July 9, 2026

The Hidden Architecture Behind Silver's Monthly Price Drops

Every commodity market contains layers that most participants never see. For silver, one of those layers activates on a predictable monthly schedule, producing price drops that look alarming, generate panicked selling, and then quietly reverse within days. The investors who understand this mechanism hold a structural advantage. Those who do not tend to exit positions at precisely the wrong moment, then watch the price recover without them.

This is not a fringe theory. The silver options expiration price drop is a recurring, calendar-driven event rooted in the mathematics of derivatives markets. Understanding it requires stepping beneath the surface of quoted silver prices into the mechanics of how those prices are actually formed.

When big ASX news breaks, our subscribers know first

Silver's Two-Layer Price Architecture: Paper and Physical

Most investors interact with silver through a single number: the spot price. What that number actually reflects is less straightforward than it appears.

Silver trades simultaneously across two fundamentally different markets:

- The physical market, where real silver changes hands between miners, refiners, industrial buyers, jewellers, and retail investors

- The paper derivatives market, where futures and options contracts on COMEX trade at volumes that dwarf physical transactions by orders of magnitude

The spot price that appears on financial terminals and dealer websites is derived from COMEX paper-market settlement, not from real-time physical transactions. These two layers connect at settlement points, but between settlements they operate under entirely different rules, incentive structures, and leverage profiles.

This dual architecture is precisely why silver exhibits predictable, recurring price behaviour tied to monthly expiration cycles. Furthermore, to understand why, it helps to understand what COMEX silver options actually are and who writes them. Silver's dual role as both a monetary and industrial asset further complicates how these layers interact, which is why understanding silver's dual role is essential context for any serious investor.

What COMEX Silver Options Actually Are

A COMEX silver option is a contract giving its buyer the right, but not the obligation, to buy or sell a silver futures contract at a predetermined strike price before a specific expiration date. Options expire on a monthly schedule, and the next expiration as of July 2026 is scheduled for July 29, 2026.

The critical dynamic involves the parties who sell these options rather than buy them. Options writers, typically institutional traders and market makers, collect the premium paid by options buyers upfront. Their profit is maximised when options expire worthless, meaning the underlying asset's price never reaches the strike level. A trader who has sold call options at a $50 strike price collects the full premium only if silver closes below $50 at expiration. That financial incentive is direct, significant, and it comes with the tools to act on it.

Key Concept: Options writers profit when contracts expire worthless. This creates a measurable financial incentive to keep silver below key strike prices heading into expiration, and the paper futures market provides the mechanism to do exactly that.

Delta Hedging: The Algorithm That Moves Silver's Price

How the Mechanics Work

Delta is a measure of how sensitive an option's value is to changes in the price of the underlying asset. When an options writer sells call options, their delta exposure increases as silver's price rises toward the strike. To hedge this risk, they sell futures contracts, which offsets their paper exposure.

Here is the critical detail: this hedging is not discretionary. Algorithms execute the trades automatically the moment predefined price thresholds are crossed. No human makes the decision. A mathematical trigger fires, and futures are sold into the market. The effect on the quoted spot price is real and immediate, even though no physical silver has changed hands.

How Leverage Multiplies the Effect

The leverage structure inside COMEX silver amplifies this mechanism considerably:

- Layer 1: Silver futures carry approximately 5:1 leverage relative to physical silver

- Layer 2: Options on futures create a second-order leverage system layered on top of futures positions

This stacked leverage means a relatively modest volume of paper selling can produce a measurable downward shift in the quoted spot price. Silver is particularly susceptible to this effect compared to gold, because silver's physical market is significantly smaller relative to its paper derivatives market, making the ratio of paper volume to physical volume exceptionally high.

The Gamma Amplification Layer

Gamma is the rate at which delta changes as the underlying price moves. Near expiration, gamma grows extremely large around key strike prices, meaning even minor price movements trigger disproportionately large hedging responses.

This creates a feedback mechanism known as a gamma squeeze: forced hedging that accelerates as the price approaches a strike level, amplifying volatility in the final hours surrounding expiration. The entire process is mathematically driven, not coordinated in any conspiratorial sense.

Technical Insight: Near expiration, gamma exposure in silver options can compress what would normally be a multi-day price move into a window of hours. This is why silver's expiration-driven drops frequently appear sudden and disproportionate to any visible news catalyst.

