July 17, 2026

The Metal That Makes 5G Work, and Why the West Has Almost None of It

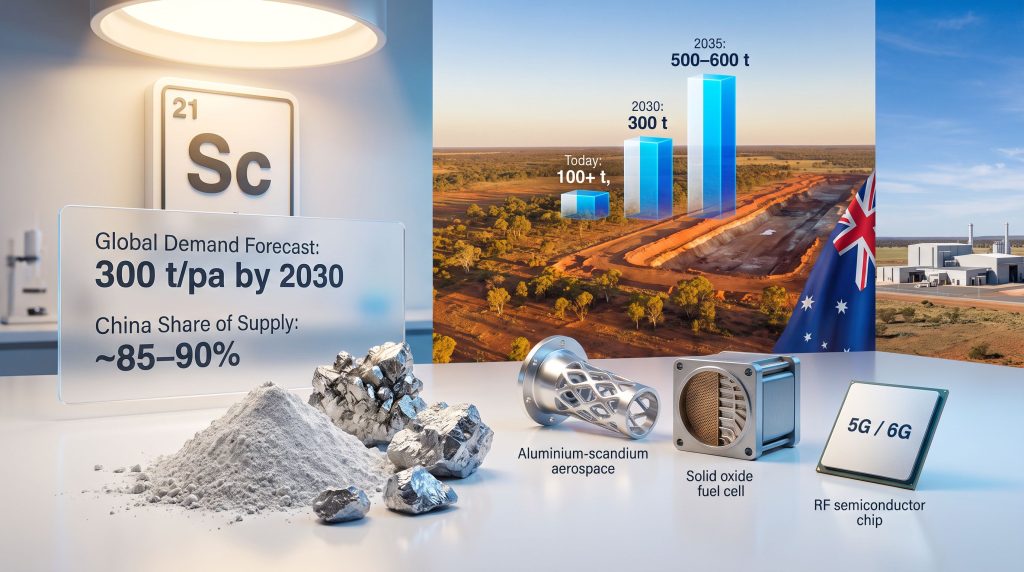

Few technology dependencies are as overlooked, or as consequential, as the Western world's reliance on a single nation for a metal most investors have never heard of. Scandium sits quietly at atomic number 21 on the periodic table, classified as a transition metal, yet it underpins three of the most strategically vital technology sectors of the decade: advanced aerospace alloys, clean energy fuel cells, and 5G and 6G semiconductor chips. The uncomfortable reality is that roughly 85 to 90% of global scandium supply originates from China, predominantly recovered as a trace byproduct of titanium and iron ore processing at concentrations of just 10 to 20 parts per million (ppm). There is currently no operating primary scandium mine anywhere outside China. For investors tracking critical minerals, that fact alone reframes the entire investment thesis around the Sunrise Energy Metals scandium project.

When big ASX news breaks, our subscribers know first

Understanding Scandium: Why Purity Is Less Important Than Partnership

Scandium in its pure metallic form is, paradoxically, almost useless industrially. It is brittle, difficult to work with, and offers few standalone applications. Its extraordinary value emerges only when it is introduced into other materials, either as an alloying agent or as a dopant in semiconductors. This distinction is critical and often misunderstood by generalist investors approaching the critical minerals space.

The three primary demand pillars that define scandium's strategic importance are structurally distinct from one another, which gives the metal an unusually broad and resilient demand base.

Aluminium-Scandium Alloys for Aerospace and Defence

Adding just 0.1 to 0.5% scandium by weight to aluminium produces dramatic improvements in strength, corrosion resistance, weldability, and ductility. These are not marginal gains. The resulting alloys are increasingly specified for component manufacturing in advanced aerospace and defence programs, including drone platforms and high-performance fighter aircraft such as the F-35. As Western defence budgets expand and supply chain localisation becomes a policy priority, aluminium-scandium alloys are moving from optional material upgrade to preferred specification.

Solid Oxide Fuel Cells (SOFCs) and Clean Power Infrastructure

Scandium's largest single commercial market today is solid oxide fuel cells. In this application, scandium functions as a stabilising agent within the electrochemical reaction that converts natural gas into electricity, extending the operational lifespan and efficiency of the fuel cell system. This technology traces its origins to NASA research programmes and has been commercialised most prominently by Bloom Energy, based in California. Importantly, SOFC demand for scandium is growing as AI data centre operators seek distributed, low-emissions power solutions that do not depend on grid availability.

