July 23, 2026

Silver's Irreplaceable Industrial Properties

Industrial demand for silver has fundamentally transformed the precious metals landscape, driven by silver's unique atomic structure that creates unmatched performance characteristics. At the molecular level, silver's single valence electron configuration enables optimal electron mobility, making it the most electrically conductive element on Earth. This fundamental physics drives demand across sectors where performance margins determine success or failure.

Modern industrial applications depend on silver's unique combination of electrical conductivity, thermal management, and antimicrobial properties. Unlike other precious metals, silver delivers performance characteristics that cannot be synthetically reproduced or economically substituted.

Table: Silver's Industrial Performance vs. Alternatives

| Property | Silver Performance | Best Alternative | Performance Gap |

|---|---|---|---|

| Electrical Conductivity | 63.0 × 10⁶ S/m | Copper (59.6 × 10⁶ S/m) | 5.4% efficiency advantage |

| Thermal Conductivity | 429 W/m·K | Copper (401 W/m·K) | 7% heat dissipation advantage |

| Antimicrobial Effect | Natural oligodynamic | Synthetic coatings | No equivalent substitute |

| Signal Integrity (5G+) | Optimal at 5+ GHz | Copper degrades >3 GHz | Critical for high-frequency |

Why Substitution Attempts Fail

Industrial engineers have spent decades attempting to replace silver with cheaper alternatives, yet these efforts consistently fail in high-performance applications. Copper approaches silver's conductivity but falls short in applications requiring signal integrity above 5 GHz, which includes all 5G telecommunications infrastructure. The 5.4% conductivity gap translates to measurable signal degradation in radiofrequency applications.

Technical Performance Breakdown:

- Aluminum: Only 37% of silver's conductivity, oxidises rapidly

- Carbon nanotubes: Laboratory-stage only, cannot achieve commercial-scale production

- Gold: Superior corrosion resistance but 100x cost premium limits use to aerospace applications

- Synthetic antimicrobials: Degrade over time, cannot match silver's persistent biocidal effect

In thermal management applications, silver's 7% advantage over copper translates to 3-5°C lower operating temperatures in processor cores, directly extending component lifespan and system reliability.

When big ASX news breaks, our subscribers know first

Electronics Manufacturing: The Demand Foundation

Electronics manufacturing consumes approximately 460-480 million ounces of silver annually as of 2024, representing 33% of total industrial demand for silver. This sector's growth stems from fundamental technological trends that multiply silver requirements rather than reduce them.

Device-Level Silver Integration

Every smartphone contains 200-300 milligrams of silver distributed across multiple critical components:

- Circuit board traces: Primary conductor paths requiring zero signal loss

- Switching contacts: Power management circuits handling rapid on/off cycles

- Antenna elements: Cellular, Wi-Fi, and Bluetooth transmission systems

- Solder alloys: IPC-A-610 standard tin/silver/copper compositions

Industry Volume Multiplier Effect:

- Annual smartphone production: ~1.3 billion units globally

- Silver per device: 250 mg average

- Total smartphone silver consumption: ~10.4 million ounces annually

- This represents just smartphone production within the broader electronics category

5G Infrastructure Silver Requirements

The global 5G network buildout creates structural industrial demand for silver that extends through 2028. Each 5G base station requires 8-15 grams of silver in antenna arrays, power distribution circuits, and radiofrequency switching components.

5G Deployment Impact:

- Target installations (2024-2028): 5-6 million base stations globally

- Silver per base station: 11.5 grams average

- Cumulative 5G silver demand: 60-75 million ounces over deployment period

- Annual requirement: 15-19 million ounces during peak buildout years

Critical Insight: Silver's performance advantage actually widens at higher frequencies. While copper handles 2G-4G applications adequately, 5G's 2.6-28 GHz operating range makes silver's conductivity advantage essential rather than optional.

IoT Device Expansion

Internet of Things deployment represents an emerging but rapidly expanding silver consumption category. Connected device installations grew from 15.1 billion active units in 2024 toward a projected 27.5 billion by 2030.

