July 17, 2026

The Infrastructure Gap Hiding Inside America's Precious Metals Market

Critical infrastructure rarely fails all at once. It degrades quietly, through accumulated assumptions that were never questioned and structural dependencies that were never mapped. The U.S. electricity grid required decades of stress events before redundancy became a legislative priority. Broadband internet built coastal concentration problems that took years of policy intervention to unwind. Now, a parallel vulnerability has been identified inside the architecture of America's precious metals futures market, and the SILVER Act precious metals depositories reform is the bipartisan legislative response taking shape.

The problem is straightforward once you understand the system: the vast majority of exchange-approved precious metals storage capacity in the United States is clustered within a narrow geographic corridor near New York City. This concentration was never the result of a deliberate national policy. It evolved organically from the historical proximity of commodity exchanges and the vault infrastructure built around them.

However, what began as a practical convenience has calcified into a systemic fragility that industry participants, legislators, and regulators are now actively working to correct.

When big ASX news breaks, our subscribers know first

What the SILVER Act Actually Is

Introduced on May 21, 2026, the System Integrity through Licensed Vault Expansion and Resilience Act, commonly referred to as the SILVER Act, represents one of the most substantive structural reforms proposed for U.S. precious metals market infrastructure in recent memory.

Filed simultaneously as Senate Bill SB 4621 and House Resolution H.R. 8007, the legislation carries genuine bipartisan credentials across both chambers of Congress. Lawmakers have introduced the Silver Act to increase precious metals storage sites across the U.S., addressing a long-standing infrastructure gap that has gone largely unaddressed for decades.

Legislative Sponsorship

| Chamber | Sponsor | Party | State |

|---|---|---|---|

| Senate | Sen. Jim Risch | Republican | Idaho |

| Senate | Sen. Catherine Cortez Masto | Democrat | Nevada |

| House | Rep. Mark Harris | Republican | North Carolina |

| House | Rep. Russ Fulcher | Republican | Idaho |

| House | Rep. Susie Lee | Democrat | Nevada |

The geographic spread of the bill's sponsors is itself instructive. Idaho, Nevada, and North Carolina are all states with meaningful existing or potential precious metals storage infrastructure, and none of them sit within the New York metro concentration zone that the bill seeks to disrupt.

What the Legislation Would Require

The SILVER Act does not designate specific depositories or hand-pick approved operators. Instead, it mandates a structural minimum by requiring:

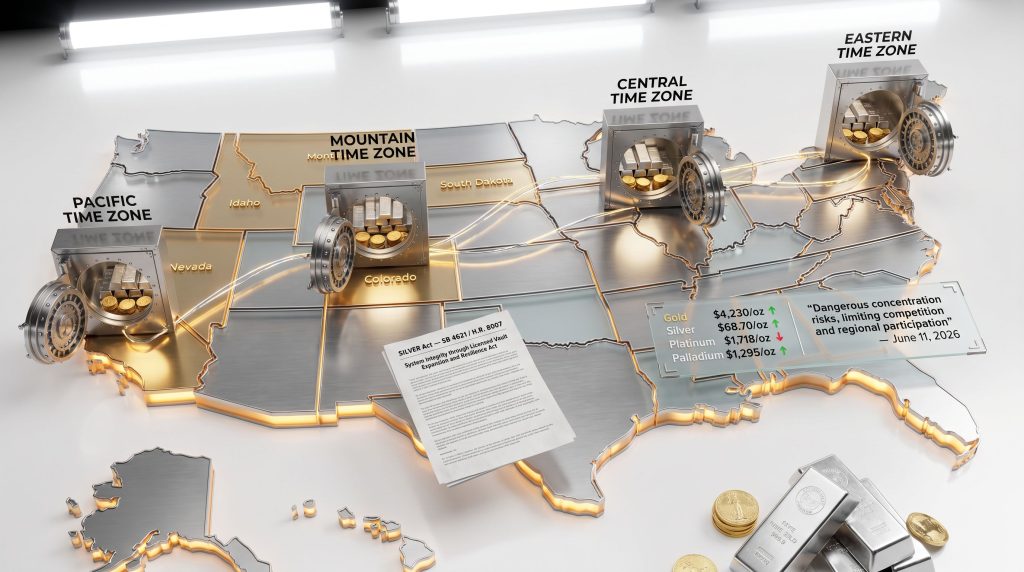

- At least two exchange-approved depositories in each of the four continental U.S. time zones: Eastern, Central, Mountain, and Pacific

