July 10, 2026

When the Strait Closes: How Energy Supply Shocks Are Redrawing the Architecture of Global Oil Storage

Every few decades, a single geopolitical event forces energy markets to confront an assumption so deeply embedded that it had ceased to feel like an assumption at all. For much of the modern oil era, the implicit belief was that the Strait of Hormuz would remain passable. That belief has now been tested in a way that is reshaping how the world's largest producers think about where they hold their oil, and how quickly they can deliver it.

The disruption of energy flows through the Strait of Hormuz during the Iran conflict did not merely tighten supply for a few weeks. It exposed a structural vulnerability that no amount of spare production capacity could fully offset: the absence of sufficient producer-side storage positioned close to consuming markets. For Saudi Aramco, the world's largest oil exporter, this exposure has triggered a strategic recalibration that goes well beyond routine infrastructure investment.

Saudi Aramco expanding storage capacity worldwide is now a signal that the company's leadership has concluded that pre-positioned inventory in consumer markets is no longer optional. It is, increasingly, a core instrument of market defence.

When big ASX news breaks, our subscribers know first

The Hormuz Disruption as a Structural Turning Point

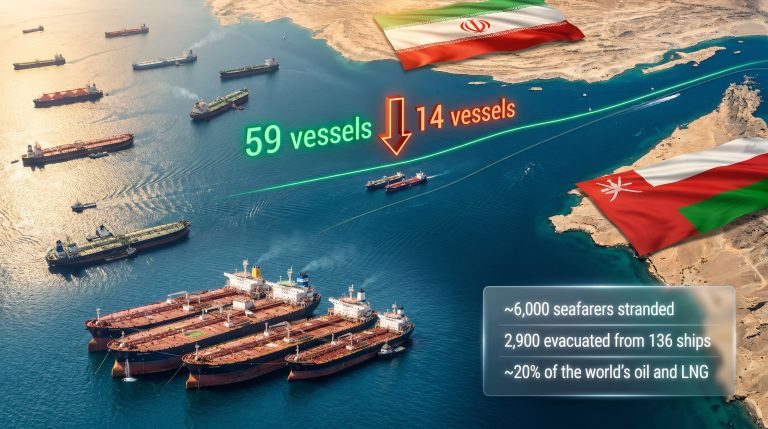

The Strait of Hormuz is a narrow waterway separating the Persian Gulf from the Gulf of Oman. At its narrowest point it spans roughly 33 kilometres, yet approximately 20% of all globally traded oil passes through this single corridor every day. When the Iran conflict disrupted those flows, the ripple effects reached refineries in Japan, South Korea, and Europe within days.

What made this episode qualitatively different from earlier Hormuz tension events was the inadequacy of the response infrastructure. Consumer-nation strategic petroleum reserves (SPRs), which are designed to cushion short-term supply shocks, were drawn upon, but their drawdown rates revealed meaningful limitations. China, for instance, utilised crude stockpiles to partially absorb the shock, though the volumes deployed were modest relative to the scale of the disruption.

Furthermore, the US-China trade war impacts had already introduced additional complexity into global supply chains, making the Hormuz disruption land against a backdrop of heightened logistical fragility. The fundamental gap exposed was not between production capacity and demand, but between where oil was held and where it needed to be.

Critical context: Producer-side inventory, positioned within or adjacent to consumer markets, would have shortened response times considerably.

This is the logic driving Saudi Aramco expanding storage capacity worldwide. Speaking at the FII Priority Europe summit in Rome, Aramco Chairman Yasir Al-Rumayyan, who also serves as governor of the Public Investment Fund (PIF), indicated that the company already holds storage positions in Asia, specifically in South Korea and Japan, and that a serious evaluation of substantially larger storage facilities across multiple global regions is now underway.

Three Pillars of Aramco's Global Storage Architecture

Understanding what a global storage expansion actually entails requires separating three distinct infrastructure categories, each serving a different strategic function.

