May 20, 2026

The Mispricing Pattern Most Commodity Investors Repeat — And Why Silver May Be Next

Every major commodity repricing event in modern history has followed the same cognitive arc. Early adopters identify a structural mechanism. The broader market discounts it as speculative. Then confirmed engineering specifications, supply data, and corporate capital commitments converge simultaneously — and the repricing happens faster than most participants can react. The silver solid state battery thesis is currently sitting somewhere between the first and second stages of that arc.

Understanding why markets systematically misprice structural transitions matters more than simply knowing that they do. The answer lies in how analysts model demand. Conventional commodity valuation frameworks are built around current consumption rates with incremental adjustments. They struggle to incorporate step-change demand catalysts that have not yet produced volume shipments, even when the underlying engineering specifications have already been confirmed and production commitments have been signed.

Timeline uncertainty is consistently overweighted. Confirmed specifications are consistently underweighted.

Three historical parallels illuminate this pattern clearly:

- Lithium pre-2020: Priced as an industrial afterthought at roughly $6,000–$7,000 per metric ton before the EV transition was absorbed by valuation models. By late 2022, prices surpassed $82,000 per metric ton, driven by mass adoption commitments from Ford, GM, and European automakers (USGS Lithium Minerals Yearbook 2022). The lithium boom demonstrates precisely how violently markets can reprice when structural demand is finally absorbed into valuation models.

- Copper pre-renewable buildout: Undervalued relative to grid infrastructure requirements until the scale of the energy transition became undeniable to mainstream analysts.

- Uranium pre-nuclear renaissance: Structurally cheap through a decade of reactor construction approvals that the market treated as distant and uncertain.

In each case, the investment opportunity existed in the gap between what was already confirmed in technical specifications and what was still absent from price discovery. The silver solid state battery thesis occupies exactly that gap today.

When big ASX news breaks, our subscribers know first

Why Silver's Role Inside a Solid-State Cell Is Not Incidental

The scale of silver's involvement in solid-state battery architecture is not immediately obvious, which is precisely why it remains underpriced. In conventional lithium-ion cells, silver plays a peripheral role. Approximately 25–50 grams per vehicle appear in conductive inks and electrical contacts — useful, but not architecturally critical.

The transition from liquid to solid electrolyte fundamentally restructures silver's position in the cell. When the liquid electrolyte is removed, two distinct engineering challenges emerge that silver is uniquely positioned to solve. Furthermore, understanding silver's dual role as both a monetary metal and an industrial input helps contextualise why this shift carries such significant implications for demand.

The Electrode Interface Problem

The boundary between the solid electrolyte and the anode is where the majority of solid-state battery engineering complexity is concentrated. Solid electrolytes are brittle, and the mechanical stresses generated during charge and discharge cycles create interface degradation, dendrite formation, and cycling instability that can compromise cell longevity.

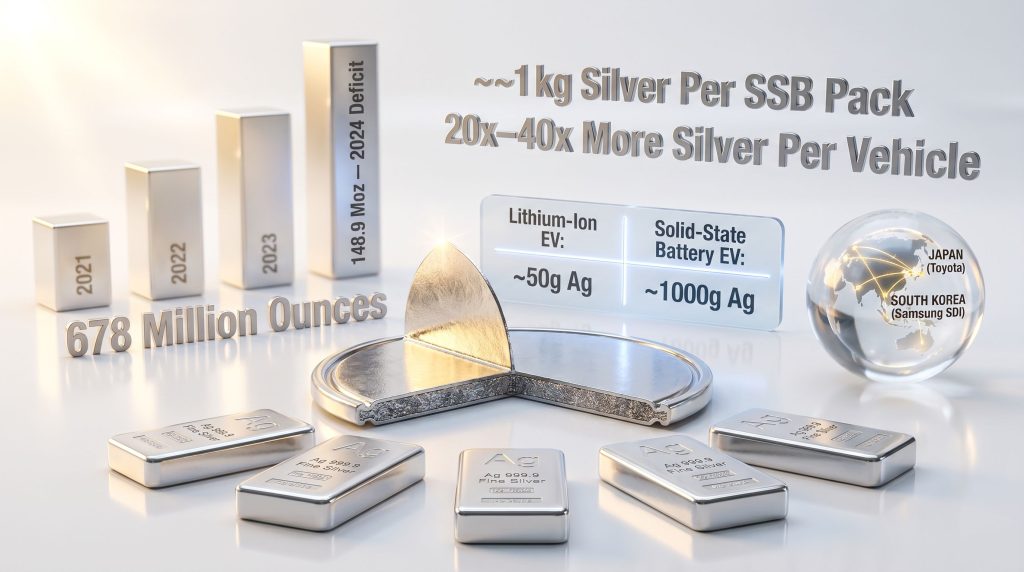

Samsung SDI's anode-less cell architecture addresses this challenge using a silver-carbon composite interlayer. The specification, presented at InterBattery 2024, calls for approximately 1 kilogram of silver — equivalent to 32 troy ounces — per 100 kWh battery pack (Samsung SDI, InterBattery 2024). This is not a theoretical figure from a research paper. It is drawn from a design actively advancing toward mass production, with prototype samples already delivered to automotive customers in 2024.

