July 10, 2026

The Three-Force Problem Driving Silver's Most Complex Pricing Environment in Years

Commodity markets tend to reward simplicity. A supply shock, a demand surge, a currency debasement cycle — most major moves in raw materials trace back to a single dominant force that investors can model and position around. Silver in May 2026 offers none of that comfort. What makes the current silver price forecast in May so analytically demanding is not that the data is absent — it is that three powerful and partially contradictory forces are simultaneously active, each with genuine historical precedent, each pulling prices in a different direction at the same time.

Understanding which force is dominant on any given week is the real work. Reacting to the loudest headline is the trap.

When big ASX news breaks, our subscribers know first

Why Silver Is the Most Conflicted Asset in the 2026 Commodity Complex

Three Competing Forces Pulling Silver in Opposite Directions

Silver's pricing complexity in May 2026 stems from three structural forces that rarely converge simultaneously.

The first is an industrial repricing catalyst: the US-China 90-day tariff reduction announced on May 10-11, 2026. For a metal that derives roughly half its annual demand from manufacturing applications — solar panels, electric vehicles, semiconductors, and medical devices — any meaningful improvement in global trade conditions directly reprices forward demand expectations. Furthermore, the market responded instantly, with silver surging 6% in a single session on May 11. Understanding the trade war impact on silver is consequently essential for any serious market participant.

The second is a monetary headwind. April 2026 CPI came in at 3.8%, above the 3.7% forecast and the highest reading since May 2023 (U.S. Bureau of Labor Statistics). Within hours of that release on May 13, the probability of a June Federal Reserve rate cut collapsed from approximately 48% to under 8% according to the CME FedWatch Tool. Markets rapidly shifted their first-cut expectations to September at the earliest, with significant probability weight falling on November or December.

The third force is a structural supply floor: six consecutive years of physical silver supply deficits with no credible near-term resolution. This is not a sentiment variable. It is a physical market reality driven by irreplaceable industrial consumption and the fundamental inability of mine supply to respond to price signals.

How Silver's Dual Identity Creates Forecast Divergence

Silver's dual role as both a monetary safe-haven and an industrial commodity creates a unique position in the commodity complex, because its price behaviour shifts depending on which macro environment is dominant:

- When fear drives markets, silver trades as a monetary safe-haven, moving in tandem with or even ahead of gold

- When manufacturing sentiment improves, silver reprices as an industrial commodity with similarities to copper

- In monetary easing environments, silver historically amplifies gold's directional moves by 2-3 times the percentage, functioning as a leveraged monetary asset

- When all three modes are simultaneously active — as in May 2026 — forecast ranges across institutional desks widen dramatically

Critical Framework: Any silver price forecast in May built entirely on a single analytical thesis — purely monetary, purely industrial, or purely speculative — is structurally incomplete. The analytical challenge is not identifying which thesis is correct in isolation. It is identifying which force holds dominant pricing power at each stage of the cycle.

Where Does Silver Actually Stand in May 2026? A Price History Snapshot

From All-Time High to Consolidation: The 2026 Price Arc

To build a credible silver price forecast for May 2026, understanding where the metal has been over the prior four months is essential. The price arc tells a story of extraordinary peak euphoria, a significant correction, and a tentative new equilibrium being tested in real time.

Silver reached a confirmed all-time high of $121.64 per ounce on January 29, 2026 (nFusion Solutions live spot price data). The move incorporated maximum optimism around the 2025 Federal Reserve easing cycle, amplified by accumulating physical supply deficit narratives and speculative inflows. February and March delivered a sustained retracement, with prices consolidating in the $70-$80 per ounce range through April — a correction of approximately 42-43% from peak.

