May 21, 2026

When Geopolitics Overrides Supply Chain Logic: The Cuba Nickel Dilemma

The global race to secure critical minerals energy security has produced a growing catalogue of policy contradictions. Western governments simultaneously champion supply diversification away from Chinese-controlled sources while deploying the very sanctions instruments that eliminate alternative producers from the accessible market. Nowhere is this tension more visible right now than in the Caribbean, where a decades-old Canadian mining operation has been caught between two competing imperatives: Washington's intensifying pressure campaign against Havana, and the urgent need for non-Chinese cobalt and nickel flowing into electric vehicle battery supply chains.

The Sherritt Cuba sanctions suspension is not simply a corporate distress story. It is a stress test of how far US executive authority can reach into foreign mining operations, and what happens to critical mineral supply when it does.

When big ASX news breaks, our subscribers know first

The Mechanics of Extended Sanctions Jurisdiction

Understanding why the Sherritt Cuba sanctions suspension has caused such severe disruption requires stepping back from the headlines and examining the architecture of US sanctions law itself. The United States has long maintained the legal position that its sanctions regime can apply extraterritorially, meaning that foreign companies operating in designated jurisdictions can face consequences even though they have no US nexus of their own.

The foundational layer for Cuba specifically is the Helms-Burton Act, codified in the 1990s, which established penalties for foreign entities deemed to be "trafficking" in assets expropriated from US persons following the Cuban revolution. This legislation was not merely symbolic. Former Sherritt CEO Ian Delaney and other executives were barred from entering the United States as a direct consequence of the company's Cuban operations, a personal legal liability that most investors in the company during its commodity boom years chose to ignore.

The May 1, 2026 executive order signed by President Donald Trump represented a structural escalation beyond Helms-Burton. Rather than targeting specific expropriated assets, the new order extended US sanctions jurisdiction to cover foreign actors operating across Cuba's metals and mining, energy, defence, financial services, and security sectors simultaneously. This is a meaningfully different legal instrument. It does not require a connection to historical expropriation claims. It designates entire sector categories as sanctionable, which means any foreign company actively operating in Cuban mining becomes a potential target regardless of how its assets were originally acquired.

Secondary Sanctions: The Banking Contagion Effect

Perhaps the most operationally damaging dimension of the sanctions framework is not the direct designation itself, but what follows in the financial system. When the US Treasury's Office of Foreign Assets Control or the State Department designates an entity, financial institutions worldwide face a difficult calculation: continue transacting with the designated party and risk losing access to US correspondent banking infrastructure, or withdraw services preemptively to avoid that risk.

This dynamic creates what practitioners in the sanctions compliance field call a "chilling effect." Banks, insurers, trade finance providers, and logistics counterparties often withdraw well before any formal enforcement action materialises. For a mining company, this can be more immediately damaging than the designation itself. Equipment imports, fuel purchases, commodity sales, and debt servicing all depend on financial intermediaries willing to process transactions.

Sherritt's own disclosures acknowledged this vulnerability, noting that financial and other providers may find themselves unable or unwilling to continue supporting the company's operations or broader business activities. This is not speculative language inserted for legal caution. It reflects the lived experience of sanctioned entities across multiple jurisdictions over the past two decades.

A Regulatory Timeline: From Venezuela Oil Shock to Sanctions Designation

The path to the Sherritt Cuba sanctions suspension actually began months before the May executive order, rooted in a cascading series of geopolitical events that compressed an already fragile operational position.

| Date | Event | Regulatory Significance |

|---|---|---|

| January 2026 | Venezuelan President Nicolás Maduro captured | Triggered accelerated US pressure on Venezuela-Cuba energy flows |

| February 2026 | Sherritt partially suspends Cuban operations | Venezuelan oil shipments to Cuba halted following US pressure; Moa faces fuel supply risk |

| May 1, 2026 | Trump executive order signed | Extended US sanctions to foreign actors in Cuba's mining, energy, defence, and financial sectors |

| May 7, 2026 | Sherritt suspends direct Cuban JV participation | Canadian employees repatriated; shares fall approximately 30% in a single session |

| May 7, 2026 | Three board members resign | Brian Imrie, Richard Moat, and Brett Richards depart |

| May 8, 2026 | Secretary of State Marco Rubio designates Sherritt | GAESA and Moa Nickel S.A. also sanctioned; secondary banking restrictions activated |

| Mid-May 2026 | Dissolution decision reversed | General Nickel Company S.A. dissolution abandoned; operational suspension maintained |

| Mid-June 2026 | Projected feedstock depletion | Fort Saskatchewan, Alberta refinery expected to exhaust Cuban nickel and cobalt supply |

