June 7, 2026

Mining industry fundamentals reveal a profound transformation in asset valuations, driven by declining discovery rates and lengthening development timelines. While historical gold project acquisitions traded within predictable enterprise value ranges, current market dynamics reflect genuine resource scarcity rather than speculative excess. This shift fundamentally alters how institutional capital approaches development-stage opportunities and creates new benchmarks for strategic asset evaluation. The emerging scarcity premium in gold acquisition transactions now influences record-high gold prices and establishes unprecedented valuation frameworks.

Understanding the Scarcity Premium Phenomenon in Gold Asset Valuations

Contemporary mining mergers and acquisitions demonstrate a pronounced departure from traditional valuation frameworks. The scarcity premium in gold acquisition transactions now represents a measurable market force, distinguishing current conditions from cyclical price appreciation or speculative bubbles.

Defining Resource Scarcity in Modern Mining M&A

Premium pricing in gold development assets reflects fundamental supply constraints rather than market speculation. Unlike commodity price volatility that affects all market participants equally, genuine scarcity premiums emerge when quality assets become systematically unavailable to potential acquirers.

The evolution from growth-driven to scarcity-driven acquisition strategies marks a structural shift in mining industry dynamics. Historical transaction patterns focused on expanding production capacity during favourable commodity cycles. Current market conditions instead prioritise securing any available quality assets, regardless of premium requirements.

Key characteristics distinguishing scarcity premiums:

- Sustained premium pricing above intrinsic asset valuations

- Multiple bidders competing for limited opportunities

- Transaction completions despite elevated pricing

- Premium persistence across multiple transaction cycles

Quantifying Premium Metrics Across Recent Transactions

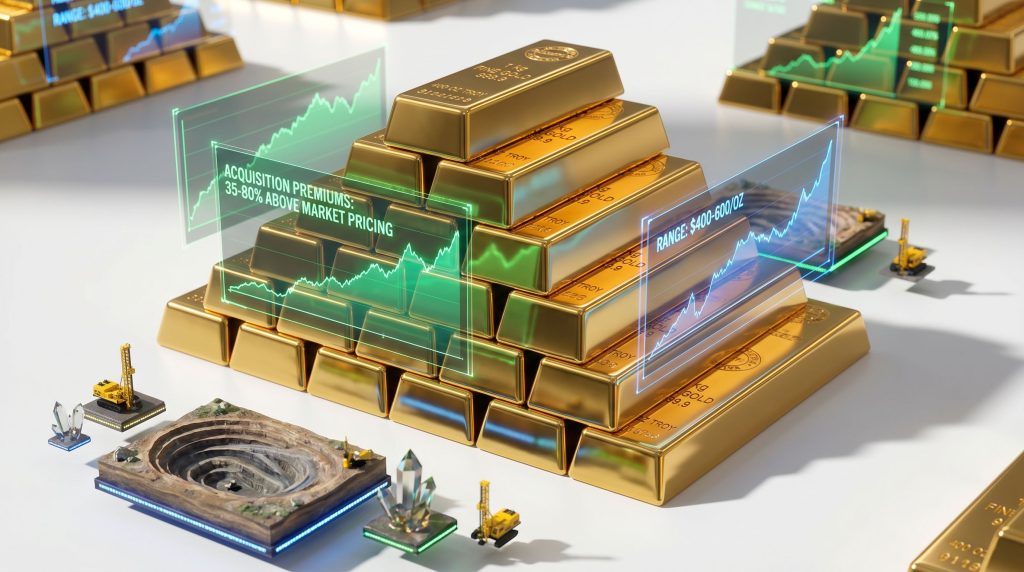

Enterprise value per ounce analysis reveals significant departures from historical benchmarks. Traditional valuations ranged between $100-200 per ounce for development-stage gold resources. Recent transactions establish new benchmarks approaching $500 per ounce, representing increases of 150-250% above historical medians.