Structural Mechanics vs. Manipulation: A Critical Distinction

The silver options expiration price drop occupies an uncomfortable conceptual space for many investors. It is neither pure noise nor straightforward manipulation. The analytical distinction matters:

| Category | Description | Legal Status |

|---|---|---|

| Delta hedging | Algorithmic futures selling to offset options exposure | Legal, systematic |

| Gamma pressure | Forced hedging amplification near strike prices | Legal, mathematical |

| Pin risk | Price gravitating toward dominant strike levels at expiration | Legal, structural |

| Margin-driven liquidation | Forced selling from margin calls at elevated volatility | Legal, structural |

| Spoofing | Placing and cancelling large orders to create false signals | Illegal, CFTC-enforced |

The observable evidence supports systematic mechanics as the primary driver: silver price drops near COMEX expiration are recurring, measurable, time-bounded, and calendar-correlated. These characteristics align with structural market dynamics rather than random noise or purely ad hoc intervention.

Notably, historical expiration cycles have seen margin increases of up to 300% that forced leveraged liquidations independent of any deliberate price management, further amplifying downward pressure during expiration windows. Phenomena such as silver backwardation also interact with these mechanics, adding further complexity to price behaviour around expiration dates.

The Pin Risk Phenomenon

A particularly counterintuitive aspect of options expiration mechanics is pin risk: the tendency for heavily traded options to cause silver to close precisely at or near a major strike price at expiration. As expiration approaches, delta hedging activity around a dominant strike creates a gravitational pull toward that level. When silver closes at a round-number strike, both call and put options on either side expire worthless simultaneously, which represents the maximum profit outcome for options writers on both sides of the market.

Silver's Physical Fundamentals Are Structurally Indifferent to Paper Events

Industrial Demand: The Driver That Ignores Expiration Dates

Whatever happens on COMEX options expiration day, solar panel factories keep running. Electric vehicles keep rolling off production lines. Semiconductor fabrication continues uninterrupted.

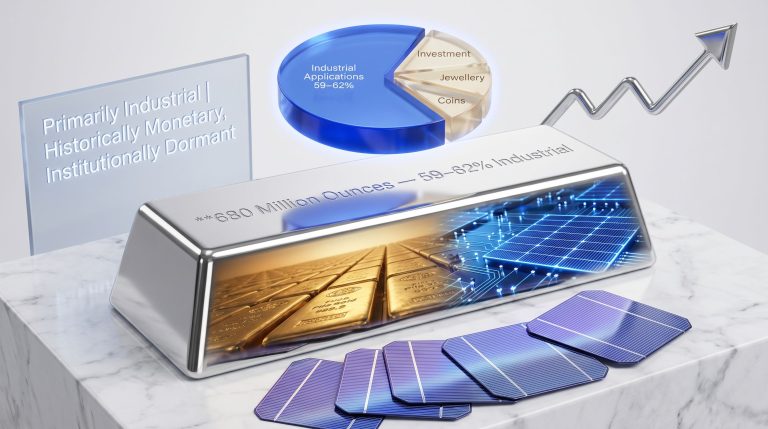

According to the Silver Institute's World Silver Survey 2025, global silver industrial demand reached 680.5 million ounces in 2024, the fourth consecutive annual record. Industrial applications now account for approximately 61% of total silver demand, a structural shift from roughly 35% approximately 25 years ago.

The primary industrial demand categories driving this growth include:

- Solar photovoltaics: The largest and fastest-growing application, directly tied to global renewable energy expansion

- Electric vehicles: Silver-intensive electrical architectures across drivetrains, battery management systems, and charging infrastructure

- Electronics and semiconductors: Persistent baseline demand across consumer and industrial applications

A silver options expiration price drop does not reduce industrial consumption by a single ounce. This is not a subtle point. It is the foundational reason why paper-market events do not alter the structural investment thesis.

The Five-Year Supply Deficit That Paper Trading Cannot Erase

The supply side of the silver market presents an equally compelling structural picture. According to the Silver Institute's World Silver Survey 2025, global mine production reached approximately 820 million ounces in 2024, while total demand came in at roughly 1.16 billion ounces. These persistent silver supply deficits underscore just how disconnected paper-market events are from the underlying physical reality.

| Year | Mine Production (Moz) | Total Demand (Moz) | Structural Deficit (Moz) |

|---|---|---|---|

| 2024 | ~820 | ~1,160 | 148.9 |

| 2023 | Consecutive deficit year | Consecutive deficit year | Year 3 |

| 2022 | Consecutive deficit year | Consecutive deficit year | Year 2 |

| 2021 | Consecutive deficit year | Consecutive deficit year | Year 1 |

| 2025 | Consecutive deficit year | Consecutive deficit year | Year 5 |

The 148.9 million ounce deficit in 2024 was the fourth consecutive annual shortfall. Through 2025, that streak extended to five consecutive years of structural deficit, per the Silver Institute's World Silver Survey 2026. This is not a paper-market event. It is a physical reality that no volume of futures selling can manufacture away.

