June 20, 2026

Silver prices have surged dramatically throughout 2025, fundamentally reshaping cost structures and material strategies across the photovoltaic industry. This unprecedented silver market squeeze has forced manufacturers to accelerate development of alternative metallisation approaches whilst maintaining the electrical performance standards required for 25-year operational lifespans. Understanding these technical mechanisms reveals why silver in solar manufacturing remains challenging to replace despite significant economic pressures.

Furthermore, the electrical conductivity hierarchy places silver at 63.0 × 10^6 S/m compared to copper's 59.6 × 10^6 S/m, representing approximately a 6% performance advantage in pure conductivity terms. However, this measurement alone understates silver's technical superiority in photovoltaic applications, where temperature resistance, oxidation prevention, and contact formation reliability become critical factors.

Screen printing processes for creating electron collection grids require paste formulations combining metal particles, glass frit, and organic binders that must withstand firing temperatures exceeding 850°C while maintaining electrical continuity. Consequently, silver's unique metallurgical properties enable reliable contact formation under these extreme processing conditions, whereas copper-based alternatives introduce assembly complexities and long-term reliability concerns.

Current Solar Technology Silver Requirements by Architecture Type

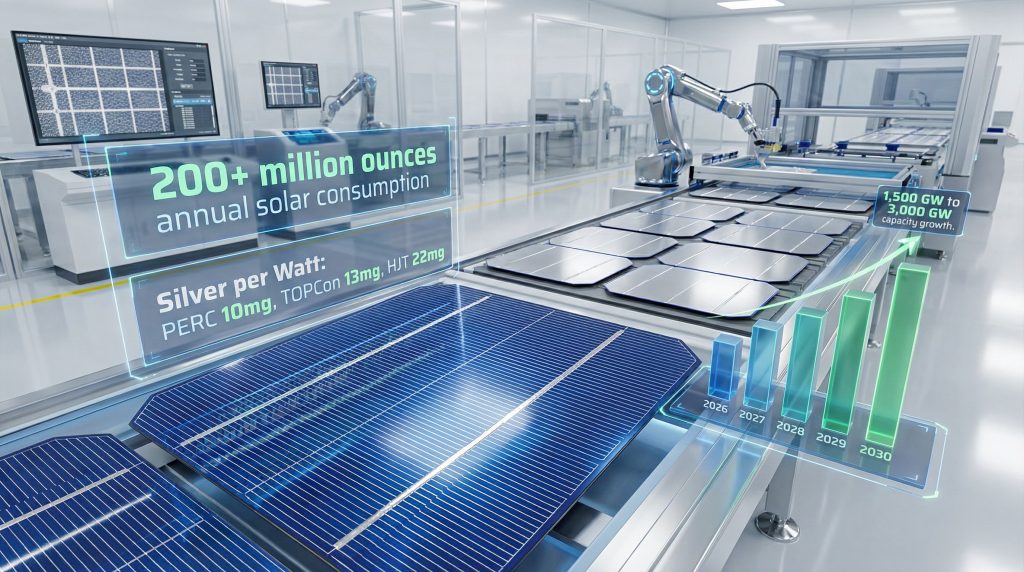

Different photovoltaic cell architectures demonstrate varying silver consumption patterns based on their electrical design requirements and manufacturing processes. These variations directly impact global silver in solar manufacturing demand projections and substitution feasibility across different efficiency segments.

| Technology | Silver per Watt (mg) | Efficiency Range | Market Share 2026 | Processing Temperature |

|---|---|---|---|---|

| PERC | 10 | 20-22% | 45% | 850-900°C |

| TOPCon | 13 | 22-24% | 35% | 900-950°C |

| HJT | 22 | 24-26% | 15% | 150-200°C |

| IBC | 25 | 25-27% | 5% | 800-850°C |

Passivated Emitter and Rear Cell (PERC) technology represents the current mainstream approach, consuming approximately 10 milligrams of silver per watt while achieving 20-22% conversion efficiency. This architecture uses conventional screen printing for front-side metallisation, making it relatively compatible with silver reduction techniques such as fine-line printing and multi-busbar designs.

Tunnel Oxide Passivated Contact (TOPCon) cells require 13 milligrams per watt due to their advanced contact architecture, which demands precise metallisation over passivated surfaces. The technology's high-temperature fabrication processes above 900°C create thermal budget constraints that limit copper substitution effectiveness, as alternative metals may compromise the critical passivation layer integrity.

Heterojunction Technology (HJT) demonstrates the highest silver intensity at 22 milligrams per watt, representing 120% higher consumption than PERC cells. This premium reflects HJT's low-temperature processing requirements below 200°C, which prevent the high-temperature sintering that enables copper-based metallisation in other architectures.

