July 9, 2026

The Ocean Floor as a Mineral Frontier: Why Seabed Mining and Critical Mineral Supply Are Converging Now

The story of how industrial civilisations source critical materials has always followed a predictable arc: initial scarcity triggers exploration, exploration reveals new frontiers, and new frontiers eventually become production centres. What took centuries to unfold on land is now playing out across the world's ocean floors within a compressed timeframe, driven by a convergence of demand pressure, technological maturation, and geopolitical urgency that has no modern precedent.

Understanding why seabed mining and critical mineral supply are becoming inseparable topics requires stepping back from individual projects or policy announcements and examining the structural forces reshaping the global minerals economy from the ground up, or more precisely, from the seafloor up.

When big ASX news breaks, our subscribers know first

Why Terrestrial Mining Alone Cannot Meet the Coming Demand Surge

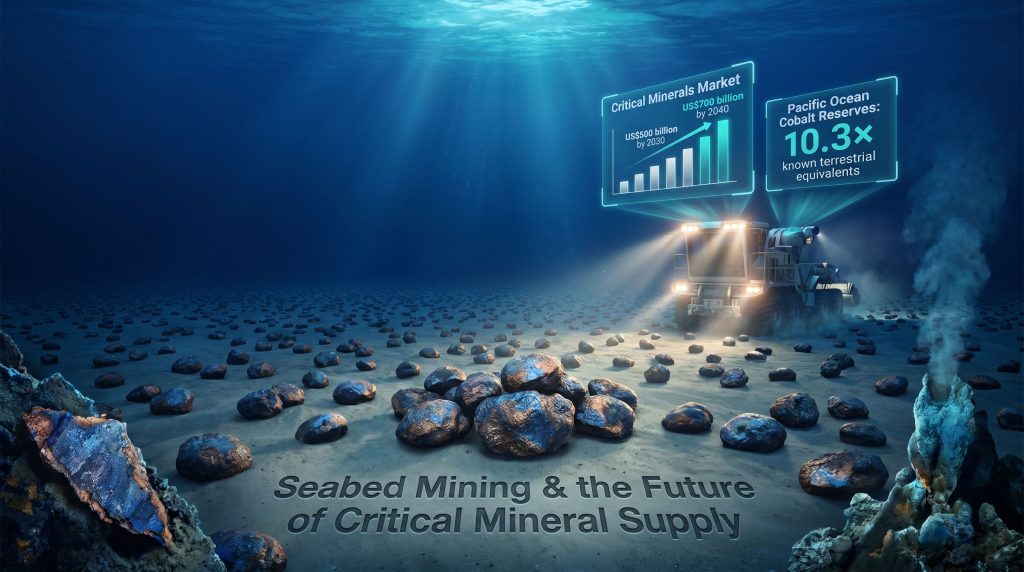

The scale of critical minerals demand projected through 2040 is difficult to overstate. According to the International Energy Agency (IEA), the combined market value of key energy transition minerals, covering cobalt, copper, graphite, lithium, nickel, and rare earth elements, is forecast to surpass US$500 billion by 2030 and climb beyond US$700 billion by 2040, representing a 55% increase from current levels. These projections are grounded in the IEA's CO2 Emission Announced Pledges Scenario, which models mineral requirements aligned with nationally committed climate targets.

To meet this demand trajectory, the IEA estimates that approximately US$590 billion in new capital investment in mining will be required between 2024 and 2040. This is not a small financing gap that marginal production increases can bridge. It represents a structural transformation of the entire global mining industry.

Several intersecting trends are compounding the challenge:

- Declining ore grades: Copper deposits in production today are yielding progressively lower concentrations than those mined a generation ago, meaning more material must be processed to produce the same output

- Extended permitting timelines: New mine development in many jurisdictions takes between 10 and 20 years from discovery to first production, meaning investment decisions made today will not yield supply until the late 2030s at the earliest

- Demand breadth: Clean energy infrastructure accounts for a significant portion of projected demand growth, but data centres, defence manufacturing, advanced electronics, and industrial automation are all competing for the same mineral pool simultaneously

This is the supply-demand arithmetic that is forcing policymakers, investors, and mining operators to look beyond conventional terrestrial resource bases.