Semiconductor Chips for 5G and 6G Communications

Perhaps the most strategically consequential application is also the most recently developed. The transition from 3G wireless networks to 5G was made possible by scandium doping of aluminium in radio frequency filtering chips. There is no known substitute for scandium in this function. Chip manufacturers producing these components, including major US-based semiconductor fabricators, have acknowledged that if scandium supply fails, the only alternative is reverting to 3G technology. As 6G development accelerates globally, furthermore, this dependency will intensify rather than diminish.

Scandium is one of the rare cases in critical minerals where the outcome of supply failure is binary. Either the technology works or it does not. There is no degraded middle ground, no cost-effective workaround, and no alternative element that can replicate its filtering performance in radio frequency chips.

The Scandium Market by the Numbers: Small, Opaque, and Growing Fast

One of the most striking features of the scandium market is how small it currently is, and how little that smallness reflects its strategic importance. Official USGS data places global scandium oxide demand at 40 to 50 tonnes per annum. However, actual consumption including undocumented use in fuel cells and alloys is estimated by industry participants at closer to 100 tonnes or more per year. The discrepancy arises because scandium is consumed as a component within other products rather than as a standalone traded commodity, making accurate measurement difficult.

| Market Metric | Estimated Figure |

|---|---|

| Official global Sc₂O₃ demand (USGS) | 40 to 50 tonnes per annum |

| Estimated actual consumption | 100+ tonnes per annum |

| Scandium metal demand (semiconductor sector) | ~5 tonnes per annum |

| China's share of global supply | 85 to 90% |

| Operating primary scandium mines outside China | Zero |

| Forecast demand by 2030 | ~300 tonnes per annum |

| Forecast demand by 2035 | 500 to 600 tonnes per annum |

Scandium does not trade on any open commodity exchange. There is no London Metal Exchange listing, no futures market, and no transparent Western pricing benchmark. The only reference index that exists is a Chinese domestic price published by a Chinese metals information service, which industry participants note does not accurately reflect what Western buyers actually pay, or what Western-produced scandium would be worth in a competitive, supply-secure environment. This pricing opacity has historically made project financing challenging, since lenders cannot anchor revenue forecasts to a verifiable market price.

The demand growth projections are compelling but conditional. Reaching 300 tonnes per annum by 2030 and 500 to 600 tonnes per annum by 2035 depends in part on whether a stable, non-Chinese supply source materialises to unlock end-user commitment. This is the classic chicken-and-egg dynamic that has suppressed Western scandium development for over a decade: manufacturers are reluctant to commit to scandium-based designs without supply certainty, while mine developers cannot secure financing without committed offtake agreements. The broader critical minerals demand surge across technology sectors is, however, beginning to shift that calculus in favour of developers with credible projects.

Why China's Export Restrictions Changed Everything

China's imposition of export quota restrictions on scandium in early 2024 transformed what had been a background supply concern into an acute supply chain emergency for Western technology companies. The restrictions tightened access to scandium oxide and, critically, to high-purity scandium metal, which is the form required for semiconductor chip production.

The significance of this cannot be overstated. There is currently no source of high-purity scandium metal outside China. Every radio frequency chip produced using scandium-doped aluminium, by every major US semiconductor company, relies on Chinese supply. Rather than easing these restrictions in response to diplomatic pressure, China has continued to tighten access in strategically sensitive sectors. For Western governments and technology companies, this has elevated scandium from a niche procurement challenge to a national security concern.

The market response has been notable. Chinese producers have opened US-based trading offices to manage direct customer relationships, effectively reinforcing China's intermediary role while simultaneously demonstrating the vulnerability of that arrangement. For a metal where there is no substitute and no alternative production geography, the structural tension between supply concentration and demand criticality is now impossible to ignore. In addition, the growing importance of critical minerals for semiconductors has prompted coordinated responses from Western governments seeking to reduce this exposure.

Inside the Syerston Project: Grade, Scale, and a Structural Cost Advantage

The Syerston scandium project, the centrepiece of the Sunrise Energy Metals scandium project development strategy, is located near Fifield in central-west New South Wales, approximately 200 to 300 kilometres west of Sydney. The region is an established Australian mining jurisdiction, supported by existing infrastructure, an experienced workforce, and proximity to multiple operating mines.

