July 28, 2026

The complexity of modern supply chain diplomacy extends far beyond traditional trade relationships. When critical materials become geopolitical leverage points, nations must navigate intricate webs of economic interdependence, technological competition, and strategic vulnerability. This evolution transforms routine diplomatic meetings into high-stakes negotiations where cultural symbolism masks underlying tensions over industrial control and resource security.

Understanding how sovereign powers manage these dynamics requires examining the intersection of ceremonial diplomacy and supply chain realpolitik, particularly when Sino-French rare earth diplomacy seeks to maintain access while simultaneously reducing dependence on dominant suppliers.

What Does Sino-French Rare Earth Diplomacy Really Mean for Global Markets?

Defining the New Era of Critical Mineral Statecraft

Critical mineral statecraft represents a fundamental shift in how nations conduct international relations. Unlike traditional diplomacy focused on political alignment or military cooperation, this approach treats mineral supply chains as instruments of national power and economic leverage.

The emergence of this diplomatic framework reflects the reality that certain materials have become essential to modern technological infrastructure yet remain concentrated in the hands of few producers. Nations controlling these resources can influence everything from renewable energy transitions to defense manufacturing capabilities.

France's position within this framework is particularly nuanced. As a nuclear power with significant technological capabilities, France possesses both the expertise and motivation to develop alternative supply chains. However, the immediate reality of European dependence on Chinese processing creates a delicate balancing act between long-term strategic goals and short-term access requirements.

Why France Leads Europe's Strategic Mineral Negotiations

France's diplomatic leadership in critical minerals stems from several converging factors. The nation's nuclear industry provides deep expertise in complex material processing, while its historical relationships across Africa and Asia offer potential alternative sourcing pathways.

French diplomatic culture emphasizes cultural bridge-building and civilizational dialogue, making it an ideal intermediary for managing tensions that could otherwise escalate into trade conflicts. Furthermore, this approach allows for maintaining dialogue even as underlying competitive dynamics intensify.

Emmanuel Macron's government has consistently advocated for European strategic autonomy while simultaneously engaging with major powers. This dual approach reflects France's understanding that complete independence is unrealistic in the short term, necessitating careful management of existing relationships during transition periods.

China's Calculated Response to Western Diversification Efforts

Beijing's approach to Western diversification efforts demonstrates sophisticated strategic thinking. Rather than resisting these efforts through confrontation, Chinese leadership has adopted a strategy of managed engagement designed to slow diversification while maintaining access to Western markets and technology.

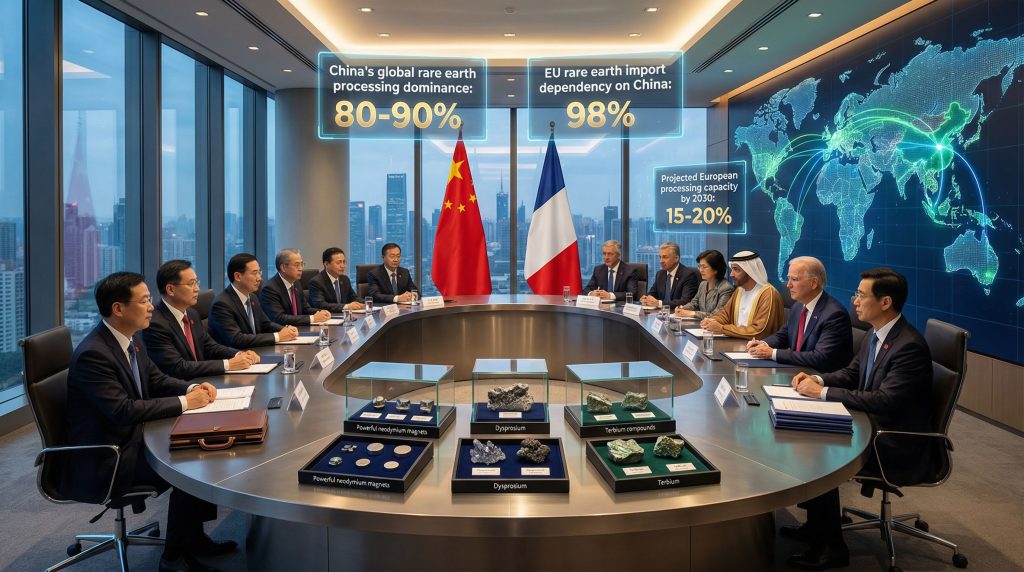

The December 2025 Chengdu meeting between Xi Jinping and Emmanuel Macron exemplifies this approach. By emphasizing cultural partnership and civilizational dialogue, Chinese state media framed the relationship in terms that transcend immediate commercial competition while carefully avoiding discussion of the underlying supply chain tensions.