The week of May 10-14 compressed months of complex analysis into four trading sessions:

- May 11: US-China 90-day tariff reduction announced; silver surges 6% in a single session, briefly clearing $87/oz

- May 13: April CPI prints at 3.8%, above forecast; silver retreats to approximately $84/oz

- Mid-May 2026: Silver sits roughly 31% below its January all-time high, but remains approximately 2.1 times its 2025 average of roughly $40/oz

Key Price Levels to Watch in May 2026

| Price Level | Significance |

|---|---|

| $121.64 | January 29, 2026 all-time high |

| $87-$88 | Post-tariff truce intraday peak (May 11-13) |

| $84 | Current mid-May 2026 trading level |

| $78-$80 | UBS year-end target / ING full-year average |

| $70-$80 | April 2026 consolidation range |

| ~$40 | Approximate 2025 full-year average |

The $84 level carries particular analytical weight. It already exceeds the full-year 2026 averages forecast by J.P. Morgan, ING, and the Reuters 30-analyst median — meaning either institutional targets require upward revision through mid-year, or the current price level implies a softening path before any next leg higher begins. You can track silver prices in real time to monitor how these key levels hold under evolving macro conditions.

What Is the Gold/Silver Ratio Signalling for Silver Right Now?

Decoding the Ratio's Fastest Compression in Years

The gold/silver ratio is one of the most underused tools in precious metals analysis — and in May 2026, it is carrying an unusually clear signal. Conducting a thorough gold/silver ratio analysis is consequently one of the most productive analytical exercises available to investors navigating the current environment.

Entering May 2026, the ratio stood at approximately 62:1. Following the tariff truce announcement on May 10-11, it compressed to below 55:1 within a single week. As of May 14, it sits at approximately 55.25:1. The analytically significant detail is that gold barely moved during this compression period. Silver drove the entire repricing — confirming that the tariff news was pricing an industrial demand recovery narrative, not a monetary safe-haven flow.

This distinction matters enormously for forecasting. If gold had also surged, the ratio compression would merely reflect parallel safe-haven buying. The fact that silver outperformed gold in isolation identifies the specific thesis the market was pricing: improved manufacturing demand from trade normalisation.

Historical Ratio Benchmarks for Context

| Market Condition | Gold/Silver Ratio |

|---|---|

| 2011 silver bull market peak | ~31:1 |

| COVID-19 crash (March 2020) | ~125:1 (extreme undervaluation) |

| 20th century long-run average | ~47:1 |

| Post-2000 modern average | ~60-65:1 |

| Late 2025 levels | ~80:1 |

| Mid-May 2026 | ~55.25:1 |

At 55:1, silver sits below the modern post-2000 average, indicating it has already undergone meaningful repricing from the 80:1 levels seen in late 2025. However, the 2011 bull market compression to 31:1 demonstrates how much further the ratio can move during confirmed bull phases.

What Ratio Direction Tells Investors About Silver's Next Move

The ratio's near-term trajectory depends on two scheduled events:

- The outcome of ongoing US-China trade negotiations, including the Trump-Xi summit, which will determine whether the 90-day tariff truce holds or breaks down

- The June 16-17 FOMC meeting and its accompanying dot plot — the Fed's first updated interest rate projection since March 2026

A sustained move below 50:1 would historically signal silver entering confirmed outperformance mode, consistent with prior bull market leadership phases. A reversal above 62:1 would indicate the tariff-driven industrial repricing narrative is unwinding.

What Are Major Institutional Banks Forecasting for Silver in 2026?

The Widest Forecast Spread Seen for Any Major Commodity

The divergence between institutional silver forecasts in 2026 is not merely wide — it is historically unprecedented for any major commodity. That spread itself carries analytical information: it reflects genuine fundamental uncertainty about which of silver's three pricing forces will prove dominant through the remainder of the year.

| Institution | 2026 Silver Price Forecast | Key Rationale |

|---|---|---|

| Bank of America | $135-$309 (scenario range) | Ratio compression modelling — not a base case |

| Citigroup | $110 (H2 2026 target) | Acute physical supply shortages |

| Goldman Sachs | $85-$100 (full-year average) | Green energy transition demand |

| J.P. Morgan | ~$81/oz (full-year average) | Post-2025 rally normalisation |

| Reuters 30-analyst median | ~$79.50 | Consensus central tendency |

| ING | ~$78 (full-year average) | Conservative demand outlook |

| UBS | $80 (year-end target, revised down) | Demand destruction at elevated prices |

| Coincodex algorithm | ~$159.77 (year-end) | Quantitative momentum modelling |

Sources: J.P. Morgan Global Research; Goldman Sachs commodity research; Citigroup Global Markets; Bank of America Global Research; Reuters 30-analyst survey, 2026; ING commodity research; UBS commodity research.