Further reinforcing the physical tightness, as of mid-2026, silver futures markets remain in backwardation, meaning spot prices trade above futures prices. This inversion of the normal market structure signals acute near-term demand pressure. For context, only approximately 14% of COMEX silver futures positions are covered by physical inventory, a ratio that creates the conditions for a potential short squeeze if paper-market corrections deepen rather than reverse.

Data Point: A five-year consecutive structural supply deficit totalling hundreds of millions of ounces reflects the physical reality of a market where demand has systematically outpaced mine supply. Monthly options mechanics operate entirely above this foundation without touching it.

Monetary Demand and the Gold Displacement Dynamic

Industrial demand is not silver's only structural driver. Sustained central bank gold accumulation has maintained elevated gold prices, progressively reducing gold's accessibility for retail investors. As gold becomes prohibitively priced for many buyers, monetary-demand capital migrates toward silver as a functionally comparable but far more affordable monetary asset.

This displacement dynamic is not theoretical. It played out during the final phase of the 1980 bull market, when silver absorbed displaced monetary demand as gold's price exceeded the reach of retail participants. Examining silver vs gold performance across historical cycles reveals consistent patterns that support this thesis. The macro conditions producing this pattern in 2026, including elevated gold prices and intact monetary uncertainty, remain structurally present regardless of what happens on options expiration day.

Silver in 2026: Reading the Correction Correctly

From All-Time High to Current Levels

Silver reached an all-time high of $121.62 per ounce in January 2026. As of July 2026, the metal trades at approximately $59 per ounce, representing a correction of roughly 51% from its peak.

Corrections of this magnitude following parabolic advances have historical precedent in silver's price history. The analytical question is not whether the correction is large, but whether it reflects a change in the underlying supply-demand thesis or whether it reflects profit-taking, paper-market mechanics, and macro repositioning.

The Silver Institute's five-year consecutive deficit data, record industrial demand at 680.5 million ounces in 2024, and persistent market backwardation in 2026 collectively suggest the structural thesis is intact. The paper-driven correction and the physical market reality are operating on different timescales with different drivers.

An additional data point of note: the spread between silver's current spot price and average all-in mining costs represents historically wide territory as of mid-2026. When the gap between silver's market price and its cost of production expands significantly, it tends to signal either a temporary mispricing or genuine margin compression at the mine level, neither of which alters the demand-side equation. In addition, gold-silver ratio analysis at current levels also suggests silver remains historically undervalued relative to gold, which reinforces the broader structural case.

The next major ASX story will hit our subscribers first

A Decision Framework for Investors: Reading Expiration-Driven Drops

The Diagnostic Checklist

When silver drops near month-end, the following five-step process provides a structured framework for evaluating whether the move is paper-market noise or a genuine fundamental signal:

- Check the calendar: Is the drop occurring within five trading days of COMEX options expiration?

- Check the news: Is there a macro catalyst such as a Federal Reserve decision, CPI print, or geopolitical event that independently explains the move?

- Check physical premiums: Are physical silver dealers raising premiums or reporting supply tightness? If premiums are stable, the physical market is unaffected.

- Check the recovery pattern: Did silver recover within one to three days after expiration? Rapid recovery is a characteristic signature of paper-market events.

- Check the structural thesis: Have industrial demand forecasts, mine supply data, or deficit projections materially changed? If not, the investment case is unchanged.

Why Retail Investors Systematically Misread These Events

The behavioural pattern that expiration mechanics exploit is consistent: investors accumulate during pre-expiration price advances and liquidate during expiration-driven pullbacks, which is precisely the opposite of optimal positioning. Without understanding the paper-market mechanism, a 5–10% decline over 48 hours appears to signal fundamental deterioration.

This dynamic functions as a form of bull market attrition. The price window created by expiration mechanics may last anywhere from three minutes to three days. Retail execution speed rarely permits profitable trading around this window. Consequently, the practical implication is that attempting to trade the expiration cycle is less productive than understanding it well enough to ignore it.