- The establishment of transparent, objective evaluation criteria for depository approval processes

- Formal weighting of geographic concentration risk and broader public-interest considerations in approval decisions

This design choice is deliberate and important. Rather than prescribing outcomes, the legislation redesigns the evaluation framework itself, creating conditions for merit-based competition among vault operators across all U.S. regions.

Understanding the Concentration Problem

Why New York Became the Default

The current geographic concentration of approved depositories traces back to the structural gravity of commodity exchange infrastructure. COMEX, the primary U.S. exchange for gold and silver futures, is headquartered in New York. Approved delivery vaults naturally clustered nearby because physical proximity to exchange operations reduced logistical friction for institutional traders.

Over decades, this practical logic became self-reinforcing. New entrants seeking exchange-approved status faced approval processes that implicitly favoured incumbents operating within established geographic norms. The result is a market where futures contract delivery, the mechanism that ultimately anchors spot price discovery, depends overwhelmingly on vault capacity concentrated in a single metropolitan region.

The Compounding Risks

Concentration risk in precious metals storage does not operate in isolation. It creates cascading vulnerabilities across at least three distinct systems:

-

Financial markets: Futures contract settlement requires physical delivery to approved locations. Geographic clustering embeds regional risk directly into price discovery mechanisms.

-

Physical supply chains: Gold, silver, platinum, and palladium are no longer purely monetary metals. They are critical industrial inputs for defence systems, aerospace components, semiconductor manufacturing, medical devices, and clean energy technologies. A disruption to New York-area vault infrastructure could interrupt supply chains extending across the entire national economy.

-

National security frameworks: The strategic importance of precious metals has grown significantly as their role in advanced manufacturing has expanded. Single-region dependency for regulated storage of these materials creates a vulnerability profile that national security analysts increasingly flag as material.

Geographic redundancy is a foundational principle applied across critical infrastructure sectors from banking to energy grids to data centres. The fact that precious metals storage had not yet incorporated this principle reflects an oversight that is no longer defensible given the expanded industrial role these metals now play.

Furthermore, the 2025 gold and silver market dynamics driven by central bank activity have only amplified the urgency for robust domestic storage infrastructure.

How Other Commodity Markets Handle This

Agricultural futures markets distribute delivery infrastructure across dozens of designated storage facilities spanning multiple states and regions. Oil storage and pipeline infrastructure operates under regulatory frameworks that explicitly account for regional concentration risk. Precious metals storage has lagged significantly behind these models, and the SILVER Act is designed to close that gap.

The Distinction Between Depository Types

A common source of confusion in this debate is the difference between two distinct categories of regulated precious metals storage.

| Criteria | IRS-Approved Depository | Exchange-Approved Depository |

|---|---|---|

| Primary Use | Precious metals IRA storage | Futures contract physical delivery |

| Governing Body | Internal Revenue Service | CFTC / Exchange operators (e.g., COMEX) |

| Geographic Distribution | Relatively broader | Heavily concentrated near New York |

| Investor Type | Retail / retirement savers | Institutional / commercial traders |

| SILVER Act Impact | Indirect benefit | Direct reform target |

The SILVER Act specifically targets exchange-approved depository infrastructure, which governs how futures contracts are settled through physical delivery. For investors considering physical gold versus ETFs as investment options, understanding this distinction is increasingly relevant when evaluating custody and storage arrangements.

The Industry Coalition Driving Reform

A Sector-Wide Mobilisation

On June 11, 2026, a coalition of more than 40 companies and trade organisations submitted a formal letter to Congressional leadership urging advancement of the SILVER Act precious metals depositories legislation. The signatories represent every segment of the U.S. precious metals industry: dealers, refiners, private mints, vault operators, financial institutions, and industry associations.