The Geographic Concentration Problem: A Structural Vulnerability

Beyond raw volume, the composition of mineral supply chains presents its own category of strategic risk. For copper, lithium, nickel, cobalt, graphite, and rare earth elements, the average market share controlled by the top three producing nations rose from approximately 82% in 2020 to 86% in 2024, according to IEA data. The vast majority of this concentration growth is attributable to just two supply sources: Indonesia for nickel and China across nearly all other listed minerals.

| Dimension | 2020 Baseline | 2024 Position |

|---|---|---|

| Top 3 producers' avg. market share | ~82% | ~86% |

| Primary concentration drivers | Indonesia (nickel), China (others) | Indonesia (nickel), China (others) |

| Strategic risk classification | Elevated | High |

This geographic consolidation creates a systemic fragility that goes beyond price risk. Nations seeking to decarbonise industrial infrastructure or maintain sovereign defence capabilities find themselves dependent on supply chains that run through a very small number of jurisdictions, some of which operate under different strategic priorities. The logic of supply diversification, therefore, is not purely economic. It carries energy security implications that are increasingly shaping mineral policy across the United States, European Union, Japan, and Australia.

What the Seafloor Actually Contains: Deposit Types and Their Strategic Value

The ocean floor hosts mineral wealth across four distinct deposit categories, each with different geological characteristics, extraction profiles, and strategic relevance.

Polymetallic Nodules: The Commercial Priority

Polymetallic nodules are arguably the most strategically significant seabed deposit type for near-term commercial development. These roughly potato-sized formations rest freely on the seafloor surface, requiring no blasting, drilling, or subsurface excavation. They concentrate nickel, cobalt, copper, and manganese within a single ore body, a multi-commodity yield profile that no terrestrial deposit type replicates at equivalent scale.

The Pacific Ocean's nodule reserves are extraordinary by any measure:

- Manganese reserves approximately 5.7 times larger than known terrestrial equivalents

- Nickel reserves approximately 4.1 times larger than land-based known reserves

- Cobalt reserves approximately 10.3 times larger than terrestrial equivalents

The Clarion-Clipperton Zone, a band of Pacific Ocean floor stretching roughly 4.5 million square kilometres between Hawaii and Mexico, hosts some of the densest nodule concentrations known to science. Nodule fields in this zone sit at depths of approximately 4,000 to 6,000 metres, well beyond the reach of conventional marine operations but accessible to purpose-built collection systems now in advanced development.

A critical and underappreciated detail: because the nodules are not physically attached to the seafloor substrate, their collection is mechanically distinct from all forms of conventional mining. The concepts of ore body delineation, blasting, and underground risk management do not apply in the same way. This changes the engineering problem fundamentally.

Other Seabed Deposit Types

Cobalt-rich ferromanganese crusts encrust seamounts and underwater ridges at shallower depths than nodule fields. Their elevated cobalt and rare earth element concentrations make them particularly relevant for nations seeking to reduce dependence on Chinese rare earth supply chains, a priority that has intensified significantly since 2020.

Hydrothermal seafloor massive sulfides form at active and inactive vent systems and carry meaningful concentrations of copper, zinc, and gold. Their relative shallowness offers certain logistical advantages, though their co-location with unique vent ecosystems creates particularly complex environmental considerations.

Rare earth-rich sediment muds represent a longer-term commercial prospect. Japan has pursued pilot extraction programmes targeting these deposits as part of a national resource security framework, recognising that rare earth self-sufficiency would materially reduce strategic dependence on a single supplier.

How Seabed Mining Compares to Conventional Terrestrial Operations

| Factor | Terrestrial Mining | Polymetallic Nodule Collection |

|---|---|---|

| Ore body attachment | Embedded in host rock | Free-resting on seafloor |

| Extraction method | Drilling, blasting, underground or open-cut excavation | Mechanical seafloor collection |

| Subsurface risk | Significant, requires extensive management | Not applicable |

| Commodity yield per operation | Typically single or dual mineral focus | Nickel, cobalt, copper, manganese combined |

| Environmental footprint | Land disturbance, tailings, freshwater use | Marine ecosystem disruption, sediment plumes |

| Permitting timeline | Often 10 to 20+ years | Evolving; frameworks under active development |

The offshore oil and gas industry offers an instructive historical parallel. Deepwater regions such as the Gulf of Mexico and offshore Brazil were once widely considered too technically complex and commercially uncertain to develop at scale. Over time, the convergence of advances in subsurface imaging, drilling technology, and regulatory frameworks transformed these regions into cornerstone components of global energy supply. Seabed mining and critical mineral supply dynamics are exhibiting recognisably similar early-stage characteristics, though with important distinctions.