Premium percentage calculations demonstrate consistent elevation across competitive acquisition scenarios. Recent major transactions show premiums of 35-80% above market pricing, with some exceptional cases reaching higher multiples when strategic synergies justify additional consideration.

| Transaction Type | Historical Range ($/oz) | Current Range ($/oz) | Premium vs Historical |

|---|---|---|---|

| Development Stage | $100-200 | $400-500 | 150-250% |

| Near-Production | $150-250 | $500-600 | 140-200% |

| Strategic Consolidation | $200-300 | $500+ | 150%+ |

The relationship between resource valuations and gold prices maintains traditional proportions despite absolute value increases. Current $500 per ounce valuations represent approximately 10% of prevailing gold prices, consistent with historical relationships even as absolute values double previous benchmarks.

When big ASX news breaks, our subscribers know first

What Drives Scarcity Value in Gold Development Assets?

Reserve replacement challenges create fundamental pressure driving premium valuations. Major gold producers face declining reserve-to-production ratios as existing mines approach depletion while discovery rates fail to offset consumption.

Reserve Replacement Crisis Among Major Producers

Discovery frequency data indicates systematic reduction in new deposit identification per exploration dollar invested. Technological advances in exploration techniques cannot offset the fundamental reality of resource depletion in easily accessible, high-grade deposits.

Mine life calculations across major producers reveal average operational timelines contracting as accessible reserves become exhausted. This creates urgency for strategic asset acquisition before remaining opportunities disappear from available inventory. Furthermore, the scarcity premium emerges as a direct response to diminishing quality prospects.

Critical factors intensifying replacement pressure:

- Declining success rates in greenfield exploration

- Increasing capital requirements for equivalent resource access

- Geographic concentration risks in politically stable jurisdictions

- Environmental permitting complexities extending development timelines

Quality Asset Characteristics Creating Premium Valuations

Minimum production thresholds effectively exclude smaller projects from institutional consideration. Analysis suggests 250,000+ ounce annual capacity represents the entry point for serious acquisition interest from major producers.

Grade specifications create additional filtering criteria. Open-pit economic requirements typically demand 1.5+ grams per tonne resources to justify infrastructure investment and operational complexity associated with large-scale development.

Build-Ready Asset Criteria:

- Advanced engineering studies completed or substantially progressed

- Environmental baseline studies supporting permit applications

- Infrastructure access or clear pathways to required utilities

- Resource confidence levels supporting investment decisions

- Management teams with development track records

- Financial capacity or clear funding pathways to construction

Infrastructure proximity significantly influences acquisition premiums. Projects requiring extensive new infrastructure face higher capital intensity and longer development timelines, reducing attractiveness compared to assets with existing access to power, water, and transportation networks.

How Market Dynamics Amplify Acquisition Competition?

Balance sheet analysis across major gold producers reveals limited acquisition capacity relative to available opportunities. This mismatch between buyer financial capacity and asset availability intensifies competitive dynamics driving premium valuations.

Competitive Positioning Among Major Acquirers

Major producers with demonstrated acquisition capacity operate under strategic mandates requiring growth through external acquisition rather than organic development alone. Board commitments to shareholders create pressure for deal completion regardless of premium requirements.

| Producer | Estimated Acquisition Capacity | Recent Activity | Strategic Priority |

|---|---|---|---|

| Kinross | $2-3B available | Evaluating targets | Growth mandate |

| Barrick | $3-5B capacity | Selective approach | Quality focus |

| DPM | $1-2B available | Opportunistic | Regional consolidation |

| SSR Mining | $1B+ post-divestiture | Active evaluation | Portfolio optimisation |

Timing Pressures in Current Market Cycle

Construction-ready project scarcity creates artificial urgency amongst potential acquirers. With fewer than five tier-one development opportunities available for near-term construction, competitive dynamics intensify beyond normal market cycles.

Permitting bottlenecks extend development timelines beyond traditional planning horizons. Projects capable of advancing through regulatory approval within current commodity cycles command premium attention compared to earlier-stage opportunities requiring multi-year permitting processes.

Market timing factors driving competition:

- Limited construction-ready inventory available

- Regulatory approval timelines extending beyond historical norms

- Capital market windows favouring development finance during strong gold price environments

- Integration capacity limitations preventing simultaneous multiple acquisitions

Consequently, the current gold price forecast indicates sustained pressure on acquisition valuations.

Case Study Analysis: Recent Premium Acquisition Patterns

The Finland consolidation transaction executed by Agnico Eagle demonstrates sophisticated acquisition structuring addressing complex land position requirements while establishing new valuation benchmarks for quality development assets.

