively Arab Light crude face several economic considerations:

- Margin optimisation challenges when product yields don't match optimal market demand patterns

- Processing unit utilisation inefficiencies in facilities designed for heavier crude processing

- Blending constraint costs when limited crude variety restricts optimal feedstock combinations

- Product slate market value variations when yield patterns change from normal operations

The tight supplies to Asian refineries mentioned in industry reports likely reflect not just volume constraints but also the economic impact of operating with limited crude quality flexibility.

Alternative Crude Sourcing Technical Considerations

When seeking alternative suppliers, Asian refiners must evaluate:

- Quality compatibility with existing processing equipment and optimisation strategies

- Blending characteristics when mixing alternative crudes with available Arab Light supplies

- Transportation logistics including tanker size compatibility and port facilities

- Contract terms flexibility for quality specifications and delivery timing

The technical complexity of these evaluations explains why major refiners like Sinopec arrange large-scale supply agreements rather than relying primarily on spot market procurement during disruption periods.

Disclaimer: This analysis is based on publicly available information and industry reports. Energy market conditions can change rapidly, and readers should consult current market data and professional advisors when making investment or operational decisions. Saudi Aramco cuts oil supply to Asia impacts and timeline estimates are subject to significant uncertainty based on geopolitical and operational developments beyond current market visibility.

Looking to capitalise on energy sector volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across the energy and commodities sectors, providing critical market intelligence during periods of supply chain disruption and geopolitical uncertainty. Stay ahead of emerging opportunities in energy-related mining ventures and begin your 14-day free trial today to position yourself strategically in volatile markets.