Unlike hydrocarbon extraction, polymetallic nodules are inert, non-fluid, non-flammable, and non-fugitive. There is no blowout risk, no subsurface pressure management challenge, and no equivalent to the hydrocarbon spill scenario that defines offshore oil risk frameworks. The risk profile is genuinely different, even if the operational complexity and capital requirements share certain similarities.

The Regulatory Landscape: Domestic Frameworks Accelerating Faster Than International Consensus

The governance architecture for seabed mining operates across two distinct jurisdictions: domestic waters governed by individual nations, and international waters governed by the International Seabed Authority (ISA) under the United Nations Convention on the Law of the Sea (UNCLOS). Furthermore, deep-sea mining regulations continue to evolve at different speeds across these two distinct tiers.

The United States Domestic Framework

In April 2025, the United States issued Executive Order 14285, formally designating critical minerals as a national security priority and initiating a coordinated federal effort to develop offshore and deep-sea mineral potential. Following this, the National Oceanic and Atmospheric Administration (NOAA) began advancing a structured licensing and permitting pathway for deep seabed exploration and commercial recovery, actively processing applications through a federal review process.

The United States has not ratified UNCLOS, meaning it operates under its own domestic legal architecture, specifically the Deep Seabed Hard Mineral Resources Act, for activities in international waters. This positions the U.S. to advance seabed mineral development without waiting for ISA regulatory finalisation, a strategic advantage in an environment where international negotiations have moved slowly.

International Governance: The ISA's Unresolved Regulatory Gap

The ISA classifies seabed minerals in international waters as the common heritage of humankind. Despite years of multilateral negotiations, final commercial mining regulations remain unadopted. Talks that broke down in July 2025 resumed in 2026, but a definitive regulatory framework governing commercial extraction in international waters has not yet been established.

This creates a bifurcated development environment. Nations with domestic legislative frameworks, particularly the United States, are advancing faster than those waiting for ISA consensus. China and Russia have embedded seabed mineral access into long-term strategic resource portfolios through ISA exploration contracts, while Norway passed its Seabed Minerals Act in 2019 but adopted a more cautious position in 2024 amid intensifying environmental scrutiny.

A pattern is emerging across the global seabed minerals sector: nations that have invested in domestic regulatory infrastructure are pulling ahead in development pace, while those dependent on ISA finalisation face an indefinite holding pattern.

The next major ASX story will hit our subscribers first

Environmental Risks: The Debate That Will Shape Commercial Viability

No credible analysis of seabed mining and critical mineral supply can sidestep the environmental dimension. The deep-sea mining controversy has grown considerably, with close to 1,000 marine scientists from 38 countries formally calling for a moratorium, precautionary pause, or outright ban, citing the potentially irreversible nature of deep-ocean ecosystem disruption.

The primary scientific concerns centre on four areas:

- Direct habitat loss: Mechanical collection permanently displaces or eliminates seafloor ecosystems, including species found nowhere else on Earth and whose ecological roles are poorly understood

- Sediment plume dispersion: Operations generate suspended sediment clouds capable of travelling hundreds of kilometres, with cascading effects on filter-feeding organisms and broader food webs

- Carbon cycle interference: Deep-sea sediments store significant quantities of sequestered carbon; physical disturbance risks releasing this into the water column and potentially contributing to atmospheric concentrations

- Fisheries impacts: Surface and mid-water species dependent on deep-sea nutrient cycling may be indirectly affected, with consequences that could extend to commercial fishing operations

The proponent case is not without merit, however. Advocates argue that properly regulated nodule collection may carry a lower overall environmental footprint than equivalent terrestrial mining operations, given the absence of deforestation, tailings dam construction, and freshwater contamination. According to research published in Nature, the ecological complexity of deep-sea systems means that meaningful risk assessment requires substantially more baseline data than currently exists. Critics counter that deep-sea ecosystems remain so scientifically undercharacterised that commercial operations should not proceed without that foundation.

