July 10, 2026

Why Physical Scarcity Is Rewriting the Silver Investment Thesis

Most commodity cycles follow a predictable rhythm: prices rise, capital flows in, supply eventually catches up, and margins compress. Silver is breaking that rule in ways that even seasoned resource investors find unusual. The silver supply gap and pure-play silver miners investment case reflects a deeper structural reality, driven by persistent physical scarcity and inelastic supply conditions that are reshaping how the sector is being evaluated. Understanding this disconnect is foundational to making sense of where opportunity genuinely lies.

When big ASX news breaks, our subscribers know first

What Is the Silver Supply Gap and Why Does It Keep Growing?

Six Consecutive Years of Structural Deficit

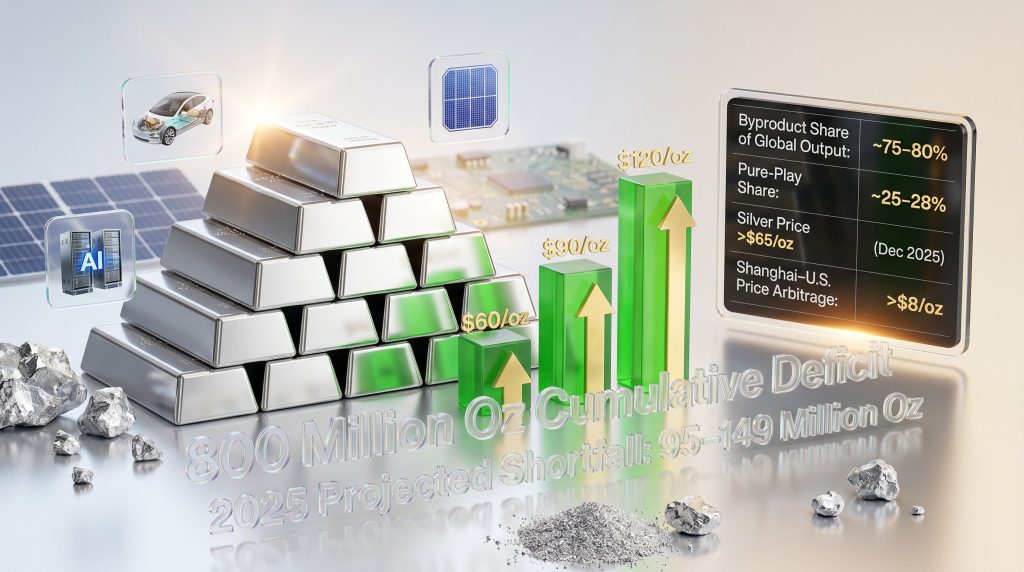

The global silver market has now recorded more than five consecutive years of annual supply deficits, with 2025 projections pointing to a shortfall of between 95 and 149 million ounces against total global demand exceeding 1.2 billion ounces. The cumulative shortfall stretching back through this period is estimated at approximately 800 million ounces, an extraordinary volume of unmet demand that has drawn down above-ground inventories to historically low levels.

What makes this deficit structurally significant rather than cyclically temporary is the nature of silver's supply chain. Approximately 75 to 80 percent of all silver mined globally is extracted as a byproduct of copper, zinc, lead, and gold operations. This means the economics of entirely different metals govern how much silver reaches the market each year. Furthermore, even with silver prices trading above $65 per ounce in late 2025, primary silver supply cannot be meaningfully expanded because throughput decisions at most mines are made based on base metal returns, not silver returns.

This condition is known in commodity economics as supply inelasticity: a market state where price signals fail to unlock proportionate new supply. For a deeper understanding of what is driving these silver supply deficits, the structural demand forces at play are equally important to examine alongside the supply-side constraints.

| Supply Characteristic | Detail |

|---|---|

| Byproduct share of global silver output | ~75-80% |

| Primary silver share of global output | ~25-28% |

| Consecutive years of supply deficit | 5+ years through 2025 |

| Estimated cumulative shortfall | ~800 million ounces |

| 2025 projected annual deficit range | 95-149 million ounces |

| Silver price level (late 2025) | Above $65/oz |

Why Physical Demand Is Absorbing Every Available Ounce

One of the least-reported dimensions of the current silver market is just how immediate physical demand has become at the mine level. Primary silver operations are receiving orders for physical ounces virtually as fast as they can be processed. Demand from buyers across the Middle East, Asia, India, and China has shown no signs of softening regardless of what the paper price is doing.

