May 20, 2026

When Geography Becomes Destiny: The Strait of Hormuz and the Architecture of Global Oil Vulnerability

Every barrel of crude oil that powers Asia's factories, Europe's transport networks, and the Middle East's own domestic economies travels through a handful of maritime corridors so narrow that a single disruption can send shockwaves across the entire global energy system. Of all these chokepoints, none carries more consequence than the Strait of Hormuz. At its narrowest point, the strait measures roughly 33 kilometres across, yet it functions as the circulatory system for a significant share of the world's seaborne crude supply. When that system is compromised, the consequences cascade outward within days, not weeks.

The events of early 2026 have transformed what was once a theoretical risk scenario into a lived reality for oil markets. The Iran conflict has effectively constrained tanker movement through the Gulf corridor, and the downstream data has confirmed what traders feared: Saudi Arabia's March crude exports dropped to the lowest on record, with figures that have no precedent in over two decades of systematic tracking. Understanding oil price geopolitics is therefore essential context for interpreting what these numbers truly represent.

When big ASX news breaks, our subscribers know first

The Geography of Energy Vulnerability: Why No Alternative Can Replace Hormuz

To understand why the Saudi Arabia March crude exports drop to lowest on record carries such systemic weight, it helps to first understand the physical geography that makes Hormuz irreplaceable. The strait sits between the Arabian Peninsula and Iran, serving as the only maritime exit point for crude produced across Saudi Arabia, Iraq, Kuwait, the UAE, and Qatar. Under normal operating conditions, an estimated 20 to 21 million barrels per day of crude and petroleum products transit this corridor, representing roughly one-fifth of total global oil consumption.

No alternative route can absorb Hormuz-scale throughput without significant capacity constraints:

- The Suez Canal handles substantially lower crude volumes and is geographically irrelevant to Gulf export flows

- The Strait of Malacca connects Asian import markets but is an entry point, not an exit route for Gulf producers

- Saudi Arabia's East-West Pipeline (Petroline) provides a partial bypass to the Red Sea terminal at Yanbu, but carries meaningful throughput limitations

- Overland pipeline alternatives across the broader region lack the infrastructure scale to compensate for maritime closure

The fundamental asymmetry is this: it takes decades to build alternative export infrastructure, but only days for conflict to make existing routes unusable. Furthermore, this oil market disruption has exposed just how fragile the assumptions underpinning global energy security have always been.

What the JODI Data Reveals: Parsing a Historic Supply Collapse

Decoding the March 2026 Figures

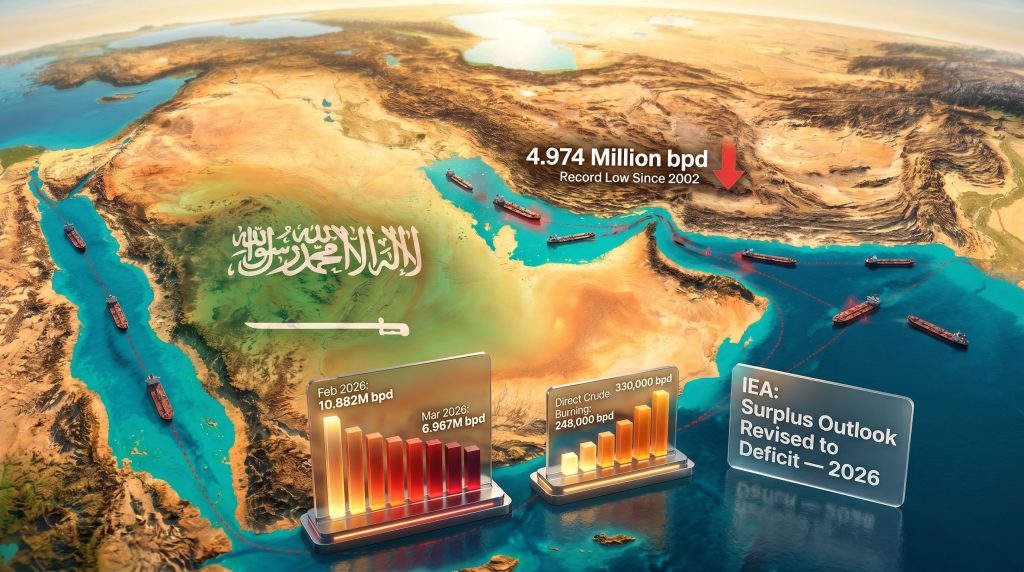

The Joint Organizations Data Initiative, known as JODI, is a transparency mechanism coordinated by international energy bodies including OPEC and the IEA, through which member states self-report monthly production, export, and refinery data. Saudi Arabia's JODI submission for March 2026 produced numbers that have no comparable precedent in the dataset's history, which extends back to January 2002.