Critical Observation: With silver trading at approximately $84/oz in mid-May 2026, it already sits above the J.P. Morgan full-year average ($81), the Reuters consensus median ($79.50), and the ING projection ($78). The most actionable signal to monitor is not any individual price target — it is the direction of institutional revisions through mid-year. Upgrades from major desks are structurally bullish. Downgrades would represent genuine near-term headwinds.

It is also worth noting that HSBC has raised its silver price targets for 2026 and 2027, though the bank sees limited upside from current levels — a cautious but constructive stance that broadly aligns with the UBS and J.P. Morgan positioning.

Short-Term Algorithmic Forecasts for May 2026

Quantitative momentum models offer a different analytical angle from institutional bank research:

- Coincodex (updated May 14, 2026) projects silver rising to approximately $95.94 by May 20 — representing an 11-13% move from mid-May levels

- The same model's one-month outlook targets approximately $103.91 by mid-June 2026

- The projected May 2026 average from this model falls in the $88-$91/oz range, with a minimum of approximately $84.56 and a maximum near $96.17

Algorithmic forecasts of this nature deserve contextual caution. They are built on momentum and historical pattern recognition, not fundamental supply-demand modelling. In an environment where monetary policy decisions can collapse price by 5% in a single session, quantitative models face structural limitations. They are best understood as measuring market momentum rather than forecasting fundamental value.

Why Is Silver's Physical Supply Deficit the Structural Foundation of the Bullish Case?

Six Years of Consecutive Shortfalls: The Numbers Behind the Thesis

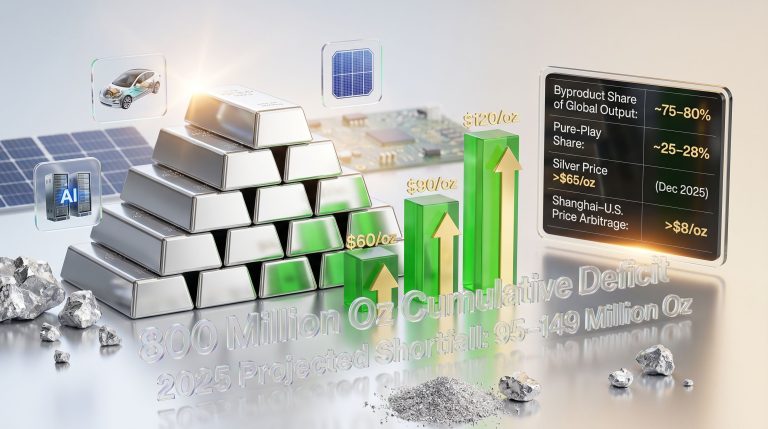

Beneath the week-to-week volatility generated by tariff announcements and inflation prints lies a physical market reality that does not reset between news cycles. The silver market is entering its sixth consecutive year of supply deficit — a streak with no modern precedent for a commodity with this level of industrial irreplaceability.

Key figures from the Silver Institute's World Silver Survey 2026:

- 2026 projected annual deficit: approximately 46 million ounces

- Cumulative drawdowns from above-ground stocks since 2021: nearly 762 million ounces — equivalent to roughly nine months of total global mine output

- COMEX registered inventories: fallen from an October 2025 peak of 531 million ounces to approximately 315 million ounces by mid-May 2026

- US physical outflows: approximately 95 million ounces left the United States in just the first two months of 2026 alone

Why Mine Supply Cannot Simply Respond to Higher Prices

This is perhaps the least understood structural feature of the silver market among non-specialist investors. Unlike most commodities, where elevated prices incentivise new supply within one to three years, silver's mine supply operates under fundamentally different constraints:

- Global annual mine production: approximately 813 million ounces in 2025, edging toward 820 million ounces in 2026

- Approximately 70% of silver is extracted as a byproduct of gold, copper, and zinc mining — meaning silver supply cannot be independently ramped up in response to silver-specific price signals

- Average lead time from discovery to production for a new dedicated silver mine: more than eight years

- When silver rallied approximately 147% during 2025, new dedicated silver mines did not materialise — and they will not within any timeframe relevant to current market positioning

Supply Constraint Reality Check: The critical distinction between silver and gold lies in consumption. Above-ground gold stocks are estimated to dwarf annual mine output, and gold is essentially never permanently consumed — it cycles through jewellery, investment, and central bank holdings. Silver is permanently consumed in industrial applications. The silver used in a solar panel, an EV battery management system, or a semiconductor wafer does not re-enter the market. This consumption dynamic is structurally distinct from gold and is the primary mechanism enabling consecutive multi-year deficits.