What this timeline reveals is that the February partial suspension was an early warning sign that most market participants underweighted. The Venezuela-Cuba energy nexus had already created an operational vulnerability at the Moa joint venture months before the formal designation. Trump subsequently signed a separate executive order imposing tariffs on any country that sells or provides oil to Cuba, which severed the island from its primary fuel supplier. By the time the May 1 order was signed, Sherritt's Cuban operations were already running on diminished capacity and borrowed time.

The "Reversal Without Resumption" Paradox

One of the more technically complex aspects of the Sherritt Cuba sanctions suspension is the company's decision to reverse its planned dissolution of Cuban assets while simultaneously maintaining a complete operational suspension. This seemingly contradictory posture makes sense when viewed through a sanctions legal framework.

Dissolving assets and renouncing interests in a sanctioned jurisdiction is not a legally neutral act. Depending on how the transaction is structured, unwinding a joint venture could itself constitute a prohibited transaction under the sanctions regime, potentially triggering violations rather than resolving them. There is also the question of asset valuation. Writing down Cuban assets to zero through formal dissolution forecloses any future recovery scenario, even if diplomatic conditions change. Maintaining suspended assets in limbo preserves optionality at the cost of operational and financial clarity.

After consulting with legal and financial advisors and reviewing information available following the initial suspension announcement, Sherritt concluded that proceeding with the dissolution and renunciation of its Cuban interests was not in the corporation's best interests at that time. The reversal specifically included abandoning the dissolution of General Nickel Company S.A., the entity through which the Moa joint venture is structured.

Cuba's Nickel and Cobalt: What Is Actually at Stake

To understand why the Sherritt Cuba sanctions suspension carries implications beyond one company's share price, it is necessary to appreciate the geological and market context of the Moa operation specifically.

Cuba's Holguín province hosts laterite nickel deposits, a fundamentally different ore type from the sulphide nickel deposits that dominate Canadian and Australian production. Laterite nickel, found extensively in Cuba, the Philippines, Indonesia, and parts of West Africa, is processed using pressure acid leaching technology, which produces a mixed nickel-cobalt sulphide or hydroxide intermediate that can then be refined into battery-grade materials. The Moa joint venture has been operating this process since the 1990s, making it one of the most established laterite nickel operations in the Western Hemisphere.

Sherritt holds a 50% stake in Moa Nickel S.A., operated alongside the Cuban state. The company also holds a one-third interest in Energas S.A., a joint venture that processes raw natural gas to generate electricity on the island, as well as stakes in Cuban oil drilling activities. This integrated presence means the sanctions impact extends beyond nickel and cobalt into Cuban power generation, creating a broader economic disruption than a pure mining operation would suggest.

The Cobalt Concentration Problem

Cobalt is where the supply chain implications become most acute. The global cobalt supply is heavily concentrated, with the Democratic Republic of Congo accounting for approximately 70% of mined supply. Outside of the DRC, significant cobalt production is limited to a relatively small number of operations, of which Cuban output through the Moa JV represents one of the few non-African, non-Indonesian sources accessible to Western refiners.

The strategic significance of this geography is considerable. Cobalt is a cathode material input for nickel-manganese-cobalt and nickel-cobalt-aluminium lithium-ion battery chemistries, both of which remain important in high-performance EV applications and aerospace power systems. Governments across the US, EU, Canada, and Australia have formally classified cobalt as a critical mineral precisely because of this combination of concentrated supply and strategic demand.

Removing Moa's cobalt output from the accessible Western supply pool, even temporarily, adds marginal pressure to an already geographically concentrated market. Furthermore, the beneficiaries of this supply displacement are likely to include:

- Australian cobalt producers with established Western offtake agreements

- DRC operators structured through Western-owned or partnered entities

- Battery material recyclers processing end-of-life lithium-ion cells

- Cobalt refining operations in Finland, Belgium, and Canada with diversified feedstock access

The Fort Saskatchewan Refinery: A Hard Deadline

One dimension of the Sherritt Cuba sanctions suspension that has received insufficient analytical attention is the specific operational vulnerability created at the Fort Saskatchewan, Alberta refinery. This facility processes Cuban-sourced nickel and cobalt feedstock into finished metals, and it represents Sherritt's primary revenue-generating asset in Canada.