IoT Silver Consumption Analysis:

- Average silver content per IoT device: 50-200 mg (varies by complexity)

- Current annual IoT silver demand: 15-25 million ounces

- Projected 2030 IoT silver demand: 35-50 million ounces

- Growth rate: 12-15% annually through 2030

Solar Photovoltaics: The Fastest-Growing Application

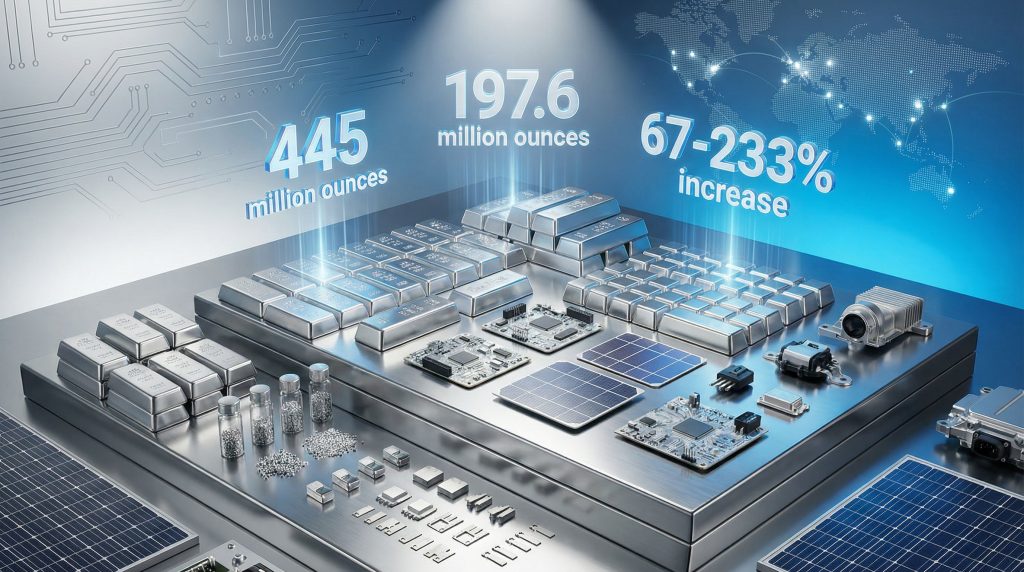

Solar panel manufacturing consumed 197.6 million ounces in 2024, making photovoltaics the fastest-expanding industrial silver application with 29% of total industrial demand for silver. Furthermore, unlike other sectors where efficiency improvements reduce material requirements, advanced solar cell designs actually increase silver consumption per panel.

Panel Silver Content Evolution

Each photovoltaic panel requires 15-20 grams of silver distributed across multiple components:

- Front-surface electrode grids: 10-12 grams (primary current collection)

- Back-contact systems: 2-3 grams (bifacial panel designs)

- Interconnection ribbons: 1-2 grams (cell linking)

- Advanced cell architectures: +30-40% silver vs. conventional designs

Efficiency Paradox in Solar Technology:

Modern high-efficiency cell designs (TOPCon, heterojunction) require more silver per unit, not less. These technologies need thicker electrode grids to handle increased current densities from higher conversion efficiency, directly increasing silver requirements by 30-40% compared to older panel technology.

Global Solar Installation Trajectory

Installation Capacity Growth:

- 2024: 2.2 TW total installed capacity worldwide

- 2030 IEA Net Zero target: 7+ TW installed capacity

- Annual installation rate (2024): ~400 GW added globally

- Required 2030 installation rate: 800+ GW annually

Projected Silver Demand Impact:

| Year | Installation Rate | Silver per GW | Annual Silver Demand |

|---|---|---|---|

| 2024 | 400 GW | 494,000 oz/GW | 197.6 million oz |

| 2027 | 600 GW | 510,000 oz/GW | 306 million oz |

| 2030 | 800+ GW | 525,000 oz/GW | 420+ million oz |

Supply Chain Concentration Risk

Over 80% of global photovoltaic panel manufacturing occurs in China, creating geographic concentration risk for industrial demand for silver. Chinese solar installations alone consumed approximately 40-45 million ounces in 2024, representing 20% of global solar silver demand from a single country's domestic market.

