June 16, 2026

The Energy Economics Reshaping European Aluminium Production

Across the global metals industry, few structural transitions carry as much economic and environmental significance as the shift from primary to secondary aluminium production. Unlike most industrial pivots driven by short-term market fluctuations, this one is underpinned by a convergence of irreversible forces: tightening carbon regulations, permanently elevated European energy costs, accelerating automotive lightweighting demand, and the progressive attrition of primary smelting infrastructure. Western Europe sits at the epicentre of this transformation, and three countries in particular, Italy, France, and Belgium, illustrate both the scale and the complexity of how secondary aluminium in Italy, France, and Belgium has evolved into a foundational industrial pillar rather than a supplementary materials stream.

When big ASX news breaks, our subscribers know first

Understanding Secondary Aluminium: What It Is and Why It Matters

Primary Versus Secondary: More Than a Semantic Distinction

Primary aluminium is produced through the Bayer and Hall-Héroult processes, extracting aluminium from bauxite ore through refining and electrolytic smelting. It is capital-intensive, energy-hungry, and emissions-heavy. Secondary aluminium, by contrast, originates from the remelting and refining of post-consumer scrap, industrial offcuts, and end-of-life manufactured goods. The two routes produce functionally comparable metal but diverge sharply in their resource footprints.

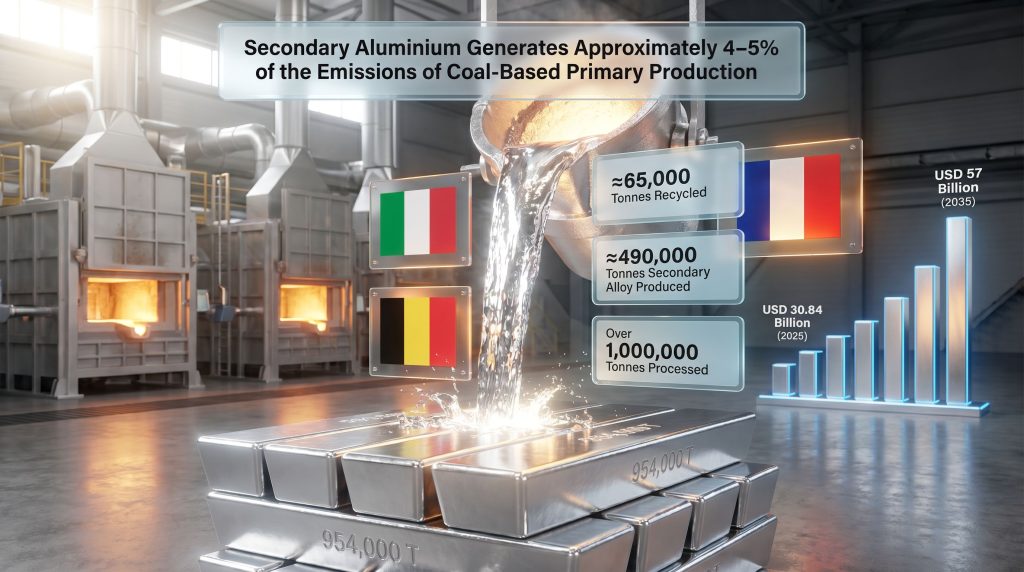

The energy consumption differential is substantial. Secondary aluminium production requires roughly 5% of the energy needed to produce primary aluminium from raw ore. On an emissions basis, secondary aluminium generates approximately 4 to 5% of the greenhouse gas emissions associated with coal-based primary production. This is not a marginal improvement; it is a near-complete decarbonisation of the production step.

This distinction matters enormously for European industrial policy. As the EU Carbon Border Adjustment Mechanism (CBAM) extends its reach and sector-specific decarbonisation targets tighten, the emissions intensity of aluminium sourcing is becoming a direct cost variable for manufacturers across the automotive, packaging, and construction sectors. Furthermore, the decarbonisation benefits of secondary production extend well beyond simple emissions accounting.

The Structural Collapse of European Primary Aluminium Capacity

The decline of European primary aluminium is not a recent phenomenon. The number of active primary smelters across the European Union contracted from 23 facilities in 2002 to just 11 by 2022, with total primary output falling from 2.7 million tonnes to 1.2 million tonnes over the same period. This represents a loss of more than half of the continent's primary production base within two decades.