With existing feedstock inventory projected to run out by mid-June 2026, the refinery faces a hard operational deadline that no amount of legal positioning can defer. There is no identified alternative feedstock source that could substitute Cuban supply on short notice. Laterite nickel intermediates are not fungible commodities traded on spot markets in the way that, for instance, copper concentrates are.

The refinery is engineered around specific feedstock characteristics, and sourcing equivalent material from alternative laterite operations would require both contractual arrangements and potentially process adjustments that cannot be completed within weeks. This creates a forced decision point that is independent of the sanctions legal debate. Regardless of how the dissolution question resolves, the refinery will face curtailment or shutdown unless either Cuban feedstock resumes or an alternative is secured.

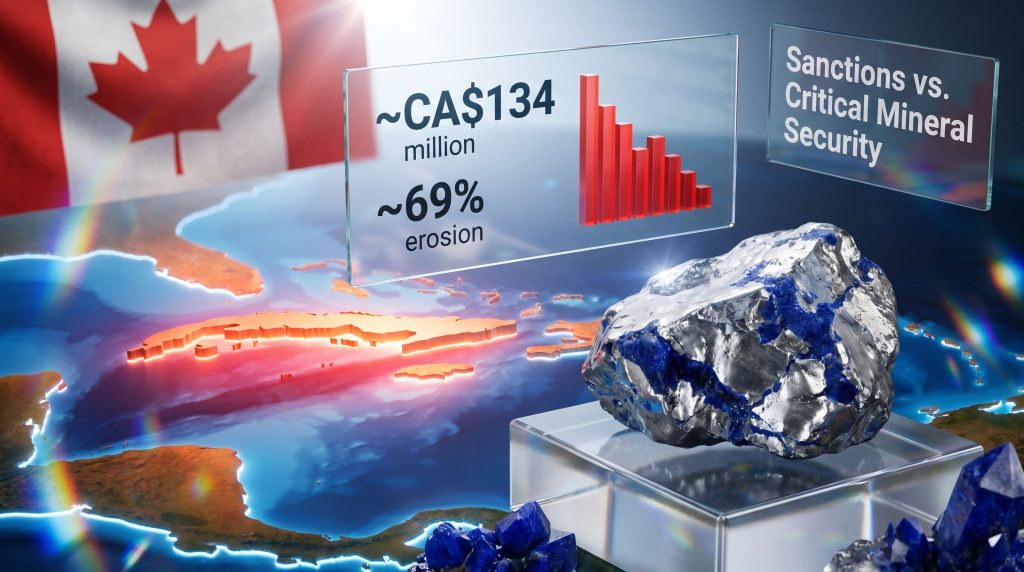

Valuation Destruction and the Compounding of Geopolitical Risk

| Period | Approximate Market Capitalisation (CAD) | Key Driver |

|---|---|---|

| Late 2000s commodity boom | ~CA$5 billion | High nickel prices, Moa JV at full production |

| May 7, 2026 (post-suspension announcement) | ~CA$134 million | Sanctions announcement, operational halt |

| Cumulative approximate decline | ~97% from peak | Compounding geopolitical, commodity, and operational risk |

Sherritt's market capitalisation trajectory is a case study in how geopolitical mining risks compound over time when they are not fully priced into asset valuations during periods of commodity strength. The company's shares were trading at approximately CA$0.18 by mid-morning on May 7, following the initial suspension announcement. The approximately 30% single-session decline that day reflected the market's attempt to rapidly reprice not just the operational disruption, but the fundamental jurisdictional exposure embedded in the investment thesis since the early 1990s.

The resignation of three board members on the same day as the suspension announcement adds a governance dimension that deserves specific attention. Directors of sanctioned entities face personal exposure that goes beyond reputational risk. Individual designation under US sanctions can result in asset freezes and travel restrictions. The departures of Brian Imrie, Richard Moat, and Brett Richards created a governance vacuum at precisely the moment requiring the most complex strategic decision-making the company has faced in its three-decade Cuba history.

The Sanctions vs. Supply Security Policy Contradiction

Washington's simultaneous policy objectives of securing critical mineral supply chains and expanding sanctions against Cuba's mining sector place these two strategic priorities in direct conflict, penalising one of the few non-Chinese cobalt producers accessible to Western refiners at a time when supply diversification is a stated priority across multiple allied governments.