Where the Demand Headwinds Are Real: An Honest Assessment

A credible silver price forecast in May must acknowledge the genuine demand-side challenges alongside the supply deficit thesis:

- Photovoltaic thrifting: Solar manufacturers are systematically reducing silver content per panel through metallisation paste optimisation and cell architecture improvements. PV sector silver demand is projected to decline approximately 19% year-on-year in 2026 (PV Magazine / Metals Focus, World Silver Survey 2026)

- Jewellery consumption: Down approximately 9% in 2026

- Silverware demand: Down approximately 17% in 2026

However, silver's electrical conductivity — the highest of any element — has no cost-effective industrial substitute at scale. The expansion of EV production globally, AI data centre infrastructure buildout, and 5G network deployment are collectively introducing new demand vectors that current thrifting trajectories cannot fully offset over a medium-term horizon.

The next major ASX story will hit our subscribers first

How Does Federal Reserve Policy Shape the Silver Price Forecast in May 2026?

The Real Yield Transmission Mechanism: How Rates Move Silver

The relationship between Federal Reserve policy and silver prices operates through a specific and well-documented transmission mechanism. Understanding this chain is essential for interpreting every monetary policy development that surfaces between now and year-end:

- The Federal Reserve reduces its benchmark rate, compressing nominal yields across the curve

- As nominal yields fall and inflation expectations remain anchored, real yields (nominal yields minus inflation expectations) compress

- Compressed real yields reduce the opportunity cost of holding non-yielding assets, including precious metals

- Silver, functioning as a leveraged monetary metal with significant industrial demand underpinning, amplifies gold's response to this compression by 2-3 times

- Conversely, when the easing cycle pauses or reverses, silver consolidates — sometimes sharply and rapidly

The Fed Rate Cycle and Silver's Historical Response

| Easing Cycle | Silver Price at Start | Silver Price at Peak | Approximate Gain |

|---|---|---|---|

| 2019-2020 easing | ~$14/oz | ~$29/oz | ~107% |

| 2025 easing cycle | ~$29/oz | $121.64/oz (Jan 2026) | ~319% |

The pattern is consistent: each time the Federal Reserve moved into meaningful easing, silver amplified gold's directional move by a factor of two to three. Each time the Fed paused, silver consolidated. The April 2026 CPI print consequently extended the pause, reinforcing the importance of monitoring both gold and silver markets together for a complete macro picture.

May 2026 Fed Outlook: What the CPI Print Changed

The Federal Reserve has held its target range at 3.50-3.75% across three consecutive meetings, following the rate cuts delivered through 2025 (Federal Reserve, FOMC Press Release, April 29, 2026). The sequence of events following the April CPI release was rapid and consequential:

- Pre-May 13: CME FedWatch pricing approximately 48% probability of a June rate cut

- April CPI release (May 13): 3.8% headline, above the 3.7% forecast — the highest reading since May 2023

- Post-print: June cut probability collapses to under 8%; consensus shifts first-cut expectations to September at the earliest

The June 16-17 FOMC meeting is now the single most important near-term date on silver's calendar. It includes a dot plot — the Federal Reserve's first updated interest rate projection since March 2026. Incoming Fed Chair Kevin Warsh's documented hawkish stance on inflation introduces additional uncertainty around whether the dot plot will signal any 2026 cuts at all.