Academic research published in 2026 from Stanford confirmed that ultrathin silver coatings measurably improve crack resistance in solid electrolyte materials. This finding extends silver's functional role beyond anode design into structural protection of the electrolyte itself — a broader application than most analysts currently model.

The Thermal Management Problem

Liquid electrolytes provide a degree of passive thermal self-regulation inside a conventional cell. Solid electrolytes cannot perform this function. At high charge rates, heat management becomes a critical engineering constraint.

Silver carries the highest thermal conductivity of any commercially relevant metal at 429 W/(m·K), compared to copper's 401 W/(m·K). Silver-coated components within solid-state cells manage heat dispersion at rates that no currently scalable alternative can match at this cost and performance level. This is not a preference — it is an engineering constraint.

Silver Demand Comparison: Conventional EV vs. Solid-State Battery

| Battery Architecture | Silver Per Vehicle | Primary Application |

|---|---|---|

| Conventional lithium-ion EV | ~25–50 grams | Conductive inks, electrical contacts |

| Solid-state EV (silver-carbon anode) | ~1,000 grams (32 troy oz) | Anode interlayer + thermal management |

| Demand multiplier | ~20x to 40x | Structural, not incidental |

A Market Already Drawing Down Its Own Inventories

The silver solid state battery thesis does not arrive into a balanced commodity market. It arrives into one already running a sustained structural shortfall. In addition, the silver supply deficits already documented through 2024 establish a baseline of structural stress that precedes any solid-state battery demand entirely.

The Silver Institute's World Silver Survey 2025 confirmed four consecutive annual supply deficits through 2024. The most recent single-year shortfall reached 148.9 million ounces, with industrial demand hitting a fourth consecutive annual record of 680.5 million ounces (Silver Institute / GlobeNewswire, April 2025). Cumulative above-ground stock drawdowns from 2021 through 2024 reached approximately 678 million ounces — roughly equivalent to ten months of total global mine production consumed before a single commercial solid-state battery has shipped at volume.

| Year | Supply Deficit Status |

|---|---|

| 2021 | Part of 678 Moz cumulative shortfall |

| 2022 | Part of 678 Moz cumulative shortfall |

| 2023 | Part of 678 Moz cumulative shortfall |

| 2024 | 148.9 million ounces (single-year shortfall) |

| 2021–2024 cumulative | ~678 million ounces |

| 2025 | Fifth consecutive deficit forecast |

The supply-side constraint compounds the demand picture. Approximately 70% of global silver production is extracted as a byproduct of copper, zinc, and lead mining (Silver Institute). Primary silver mine output is therefore structurally hostage to the economics of other metals, not to silver's own price trajectory. When silver demand rises, new supply cannot simply be mobilised in response — a constraint that amplifies the impact of any incremental demand catalyst, including solid-state batteries.

The SSB demand thesis does not create a silver supply problem. It arrives into one that already exists. The 678 million ounce cumulative drawdown from 2021 to 2024 represents roughly ten months of total global mine output consumed from above-ground stocks — before a single commercial solid-state battery has shipped at scale.

Where Solid-State Battery Commercialisation Actually Stands

Intellectual honesty requires acknowledging the history here. Battery breakthrough timelines have consistently slipped by two to five years from initial projections. The engineering challenges involved in solid-state manufacturing at scale — interface pressure management, electrolyte deposition uniformity, and production cost reduction — are real and active problems. Research published by MIT in 2026 on dendrite stress behaviour inside solid electrolytes confirmed that these are not trivially solved challenges.

However, the competitive and corporate commitment landscape has shifted materially in the past 24 months in ways that distinguish this period from previous cycles of SSB optimism.