This is not a new type of contradiction in US foreign policy. The Trump administration's broader regional strategy has deployed tariffs, sanctions, and diplomatic pressure against governments deemed adversarial, often without full coordination between the geopolitical objectives of those instruments and the supply chain security objectives pursued through separate policy channels. Congo cobalt disruptions have similarly illustrated how fragile supply structures can be when political decisions override market logic.

The GAESA designation is particularly illustrative of this tension. GAESA is Cuba's military-linked commercial conglomerate, controlling significant portions of the island's tourism, retail, and industrial sectors. Its simultaneous sanctioning alongside Moa Nickel S.A. signals that Washington's pressure campaign is targeting the structural economic architecture of the Cuban state comprehensively, not merely specific mining operations. However, this blanket approach inevitably captures critical mineral assets that Western supply chain policy would otherwise seek to develop and integrate.

The next major ASX story will hit our subscribers first

Scenario Analysis: Three Pathways Forward

Scenario 1: Diplomatic Resolution and Phased Resumption

A negotiated adjustment to the sanctions framework, potentially involving Canadian government engagement given that a Canadian company and Canadian jobs are directly affected, could create a pathway to resumed operations. This scenario requires a meaningful shift in US-Cuba diplomatic posture that is not currently evident. Timeline: 6 to 18 months minimum under optimistic assumptions.

Scenario 2: Prolonged Suspension and Constructive Abandonment

If no diplomatic resolution materialises before mid-June feedstock depletion, Fort Saskatchewan faces curtailment. Extended suspension without revenue from Cuban operations or the Alberta refinery would place severe pressure on Sherritt's financial position given its CA$134 million market capitalisation, which implies limited debt capacity and constrained equity raising options. This scenario risks de facto operational collapse without formal dissolution.

Scenario 3: Creditor-Driven Restructuring

Sanctions designations frequently trigger covenant breaches in existing debt facilities, as lenders build in provisions that treat designation events as defaults. If Sherritt's debt structure contains such provisions, creditor-driven restructuring could force asset sales or administration proceedings on a timeline driven by lender decisions rather than management strategy.

The reversal of the dissolution decision indicates that Sherritt's management and advisors continue to view the first scenario as sufficiently probable to warrant preserving optionality, accepting near-term operational and financial uncertainty in exchange for maintaining the possibility of a return to Cuban operations if the sanctions environment shifts.

What Foreign Mining Operators Should Take From the Sherritt Case

The Sherritt Cuba sanctions suspension offers a framework for assessing jurisdictional sanctions exposure that is applicable well beyond Cuba specifically. Lithium battery supply chains face similarly complex jurisdictional pressures, and consequently four layers of risk deserve consideration for any foreign resource operator in a geopolitically sensitive jurisdiction:

- Primary Designation Risk – The possibility that the company, its joint venture partners, or the state entities it operates alongside are formally listed under sanctions regimes

- Secondary Banking Risk – The withdrawal of financial services by institutions seeking to protect their own access to US correspondent banking infrastructure

- Operational Continuity Risk – The practical inability to source fuel, equipment, insurance, or services when counterparties assess designation risk as too high

- Asset Preservation vs. Dissolution Dilemma – The legal tension between maintaining ownership of suspended assets and potentially triggering violations through active management decisions

Sherritt's three-decade Cuba presence illustrates how all four of these risk layers can activate simultaneously when a sanctions trigger event occurs, and how the resulting operational paralysis can be more damaging than formal expropriation, which at least provides a defined legal endpoint and potentially an arbitration pathway.

The Helms-Burton precedent remains instructive. The personal legal exposure faced by Sherritt executives in the 1990s was a clear signal that Cuba operations carried asymmetric risk that commodity cycle strength could obscure but not eliminate. Furthermore, as reported by Mining.com, the current sanctions cycle represents an intensification of a legal risk environment that was never fully absent, even during the periods of highest profitability.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario analyses, and market assessments involve inherent uncertainty. Readers should conduct independent due diligence before making any investment decisions related to companies or sectors discussed herein. Past performance of commodity prices or company valuations is not indicative of future results.

Want to Stay Ahead of ASX Mineral Discoveries Amid Shifting Supply Chains?

As geopolitical pressures reshape critical mineral access globally, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex sector data into actionable investment insights for traders and long-term investors alike. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major opportunity.