Crude Oil Buffer Storage: The Market Presence Layer

This is the most visible component of Aramco's global footprint. By holding physical crude inventories in proximity to refining hubs in consumer nations, Aramco can respond to demand spikes or supply disruptions faster than any competitor relying solely on seaborne shipments from the Arabian Peninsula.

The existing footprint already spans several major regions:

| Region | Storage Hub | Known Capacity / Volume | Strategic Purpose |

|---|---|---|---|

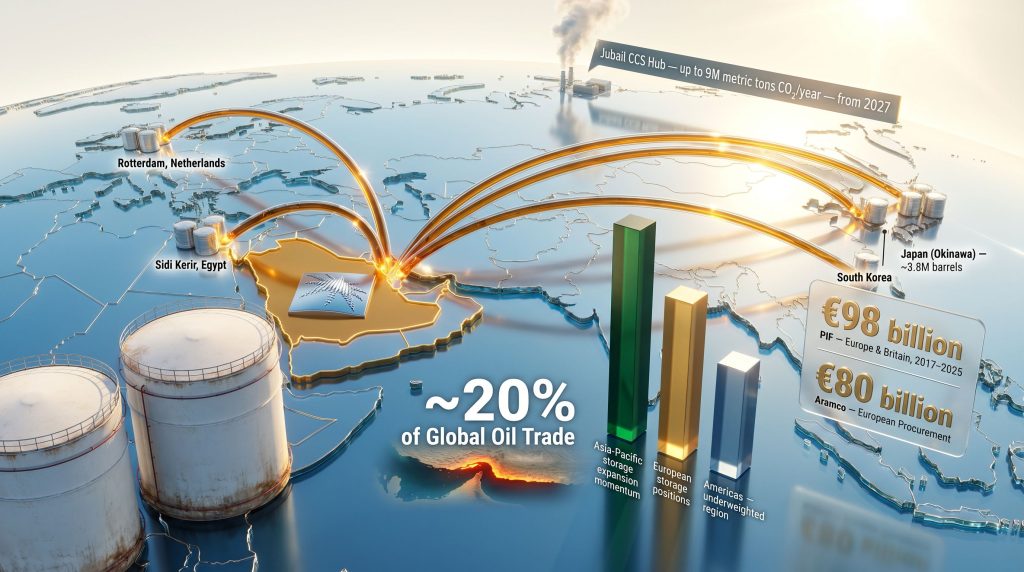

| Japan (Okinawa) | Crude storage facility | ~3.8 million barrels (initial volume) | Asian market access and energy security |

| Netherlands (Rotterdam) | European storage hub | Undisclosed (acquired 2017) | European supply continuity and market share |

| Egypt (Sidi Kerir) | Mediterranean transit hub | Undisclosed | Suez Canal bypass and North Africa coverage |

| South Korea | Asian storage facility | Undisclosed | Northeast Asian demand coverage |

| Saudi Arabia (Domestic) | Multiple tank farms | Integrated with export terminals | Baseline production and export buffer |

The Okinawa facility is particularly instructive as a proof of concept. An initial volume of approximately 3.8 million barrels represents a relatively modest start, but the facility's existence demonstrates that bilateral storage arrangements with consumer-nation governments are achievable and replicable at scale.

Gas System Storage: The Hawiyah Blueprint

Less discussed but equally significant is Aramco's domestic gas storage infrastructure. The Hawiyah Gas Storage facility functions as an underground reservoir capable of reintroducing up to 2 billion standard cubic feet per day back into Saudi Arabia's Master Gas System during periods of peak demand.

This operational model, in which depleted gas fields or purpose-built caverns serve as seasonal and emergency supply buffers, has direct implications for how gas storage partnerships might be structured internationally. The question of whether this domestic blueprint can inform international gas storage partnerships, particularly in markets where Aramco already holds downstream positions, remains an open and underexplored strategic dimension.