This creates a striking paradox: the price that investors observe on their screens is being set by a paper market operating on entirely different logic from the physical market where actual ounces change hands. Understanding this divergence is foundational to evaluating pure-play silver miners with any analytical rigour.

What Is Driving Industrial Demand for Silver to Record Levels?

The Four Pillars of Irreplaceable Industrial Consumption

Industrial demand for silver now exceeds 700 million ounces annually, representing the dominant demand category in the global market. Silver's dual role as both a precious metal and industrial commodity makes it functionally irreplaceable across several of the fastest-growing sectors in the global economy:

- Solar photovoltaic manufacturing requires silver paste in cell production, and no commercially viable substitute exists at industrial scale

- Electric vehicles contain significantly more silver per unit than conventional vehicles due to power electronics, battery management systems, and advanced sensor arrays

- AI infrastructure and data centres depend on silver-based components in server hardware, semiconductors, and high-performance computing systems

- Consumer electronics and medical devices provide persistent baseline demand across mature but large-volume categories

The U.S. government has formally designated silver as a critical mineral, a classification that reflects growing recognition of its strategic importance across defence electronics, clean energy infrastructure, and national security supply chains. According to the Silver Institute's supply and demand data, industrial consumption has grown substantially over recent years and shows no signs of plateauing.

How Does Paper Trading Distort the Silver Price Signal?

The Divergence Between Paper Volume and Physical Reality

One of the more technically significant dynamics in the current silver market is the relationship between paper silver instruments and the physical ounces they nominally represent. The volume of paper silver trading, including ETFs, futures contracts, and algorithmically driven derivatives, has reportedly doubled relative to its historical average ratio to physically-backed silver holdings.

What this means practically is that far more silver is being traded on paper than physically exists or is physically represented in underlying vaults. The implications for price discovery are substantial.

Algorithmic Selling and the Self-Reinforcing Feedback Loop

The mechanics work as follows: macro headlines, whether inflation data, interest rate signals, or geopolitical developments, trigger algorithmic selling in silver futures and ETFs. Programme trading then amplifies the price decline. The falling price generates further negative headlines, which trigger further algorithmic selling.

This feedback loop can drive the paper silver price down sharply and persistently, completely independent of what is happening to physical supply and demand. The result is a market where silver prices can remain suppressed even as physical silver coming out of the ground is absorbed immediately by real industrial buyers.

"The paper silver market and the physical silver market are currently operating on entirely different supply-demand dynamics. Physical silver is being absorbed instantaneously by buyers across multiple continents, while the price signal visible to investors reflects paper market dynamics rather than physical market reality."

The Shanghai Price Arbitrage: A Signal of Physical Tightness

A price differential of over $8 per ounce opened between Shanghai and U.S. silver markets in late 2025, a gap large enough to trigger significant physical silver flows toward higher-priced markets. China's response was to implement silver export restrictions effective January 1, 2026, effectively ringfencing domestic supply from international arbitrage.

Export restrictions of this type are a classic policy response to domestic physical scarcity. Governments do not restrict exports of commodities they have in abundance. This development is arguably one of the clearest signals that physical silver tightness is becoming a geopolitical as well as a market consideration.

What Are Pure-Play Silver Miners and Why Do They Matter?

Defining Pure-Play in the Silver Mining Context

A pure-play silver miner is a producer for whom silver represents the primary economic driver of the operation rather than a byproduct credit from another metal's extraction. The defining characteristics include:

- Silver as the principal revenue source, typically exceeding 50% of net revenue

- Deposits where silver mineralisation is the target, not incidental

- Processing infrastructure optimised specifically for silver recovery

- Financial metrics including margins, all-in sustaining costs, and reserve valuations that move directly with silver prices

The importance of "pure-play" status extends beyond definition. There is a meaningful distinction between companies that mine silver incidentally as part of a diversified base metal operation and those whose entire financial story is written by silver prices. The former provides diluted, indirect exposure; the latter provides direct, unhedged leverage.

Why Pure-Play Status Creates Scarcity Value

Pure-play and primary silver producers account for only 25 to 28 percent of global silver production. When examining global silver production across the ten largest producing companies globally, none are classified as primary silver miners. The largest producers are diversified operations where lead and zinc together comprise approximately 31 percent of combined activity.