Verified Commercial Milestones by Manufacturer

Toyota

- Official solid-state battery production approval granted in Japan: October 2025 (Toyota Global Newsroom)

- Confirmed commercialisation target: 2027–2028

- Dedicated solid electrolyte supply partnerships established with Idemitsu Kosan and Sumitomo Metal Mining (Shanghai Metals Market, November 2025)

Samsung SDI

- Mass production commitment confirmed for 2027 (Samsung SDI Newsroom, March 2024; Electrive, March 2024)

- Target energy density: 900 Wh/L — approximately 40% higher than current best-in-class lithium-ion cells

- Dedicated SSB commercialisation team established late 2023; pilot production line launched same year; prototype samples delivered to automotive customers in 2024

QuantumScape + Volkswagen PowerCo

- Cell validation by VW PowerCo completed early 2024: more than 1,000 charging cycles retaining 95% capacity (Volkswagen Group press release)

- Industry A-sample benchmark for comparison: 700 cycles at 80% retention — QuantumScape's validated result exceeded this standard

- Volume production licensing agreement signed July 2024: up to 80 GWh per year targeted

| Manufacturer | Key Milestone | Target Date |

|---|---|---|

| Toyota | Production approval granted (Japan) | October 2025 |

| Toyota | Commercial vehicle availability | 2027–2028 |

| Samsung SDI | Mass production commitment | 2027 |

| Samsung SDI | Energy density target | 900 Wh/L |

| QuantumScape / VW PowerCo | Volume licensing agreement signed | July 2024 |

| QuantumScape / VW PowerCo | Volume production target | Up to 80 GWh/year |

What Even Conservative SSB Penetration Does to the Demand Arithmetic

Scenario modelling built from confirmed engineering specifications — rather than optimistic adoption forecasts — produces figures that demand attention even at low penetration assumptions.

A conservative base case assumes 5% solid-state battery penetration across a global EV market of 25 million units in 2028. At Samsung SDI's confirmed specification of 32 troy ounces per pack, this produces approximately 40 million ounces of new annual silver demand — equivalent to roughly 27% of the current single-year supply deficit, layered onto a market already consuming its own inventory reserves.

| Penetration Rate | SSB Vehicles (2028, 25M EV base) | New Silver Demand | % of 2024 Annual Deficit |

|---|---|---|---|

| 2% | 500,000 | ~16 million oz | ~10.7% |

| 5% | 1,250,000 | ~40 million oz | ~26.9% |

| 10% | 2,500,000 | ~80 million oz | ~53.7% |

| 20% | 5,000,000 | ~160 million oz | ~107.4% |

These scenarios are illustrative projections based on confirmed per-unit silver specifications and publicly available EV market forecasts. They represent structural sensitivity analysis, not investment forecasts.

How the Lithium Analogy Holds — and Where It Breaks

The lithium price trajectory following Tesla's Battery Day in September 2020 is frequently cited as the template for the silver solid state battery opportunity. The analogy is instructive but requires careful qualification — and the differences are arguably more important for investors than the similarities.

Where the Parallel Is Valid

Before Battery Day, lithium carbonate traded at approximately $6,000–$7,000 per metric ton. The market had not yet absorbed the scale of EV adoption commitments. By late 2022, spot prices exceeded $82,000 per metric ton as supply-demand gap realities forced repricing (USGS Lithium Minerals Yearbook 2022). The investors who understood the mechanism before it became consensus captured the asymmetric return.

Silver carries a structurally comparable setup today: confirmed engineering specifications pointing to step-change demand growth, on top of a supply base with limited elasticity, in a market that has not yet incorporated the full implications into price discovery. Consequently, tracking battery raw materials across this transition period provides useful comparative context for modelling silver's trajectory.

Where the Analogy Breaks — and Why That May Be an Advantage

| Dimension | Lithium (2020–2022) | Silver (Current) |

|---|---|---|

| Monetary demand component | None — purely industrial | Significant — monetary + safe haven |

| Supply response capability | New brine/hard rock projects could be developed | ~70% byproduct — supply inelastic to price |

| Price catalyst dependency | Required EV adoption confirmation | Structural deficit exists independently of SSBs |

| SSB as a demand driver | Not applicable | Additive to existing deficit and industrial demand |

Silver does not require SSB commercialisation to maintain a structural bull case. The deficit, monetary demand from central bank reserve diversification, and record industrial consumption from solar photovoltaics and conventional EVs collectively constitute the foundational position. The silver solid state battery thesis functions as an additional option layered on top of a position that already carries structural support on multiple independent dimensions.

The next major ASX story will hit our subscribers first

Silver's Triple Classification: What Most Generalist Investors Overlook

In 2025, the U.S. Geological Survey and the Department of the Interior formally designated silver a U.S. critical mineral, citing economic significance, national security relevance, and supply chain vulnerability as the qualifying criteria (Interior Department Final 2025 Critical Minerals List).

This places silver in analytically unusual territory. Most commodities receive one of three possible classifications:

- Monetary metal (gold, historically silver)

- Industrial input (copper, lithium, cobalt)

- Strategic resource (rare earths, certain technology metals)

Silver now simultaneously holds all three. A monetary metal with safe-haven demand properties, a record industrial input across solar, EVs, and electronics, and a formally designated strategic resource with supply chain vulnerability status. This convergence is not yet reflected in how most generalist investors price the metal or allocate to it within portfolio frameworks. Furthermore, monitoring the gold-silver ratio provides an additional lens through which to assess whether silver's current pricing reflects these structural dynamics accurately.