Carbon Capture and Storage: The Long-Duration Licence Play

The third pillar is the Jubail carbon capture and storage (CCS) hub, currently targeting a sequestration capacity of up to 9 million metric tons of CO₂ per year, with operations projected from 2027. Notably, Saudi Arabia's CCS market is projected to store 44 million tons by 2035, underscoring the scale of ambition behind this infrastructure investment.

While CCS is technically distinct from crude or gas storage, it is inseparable from Aramco's long-term commercial strategy. European and Asian import markets are progressively tightening carbon intensity requirements for purchased hydrocarbons. For Aramco, CCS investment is not merely an environmental commitment; it is a mechanism for maintaining the social and regulatory licence to operate in markets where emission-linked procurement criteria will increasingly determine supplier selection.

The PIF-Aramco Capital Nexus and European Investment Dynamics

The scale of Saudi capital deployed in Western markets provides important context for understanding how storage expansion ambitions are financed and positioned diplomatically. Between 2017 and 2025, PIF deployed approximately €98 billion (equivalent to roughly $112.86 billion) across European and British markets. Over the same period, Aramco accumulated approximately €80 billion in procurement and investment commitments with European counterparties.

These figures reveal a relationship that goes beyond simple commercial transactions. When sovereign capital and national oil company procurement are deployed at this scale, they create bilateral dependency structures that can support bilateral storage agreements, pipeline access negotiations, and long-term supply contracts simultaneously.

However, Al-Rumayyan's remarks at the FII Priority Europe summit carried a pointed warning directed at European policymakers. Regulatory complexity within European energy markets was identified as a primary factor discouraging new investment and threatening retention of existing positions held by entities including Aramco, SABIC, and PIF itself. The geopolitical trade tensions reshaping global commerce have only amplified this concern, making the regulatory environment an even more critical variable for Gulf capital allocation decisions.

Three Regulatory Scenarios for European Storage Investment

-

Scenario A – Regulatory Accommodation: European authorities streamline energy infrastructure approvals and reduce compliance friction. Aramco scales its Rotterdam and Mediterranean storage positions. European supply resilience strengthens.

-

Scenario B – Regulatory Stagnation: Bureaucratic delays persist without resolution. Aramco prioritises Asia-Pacific storage expansion. Europe faces longer supply lead times during future disruption events.

-

Scenario C – Regulatory Escalation: Carbon border taxes and energy market restrictions intensify. Gulf producers accelerate their pivot toward Asia-Pacific storage networks. A structural European energy vulnerability deepens over time.

The probability weighting across these scenarios matters enormously for European energy security planning, yet it remains highly uncertain. What is not uncertain is that the option value of European storage investment is currently being reassessed by Gulf producers in real time.

Asia-Pacific: The Primary Theatre for New Storage Investment

If European regulatory conditions continue to present friction, the gravitational pull of Asia-Pacific becomes even stronger. Furthermore, Saudi Arabia's global mining push into resource-rich regions signals a broader strategic intent that complements this storage expansion logic. Several structural factors make Asia-Pacific the most logical priority for new storage capacity:

- Asia-Pacific contains the world's fastest-growing oil demand trajectory across the medium term.

- Existing bilateral energy relationships with Japan, South Korea, and China provide institutional frameworks within which storage agreements can be embedded.

- Indian Ocean shipping routes offer more direct connectivity between Saudi export terminals and Asian storage hubs compared to the longer routes required to serve European facilities.

- State energy companies in Japan, South Korea, and increasingly China have demonstrated willingness to co-invest in strategic reserve infrastructure as national energy security assets.

The Japanese model is particularly relevant. The Okinawa facility's structure, where Aramco holds crude inventories that simultaneously serve Aramco's commercial interests and Japan's energy security objectives, created a template in which both parties benefit without either party subordinating its core interests.