When big ASX news breaks, our subscribers know first

Manufacturing Process Innovations Reducing Silver Consumption

Solar manufacturers have implemented multiple technological approaches to reduce silver consumption whilst maintaining electrical performance standards. These innovations address both material cost pressures and supply security concerns affecting silver in solar manufacturing economics, particularly as established critical raw materials facility initiatives struggle to meet growing demand.

Fine-Line Printing Technology Advances

Advanced screen printing equipment enables finger width reduction from traditional 100-150 micrometers to 50-75 micrometers, achieving 15-20% silver savings through reduced cross-sectional area. However, this approach requires significant equipment precision upgrades and presents yield challenges from increased breakage rates during handling and assembly processes.

Manufacturing facilities implementing fine-line printing typically experience initial yield reductions of 3-5% during the transition period, requiring careful process optimisation to maintain economic viability. The technique works most effectively with PERC and TOPCon architectures but shows limited applicability for HJT cells due to their unique contact formation requirements.

Copper Electroplating Over Silver Seed Layers

The most promising substitution approach involves depositing thin silver seed layers of 2-5 micrometers followed by copper electroplating to achieve required conductivity levels. This method can reduce silver consumption by 60-80% whilst maintaining electrical performance comparable to full silver metallisation.

Chinese manufacturers including Longi Green Energy Technology, Jinko Solar, and Shanghai Aiko Solar Energy have announced commercial implementation timelines for Q2 2026. Early production data indicates successful technical feasibility but reveals increased assembly costs and reliability concerns requiring extended field testing validation.

Multi-Busbar Design Optimisation Strategies

Traditional solar cell designs utilise 2-3 busbars for current collection, while advanced multi-busbar configurations employ 9-12 parallel conductors to reduce current path lengths and ohmic losses. This approach enables 10-15% silver reduction through optimised current distribution without compromising electrical performance.

Implementation complexity increases at the module assembly level, requiring specialised soldering equipment and modified interconnection procedures. However, the relatively low capital requirements make multi-busbar adoption attractive for manufacturers seeking immediate silver savings without major production line modifications.

Regional Manufacturing Responses to Silver Price Volatility

Geographic manufacturing concentration creates distinct regional approaches to managing silver in solar manufacturing cost pressures. Chinese producers, controlling approximately 80% of global solar cell production, demonstrate more aggressive substitution timelines compared to manufacturers in other regions, particularly as copper price trends influence alternative metallisation economics.

Asia-Pacific Manufacturing Strategy

Asian manufacturers benefit from vertical integration advantages, controlling both solar cell production and silver paste supply chains. This integration enables coordinated material substitution programmes and risk management strategies not available to Western competitors relying on imported materials.

Silver paste formulation optimisation programmes in China target paste utilisation efficiency improvements of 5-10% through better rheological properties and printing parameters. These incremental gains complement more dramatic substitution efforts, providing immediate cost relief whilst longer-term copper integration projects mature.

European Manufacturing Adaptation

European producers focus on high-efficiency, premium solar applications where silver's performance advantages justify higher material costs. Companies like Meyer Burger and Oxford PV maintain silver-intensive processes for heterojunction and perovskite-silicon tandem technologies targeting efficiency levels above 26%.

This strategy accepts higher material costs in exchange for premium pricing capabilities and reduced competition from lower-cost Asian alternatives. The approach works particularly well for specialised applications such as space-grade cells and concentrated photovoltaic systems where efficiency takes precedence over cost considerations.

Supply Chain Risk Management and Strategic Material Procurement

Solar manufacturers employ sophisticated procurement strategies to manage silver price volatility and supply security concerns. These approaches include long-term contracts, inventory optimisation, and vertical integration considerations that influence silver in solar manufacturing demand patterns, particularly as manufacturers develop silver pricing strategies to navigate current market conditions.

Contract Pricing Mechanisms

Major solar manufacturers typically secure 6-12 month forward contracts for silver paste procurement, providing price stability during production planning cycles. Some industry leaders extend contracts to 24-36 months when market conditions favour buyers, though such long-term commitments require careful demand forecasting and inventory management.