Most commodities receive one of the three designations that silver now holds. The convergence of all three classifications is structurally unusual and creates a demand profile with multiple independent support mechanisms that do not require each other to function.

Bull and Bear Case Architecture for the Silver Solid State Battery Thesis

The investment framework for this thesis does not depend on SSB commercialisation arriving precisely on schedule.

Bull Case

- SSBs reach commercial volumes on the 2027–2028 schedule confirmed by Toyota and Samsung SDI.

- Silver demand from SSB production compounds onto an already structurally deficient physical market.

- Monetary demand remains elevated by central bank reserve diversification and fiscal expansion pressures.

- Three reinforcing demand drivers converge simultaneously on an inelastic supply base — producing non-linear demand multiplier effects.

Bear Case

- SSB timelines slip by two to three years, consistent with historical battery development patterns.

- Record industrial demand from solar and conventional EVs continues expanding regardless.

- A fifth consecutive annual deficit is already forecast for 2025 (Silver Institute, WSS 2025).

- Critical mineral designation elevates institutional and strategic stockpiling interest independently of SSB outcomes.

Risk Factors Worth Acknowledging

- Solid-state battery cost competitiveness versus advanced lithium-ion remains unresolved at commercial scale.

- Interface degradation and pressure management within solid electrolytes are active engineering challenges, as confirmed by MIT dendrite stress research published in 2026.

- The term solid-state is inconsistently applied across industry reporting — some commercially described SSB products retain small liquid electrolyte components, which may reduce silver intensity per cell compared to fully anode-less designs.

- Silver's current price already reflects four years of deficit and record industrial demand, meaning some structural repricing is already embedded in the spot price.

Frequently Asked Questions: Silver and Solid-State Battery Technology

How much silver does a solid-state battery require compared to a standard EV battery?

Samsung SDI's anode-less solid-state architecture specifies approximately 1 kilogram — around 32 troy ounces — of silver per 100 kWh battery pack, used primarily in the silver-carbon composite interlayer at the electrode interface. A conventional lithium-ion EV battery uses roughly 25–50 grams of silver in conductive inks and electrical contacts. The differential is 20 to 40 times more silver per vehicle (Samsung SDI, InterBattery 2024).

Why is silver used specifically in solid-state battery design?

Two distinct functional roles make silver difficult to substitute. First, the silver-carbon composite interlayer at the solid electrolyte–anode boundary stabilises the interface, preventing dendrite formation and cycling degradation. Second, silver's thermal conductivity of 429 W/(m·K) — the highest of any metal — manages heat dispersion at high charge rates in the absence of a liquid electrolyte buffer. No currently scalable alternative meets both requirements simultaneously at competitive cost.

Is there already a silver supply deficit independent of solid-state batteries?

Yes. The Silver Institute's World Silver Survey 2025 confirmed four consecutive annual deficits through 2024, with a 148.9 million ounce shortfall in 2024 alone. The cumulative drawdown from 2021 through 2024 reached 678 million ounces. A fifth consecutive deficit is forecast for 2025.

Which manufacturers are closest to commercial solid-state battery production?

Toyota received production approval in Japan in October 2025 and is targeting commercial vehicle availability in 2027–2028. Samsung SDI has committed to mass production in 2027. QuantumScape and Volkswagen's PowerCo division signed a volume production licensing agreement in July 2024 targeting up to 80 GWh per year.

What is the difference between all-solid-state and semi-solid battery designs, and does it affect silver demand?

All-solid-state designs, such as Samsung SDI's anode-less architecture, eliminate liquid electrolyte entirely and require the full silver-carbon composite interlayer specification. Semi-solid or hybrid designs retain a small liquid electrolyte component to manage interface challenges. These hybrid cells may require less silver per unit, making the confirmed per-pack specification most directly applicable to fully anode-less architectures specifically.

Does the solid-state battery thesis change the fundamental case for holding physical silver?

The SSB thesis adds to the structural case rather than replacing it. The supply deficit, monetary demand, and industrial demand from solar and conventional EVs constitute the existing foundational position. SSB commercialisation would introduce a third major demand driver onto an already supply-constrained market, strengthening rather than creating the investment rationale.

This article is for informational and educational purposes only. It does not constitute investment advice. All scenarios and projections are illustrative and based on publicly available data. Past performance is no guarantee of future results. Please consult a qualified financial adviser before making any investment decisions.

Want to Know When the Next Major Mineral Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across silver, lithium, copper, and more than 30 other commodities — turning complex data into actionable opportunities before the broader market reacts. Start your 14-day free trial at Discovery Alert today, or explore the discoveries page to understand how historic ASX mineral discoveries have generated extraordinary returns for early-positioned investors.