This structural reality means genuinely silver-focused producers represent a rare and structurally scarce asset class within the broader mining universe. Dedicated silver investment strategies that allocate the majority of holdings to silver-focused companies can deliver roughly double the silver price exposure compared to diversified mining funds.

Operational Leverage: The Mathematics of Pure-Play Mining

The financial argument for pure-play silver miners in a rising price environment rests on the arithmetic of operational leverage. Consider an operation with an all-in sustaining cost of approximately $20 per ounce, which is consistent with costs at some of the more efficient primary silver producers currently operating:

| Silver Price Scenario | AISC ($/oz) | Operating Margin ($/oz) | Margin vs. Cost |

|---|---|---|---|

| $60/oz | $20 | $40 | 200% |

| $90/oz | $20 | $70 | 350% |

| $120/oz | $20 | $100 | 500% |

This exponential margin expansion is the defining financial characteristic of pure-play leverage. A 50 percent increase in the silver price from $60 to $90 produces a 75 percent increase in operating margin per ounce. This asymmetric return profile is precisely why silver-focused producers command strategic premiums in bull markets.

Does High Profitability Risk Flooding the Market With New Supply?

Why Strong Margins Have Not Closed the Structural Gap

A reasonable counterargument to the silver bull case runs as follows: if pure-play miners are generating operating margins of 60 to 66 percent or more at current silver prices, why wouldn't capital rush into the sector and close the supply deficit? However, the evidence suggests several structural barriers prevent this from happening quickly:

Permitting and regulatory timelines:

The mining permitting timelines required to bring a new silver mine from initial discovery through to production typically span 7 to 15 years of environmental licensing, prefeasibility and feasibility studies, infrastructure development, and community engagement. No silver price, however elevated, can compress this timeline meaningfully.

The byproduct dependency constraint:

Since approximately 75 to 80 percent of silver supply is produced as a byproduct of base metal mining, the majority of potential incremental supply is governed by copper, zinc, and lead investment decisions. Silver economics alone cannot direct capital toward new primary silver production at the speed needed to close a 95 to 149 million ounce annual deficit.

Capital intensity and jurisdiction risk:

New mine development requires sustained capital commitment across years of uncertain permitting outcomes, in jurisdictions that carry varying degrees of political stability, royalty regime predictability, and community relationship risk.

"The combination of high current margins and structurally constrained new supply is actually a bullish signal for existing permitted producers. It means the supply gap is unlikely to be closed quickly, and companies already in production or holding advanced permits are positioned to capture sustained margin expansion over an extended period."

The Consolidation Dynamic: Cash-Rich Majors Hunting Juniors

Larger silver producers operating at elevated margins are accumulating significant cash reserves. Much of this capital is being deployed to acquire junior mining projects and development-stage assets. The economic rationale is clear: acquiring a permitted or near-permitted junior project is often faster and considerably cheaper than developing a new mine from the discovery stage.

This dynamic is creating a consolidation wave across the silver junior development space. For investors in well-positioned junior silver developers, it introduces an acquisition premium dimension that is independent of the silver price itself.

The next major ASX story will hit our subscribers first

What Defines a High-Quality Junior Silver Developer?

A Framework for Evaluating Development-Stage Silver Assets

For investors evaluating junior silver miners and developers within the context of the silver supply gap and pure-play silver miners opportunity, the following criteria provide a structured assessment framework:

- Community and government support at both the local and national level, reducing the risk of environmental or social disruption to project timelines

- Mineral grade and metallurgical simplicity, with high-grade silver deposits and straightforward processing chemistry commanding valuation premiums

- Jurisdictional quality, including stable legal frameworks, transparent royalty regimes, and well-established mining law

- Management experience, specifically teams with demonstrated track records of taking projects from exploration through to production or successful sale to a major

- Permit status, with advanced or fully permitted projects eliminating the single largest timeline risk in mine development

The management quality dimension deserves particular emphasis. Many junior mining companies are run by teams without the operational experience needed to navigate the full cycle from exploration through community engagement, environmental licensing, and ultimately production or transaction. The companies that attract major acquirer interest tend to be those run by seasoned professionals who combine geological expertise with community relations capability and a track record of execution.

How Does the Silver Investment Case Compare Across Commodities?