Several reinforcing factors drove this contraction:

- Structural uncompetitiveness of European electricity tariffs relative to hydropower-advantaged producers in Canada, Norway, and the Middle East

- Rising EU carbon compliance costs eroding already thin smelting margins

- Ageing smelter infrastructure with insufficient investment justification for refurbishment

- Accelerating demand for low-carbon metal creating an economic premium for secondary sources

This erosion of primary capacity did not reduce aluminium demand. Instead, it created a production gap that secondary manufacturers across Italy, France, and Belgium have progressively filled, repositioning recycled aluminium from a cost-saving complement to an essential structural supply source.

How Large Is the Secondary Aluminium Sector Across Italy, France, and Belgium?

The 65 KT, 490 KT, and 1 MT Production Framework

Aggregating across all three national markets provides a revealing picture of the combined regional footprint. Three distinct metrics define the scope of secondary aluminium activity across Italy, France, and Belgium:

| Metric | Annual Volume | Scope |

|---|---|---|

| Aluminium Recycled | ~65,000 tonnes | Post-consumer and industrial scrap recovery |

| Secondary Aluminium Produced | ~490,000 tonnes | Remelted and refined alloy output |

| Total Aluminium Processed | Over 1,000,000 tonnes | All processing operations combined |

These figures highlight an important structural nuance: the volume of aluminium recycled from scrap streams and the volume of secondary aluminium produced are not interchangeable metrics. The 490,000-tonne production figure encompasses the full remelting, alloying, and refining cycle, which draws on both directly recovered post-consumer scrap and other secondary feedstock inputs including industrial process returns and manufacturing offcuts.

The distinction between these layers of production is frequently misunderstood outside the industry. Scrap recovery rates, secondary production volumes, and total processing throughput all measure different points in the same value chain, and conflating them produces misleading assessments of a country's actual recycling performance.

Global Context: Where Does This Region Fit?

Globally, secondary aluminium accounted for approximately 35% of total aluminium production in 2025. The global aluminium recycling market reached an estimated 39.35 million tonnes in 2025, with projections placing total recycled aluminium output at 41.14 million tonnes in 2026. The combined output of Italy, France, and Belgium represents a meaningful share of European production within this global recycling hierarchy, particularly given the region's advanced industrial base and proximity to high-value end-use markets.

Europe as a whole accounts for secondary aluminium production exceeding 60% of its total aluminium supply, a proportion that reflects both primary smelter attrition and deliberate industrial policy prioritising circular material flows. According to European Aluminium, the industry's shift toward secondary production is one of the defining structural changes reshaping the continent's metals economy.

Italy: The Continent's Undisputed Secondary Aluminium Leader

Scale, Geography, and Industrial Concentration

Italy holds the position of Europe's leading recycled aluminium producer, with approximately 954,000 tonnes of secondary aluminium produced in 2021. This is not the output of a single major facility but rather the cumulative result of a dense industrial ecosystem concentrated primarily in the northern manufacturing belt, spanning Lombardy, Piedmont, and the Veneto.

Northern Italy's industrial geography is uniquely suited to secondary aluminium production. Proximity to automotive tier-one suppliers, packaging converters, and die-casting manufacturers creates tight closed-loop scrap flows. Established collection and sorting infrastructure developed over decades further lowers the effective cost of securing quality feedstock. In addition, aluminium recycling investment into joint ventures is reinforcing the sector's long-term viability.

Key Italian Producers and Their Capacities

| Producer | Location | Estimated Annual Capacity |

|---|---|---|

| Raffmetal SpA | Casto | 300,000 tonnes |

| STEMIN SpA | Bergamo | 70,000 tonnes |

| Novelis S.p.A. | Borgofranco | 70,000 tonnes |

| Indinvest LT | Cisterna di Latina | 60,000 tonnes |

Beyond this core group, Italy's secondary aluminium cluster includes additional operators such as Abruzzo Laminazione Alluminio, Ocma, and Hydro Alluminio, reinforcing the distributed, network-like character of the national sector. Raffmetal's 300,000-tonne capacity is particularly notable, representing the single largest secondary aluminium remelting operation in Europe and anchoring Italy's dominant continental position.

"Italy's secondary aluminium dominance is structural rather than coincidental. The combination of a large domestic manufacturing base, mature scrap logistics networks, and competitive remelting operations has created a self-reinforcing industrial ecosystem that is extremely difficult for other markets to replicate quickly."