China Solar Manufacturing Scale:

- 2024 domestic installations: 218 GW (53% of global additions)

- Manufacturing capacity: 77% of global PV production

- Projected 2030 installations: 300+ GW annually

- Implied 2030 silver demand from China alone: 55-65 million ounces

Electric Vehicle Silver Integration Patterns

Electric vehicle production creates a 67-233% increase in silver consumption per vehicle compared to conventional internal combustion engines. Consequently, this fundamentally reshapes automotive industrial demand for silver patterns across the sector.

Vehicle Platform Silver Content

Table: Automotive Silver Usage by Vehicle Type

| Vehicle Category | Silver Content | Primary Applications |

|---|---|---|

| Conventional ICE | 15-28 grams | Engine management, basic electronics |

| Hybrid Electric | 35-45 grams | Dual powertrains, regenerative systems |

| Battery Electric | 25-50 grams | Motor controllers, charging infrastructure |

| Autonomous-Ready | 50-80 grams | Sensor arrays, computing platforms |

EV-Specific Silver Applications

Electric vehicles require silver in applications absent from conventional vehicles:

- Battery management systems: Precision current monitoring and thermal control

- Motor controllers: High-frequency switching circuits managing AC motor operation

- Onboard charging systems: AC-DC conversion requiring signal integrity

- Thermal management: Heat dissipation in high-power battery and motor systems

Market Penetration Impact Analysis:

The transition from 15-28 grams (ICE) to 25-50 grams (BEV) per vehicle creates multiplicative demand growth as EV market share increases.

- Conservative scenario (30% EV share by 2030): +45 million ounces annually

- Moderate scenario (50% EV share by 2030): +75 million ounces annually

- Aggressive scenario (70% EV share by 2030): +105 million ounces annually

Moreover, this analysis examines tariff impacts on silver pricing as trade policies affect manufacturing locations.

Autonomous Vehicle Silver Intensity

Self-driving vehicle development adds another layer of silver requirements beyond basic electrification:

- LiDAR sensor systems: Precision optoelectronic components

- Radar arrays: Multiple radiofrequency transmission/reception units

- Computing platforms: AI processing requiring advanced thermal management

- Communication systems: 5G connectivity for vehicle-to-infrastructure data

Fully autonomous vehicles may contain 50-80 grams of silver, representing a 250-400% increase over conventional vehicles.

AI Infrastructure and Data Centre Demand

Artificial intelligence expansion and data centre growth represent an emerging but rapidly accelerating industrial demand for silver category. Global IT power capacity has grown 53 times since 2000, with AI computing demand projected to increase 300% by 2030.

Data Centre Silver Applications

Computing Infrastructure Requirements:

- Server motherboards: Enhanced conductivity for multi-GHz processor operation

- Memory modules: Signal integrity in high-density RAM configurations

- Storage systems: Data transmission in solid-state and optical storage

- Cooling systems: Thermal management in high-power computing environments

- Power distribution: Efficient electricity delivery to computing clusters

Silver Intensity Metrics:

- Silver content per data centre: 2-5 kg per megawatt of computing capacity

- Hyperscale facility requirements: 15-25 kg silver per facility

- Edge computing deployment: 0.5-2 kg per distributed processing node

AI Computing Silver Requirements

Machine learning and AI training systems create silver demand through specialised hardware requirements:

- GPU clusters: Graphics processing units requiring advanced thermal solutions

- Tensor processing units: Custom AI chips with high-frequency signal integrity needs

- Quantum computing research: Superconducting circuits requiring ultra-pure silver components

- Networking infrastructure: High-bandwidth data transmission between processing nodes

Projected AI Silver Demand:

Current AI infrastructure silver consumption remains relatively small at 5-8 million ounces annually. However, growth trajectories suggest 20-35 million ounces by 2030 as AI computing scales exponentially.

Silver Supply Structure and Industrial Availability

Silver's unique supply structure creates industrial availability challenges fundamentally different from other commodities. Approximately 70-80% of silver production comes as a by-product of base metal mining, making supply largely unresponsive to silver price movements.