This debate will not be resolved quickly, and its resolution will materially shape both the regulatory trajectory and the social licence environment that determines long-term capital access for the sector.

Three Scenarios for Seabed Mineral Development Through 2040

How the seabed mining sector develops over the next 15 years will depend primarily on the pace of regulatory resolution, technological demonstration, and political commitment from major consuming nations. Three distinct pathways are plausible:

Scenario 1: Accelerated Development

The ISA finalises commercial regulations by 2027 to 2028. Parallel domestic licensing in the United States and allied nations advances concurrently. First commercial-scale nodule collection operations reach production in the early 2030s, contributing meaningfully to global nickel and cobalt supply and reducing concentration risk.

Scenario 2: Measured Integration

Regulatory delays persist through 2028 to 2030. Technology demonstration projects validate collection and processing systems but do not reach commercial scale until the mid-2030s. Seabed minerals enter the supply mix as a supplementary rather than primary source, providing diversification without displacing terrestrial production.

Scenario 3: Regulatory Stall

International moratorium pressure intensifies and ISA negotiations remain unresolved beyond 2030. Development becomes fragmented, concentrated in nations with domestic frameworks, and geopolitically contested. The strategic supply diversification potential of seabed minerals is realised only partially and unevenly.

Key Questions From Industry and Investors

What minerals does the seabed actually contain?

The commercially relevant mineral portfolio spans nickel, cobalt, copper, manganese, rare earth elements, zinc, and gold, distributed across polymetallic nodules, cobalt-rich ferromanganese crusts, hydrothermal massive sulfides, and rare earth-rich sediment muds. The multi-mineral yield of nodule deposits is particularly significant from an economic modelling perspective, as it allows operators to spread development costs across multiple commodity revenue streams simultaneously.

Is seabed mining commercially operational today?

As of mid-2026, no commercial-scale seabed mining operations are in production anywhere in the world. The sector remains in advanced exploration and pre-commercial development phases. Regulatory finalisation and full-scale technology demonstration represent the primary milestones separating the current state from commercial production. The NOAA's deep seabed mineral resources programme offers a useful overview of where domestic frameworks currently stand.

How does nodule collection differ from conventional deep-sea drilling?

The distinction is fundamental. Nodule collection is a surface-level mechanical process relative to the seafloor. The nodules sit freely on the ocean floor and are gathered without penetrating the substrate. Deep-sea drilling, by contrast, targets subsurface hydrocarbon reservoirs and requires penetration and pressure management that carries entirely different risk parameters.

What Seabed Mining's Emergence Means for the Critical Mineral Supply Equation

Industry formation in frontier resource sectors historically requires five conditions to align: sustained market demand, supportive commodity pricing, technological readiness, available capital, and regulatory clarity. Seabed mining and critical mineral supply dynamics are currently showing advancement across all five dimensions, though international regulatory finalisation remains the most significant outstanding variable.

It is worth being precise about what seabed mining is and is not. It is not a replacement for terrestrial mineral supply. No credible scenario positions ocean floor extraction as the primary source of global critical mineral production within the foreseeable future. What it represents, however, is an additive supply source with the potential to reduce geographic concentration risk, ease structural supply shortfalls, and give consuming nations greater leverage in a market currently characterised by extraordinary supplier concentration.

The sector's long-term success will hinge not only on geology and engineering, but on the industry's ability to demonstrate environmental responsibility at sufficient rigour to maintain social licence and investor confidence simultaneously. In a minerals economy where the stakes have never been higher, that combination of technical credibility and environmental accountability will determine which frontier becomes the next production centre.

This article is intended for informational purposes only and does not constitute financial or investment advice. Projections referenced from the IEA and other sources are based on modelled scenarios and are subject to revision. Readers should conduct independent research before making any investment decisions related to the seabed mining sector.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across critical minerals and beyond, instantly translating complex data into actionable investment insights for both traders and long-term investors — explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.