The Competitive Drivers Behind Italy's Advantage

Several factors underpin Italy's sustained leadership in secondary aluminium production:

- End-use demand proximity: Italy's automotive components sector and packaging industry generate large, predictable scrap volumes that feed directly back into remelters

- Scrap infrastructure maturity: Decades of industrial scrap trading have produced a well-developed collection, sorting, and logistics network across the north

- Energy cost pressure: Italy's relatively high industrial electricity prices have made the energy economics of secondary production, requiring far less power than primary smelting, especially compelling

- Alloy expertise: Italian remelters have developed significant technical capability in producing specific alloy grades for die-casting and sheet applications, enabling higher-value product positioning

France: Recycling Intensity as a Competitive Identity

The 60% Benchmark and What It Reveals

Approximately 60% of aluminium produced annually in France originates from recycling operations. This proportion is particularly striking given that France operates only two active primary aluminium smelting sites, making it structurally dependent on secondary supply to meet domestic industrial demand.

France's recycling intensity reflects both industrial economics and deliberate policy orientation. EU decarbonisation targets, recycled content mandates filtering through automotive and construction procurement chains, and France's own carbon reduction commitments have collectively created a policy environment favouring secondary production investment. Consequently, renewable energy solutions are also being integrated into French remelting operations to reduce residual carbon exposure further.

Major French Secondary Aluminium Operators

| Producer | Location | Estimated Annual Capacity |

|---|---|---|

| Regeal Affimet | Compiègne | 70,000 tonnes |

| Loiret Affinage | Fontenay-sur-Loing | 20,000 tonnes |

| Manzoni-Bouchot (MBF Aluminium) | St. Claude | 15,000 tonnes |

| Affinage Recuperation Negoce SA (ARN) | Neuilly St. Front | 7,000 tonnes |

TRIMET's French operations represent a notable example of integrated primary-to-secondary business model evolution, with the company expanding its recycled aluminium alloy production capacity as part of a broader strategic repositioning toward lower-carbon output. This type of operator-level transition is becoming increasingly common as European aluminium producers align capital allocation with circular economy priorities.

France also functions as a net processor of aluminium scrap imported from neighbouring markets, including feedstock originating in Germany, the Benelux region, and the UK, reinforcing its role as a regional hub within the broader European circular aluminium economy.

Belgium: Strategic Node Within a Pan-European Value Chain

A Different Kind of Aluminium Geography

Belgium's role within the secondary aluminium landscape cannot be assessed using the same metrics applied to Italy or France. Rather than operating as a major standalone secondary producer, Belgium functions as an embedded participant in a pan-European aluminium value chain that spans over 600 plants across 30 European countries.

Belgium's strategic value lies in its logistics infrastructure, trade facilitation capacity, and manufacturing integration within the Northwest European industrial corridor connecting Antwerp, Brussels, and the Rhine-Ruhr region. Aluminium scrap and semi-finished secondary products move through Belgian ports and processing nodes as part of a regional material flow that does not align neatly with national production accounting.

"The absence of publicly disclosed Belgian-specific secondary aluminium production volumes does not indicate a minor sector. It more likely reflects how multinational operators consolidate reporting across Benelux operations as a single regional unit, obscuring the Belgian contribution within aggregate figures."

What the Data Gap Signals to Industry Observers

The opacity of Belgian secondary aluminium data carries its own analytical value. It suggests that:

- Major operators in Belgium report production at a regional or group level rather than by national jurisdiction

- Belgium's secondary aluminium activity is likely captured within the consolidated reporting of companies headquartered in Germany, France, or the Netherlands

- Granular national data for Belgium represents a genuine research gap, and any analysis drawing on publicly available sources will structurally undercount Belgian contributions to regional secondary production

The next major ASX story will hit our subscribers first

Comparing the Three Markets: A Structured Overview

| Dimension | Italy | France | Belgium |

|---|---|---|---|

| Secondary Production Volume | ~954,000 tonnes (2021) | Not fully disclosed | Not publicly quantified |

| Recycling Share of National Output | High | ~60% | Embedded in EU aggregate |

| Primary Smelter Presence | Minimal | Two active sites | Limited |

| Key Industrial Clusters | Northern Italy | Île-de-France, Loire Valley | Brussels-Antwerp corridor |

| Largest Operator by Capacity | Raffmetal SpA (300,000 t) | Regeal Affimet (70,000 t) | Not identified |

| End-Use Demand Drivers | Automotive, packaging | Automotive, construction | Logistics, trade, manufacturing |