| Metric | February 2026 | March 2026 | Change |

|---|---|---|---|

| Saudi crude exports (bpd) | ~7.1 million (Kpler est.) | 4.974 million | ↓ ~30-36% |

| Saudi crude production (bpd) | 10.882 million | 6.967 million | ↓ ~36% |

| Refinery crude throughput (bpd) | 3.012 million | 2.266 million | ↓ 0.746 million |

| Direct crude burning (bpd) | ~248,000 | 330,000 | ↑ 82,000 |

Three features of this data deserve particular analytical attention. First, the simultaneous collapse in both production and exports rules out a deliberate OPEC+ quota adjustment as the primary explanation. When Saudi Arabia voluntarily manages output, production typically declines while export figures adjust more gradually. Here, both numbers fell sharply in tandem, pointing to a structural inability to move barrels rather than a policy decision.

Second, the increase in direct crude burning is a subtle but important signal. When export pathways narrow, Saudi Arabia absorbs more of its own crude for domestic power generation rather than refining and shipping it abroad. The rise from approximately 248,000 bpd to 330,000 bpd represents an 82,000 bpd shift toward internal consumption, which partially masks the full magnitude of the production decline.

Third, the cross-validation between JODI self-reported figures and Kpler tanker-tracking data is instructive. Kpler's satellite and vessel identification data estimated Saudi crude exports at approximately 4.355 million bpd, sitting slightly below the JODI figure of 4.974 million bpd. Rather than creating confusion, this bracketing effect actually narrows the uncertainty range and confirms that the supply reduction is of genuine historic proportions. According to EIA short-term energy outlook projections, sustained disruptions of this magnitude carry significant implications for global inventory levels through the remainder of 2026.

"Critical Insight: The divergence between JODI and Kpler figures likely reflects differences in timing conventions and cargo assignment methodologies, not data error. Both datasets independently confirm a supply reduction unlike anything recorded in the post-2002 era, and investors and analysts should treat the range of 4.3 to 5.0 million bpd as the credible export boundary for March."

How Saudi Arabia's Export Infrastructure Buckled Under Pressure

The Yanbu Rerouting and Its Hard Limits

Under normal operating conditions, Saudi Arabia's crude export architecture relies on two primary terminal systems. Ras Tanura, located on the Gulf coast, handles the dominant share of export volume and is one of the largest crude terminals in the world by throughput capacity. Yanbu, situated on the Red Sea coast and connected to the eastern oilfields via the East-West Pipeline (Petroline), functions as a secondary outlet and strategic redundancy measure.

When Gulf tanker routes became operationally constrained by the conflict, Saudi Aramco redirected export flows toward Yanbu. However, this diversion quickly encountered hard infrastructure limits. Kpler shipping data indicated that Yanbu crude loadings peaked at approximately 4.3 million bpd in late March 2026, before declining to around 3.5 million bpd in the week of April 13, suggesting the Red Sea route was operating at or near its sustainable throughput ceiling.

The Petroline has a reported maximum design capacity of approximately 5 million bpd, but sustained operation at that ceiling creates compounding stresses:

- Pipeline pressure management becomes more technically demanding at maximum throughput

- Port scheduling at Yanbu becomes congested when volumes surge beyond normal operating levels

- Red Sea maritime security considerations add routing complexity for tanker operators

- War-risk insurance repricing for Red Sea transits elevates shipping costs, reducing economic viability for some cargo movements

The net result is that the structural gap between what Yanbu can realistically sustain and what Saudi Arabia normally exports through Gulf terminals directly accounts for the export shortfall captured in the March JODI figures.