The scale of this coordination is notable. Sector-wide alignment of this breadth around a single legislative reform is uncommon, and it signals that the geographic concentration problem has reached a threshold where industry participants across all market segments view reform as operationally necessary rather than merely preferable.

The Coalition's Core Arguments

The industry's case rests on five interconnected pillars:

-

Market structure distortions: Current approval frameworks impose artificial constraints on competition, effectively protecting incumbents rather than serving the broader public interest.

-

Supply chain resilience: Distributing regulated vault capacity across multiple U.S. regions would materially strengthen domestic precious metals supply chains.

-

Digital product innovation: Emerging technology-driven products, including digitally-backed physical metals and blockchain-verified storage instruments, require distributed infrastructure to function effectively at scale.

-

Liquidity expansion: Broader geographic access would deepen market participation from institutional and retail segments currently underserved by New York-centric infrastructure.

-

Cost reduction: Regional competition among approved depositories would compress storage and delivery premiums currently embedded in futures pricing, reducing costs for all market participants.

In addition, the supply constraints shaping precious metals in 2025 have reinforced the broader argument that domestic infrastructure resilience is no longer optional.

Regulatory Alignment: The CFTC Position

The political and regulatory context surrounding the SILVER Act is unusually well-aligned. CFTC Chairman Michael Selig has publicly indicated support for examining national security risks arising from the geographic concentration of precious metals depositories. Given that the CFTC would be the primary regulatory body responsible for implementing new depository approval standards under the legislation, this alignment between Congressional intent and regulatory-level acknowledgment is a meaningful indicator of the bill's viability.

The combination of bipartisan Congressional sponsorship, cross-industry coalition support, and regulatory-level engagement creates a policy environment where structural reform appears genuinely achievable rather than aspirational.

The next major ASX story will hit our subscribers first

Existing Models That Prove the Concept

One of the SILVER Act's strongest arguments is that geographic distribution of regulated precious metals storage is not a theoretical proposition. It already works.

The Texas Bullion Depository, a state-operated facility established under Texas law, represents a functioning model demonstrating that regulated, audited precious metals storage outside the New York ecosystem is both operationally viable and publicly trusted. Several private vault operators in the Mountain and Pacific time zones similarly serve institutional and retail clients effectively but currently lack exchange-approved status.

The SILVER Act would create a clear, transparent regulatory pathway for these existing facilities to seek exchange approval under standardised, publicly available criteria. States including Nevada, Idaho, Colorado, South Dakota, Montana, and Alaska have been identified as natural beneficiaries of expanded regional storage mandates.

Current Precious Metals Market Context

Precious metals prices as of the week of June 21, 2026 reflect broader macroeconomic conditions independent of the legislative process.

| Metal | Spot Price | Weekly Change |

|---|---|---|

| Gold | $4,230/oz | -3.0% |

| Silver | $68.70/oz | -2.0% |

| Platinum | $1,718/oz | -6.0% |

| Palladium | $1,295/oz | ~0.0% |

Disclaimer: These price movements reflect macroeconomic factors including interest rate expectations and currency dynamics. They are not directly connected to the SILVER Act legislative process. Precious metals prices are volatile and past performance is not indicative of future results. Nothing in this article constitutes financial or investment advice.

Platinum's notable weekly decline of 6% from the prior Friday level of $1,831 per ounce is particularly relevant to the structural debate. Platinum's growing role in hydrogen fuel cell technology and industrial catalysis makes its supply chain security increasingly significant. Consequently, the concentration of regulated storage infrastructure represents more than a futures market technicality. Moreover, the trade war's ongoing impact on gold and silver prices further underscores the need for resilient domestic infrastructure.

Long-Term Structural Implications

Market Architecture Transformation

If enacted, the SILVER Act would trigger a multi-year restructuring of how physical precious metals are stored, transferred, and delivered across the United States. The downstream implications extend well beyond the futures market:

-

Basis risk reduction: Improved physical delivery access across time zones could narrow the spread between regional spot prices and futures pricing, improving market efficiency for participants outside the Northeast.