The Demand Forces Reshaping Secondary Aluminium Across Western Europe

Energy Economics: The Primary Commercial Driver

The economics of secondary aluminium production rest on a single undeniable advantage: energy consumption per tonne is roughly 95% lower than primary smelting. In a European energy landscape permanently altered by post-2021 price dislocations, this advantage is not cyclical but structural. Every incremental increase in industrial electricity costs widens the economic moat surrounding secondary aluminium producers relative to their primary counterparts.

This dynamic is particularly acute for aluminium because primary smelting is among the most electricity-intensive industrial processes in existence, consuming approximately 14 to 15 kilowatt-hours per kilogram of metal produced. Secondary remelting, by comparison, requires roughly 0.7 kilowatt-hours per kilogram, representing an order-of-magnitude difference in power exposure.

CBAM, Decarbonisation Mandates, and Supply Chain Transformation

The EU Carbon Border Adjustment Mechanism is beginning to reshape aluminium sourcing decisions across European manufacturing. By placing a carbon cost on imported aluminium that reflects the emissions intensity of its production process, CBAM structurally advantages domestically recycled metal over primary imports from coal-powered smelters in China, India, and the Gulf region.

Simultaneously, automotive original equipment manufacturers are embedding minimum recycled content requirements into their supply chain specifications, driven by both regulatory compliance pressures and corporate sustainability commitments. This creates a direct procurement channel favouring secondary aluminium producers in Italy and France who can demonstrate certified recycled content and low-carbon credentials. Furthermore, green metals pricing dynamics are increasingly influencing how secondary aluminium is valued relative to primary metal across European procurement frameworks.

Market Growth Trajectory: European Aluminium to USD 57 Billion by 2035

The European aluminium market is projected to expand from USD 30.84 billion in 2025 to USD 57 billion by 2035, representing compound growth driven primarily by three demand vectors:

- Automotive lightweighting: Increasing aluminium content per vehicle across electric vehicle platforms, where battery efficiency directly benefits from reduced vehicle mass

- Renewable energy infrastructure: Solar panel mounting systems, wind turbine components, and electrical transmission infrastructure all rely heavily on aluminium

- Sustainable packaging: Brand owner commitments to recycled content and aluminium's infinite recyclability are sustaining packaging sector demand growth

Given the structural constraint on primary capacity expansion across Europe, secondary aluminium is positioned to capture a disproportionate share of this market growth.

Challenges Confronting Secondary Aluminium Producers

Alloy Integrity Across Recycling Cycles

One of the least-discussed technical challenges in secondary aluminium production is the progressive degradation of alloy purity through repeated recycling cycles. As aluminium passes through multiple end-of-life and remelting stages, contaminating elements including iron, copper, silicon, and magnesium accumulate in ways that can limit the application range of the recycled output.

This phenomenon, sometimes referred to as downcycling, means that post-consumer aluminium scrap from mixed sources cannot always substitute directly for primary metal in high-specification applications without additional processing. Advanced sensor-based sorting technologies and AI-assisted scrap classification systems are being deployed to address this, improving the ability to segregate alloy-specific scrap streams before remelting and thereby preserving metal quality through more cycles.

Scrap Competition and Cross-Border Export Pressure

European secondary producers face mounting competition for quality scrap feedstock. The global market for aluminium scrap is not contained within EU borders; significant volumes flow to non-EU processors in Turkey, Southeast Asia, and elsewhere, tightening domestic supply. This export pressure is particularly acute for high-grade automotive and aerospace scrap, which commands premiums that non-EU buyers are willing to pay.

Regulatory efforts to restrict scrap exports from the EU are ongoing, but enforcement complexity and trade agreement constraints limit the speed and comprehensiveness of any such interventions. For Italian and French secondary producers, feedstock security is becoming as strategically important as production efficiency. Research published through ResearchGate on secondary aluminium supply economics further underscores how feedstock availability and pricing dynamics fundamentally shape the sector's competitiveness.