Finland Consolidation Transaction Structure

Agnico's $4 billion CAD strategic consolidation required simultaneous coordination across three separate acquisition agreements. The complexity arose from overlapping land positions where optimal development required unified control across multiple ownership structures.

Transaction components:

- Rupert Resources: $2.9 billion CAD acquisition

- B2Gold Fingold JV: $325 million US for 70% interest

- Aurion Resources: $481 million CAD at $2.60 per share

The transaction structure resolved relationship complexities between prior stakeholders while enabling environmental optimisation through integrated infrastructure planning. Simultaneous acquisition avoided potential hold-out situations that could compromise optimal development approaches.

Valuation methodology established new benchmarks with approximately $500 per ounce resource pricing based on 4.2 million ounce resource definition at 2 grams per tonne. This represents operational synergies justification through infrastructure optimisation benefits unavailable under fragmented ownership.

Strategic Rationale and Premium Justification

The Finland transaction premium reflected strategic value beyond standalone asset consideration. Integrated control enabled optimal mine design addressing environmental requirements while maximising resource recovery across the entire mineral system.

Quality asset characteristics justified premium positioning:

- High-grade open-pit resource supporting 200,000-250,000 ounce annual production

- First-quartile cash cost positioning through grade advantages and operational efficiency

- Advanced permitting status reducing regulatory timeline uncertainty

- Infrastructure placement optimisation achievable only through consolidated ownership

Environmental design optimisation required integration of infrastructure placement across previously separate land packages, achievable only through simultaneous transaction completion addressing all stakeholder positions.

This transaction influenced broader gold market trends and demonstrated gold M&A acceleration.

Which Asset Categories Command the Highest Premiums?

Development-stage projects with advanced technical definition attract the highest premium valuations when combined with permitting progress and resource confidence suitable for major producer requirements.

Development-Stage Project Valuations

Advanced engineering study completion serves as a primary value multiplier distinguishing serious development candidates from earlier-stage exploration assets. Feasibility study completion provides operational confidence supporting premium acquisition pricing.

Environmental permitting progress creates additional premium layers as regulatory approval timelines represent significant project risk factors. Assets with substantial permitting advancement command higher valuations reflecting reduced uncertainty and shortened development timelines.

Resource confidence levels significantly influence valuation premiums:

- Measured resources: Highest confidence supporting construction decisions

- Indicated resources: Moderate confidence requiring additional definition

- Inferred resources: Speculative category receiving limited valuation credit

Geographic Premium Differentials

Jurisdiction stability significantly affects acquisition premiums, with politically stable mining regions commanding substantial value premiums over higher-risk jurisdictions despite potentially superior resource characteristics.

| Jurisdiction | Stability Score | Typical Premium | Infrastructure Costs |

|---|---|---|---|

| Canada | Excellent | 20-30% base | Moderate |

| Australia | Excellent | 15-25% base | Variable |

| Finland | Excellent | 25-35% base | Low |

| Nevada | Good | 15-20% base | Low |

Infrastructure development cost differentials create additional geographic valuation variations. Regions with established mining infrastructure support higher resource valuations through reduced capital intensity requirements for project development.

Investment Implications for Portfolio Construction

Current market dynamics create opportunities for informed capital allocation amongst development-stage opportunities trading below replacement cost valuations established by recent premium transactions.

Identifying Undervalued Development Opportunities

Enterprise value screening methodology identifies potential targets trading significantly below established premium benchmarks while maintaining quality asset characteristics attracting major producer interest.

Effective screening criteria include:

- Resource scale exceeding 2 million ounces minimum threshold

- Grade characteristics supporting first-quartile cost positioning

- Permitting advancement indicating realistic development timelines

- Management track records demonstrating development capability

- Financial capacity or clear funding pathways supporting construction

Technical due diligence frameworks evaluate resource quality through metallurgical characteristics, processing requirements, and infrastructure demands affecting operational economics and capital intensity. In addition, comprehensive market performance analysis helps identify optimal entry points.

Risk Management in Scarcity-Driven Markets

Portfolio concentration limits become critical during periods of elevated acquisition activity when premium valuations create both opportunity and downside risk for speculative positions in development-stage assets.