What makes Syerston fundamentally different from every other scandium project globally is its grade. China's primary scandium production comes from processing waste streams at concentrations of 10 to 20 ppm. The Syerston high-grade zone averages 665 ppm scandium, which is approximately 33 to 65 times higher than the concentration at which Chinese producers operate. This grade differential is not merely a geological curiosity. It is the foundation of the project's cost structure and its ability to respond flexibly to changes in demand.

| Resource Parameter | Specification |

|---|---|

| Total resource (measured and indicated) | ~46 million tonnes |

| Full resource average scandium grade | 414 ppm |

| High-grade zone average scandium grade | 665 ppm |

| Total contained scandium metal | ~19,007 tonnes |

| High-grade zone contained scandium | ~1,311 tonnes |

| Drill holes completed | 2,000+ |

| Total assays conducted | 50,000+ |

The mineralisation style is also operationally advantageous. Syerston is a laterite-style deposit, meaning the ore sits from surface to approximately 30 metres depth with no requirement for blasting or hard rock mining. The extraction profile resembles a strip mining operation, which simplifies the development engineering and reduces operating cost complexity. Mining, in fact, represents the least challenging component of the entire project build.

The resource also carries an important strategic footnote. Syerston has long been recognised as one of the largest nickel-cobalt laterite resources in the Western world, and was previously advanced through feasibility and permitting as a nickel-cobalt sulfate operation targeting battery materials. The pivot to scandium as the primary development pathway came after Indonesian nickel supply expansion created significant market oversupply, compressing nickel-cobalt economics. The full deposit contains over 30,000 tonnes of scandium oxide equivalent across the entire resource, providing long-term optionality for future scandium extraction whether as a primary product or as a byproduct if nickel-cobalt markets recover.

Feasibility Economics: The Numbers Behind the Development Case

The updated feasibility study, refined through 2024 and 2025, presents a capital-efficient development case relative to the strategic value of what is being produced.

| Development Parameter | Specification |

|---|---|

| Total development capital | US$120 million |

| Nameplate scandium oxide production | 60 tonnes per annum of 99.9% Sc₂O₃ |

| C1 cash operating cost | US$534/kg Sc₂O₃ |

| Mine life | 32 years |

| Active mining period | 21 years |

| Stockpile processing period | 11 years |

A nameplate capacity of 60 tonnes per annum of scandium oxide may sound modest, but the physical volume of this material is genuinely minuscule. At current production forecasts, the annual output of the entire project would fit comfortably in the corner of an office. The economic significance lies not in the tonnage but in the value per kilogram and the margin structure that a low-cost, high-grade, primary production source can achieve relative to Chinese byproduct producers.

The project timeline is structured around the following key milestones:

| Milestone | Target Timing |

|---|---|

| Final Investment Decision | Q2 2026 |

| Site construction commencement | H2 2026 |

| Commissioning | H1 2028 |

| First commercial production | Mid-2028 |

Construction activity has already commenced, with long-lead capital equipment orders being placed and the owner's team being established. The September 2025 Mineral Resource Estimate update doubled the contained scandium metal compared to prior estimates, significantly strengthening the project's long-term production profile. According to Mining Weekly's coverage of the project, the confirmed US$120 million capital cost represents a well-defined development pathway that reinforces investor confidence.

The next major ASX story will hit our subscribers first

Strategic Partnerships and Financing: De-Risking the Development Path

The Sunrise Energy Metals scandium project has secured two landmark strategic relationships that substantially reduce development risk from an investor's perspective.

Lockheed Martin Offtake Option

Sunrise has executed a five-year option agreement with Lockheed Martin for up to 15 tonnes of scandium oxide per annum, representing approximately 25% of planned annual nameplate production. The agreement remains contingent on binding offtake contracts being finalised, but its existence carries considerable signalling value. A tier-one US defence contractor does not enter option agreements for materials it does not intend to use. The agreement validates both the quality of the product specification and the seriousness of defence sector demand for non-Chinese scandium supply.

US Export-Import Bank Letter of Interest

Sunrise has received a Letter of Interest from the US Export-Import Bank for up to US$67 million in debt financing, covering approximately 50% of total development capital. This is not a guarantee of funding, but it represents a formal expression of financing interest from a US government lending institution. Consequently, it reflects the project's alignment with US critical mineral supply security objectives. Ongoing engagement with North American government financing programmes represents a significant near-term catalyst for the company.

The broader policy context matters here. Both US critical minerals policy and the defence critical materials strategy pursued by Western governments have elevated non-Chinese supply development as a funding priority, creating a favourable institutional environment for projects such as Syerston.

Equity Capital Raised

The company has completed share placements totalling approximately A$105 million, with funds allocated across pre-construction activities, long-lead equipment procurement, and owner's team development.

The combination of a Lockheed Martin partnership, a US EXIM Bank Letter of Interest, and A$105 million in equity raised positions the Syerston project as one of the most structurally de-risked critical mineral developments currently advancing outside China.