Capital Investment and Workforce Requirements

Modern secondary aluminium facilities require continuous capital investment to maintain furnace efficiency, meet evolving emissions standards, and upgrade to cleaner remelting technologies. Skilled operational and metallurgical workforce availability is also a constraint, particularly as the industry competes for technical talent with other advanced manufacturing sectors.

Frequently Asked Questions: Secondary Aluminium in Italy, France, and Belgium

What is secondary aluminium and how is it different from primary aluminium?

Secondary aluminium is produced by remelting and refining scrap metal from post-consumer or industrial sources, rather than extracting aluminium from bauxite ore through the energy-intensive electrolytic smelting process used in primary production. Secondary production uses approximately 5% of the energy required for primary smelting.

How much secondary aluminium does Italy produce annually?

Italy is Europe's leading recycled aluminium producer, with approximately 954,000 tonnes of secondary aluminium recorded in 2021, driven by a distributed network of remelters and refiners concentrated in the northern industrial regions.

What percentage of France's aluminium production comes from recycling?

Approximately 60% of aluminium produced in France each year originates from recycling operations, reflecting the country's minimal primary smelting base of only two active sites and its strong policy orientation toward circular material flows.

Why is Belgium's secondary aluminium sector difficult to quantify?

Belgium's secondary aluminium activity is embedded within multinational operator reporting structures that aggregate Benelux-wide production rather than disclosing country-level volumes, creating a data gap that is structural rather than indicative of sector size.

How does secondary aluminium support Europe's decarbonisation goals?

Secondary aluminium generates approximately 4 to 5% of the greenhouse gas emissions produced by coal-based primary aluminium manufacturing, making it one of the highest-impact decarbonisation levers available to European industry within the metals supply chain.

What is driving growth in the European aluminium recycling market?

Four primary catalysts are accelerating growth: rising energy costs that widen the economic advantage of secondary production, CBAM increasing the cost competitiveness of domestically recycled metal over imported primary aluminium, automotive lightweighting demand requiring certified low-carbon content, and EU circular economy policy mandating higher recycled material usage across key industrial sectors.

The Strategic Outlook: Secondary Aluminium as Europe's Default Production Route

Near-Term Priorities: Capacity and Feedstock Security

The immediate investment priorities for Italian and French secondary producers centre on two parallel challenges: expanding remelting capacity to meet growing demand and securing reliable, high-quality scrap feedstock as competition intensifies. Long-term supply agreements with automotive manufacturers, packaging converters, and municipal collection systems are becoming increasingly central to strategic planning. The broader significance of secondary aluminium in Italy, France, and Belgium to regional industrial resilience cannot be overstated in this context.

Medium-Term Value Chain Repositioning

Beyond volume growth, the more significant medium-term shift is the industry's movement toward producing higher-specification secondary alloys targeting automotive structural components and aerospace applications. These higher-value grades command significant price premiums over standard die-casting alloys and require more sophisticated metallurgical control, sorting infrastructure, and quality certification capabilities. Italian and French producers investing in these capabilities are effectively repositioning from commodity remelters to value-added materials suppliers.

The 2035 Scenario: Secondary as the European Structural Default

A scenario in which secondary aluminium accounts for 70 to 75% of total European aluminium production by 2035 is plausible if three conditions converge: continued primary smelter attrition without offsetting new primary investment, progressive tightening of CBAM and recycled content mandates across key end-use sectors, and sufficient capital investment in advanced sorting and remelting infrastructure to handle growing scrap volumes without quality loss.

This scenario is not guaranteed. It requires both regulatory consistency from EU policymakers and sustained private investment across the secondary production ecosystem. However, the directional trajectory is clear, and the structural logic is compelling.

"Across Italy, France, and Belgium, secondary aluminium is no longer competing with primary production for market share. In a European context defined by primary smelter closure, carbon pricing, and energy cost permanence, secondary aluminium has effectively become the default industrial production route. The question for the next decade is not whether secondary will dominate, but how quickly the infrastructure, feedstock systems, and alloy capabilities can scale to meet the demand that primary aluminium can no longer serve."

Want to Identify the Next Major Mineral Discovery Before the Market Does?

While Europe's industrial sectors race to secure sustainable material supply chains, savvy investors are positioning themselves ahead of the next wave of significant ASX mineral discoveries — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment those discoveries are announced. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to gain an immediate market-leading edge.