Structuring Silver Exposure for Monthly Volatility

A rational framework for constructing silver positions that withstand monthly paper-market pressure includes:

- Allocating to physical silver held outside the financial system, which is structurally unaffected by paper-market settlement mechanics

- Avoiding leverage in silver positions that require precise timing around expiration cycles

- Treating expiration-driven pullbacks as potential accumulation windows rather than exit signals when the structural thesis is unchanged

- Sizing positions relative to the multi-year supply-demand thesis rather than reacting to monthly price action

Investors seeking real-time data can monitor live silver futures pricing to track how spot prices behave relative to expiration windows.

Key Data Summary: Silver's Structural Position in 2026

| Metric | Data Point | Source |

|---|---|---|

| Silver industrial demand (2024) | 680.5 million ounces (record) | Silver Institute, World Silver Survey 2025 |

| Industrial demand as % of total demand | ~61% | Silver Institute / World Gold Council |

| Industrial demand share ~25 years ago | ~35% | Silver Institute |

| Global mine production (2024) | ~820 million ounces | Silver Institute, World Silver Survey 2025 |

| Total silver demand (2024) | ~1,160 million ounces | Silver Institute, World Silver Survey 2025 |

| Structural deficit (2024) | 148.9 million ounces | Silver Institute, World Silver Survey 2025 |

| Consecutive deficit years (through 2025) | 5 years | Silver Institute, World Silver Survey 2026 |

| COMEX physical inventory coverage | ~14% of futures | Market data, July 2026 |

| Silver all-time high | $121.62/oz (January 2026) | Market data |

| Silver spot price (July 2026) | ~$59/oz | Market data |

| Next COMEX silver futures expiration | July 29, 2026 | COMEX exchange calendar |

Frequently Asked Questions: Silver Options Expiration and Price Behaviour

Why does silver's price often fall in the final week of the month?

Silver frequently declines in the days preceding COMEX options expiration because professional traders who have written call options use futures contracts to push the price below profitable strike levels through a process called delta hedging. Algorithms execute these trades automatically when specific price thresholds are reached. The effect is calendar-driven rather than fundamentally motivated, and it typically reverses within hours to days after expiration passes.

What is the difference between delta hedging and market manipulation in silver?

Delta hedging is a legal, mathematically driven risk management practice used by options market makers and institutional traders. Market manipulation, such as spoofing through placing and cancelling large orders to create false price signals, is illegal and subject to enforcement by the Commodity Futures Trading Commission. Both can produce downward price pressure near expiration, but they operate through different mechanisms and carry entirely different legal and regulatory implications.

Does the silver options expiration price drop affect physical silver buyers?

The primary effect is on the quoted spot price, which is derived from COMEX paper-market settlement. Physical silver dealers do not sell at momentary paper-market lows. Physical premiums and dealer pricing reflect real-world supply and demand conditions, not intraday futures fluctuations. Long-term physical holders observe the quoted price movement but remain structurally unaffected by the underlying paper-market mechanics driving it.

Can the long-term silver price trend be controlled through paper-market selling?

No. Paper-market mechanics, including delta hedging, gamma pressure, and margin-driven liquidations, can shift silver's price within a short-term window. However, they cannot override the multi-year supply-demand fundamentals that drive the long-term price trend. With five consecutive years of structural supply deficit and record industrial demand at 680.5 million ounces in 2024, the long-term price trajectory reflects physical market realities that paper-market activity cannot permanently suppress.

What is gamma risk and why does it matter for silver near expiration?

Gamma measures how rapidly an option's delta changes as the underlying price moves. When large silver options positions approach expiration near a dominant strike price, gamma becomes very large, meaning even small price movements trigger proportionally large and rapid hedging responses. In silver, where the options market is large relative to physical trading volume, gamma effects can produce sudden price swings that appear alarming but are entirely driven by derivatives mathematics rather than changes in physical supply or demand.

What should a long-term silver investor do when silver drops near month-end?

Apply the diagnostic checklist above: verify whether the drop is calendar-coincident with options expiration, check whether physical premiums have moved, and assess whether the structural supply-demand thesis has changed. If the fundamentals are unchanged, the appropriate response is typically inaction, or for investors with available capital, treating the pullback as a potential accumulation opportunity within a multi-year structural thesis. The silver options expiration price drop is a recurring feature of the market's architecture, and recognising it as such is itself a meaningful form of risk management.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any financial instrument. All investments carry risk, including the possible loss of principal. Past performance is not indicative of future results. Always consult a qualified financial adviser before making investment decisions. Data and market conditions referenced reflect information available as of July 2026.

Want to Identify the Next Major ASX Silver Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through the noise of paper-market volatility to surface actionable opportunities the moment they're announced. Explore historic discoveries and their returns to understand the potential, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.