Two FOMC Scenarios and Their Silver Price Implications

Scenario A — Hawkish Dot Plot (no 2026 cuts signalled):

- Silver's consolidation phase extends through Q3 2026

- Price likely remains range-bound between $78-$88

- Gold/silver ratio may drift back toward 60-62:1

- Algorithmic momentum targets lose credibility as the monetary tailwind disappears

Scenario B — Dovish Signal (September easing indicated):

- Meaningful tailwind for silver's next directional leg

- Ratio compression toward 50:1 becomes a realistic near-term possibility

- Institutional targets from Citigroup ($110 H2) and Goldman Sachs ($85-$100 average) gain significantly more probability weight

- Algorithmic projections in the $95-$104 range become aligned with fundamental support

What Are the Key Risk Scenarios That Could Break Silver's Current Range?

Upside Catalysts: What Could Drive Silver Above $95 in May-June 2026

- A credible extension or formalisation of the US-China 90-day tariff truce beyond its current window, reducing the probability of renewed industrial demand disruption

- A dovish signal from the June 16-17 FOMC dot plot indicating the first rate cut arrives in September 2026

- Accelerated COMEX inventory drawdowns tightening physical availability further from the current 315 million ounce registered level

- Mid-year institutional forecast upgrades from J.P. Morgan or Goldman Sachs, which would signal that consensus has materially underestimated current demand conditions

- A sustained weakening of the US dollar index, which historically provides a secondary tailwind for dollar-denominated commodity prices

Downside Risks: What Could Push Silver Back Below $78

- A breakdown in US-China trade negotiations following the 90-day window, reversing the industrial demand repricing that drove the May 11 surge

- A June 17 FOMC dot plot removing all 2026 rate cuts from consensus projections, extending the monetary headwind through year-end

- Persistently sticky inflation through Q3 keeping real yields elevated and suppressing the amplification mechanism

- Accelerated solar thrifting reducing PV demand beyond the projected 19% decline, undermining the green energy demand narrative

Bear Case Framing: The downside scenario for silver in May 2026 is near-term and event-specific — it is not a structural argument against the metal's fundamental positioning. A trade breakdown combined with a hawkish FOMC would extend the consolidation range. Neither outcome invalidates six years of physical deficits, the irreplaceable industrial demand profile, or the monetary debasement thesis that drove silver from $29 to $121 in the 2025 easing cycle.

How Does Silver Compare to Gold as an Investment in the Current Environment?

The Amplification Relationship: Silver's Beta to Gold

Understanding silver's relationship to gold is not merely academic — it is the most practical framework available for projecting silver's directional path in the second half of 2026. Gold is trading near $4,694/oz as of mid-May 2026, approximately 16% below its January 2026 all-time high. J.P. Morgan forecasts gold at $5,000/oz by year-end 2026 (J.P. Morgan Global Research).

Running ratio-compression scenarios against that gold target produces the following implied silver price outcomes:

- If gold reaches $5,000 and the gold/silver ratio holds at the current 55:1, implied silver price: approximately $90.90/oz

- If gold reaches $5,000 and the ratio compresses to 50:1, implied silver price: approximately $100/oz

- If gold reaches $5,000 and the ratio compresses to 45:1 — consistent with historical bull market phases — implied silver price approaches $111/oz

- If gold reaches $5,000 and the ratio reaches the 2011 bull market peak of 31:1, the theoretical implied silver price exceeds $161/oz

These are scenario projections, not forecasts. They are presented to illustrate the mathematical sensitivity of silver's price to ratio compression combined with gold's directional move. Past performance does not guarantee future results, and all precious metals investments carry risk of partial or total loss.

Silver vs. Gold: Role Differentiation for Portfolio Construction

| Characteristic | Gold | Silver |

|---|---|---|

| Primary portfolio role | Stabiliser / monetary hedge | Amplifier / industrial commodity |

| Volatility profile | Lower | 2-3x higher than gold |

| Industrial consumption | Minimal | ~50% of annual demand |

| Supply response to price | More flexible | Constrained (70% byproduct) |

| Ratio to gold (May 2026) | — | ~55:1 |

| Sensitivity to rate cuts | Moderate | High (leveraged response) |

| Above-ground stock depth | Deep | Shallow relative to consumption |

A less commonly understood feature of silver's supply profile is the byproduct dynamic's sensitivity to base metal cycles. When copper markets soften and major copper miners reduce output — as occurred during parts of 2015-2016 and again briefly in 2020 — silver byproduct output falls independently of silver's own price. This creates asymmetric supply responses: silver supply can fall even when silver prices are rising, if the primary metals being co-mined experience demand weakness. This dynamic reinforces the deficit persistence thesis and is one reason institutional analysts treat silver's supply constraint as more durable than a simple price signal analysis would suggest.