By-Product Mining Dependency

Table: Silver Production Sources and Price Sensitivity

| Source Category | Production Share | Price Responsiveness | Supply Flexibility |

|---|---|---|---|

| Primary silver mines | 20-30% | High | Moderate |

| Copper by-product | 35-40% | Low | Limited |

| Lead/zinc by-product | 25-30% | Low | Limited |

| Gold by-product | 10-15% | Moderate | Limited |

Supply Constraint Dynamic: When base metal producers reduce output due to copper or zinc market conditions, silver production automatically decreases regardless of silver price levels. This creates potential shortages during periods of strong industrial demand for silver.

Additionally, recent analysis of silver supply deficits drivers demonstrates how these structural factors intensify market imbalances.

Secondary Supply and Recycling

Silver recycling rates vary dramatically across applications, affecting long-term supply availability:

Recovery Rates by Application:

- Electronics recycling: 15-25% recovery rate (complex disassembly)

- Photovoltaic panels: <5% (recycling technology still developing)

- Automotive components: 40-60% (established recycling infrastructure)

- Industrial catalysts: 85-95% (high-value recovery economics)

Recycling Limitations:

Even with improved recycling infrastructure, industrial applications face structural recycling constraints. Solar panels have 25-30 year lifespans, meaning silver installed in 2024 panels won't become available for recycling until 2049-2054. Electronics have shorter lifespans (3-5 years) but complex recovery processes limit actual silver retrieval.

The next major ASX story will hit our subscribers first

Long-Term Industrial Demand Projections

Multiple technological megatrends are converging to drive sustained industrial demand for silver growth through 2030 and beyond. In addition to current applications, these trends create a structural demand floor that transcends economic cycles.

Structural Demand Drivers

Green Energy Transition Timeline:

- Solar installations: 2.2 TW (2024) → 7+ TW (2030)

- Wind power electronics: Growing silver intensity per turbine for grid integration

- Grid modernisation: Smart grid infrastructure requiring enhanced conductivity

- Energy storage: Battery management systems for utility-scale installations

Electrification Megatrend:

- Transportation: 30-70% EV market penetration projected by 2030

- Industrial processes: Heat pumps, electric heating, process electrification

- Residential: Electric appliance adoption in developing markets

Comprehensive Demand Forecast

Table: Industrial Silver Demand Projections by Sector (Million Ounces)

| Sector | 2024 Actual | 2027 Projection | 2030 Projection | CAGR |

|---|---|---|---|---|

| Electronics | 470 | 545 | 630 | 5.0% |

| Solar PV | 198 | 290 | 420 | 13.2% |

| Automotive | 68 | 98 | 145 | 13.4% |

| AI/Data Centres | 8 | 18 | 32 | 25.9% |

| Other Industrial | 180 | 195 | 215 | 3.0% |

| Total Industrial | 924 | 1,146 | 1,442 | 7.7% |

Investment Implications of Industrial Silver Demand

Industrial demand for silver creates fundamentally different investment dynamics compared to monetary or jewellery demand. For instance, this provides both stability and volatility amplification depending on market conditions.

Demand Stability Characteristics

Low Price Elasticity in Industrial Applications:

Industrial users prioritise performance over cost in most applications. A 50% increase in silver prices might reduce smartphone production margins by 0.1-0.2%, insufficient to trigger substitution efforts that would require 18-24 months and $50-100 million in R&D investment per product line.

Long Replacement Cycles:

Technology transitions occur over 5-10 year periods, creating demand visibility that extends well beyond typical commodity cycles. Once silver becomes integrated into manufacturing processes (solder alloys, plating chemistry, component specifications), switching costs become prohibitive.

Market Structure Impact

Demand Categories and Price Impact:

- Industrial demand: 61% of total consumption, provides price floor

- Investment demand: 18% of total, creates price volatility

- Jewellery demand: 21% of total, moderately price-sensitive

Industrial demand for silver has grown from 53% (2016) to 61% (2025) of total consumption, creating a fundamental floor for silver prices. Unlike investment demand, which can disappear during economic optimism, industrial applications require continuous silver consumption regardless of macroeconomic conditions.

Furthermore, market analysts study the silver market squeeze impact on broader financial systems as industrial demand intensifies supply constraints.