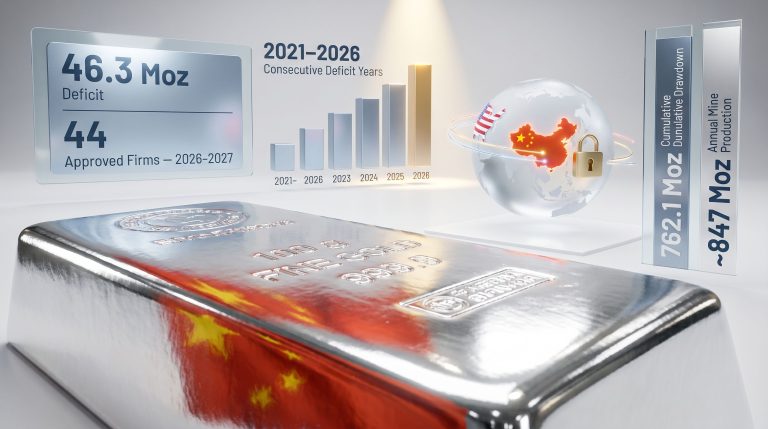

Tier-1 manufacturers often negotiate volume-based pricing that reduces per-unit costs by 8-15% compared to spot market purchases. These savings partially offset silver's increasing proportion of total module costs, which has risen from 3% in 2023 to an estimated 17-29% in 2026.

Inventory Management Strategies

Optimal silver inventory levels balance carrying costs against price volatility exposure. Industry analysis suggests most manufacturers maintain 30-45 days of silver paste inventory under normal market conditions, increasing to 60-90 days during periods of high price volatility or supply uncertainty.

Advanced inventory management systems incorporate real-time price feeds and demand forecasting algorithms to optimise purchase timing and quantities. These systems have become essential tools for managing the dramatic cost structure changes affecting silver usage in manufacturing operations.

Performance Trade-offs in Silver Substitution Applications

Whilst cost pressures drive substitution efforts, technical performance trade-offs require careful evaluation across different solar applications. Understanding these compromises helps explain why complete silver elimination remains challenging despite successful partial substitution demonstrations, particularly in applications requiring energy transition security.

Electrical Performance Degradation Analysis

Copper-based metallisation typically introduces 0.1-0.3% absolute efficiency losses compared to equivalent silver designs. Whilst seemingly modest, this degradation translates to 2-6% relative performance reduction for high-efficiency cells operating near 24-26% conversion rates.

For utility-scale applications where levelised cost of electricity (LCOE) drives purchasing decisions, efficiency losses often outweigh material cost savings. Detailed economic modelling indicates that copper substitution becomes cost-effective only when silver prices exceed $85-95 per ounce for most commercial applications.

Long-term Reliability Considerations

Silver's superior oxidation resistance provides critical advantages in outdoor environments where solar panels operate for 25-30 year service lives. Copper-based contacts show increased susceptibility to corrosion and electromigration effects that can reduce long-term power output and panel lifetime.

Field testing data from early copper implementation projects indicates potential degradation rate increases of 0.05-0.10% annually compared to silver-based designs. While still within acceptable performance parameters, these differences significantly impact financial modelling for utility-scale installations.

Accelerated aging tests simulate 25-year outdoor exposure through temperature cycling, humidity exposure, and UV radiation protocols. Results consistently favour silver-based metallisation for applications requiring maximum durability, particularly in harsh environmental conditions such as desert installations or marine environments.

Economic Impact Analysis: Silver Costs Across Different Market Segments

The dramatic increase in silver's proportion of solar module costs affects different market segments unequally, creating distinct adoption patterns for substitution technologies. Understanding these segmented impacts provides insight into future silver in solar manufacturing demand evolution.

Residential Installation Market Dynamics

Residential solar installations typically prioritise system aesthetics, warranty coverage, and installer familiarity over marginal cost differences. This market segment shows slower adoption of silver-reduced technologies, maintaining preference for proven PERC and TOPCon architectures despite higher material costs.

Premium efficiency products command price premiums of $0.10-0.20 per watt in residential markets, often exceeding the incremental silver costs. This pricing dynamic reduces substitution pressure and supports continued silver usage in high-efficiency residential applications.

Utility-Scale Project Economics

Large-scale solar installations demonstrate much greater sensitivity to material costs, as efficiency optimisation and cost per watt minimisation directly impact project financing and returns. Utility buyers increasingly specify silver-reduced technologies when available, driving rapid adoption of substitution approaches.

Competitive bidding processes for utility-scale projects create strong incentives for manufacturers to implement silver reduction technologies quickly. Projects exceeding 100 MW capacity often justify custom manufacturing specifications that prioritise cost optimisation over technological conservatism.

The next major ASX story will hit our subscribers first

Future Technology Roadmap: 2027-2030 Silver Demand Projections

Long-term projections for silver in solar manufacturing must account for technology evolution, manufacturing scale effects, and substitution implementation timelines. These factors create complex demand scenarios requiring careful analysis of multiple variables and assumptions.