Frequently Asked Questions: Silver Price Forecast in May 2026

What is the silver price forecast for May 2026?

Institutional forecasts for the silver price forecast in May span an unusually wide range. J.P. Morgan's full-year 2026 average sits at approximately $81/oz, the Reuters 30-analyst median at $79.50, and ING at $78 — all below where silver currently trades at approximately $84/oz. On the high end, Citigroup targets $110 for the second half of 2026, while Bank of America has modelled a scenario range of $135-$309 based on ratio compression. Short-term algorithmic models project silver reaching $95-$104 by mid-June. With silver already above most consensus targets, the key variable to monitor is the direction of mid-year institutional forecast revisions.

Why did silver surge 6% on May 11, 2026?

The May 11 surge was directly triggered by the announcement of a 90-day US-China tariff reduction. Silver has significant industrial applications in solar energy, electric vehicles, and electronics manufacturing, meaning any improvement in global trade conditions rapidly reprices forward industrial demand expectations. The gold/silver ratio's compression from approximately 62:1 to below 55:1 during the same period confirmed the move was driven by industrial demand sentiment rather than safe-haven monetary flows.

What is the gold/silver ratio and why does it matter for silver investors?

The gold/silver ratio measures how many ounces of silver are required to purchase one ounce of gold. At approximately 55.25:1 in mid-May 2026, silver sits below the modern post-2000 average of 60-65:1, suggesting it has already partially repriced from the approximately 80:1 levels seen in late 2025. Historically, ratio compression below 50:1 has signalled silver entering confirmed outperformance phases. A reversal back above 62:1 would indicate weakening industrial demand sentiment and potentially extending the current consolidation range.

How does the Federal Reserve's June 2026 meeting affect silver prices?

The June 16-17 FOMC meeting is the most consequential near-term event for the silver price forecast in May 2026 and its trajectory through mid-year. Following the hot April CPI print of 3.8%, the probability of a June rate cut has collapsed from approximately 48% to under 8%. A hawkish dot plot removing 2026 cuts from the projection would extend silver's consolidation into Q3. In addition, any signal of September easing would provide meaningful upside momentum. Silver's historical sensitivity to rate cycles — amplifying gold's response by 2-3 times — makes FOMC communications a primary price driver in the current environment.

Is the silver supply deficit real, and how long can it persist?

The Silver Institute's World Silver Survey 2026 projects a sixth consecutive annual supply deficit of approximately 46 million ounces in 2026, with cumulative drawdowns since 2021 reaching nearly 762 million ounces. Because approximately 70% of silver is mined as a byproduct of other metals, supply cannot respond independently to price signals — and the average lead time from discovery to production exceeds eight years. The deficit is structurally persistent unless a sustained collapse in industrial demand occurs, which current EV expansion, AI infrastructure buildout, and 5G network deployment trends make unlikely over any medium-term horizon.

What is the biggest risk to silver's price in May-June 2026?

The two most immediate risks are a breakdown in US-China trade negotiations following the 90-day truce window, and a June 17 FOMC dot plot signalling no rate cuts through the end of 2026. Either outcome alone would extend silver's consolidation. Both occurring simultaneously would represent a meaningful near-term headwind. However, neither would structurally alter the physical supply deficit thesis, the irreplaceable industrial demand profile, or the monetary debasement case that underpins long-term positioning in silver.

This article is for informational and educational purposes only. It does not constitute investment advice or a solicitation to buy or sell any asset. Precious metals investments carry risk of partial or total loss. All forecasts, price targets, and scenario projections cited represent third-party institutional research and algorithmic models, not guaranteed outcomes. Past performance does not guarantee future results. Please consult a qualified financial adviser before making any investment decisions.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While silver's multi-force pricing environment demands careful macro analysis, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries — including silver and other commodities — are announced on the ASX, translating complex data into actionable insights for investors at every level. Explore how historic ASX mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.