Downstream Metallisation: The Semiconductor Sector Opportunity

The base feasibility study covers oxide production at the mine site. However, the semiconductor sector requires something more refined: high-purity scandium metal rather than oxide. Sunrise is actively developing plans for a US-based metallisation facility capable of producing this higher-value product directly for chip manufacturers.

This downstream integration strategy is strategically logical for several reasons. Locating metallisation capacity in the United States strengthens the case for US government financing support, deepens integration with American defence and semiconductor supply chains, and captures a higher margin product from the same ore source. The development of this facility would represent an additional capital commitment beyond the base US$120 million, but the strategic value of being the only non-Chinese source of high-purity scandium metal for the semiconductor industry is difficult to overstate. Furthermore, critical minerals and energy security considerations are increasingly influencing how Western governments prioritise downstream processing investments.

Four Structural Investment Drivers Underpinning the Valuation

The share price trajectory of Sunrise Energy Metals, moving from approximately A$1.00 to A$15.00 over a twelve-month period with market capitalisation reaching approximately A$2.2 billion at peak, reflects the convergence of several structural investment drivers that are rarely found in combination.

-

Binary substitutability risk. Unlike most critical minerals where inferior substitutes exist, scandium presents a true binary outcome in key applications. Supply fails and the technology stops working. No alternative element replicates its radio frequency filtering performance in 5G and 6G chips.

-

Unmatched resource grade. No comparable primary scandium resource exists globally in terms of grade, scale, and mining simplicity. The 33 to 65 times grade advantage over Chinese production sources is a structural cost and responsiveness advantage that cannot be replicated easily.

-

China's export restrictions as a sustained demand catalyst. Rather than easing restrictions to rebuild credibility as a reliable supplier, China has continued to tighten access in strategic sectors. This behavioural pattern has convinced Western governments and technology companies that the supply security problem is not self-correcting.

-

Growing institutional awareness. Scandium's role in AI infrastructure power supply through SOFCs, in defence manufacturing, and in telecommunications is becoming better understood by institutional investors. The convergence of AI power demand, defence spending growth, and 5G to 6G network rollout has elevated scandium from an obscure industrial dopant to a recognised critical technology enabler.

Key Risks Investors Should Monitor

A balanced assessment of the Sunrise Energy Metals scandium project requires clear acknowledgment of the risks that remain between the current development stage and commercial production.

-

Financing completion risk. The Final Investment Decision is contingent on securing full project financing, including the US EXIM Bank facility and any additional debt or equity requirements. The Letter of Interest is not a binding commitment.

-

Offtake crystallisation. The Lockheed Martin agreement is an option, not a binding contract. Conversion to firm offtake is a critical pre-FID milestone.

-

Scandium market development risk. Demand growth projections assume that the availability of stable Western supply will itself unlock additional end-user commitment. If demand growth lags forecasts, project economics may be recalibrated.

-

Pricing opacity. The absence of a transparent Western scandium price benchmark creates modelling uncertainty for project revenue assumptions and lender due diligence.

-

Downstream capital requirements. US metallisation capacity requires additional investment beyond the base feasibility scope, representing a further financing and execution dependency.

-

Geopolitical volatility. While China's export restrictions are currently a tailwind for Western scandium development, any policy reversal, however unlikely given current trends, could alter competitive dynamics.

This article is for informational purposes only and does not constitute financial advice. Forecasts, demand projections, and valuation commentary involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Past share price performance is not indicative of future returns.

Milestones and Catalysts to Watch Through 2028

| Milestone | Expected Timing |

|---|---|

| North American government financing announcements | Near-term (flagged as active) |

| Binding offtake agreement finalisation | Pre-FID |

| Final Investment Decision | Q2 2026 |

| Construction commencement | H2 2026 |

| US metallisation facility development update | 2026 to 2027 |

| Commissioning | H1 2028 |

| First commercial production | Mid-2028 |

The Syerston project is attempting something that has never been achieved before: building the world's first dedicated primary scandium mine. The path from identified resource to operating production facility is long, capital-intensive, and dependent on multiple external factors resolving favourably. What distinguishes this development from historical scandium project failures is the convergence of genuine baseload demand, defence sector validation through the Lockheed Martin relationship, active US government financing interest, and a resource grade that no competing project can match. Whether that convergence is sufficient to carry the project through to first production in mid-2028 will be determined by the financing and offtake milestones that now define the critical path.

Want to Stay Ahead of the Next Major Critical Minerals Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across scandium, rare earths, and over 30 other commodities — turning complex data into actionable investment opportunities before the broader market catches on. Explore how major discoveries have historically generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.