Technology Mix Evolution Scenarios

Current market share distributions will shift significantly as higher-efficiency technologies gain adoption whilst silver reduction techniques mature. Conservative projections suggest TOPCon market share will grow to 45-50% by 2028, while HJT adoption may reach 20-25% of global production.

| Year | PERC | TOPCon | HJT | IBC | Average Silver (mg/W) |

|---|---|---|---|---|---|

| 2026 | 45% | 35% | 15% | 5% | 13.5 |

| 2028 | 30% | 50% | 18% | 2% | 14.2 |

| 2030 | 15% | 55% | 25% | 5% | 15.8 |

Substitution implementation rates will significantly modify these baseline consumption figures. Aggressive adoption scenarios suggest 30-50% silver reduction across all technologies by 2030, while conservative estimates project 15-25% reduction due to technical and reliability constraints.

Global Manufacturing Capacity Distribution

Solar manufacturing capacity expansion will continue concentrating in Asia-Pacific regions, with China maintaining 75-80% of global production through 2030. This geographic concentration accelerates substitution implementation as Chinese manufacturers coordinate technology adoption across multiple production lines.

Regional manufacturing policies increasingly emphasise domestic content requirements and supply chain security. These policies may slow substitution adoption in some markets where silver sourcing provides strategic advantages over copper-based alternatives requiring different supply chains.

Supply-Demand Balance Projections

Even with aggressive substitution implementation, absolute silver demand from solar applications will likely continue growing due to capacity expansion rates exceeding efficiency gains. Conservative estimates project solar silver demand reaching 220-250 million ounces annually by 2030, compared to 194 million ounces in 2026.

Critical supply constraints emerge when total silver demand approaches 1.2-1.3 billion ounces annually, as primary mining production struggles to exceed 900-950 million ounces without significant new mine development. Recycling contributions of 250-300 million ounces provide partial supply augmentation but cannot fully address projected shortfalls.

Strategic Investment Implications for Solar Supply Chain Participants

The evolving relationship between silver costs and solar manufacturing creates distinct investment opportunities and risks across different supply chain participants. Understanding these dynamics helps identify sectors positioned to benefit from ongoing technological transitions.

Equipment Manufacturing Investment Themes

Companies producing screen printing equipment, electroplating systems, and metallisation paste preparation technology represent primary beneficiaries of industry substitution efforts. Investment in advanced manufacturing capabilities often generates 15-25% annual returns during technology transition periods.

Process automation technologies that improve silver paste utilisation efficiency command premium pricing and rapid adoption rates. Companies like Applied Materials, Centrotherm, and Schmid Group benefit from retrofitting existing production lines with silver-efficient capabilities.

Materials Supply Chain Positioning

Silver paste manufacturers face complex positioning decisions between defending existing market share and developing substitution technologies that reduce their addressable market size. Companies successfully navigating this transition often maintain market leadership through technological innovation.

Copper plating chemistry suppliers and alternative metallisation material developers represent emerging growth opportunities. Early-stage companies developing novel approaches to solar cell metallisation attract significant venture capital investment and strategic partnership interest from major manufacturers.

Conclusion: Balancing Technical Performance with Economic Reality

The future of silver in solar manufacturing reflects broader tensions between technological optimisation and economic sustainability within renewable energy supply chains. Whilst complete silver elimination remains technically challenging, ongoing innovations continue reducing consumption rates even as absolute demand grows with industry expansion.

Material substitution efforts will likely achieve 30-50% silver reduction per watt by 2030, though this progress occurs alongside capacity growth that maintains total demand above current levels. The industry's ability to manage these transitions whilst maintaining product quality and reliability standards will determine long-term supply chain stability. Additionally, innovations in recycling end-of-life solar panels may provide alternative silver sources to support future manufacturing requirements.

Investment opportunities exist across the technology transition spectrum, from equipment suppliers enabling substitution to materials companies developing next-generation metallisation approaches. Success requires careful evaluation of technical feasibility, implementation timelines, and market adoption patterns that vary significantly across different solar applications and geographic regions.

Please note: Projections regarding silver demand, technology adoption rates, and pricing scenarios involve inherent uncertainties and should not be considered investment recommendations. Market participants should conduct independent analysis appropriate to their specific circumstances and risk tolerance levels.

Looking to Capitalise on Critical Materials in the Solar Revolution?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including silver and copper projects driving the renewable energy transition. With silver demand from solar manufacturing projected to reach 250 million ounces annually by 2030, subscribers gain crucial market intelligence on emerging mining opportunities that could benefit from this unprecedented materials squeeze. Begin your 14-day free trial today to position yourself ahead of the supply chain transformation reshaping global energy markets.