-

New financial instrument development: Physically-backed exchange-traded funds with distributed custody arrangements, tokenised metals with blockchain-verified regional storage, and regionally-settled futures contracts all become more structurally feasible under a geographically distributed vault network.

-

Onshoring of critical materials management: A distributed domestic vault network aligns with broader U.S. industrial policy trends emphasising the repatriation and domestic management of critical materials supply chains.

What the SILVER Act Does Not Do

It is equally important to understand the legislation's boundaries. The SILVER Act does not:

- Mandate approval of any specific depository or vault operator

- Guarantee market outcomes for regional storage facilities

- Override existing CFTC regulatory authority

- Constitute government funding, backing, or direct financial support for any specific project or company

The reform is procedural and structural. It changes the rules of engagement so that qualified operators outside the New York region can compete on transparent terms. What they do with that access remains entirely market-driven.

Frequently Asked Questions: SILVER Act and Precious Metals Depositories

What does the SILVER Act stand for?

The SILVER Act is an acronym for the System Integrity through Licensed Vault Expansion and Resilience Act, a bipartisan piece of U.S. legislation introduced in May 2026 to reform the geographic distribution of exchange-approved precious metals depositories.

Why are precious metals depositories concentrated near New York City?

Exchange-approved depository status historically followed the institutional gravity of COMEX, the primary U.S. gold and silver futures exchange headquartered in New York. Vaults clustered nearby for logistical convenience, and the approval process reinforced this concentration over time.

How many depositories would the SILVER Act require per time zone?

The legislation would mandate at least two exchange-approved depositories in each of the four continental U.S. time zones, Eastern, Central, Mountain, and Pacific, ensuring minimum national coverage across all major regions.

Does the SILVER Act affect gold IRAs?

Indirectly. While the SILVER Act primarily targets exchange-approved futures delivery infrastructure governed by the CFTC, a broader distribution of regulated vault facilities could expand the pool of IRS-eligible storage options available to precious metals IRA holders over time.

Who supports the SILVER Act?

Support includes a coalition of more than 40 industry companies and trade organisations, bipartisan Congressional sponsors across both chambers, and regulatory-level interest from CFTC Chairman Michael Selig. The precious metals market analysis for 2025 further contextualises why this level of institutional backing has emerged at this particular moment.

Which states could benefit most from the SILVER Act?

States including Nevada, Idaho, North Carolina, Colorado, South Dakota, Montana, and Alaska have been identified as potential locations for new or expanded exchange-approved depository facilities under a more geographically distributed regulatory framework.

Key Takeaways

The SILVER Act precious metals depositories reform addresses a structural vulnerability in U.S. precious metals infrastructure that has been accumulating for decades without adequate policy response. Several dimensions of its significance stand out:

- The legislation's bipartisan construction and cross-industry coalition backing signal genuine reform momentum rather than symbolic positioning

- Geographic diversification of exchange-approved depositories directly addresses compounding risks spanning financial markets, industrial supply chains, and national security considerations

- The reform's procedural design, changing evaluation frameworks rather than mandating specific outcomes, makes it structurally durable and resistant to special-interest capture

- Existing models like the Texas Bullion Depository already demonstrate that distributed regulated storage is operationally viable

- CFTC Chairman Selig's engagement with the national security dimensions of depository concentration creates an unusually aligned regulatory and legislative environment

- For precious metals markets increasingly shaped by industrial demand in defence, aerospace, and clean energy, the question of where physical metals are stored and how quickly they can be accessed has moved from a back-office concern to a strategic priority

The SILVER Act precious metals depositories reform debate ultimately reflects a broader reckoning with how critical infrastructure should be designed for resilience in an era of elevated geopolitical and supply chain uncertainty. The question is no longer whether geographic diversification of vault infrastructure is warranted. It is whether the legislative and regulatory machinery can move quickly enough to address a vulnerability that has been hiding in plain sight.

Want To Stay Ahead Of The Next Major Precious Metals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across gold, silver, platinum, and palladium — turning complex data into actionable insights for investors at every level. Explore historic discoveries and their returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.