Supply Deficit Persistence:

The silver market has operated in structural supply deficits for five consecutive years (2021-2025), with 2024 showing a deficit of 148.9 million ounces despite 2% supply growth.

Strategic Investment Considerations

Market Psychology Insight: Industrial demand provides silver's fundamental value foundation, while investment demand creates amplified price movement potential during monetary stress periods. This dual character makes silver both a technology play and a monetary hedge simultaneously.

Risk-Reward Profile:

Silver's industrial exposure means it doesn't behave like gold during initial market stress, often selling off with commodities before recovering as a monetary asset. However, the structural industrial demand floor means severe price declines face growing industrial buying support.

The convergence of solar, electric vehicles, 5G infrastructure, and AI computing creates multiple independent demand drivers unlikely to weaken simultaneously, providing portfolio diversification within a single commodity position.

Additionally, current silver squeeze market analysis reveals how industrial demand intersects with retail investor behaviour to create unique market dynamics.

FAQ: Industrial Silver Demand Insights

What percentage of global silver demand comes from industrial applications?

Industrial and technology applications account for approximately 61% of total global silver demand as of 2025, up from 53% in 2016. This growth reflects silver's essential role in green energy, electronics, and automotive electrification technologies that cannot substitute alternative materials.

Which industrial sector consumes the most silver annually?

Electronics manufacturing is the largest industrial silver consumer, using approximately 470 million ounces in 2024 or roughly one-third of total industrial demand for silver. This includes smartphones, computers, automotive electronics, and telecommunications infrastructure requiring silver's superior conductivity.

How much silver does a typical solar panel contain and why?

Each solar photovoltaic panel contains approximately 15-20 grams of silver, primarily in front-surface electrode grids and interconnection systems. Advanced high-efficiency cell designs (TOPCon, heterojunction) actually require 30-40% more silver than older technology due to increased current handling requirements.

Why can't industrial users substitute other materials for silver?

Silver exhibits the highest electrical conductivity of any element at 63.0 × 10⁶ S/m, compared to copper's 59.6 × 10⁶ S/m. This 5.4% performance gap becomes critical in high-frequency applications like 5G infrastructure, where signal integrity determines system functionality. No synthetic alternative matches silver's combined electrical, thermal, and antimicrobial properties.

How do electric vehicles impact silver demand compared to conventional cars?

Electric vehicles use 25-50 grams of silver compared to 15-28 grams in conventional vehicles, representing a 67-233% increase. The additional silver goes into battery management systems, motor controllers, charging infrastructure, and enhanced electronics packages that don't exist in internal combustion engines.

What happens to industrial silver demand if recycling rates improve significantly?

Current industrial silver recycling rates vary dramatically: electronics (15-25%), automotive (40-60%), and industrial catalysts (85-95%). Even with improved recycling, structural constraints limit impact. Solar panels have 25-30 year lifespans, meaning silver installed today won't become recyclable until 2049-2054, while growing applications outpace recycling improvements.

How does AI and data centre growth affect silver consumption?

AI infrastructure currently consumes 8 million ounces annually but projects 25.9% annual growth through 2030. Each data centre requires 2-5 kg of silver per megawatt of capacity in servers, memory modules, cooling systems, and power distribution networks. As AI computing scales exponentially, this sector could reach 32 million ounces by 2030.

Will technological advances reduce industrial silver requirements over time?

Counterintuitively, technological advances often increase silver requirements rather than reduce them. Advanced solar cells need more silver for higher current densities, 5G infrastructure requires silver for signal integrity at higher frequencies, and electric vehicles need silver for applications that don't exist in conventional cars. Miniaturisation may reduce silver per component but increases total component count.

For comprehensive market analysis covering all precious metals trends, see our latest precious metals analysis report. Additionally, the Silver Institute's supply and demand data provides authoritative statistics on global silver consumption patterns. Meanwhile, recent research from Mining Weekly highlights how supply deficits and industrial demand are driving silver prices higher across global markets.

Considering Silver Investments Based on Industrial Demand Trends?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including silver exploration breakthroughs that could benefit from this accelerating industrial demand. Begin your 14-day free trial today and position yourself ahead of the market as industrial silver consumption continues its structural growth trajectory.