The Geopolitical Risk Premium: How Conflict Translates Into Market Pricing

Historical Precedents and the 2026 Context

Oil markets have navigated Gulf disruptions before, but the 2026 situation differs from prior episodes in ways that matter for market interpretation. A comparative framework is useful:

| Event | Period | Estimated Export Impact | Price Response |

|---|---|---|---|

| 2019 Abqaiq-Khurais attacks | September 2019 | ~5.7 million bpd temporarily offline | Brent +15% in 24 hours |

| 2020 Russia-Saudi price war | March-April 2020 | Voluntary production surge | Brent fell below $20/bbl |

| 2022 OPEC+ production cuts | October 2022 onward | ~2 million bpd voluntary reduction | Brent stabilised ~$90-95 |

| 2026 Iran war / Hormuz disruption | March 2026 | Exports at 4.974M bpd, record low since 2002 | Prices sharply higher |

The 2019 Abqaiq-Khurais drone strikes remain the closest modern analogue for infrastructure-driven supply shock, but they were resolved within weeks as Saudi Aramco rapidly restored damaged processing capacity. The 2026 disruption is structurally different because it is not tied to a specific infrastructure failure that can be repaired. It is tied to an ongoing armed conflict with no defined resolution timeline, meaning the market cannot price in a near-term supply recovery with any confidence.

Monitoring Brent and WTI futures has consequently become a critical tool for gauging real-time market sentiment during this period of unprecedented uncertainty. The 1980s Tanker War provides a longer historical reference point, during which tanker insurance costs escalated dramatically and some vessels were requisitioned or flagged under alternative registrations to navigate the risk environment. The key lesson from that episode is that maritime risk escalation into supply shock occurs faster than markets typically anticipate, and the recovery of normal shipping patterns takes longer than initial estimates suggest.

"Market Psychology Note: Experienced commodity traders recognise that the initial price spike on a supply shock often understates the eventual market adjustment. When the disruption is tied to ongoing conflict rather than a fixable infrastructure failure, the sustained supply shortfall tends to produce a second wave of price pressure as inventories deplete and alternative supply sources prove insufficient to fill the gap."

Global Supply Implications: Who Absorbs the Shock

Asia's Refining Sector Faces the Most Direct Exposure

The geography of Saudi crude supply contracts concentrates downstream exposure heavily in Asia. China, India, Japan, and South Korea collectively represent the primary destinations for Saudi long-term supply agreements, and their refining sectors are calibrated around consistent Gulf crude feedstock. A sustained reduction in Saudi export volumes creates cascading pressure at multiple points:

- Inventory drawdown as refiners consume stockpiles rather than reduce throughput immediately

- Spot market competition intensifies as Asian buyers seek West African, US, and Latin American crude to fill the gap

- Refinery margin compression occurs when feedstock premiums rise faster than refined product prices

- Throughput reduction becomes necessary for refiners that cannot economically substitute alternative crudes

The IEA has revised its 2026 global supply outlook from an earlier projection of a market surplus to an anticipated supply deficit, a significant directional shift that reflects the cumulative impact of constrained Gulf exports. Furthermore, OPEC demand revisions have introduced a complicating variable, as the economic drag from elevated fuel prices, reduced industrial activity, and consumer spending compression is already feeding back into demand projections.

This creates an unusual market environment where both supply and demand are being revised simultaneously in directions that produce conflicting price signals for analysts using standard supply-demand modelling frameworks. In addition, OPEC market influence over pricing and output decisions remains a central factor in how the broader market responds to these evolving pressures.

The Freight and Insurance Premium Multiplier

One dimension of the 2026 disruption that receives less attention than crude price movements is the secondary cost transmission through freight and war-risk insurance markets. Saudi Arabia's crude export data from late 2025 illustrates just how dramatically conditions have reversed in a matter of months. Tankers rerouting around the Arabian Peninsula via the Cape of Good Hope add approximately 10 to 14 days to voyage times compared to Hormuz transit routes, meaningfully increasing tonne-mile demand and pushing freight rates higher. War-risk insurance premiums for vessels operating in or near the Gulf have repriced sharply, adding per-barrel cost burdens that ultimately flow through to refiner feedstock economics and retail fuel prices.