Comparative Analysis: Four Metals, Four Structural Dynamics

| Commodity | Supply Constraint Type | Paper Market Influence | Key Demand Driver | Current Miner Dynamic |

|---|---|---|---|---|

| Silver | Byproduct inelasticity + 6-year deficit | Very high (doubled paper volume) | Industrial: solar, EVs, AI | Miners underperforming physical |

| Gold | Major mine depletion + permitting lag | High (ETFs, futures) | Central bank accumulation | Beginning to outperform |

| Uranium | Long-term utility contracts | Minimal (near-no futures market) | Nuclear power (~20% of U.S. electricity) | Miners significantly lagging spot |

| Copper | Greenfield development timelines | Low (economic signal function) | Electrification infrastructure | Juniors offering high upside |

Gold: A Different Supply Logic With Similar Paper Pressure

The major gold producers are sitting on substantial cash reserves generated by two or more years of gold price appreciation. Many carry all-in sustaining costs well below $2,000 per ounce, creating extraordinary margins at gold prices trading above $4,100 per ounce. Central bank demand remains a structural pillar, with approximately 45 percent of central banks surveyed expressing intent to increase gold reserves, an all-time high reading.

A 35-year analytical framework covering the period from 1992 suggests gold has delivered approximately five times the purchasing power preservation of cash and roughly two times the real return of U.S. Treasury bonds after adjusting for inflation. In addition, the leverage available through the mining sector amplifies this considerably:

- Major gold producers vs. gold: approximately 15x leverage potential

- Well-selected junior gold developers in optimal jurisdictions: up to 100x leverage potential

Uranium: The Widest Miner-to-Commodity Valuation Gap

Uranium represents one of the more technically interesting commodity situations currently visible in the resource sector. Spot prices have stabilised at approximately $85 per ounce, with utility companies signing forward contracts at $95 to $100 per ounce. Nuclear power supplies approximately 20 percent of U.S. electricity generation, creating non-negotiable long-term demand that utility operators must plan for years in advance.

The uranium futures market is effectively non-existent compared to gold and silver. Consequently, paper selling cannot suppress uranium's commodity price the way it does in precious metals. However, uranium mining equities can be sold in paper markets, which is exactly what has happened, creating a valuation gap that represents a compelling anomaly for informed investors.

Copper: Physical Scarcity Without Paper Suppression

Copper has been notably resistant to the paper-driven price suppression observed in silver and gold. The metal reached multi-year highs in 2025 and has maintained elevated levels during a period of broader macro uncertainty. The structural demand case for copper is driven by electrification at every level: grid infrastructure upgrades, EV charging networks, renewable energy systems, and AI data centre power delivery all require substantial copper inputs.

What Is the Long-Term Outlook for the Silver Supply Gap and Pure-Play Silver Miners?

A New Pricing Paradigm: When Scarcity Overlays Commodity Cycles

The structural nature of the silver supply gap, driven by inelastic byproduct supply and irreplaceable industrial demand, suggests the market may be transitioning into a pricing environment that operates by different rules than previous commodity cycles. The silver squeeze dynamics currently unfolding are being closely watched by analysts and institutional investors alike. Industrial offtakers including solar manufacturers, EV producers, and electronics companies are actively seeking long-term supply agreements directly with primary producers. Furthermore, analysis from Sprott ETFs on pure-play silver strategies underscores why focused silver exposure matters for investors seeking genuine commodity leverage.

The paper silver market will continue to generate volatility. Macro headlines, algorithmic reactions, and programme trading will periodically disconnect the observable price from physical market fundamentals. However, this volatility is not evidence that the physical supply thesis is wrong. It is evidence that paper markets and physical markets are pricing different things, and that the divergence between them contains one of the more asymmetric opportunity sets currently available in the resource sector.

Physical supply ultimately determines where prices settle over multi-year horizons. When the volume of paper silver created to absorb investor demand eventually requires physical backing, or when industrial offtakers begin competing more aggressively for contracted supply, the price signal from the physical market will reassert itself. The silver supply gap and pure-play silver miners investment case rests on exactly that eventual convergence.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, investment recommendations, or an offer or solicitation to buy or sell any securities. All statistics, projections, and market data referenced involve inherent uncertainty and should not be relied upon as the sole basis for any investment decision. Past performance of any asset class, commodity price, or mining sector does not guarantee future results. Readers should conduct their own independent research and consult a licensed financial adviser before making any investment decisions.

Want to Be First When the Next Major Silver Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across silver and more than 30 other commodities — giving subscribers an actionable market edge before the broader investment community reacts. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself ahead of the next major find.