Recommended portfolio strategies:

- Maximum 15-20% allocation to development-stage speculative positions

- Diversification across multiple jurisdictions reducing regulatory risk concentration

- Liquidity maintenance enabling opportunistic position building during market dislocations

- Stage diversification balancing early exploration with advanced development opportunities

Liquidity considerations in smaller-cap acquisition targets require careful position sizing as trading volumes may inadequately support large position changes during volatile periods surrounding acquisition activity.

The scarcity premium in gold acquisition transactions significantly influences mining equities impact across various market segments.

The next major ASX story will hit our subscribers first

Future Market Structure and Scarcity Evolution

Supply pipeline analysis through 2030 suggests persistent asset scarcity as development project timelines extend while exploration success rates continue declining relative to capital deployed in discovery efforts.

Supply Pipeline Analysis Through 2030

Development project timeline mapping indicates fewer than 10 tier-one assets globally positioned for construction completion before 2030, assuming normal permitting and construction schedules without significant delays.

Projected timeline constraints:

- Environmental permitting: 3-5 years average completion

- Construction phase: 2-3 years for major projects

- Ramp-up to full production: 1-2 years additional timeline

Exploration success rate projections suggest discovery frequency insufficient to replace depleting reserves across major producer portfolios, intensifying competition for available development opportunities regardless of premium pricing.

Strategic Response Options for Market Participants

Joint venture structures provide alternative exposure mechanisms avoiding full acquisition premiums while maintaining strategic participation in quality development projects.

Streaming and royalty models enable asset exposure without operational control requirements, though these structures typically command premium pricing reflecting passive investment characteristics and cash flow predictability.

Alternative strategic approaches:

- Strategic partnerships sharing development risk and capital requirements

- Off-take agreements securing future production without ownership requirements

- Convertible financing providing development capital with equity conversion options

- Royalty acquisition purchasing existing cash flow streams from producing assets

However, the scarcity premium in gold acquisition transactions continues to reshape traditional valuation metrics across all strategic approaches.

Frequently Asked Questions About Gold Acquisition Premiums

Why Are Gold Companies Paying Such High Premiums Now?

Reserve replacement urgency drives premium acceptance as major producers face systematic depletion of existing mine inventories without adequate replacement through organic exploration success. Limited availability of quality assets meeting institutional scale requirements creates competitive dynamics where premium payment becomes necessary for strategic positioning.

Development timeline pressures compound premium justification as projects requiring 5-7 years from acquisition to production must be secured during current market windows, regardless of near-term premium costs relative to anticipated long-term strategic value.

How Do Investors Benefit from Understanding Scarcity Premiums?

Portfolio positioning ahead of acquisition activity enables participation in premium valuations through strategic accumulation of undervalued development opportunities before major producer attention creates competitive bidding scenarios.

Valuation framework application for unlisted or early-stage opportunities provides analytical tools for identifying assets likely to attract future acquisition interest based on established premium benchmarks and quality criteria demonstrated through recent transactions.

What Defines a "Tier-One" Gold Development Asset?

Production scale criteria require annual capacity exceeding 250,000 ounces to attract institutional acquisition interest, with preference for assets supporting 300,000+ ounce annual production over extended mine life.

Grade and jurisdiction standards combine resource grade sufficient for first-quartile cost positioning with political stability supporting long-term operational planning and capital investment security.

Infrastructure and development stage requirements include advanced technical studies, environmental permitting progress, and management capabilities demonstrated through prior development experience or strategic partnerships with established operators.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Gold mining investments involve significant risks including commodity price volatility, operational challenges, and regulatory uncertainties. Premium valuations in acquisition transactions may not reflect sustainable market conditions, and individual investment outcomes may vary significantly from historical transaction patterns discussed. Readers should conduct independent research and consult qualified investment professionals before making investment decisions.

Ready to Identify the Next Major Gold Discovery Before Premium Acquisition?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering subscribers to position themselves ahead of the premium acquisition cycles discussed above. With major producers paying unprecedented valuations for quality development assets, early identification of emerging opportunities through Discovery Alert's discoveries page can provide the market edge needed to capitalise before institutional competition drives premium pricing beyond individual investor reach.