The next major ASX story will hit our subscribers first

Short-Term Pressures and Long-Term Structural Shifts

Immediate Market Dynamics (0-6 Months)

- Yanbu continues operating near throughput capacity, limiting Saudi export recovery potential

- IEA member states accelerate strategic petroleum reserve release protocols

- Spot price premiums for non-Middle Eastern crude grades widen as buyers diversify supply sources

- Freight rates remain elevated as tankers reroute via the Cape of Good Hope

- Asian refiners face difficult decisions between inventory drawdown, throughput reduction, and expensive spot purchases

Structural Reconfigurations (6-24 Months)

The longer the Hormuz disruption persists, the more it shifts from a cyclical supply shock into a structural reconfiguration of global crude trade patterns. Several dynamics are already beginning to emerge:

- Investment appetite for alternative supply capacity in US shale, West Africa, and Latin America is rising

- Importing nations are reviewing the adequacy of their strategic petroleum reserve levels and diversification strategies

- Energy security frameworks that previously treated Gulf supply disruption as a tail risk are being repriced toward base-case scenarios

- The economic case for accelerating electrification timelines strengthens when oil import vulnerability is rendered visible at this scale

"Strategic Consideration: If the Hormuz disruption persists through Q2 and Q3 of 2026, the cumulative supply deficit could reach hundreds of millions of barrels, a figure that strategic petroleum reserves cannot sustainably offset. The 2026 episode may ultimately prove to be the event that permanently restructures assumptions about Gulf supply reliability in national energy security planning frameworks globally."

Frequently Asked Questions

What is the lowest level Saudi Arabia's crude exports have reached on record?

According to JODI data covering January 2002 onward, Saudi Arabia's March crude exports dropped to the lowest on record at approximately 4.974 million barrels per day, the lowest monthly figure in the dataset's recorded history.

Why did Saudi Arabia's crude production drop so sharply in March 2026?

The decline from 10.882 million bpd in February to 6.967 million bpd in March is primarily attributed to conflict-driven disruption of Gulf tanker routes, which has severely constrained the ability to move crude through the Strait of Hormuz. This is not a policy-driven OPEC+ output adjustment.

How is Saudi Arabia rerouting crude exports during the disruption?

Export flows have been redirected through the Red Sea terminal at Yanbu, connected to Gulf oilfields via the East-West Pipeline. Kpler data suggests this route was operating near its throughput ceiling in late March 2026, limiting the extent to which it can compensate for Gulf terminal losses.

Which countries face the greatest supply exposure?

Asian importing nations including China, India, Japan, and South Korea carry the heaviest exposure through long-term Saudi supply contracts. European buyers and global spot markets face tighter conditions as competition for non-Gulf crude intensifies.

What does the IEA's revised outlook mean for markets?

The IEA has shifted its 2026 supply forecast from an expected surplus to an anticipated deficit, and has publicly warned that commercial oil inventories are being depleted at a pace that could exhaust buffer stocks within weeks under current conditions.

Key Takeaways

- Saudi Arabia's March 2026 crude exports of 4.974 million bpd represent the lowest monthly reading in over two decades of JODI data

- Production simultaneously fell to 6.967 million bpd, also a record low, down from 10.882 million bpd in February

- The primary driver is conflict-related disruption to Gulf tanker routes, not a deliberate production policy decision

- Yanbu's Red Sea export route is absorbing redirected flows but is operating near its infrastructure capacity ceiling

- The IEA has reversed its 2026 supply outlook from surplus to deficit, signalling systemic market tightening

- Asian refiners carry the most immediate downstream exposure, with global fuel prices rising in response

- The 2026 disruption is structurally distinct from prior Saudi supply shocks due to its ongoing conflict-linked nature and undefined resolution timeline

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, market projections, and scenario analyses discussed herein involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers are encouraged to consult independent financial and energy market advisors. Data sourced from JODI, IEA, Kpler, and Reuters reporting as of May 2026.

Want To Stay Ahead Of The Next Major Commodity Market Shift?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through market complexity to surface actionable opportunities the moment they emerge — explore historic examples of exceptional discovery returns to understand the upside potential, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.