How Aramco's Strategy Compares to Other National Oil Companies

Placing this expansion drive in competitive context reveals why it represents a meaningful strategic differentiation rather than routine infrastructure maintenance.

| National Oil Company | Primary Storage Regions | Strategic Emphasis | Notable Differentiator |

|---|---|---|---|

| Saudi Aramco | Asia, Europe, Middle East | Market access and supply resilience | Expanding aggressively post-Hormuz disruption |

| QatarEnergy | Global LNG terminals | LNG liquefaction buffer capacity | Dominates global LNG storage infrastructure |

| Abu Dhabi National Energy Co. (TAQA) | GCC and Europe | Domestic gas balancing | Integrated utility model |

| Kuwait Petroleum Corp. | Regional, limited overseas | Primarily domestic | Refinery-linked storage |

| Rosneft (pre-sanctions) | Europe and Asia | Pipeline-linked tank farms | Now heavily redirected toward Asia |

The contrast with QatarEnergy is instructive. Qatar's storage infrastructure is primarily LNG-focused and tied to liquefaction capacity at the source rather than distributed across consumer markets. Aramco's model, by contrast, aims to embed physical inventory within consumer geographies — a structurally different approach that prioritises delivery speed and market presence over liquefaction scale.

Market dynamics insight: Producers capable of guaranteeing delivery from pre-positioned consumer-market storage, rather than from origin, are positioned to command stronger long-term buyer loyalty in an era where geopolitical supply risk has been permanently repriced upward.

The next major ASX story will hit our subscribers first

Storage as a Market Defence Instrument: The Economics of Pre-Positioned Crude

There is a commercial logic to global storage expansion that operates entirely independently of geopolitical considerations. Pre-positioned crude gives Aramco the ability to respond to Asian or European demand spikes within days rather than the three to six weeks required for a voyage from the Arabian Gulf. This delivery speed advantage translates directly into preferential supply relationships with refiners who value reliability over marginal cost savings.

There is also an OPEC+ dimension that is rarely discussed in this context. When production quotas constrain Saudi output volumes, pre-positioned overseas inventory can be drawn down to maintain market presence in key consumer markets without technically violating production agreement terms. Storage, in this reading, functions as a buffer that decouples market share maintenance from production quota compliance, at least over short to medium timeframes.

Additionally, producers with accessible local inventory can intervene in spot markets during supply disruptions in ways that stabilise prices, reinforcing their reputation as reliable suppliers and deepening long-term buyer relationships that competitors without local inventory cannot easily replicate. In addition, the Saudi critical minerals strategy further illustrates how Riyadh is systematically diversifying its resource leverage well beyond conventional hydrocarbons.

The Long-Term Vision: From Producer to Integrated Energy Logistics Operator

The cumulative effect of Saudi Aramco expanding storage capacity worldwide, if executed across five or more major consumer market geographies simultaneously, would represent a qualitative transformation in the company's market position. Aramco would cease to function purely as an upstream producer delivering crude via seaborne freight and would increasingly resemble an integrated global energy logistics operator with embedded inventory positions across the world's major demand centres.

This transition carries significant implications for competing exporters. Russia, Iraq, the UAE, and non-OPEC producers would face a rival that is not only the lowest-cost producer in the world but also the fastest-delivering supplier in every major market simultaneously. The combination of production cost advantage and logistics proximity advantage is difficult to overcome competitively.

Consequently, the Saudi exploration licences being aggressively pursued in parallel underscore that this is not a company narrowing its focus, but one broadening its global footprint across multiple strategic dimensions simultaneously. For consumer nations, the scenario presents its own complexity. Pre-positioned Aramco crude within national borders simultaneously strengthens energy security and deepens bilateral energy dependency. The political economy of this trade-off is likely to evolve differently across different consumer geographies.

Disclaimer: This article is intended for informational and analytical purposes only. It does not constitute financial advice or an investment recommendation. Projections, scenarios, and forward-looking statements involve inherent uncertainty and should not be relied upon as forecasts of future outcomes. Readers should conduct their own independent research before making investment decisions.

Want To Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex resource data into actionable investment insights the moment they hit the exchange — explore historic discoveries that have generated extraordinary returns or begin your 14-day free trial today to secure a market-leading edge.