This diplomatic choreography serves multiple purposes: it maintains goodwill during a period of structural change, provides China with insights into European strategic thinking, and creates space for potential bilateral arrangements that could benefit Chinese interests even as broader Western diversification proceeds. In addition, this reflects broader patterns seen in rare earth talks russia-us negotiations.

When big ASX news breaks, our subscribers know first

How Do Export Controls Shape Modern Diplomatic Relations?

The Economics Behind China's Rare Earth Export Licensing System

China's export licensing system functions as both an economic management tool and diplomatic leverage mechanism. The system allows Chinese authorities to control not just the volume of exports but also their timing and destination, creating opportunities to reward cooperative behavior and signal displeasure with policies that threaten Chinese interests.

The economic logic centres on maximising value capture from China's processing dominance. By controlling exports at the refined material stage rather than raw mineral stage, China ensures that high-value processing activities remain within its borders while maintaining flexibility to adjust supply based on strategic considerations.

This approach generates substantial revenue while providing political leverage. European manufacturers dependent on Chinese rare earth materials must consider the potential for supply disruptions when their governments implement policies that conflict with Chinese interests, creating a feedback loop that influences European policy formation.

European Union's Critical Raw Materials Act as Diplomatic Leverage

The EU's Critical Raw Materials Act represents Europe's attempt to create counter-leverage in rare earth diplomacy. By establishing targets for domestic processing capacity and alternative sourcing, the legislation signals European determination to reduce dependence while providing a timeline that can be adjusted based on diplomatic developments.

The Act's structure allows for flexibility in implementation, creating space for bilateral agreements that could moderate the pace of diversification in exchange for guaranteed access and stable pricing. This flexibility transforms the legislation from a purely confrontational measure into a diplomatic tool that can accommodate various negotiating scenarios.

European policymakers recognise that complete independence is neither feasible nor necessarily optimal. Consequently, the Act aims to achieve sufficient diversification to eliminate Chinese veto power over European critical mineral access while maintaining beneficial trade relationships where possible.

Timeline of Escalating Restrictions and Diplomatic Responses

The evolution of rare earth export controls reflects broader geopolitical tensions. Initial restrictions emerged from environmental and resource conservation concerns but gradually incorporated strategic considerations as global competition intensified, mirroring patterns in the us-china trade war impact on various sectors.

Key milestones include China's implementation of export quotas in the 2000s, subsequent WTO challenges, and the recent expansion of controls to cover processed materials rather than just raw ores. Each escalation has prompted diplomatic responses designed to maintain dialogue while addressing underlying concerns.

Recent diplomatic engagements, including the Xi-Macron meeting, represent attempts to manage this escalation through direct dialogue rather than allowing it to proceed through purely regulatory channels. However, the challenge lies in addressing legitimate security concerns while maintaining beneficial economic relationships.

| Metric | Current Status | Trend Direction |

|---|---|---|

| China's global rare earth processing share | 80-90% | Stable but declining |

| EU import dependency on China | 98% | Targeted for reduction |

| Projected European processing capacity by 2030 | 15-20% | Increasing investment |

Which Strategic Scenarios Could Emerge from Current Tensions?

Scenario 1 – Managed Competition Through Bilateral Agreements

The managed competition scenario envisions sustained Chinese dominance in rare earth processing combined with bilateral agreements that guarantee European access in exchange for technological cooperation and market access commitments. This outcome would require both sides to accept partial interdependence while managing competitive dynamics in other sectors.

Under this scenario, France's diplomatic engagement would prove successful in establishing frameworks for ongoing cooperation. Chinese export controls would become more predictable and transparent, while European diversification efforts would proceed at a measured pace designed to create alternatives without eliminating Chinese suppliers.

The probability of this scenario depends largely on broader geopolitical developments. For instance, if tensions in other areas (technology transfer, military cooperation, human rights) can be contained, economic logic favors maintaining beneficial trade relationships even amid strategic competition.

Scenario 2 – Accelerated European Supply Chain Independence

The independence scenario assumes that current diplomatic engagement fails to address fundamental European concerns about supply security. Under this pathway, European investment in alternative processing capacity would accelerate, supported by substantial public funding and regulatory requirements for supply chain diversification.

This scenario would transform current diplomatic meetings from genuine negotiations into tactical temperature-lowering exercises designed to prevent escalation while Europe builds alternative capacity. Chinese responses could include preference for other customers or acceleration of downstream integration to maintain market position.

The timeline for this scenario depends on technological development and capital availability. European processing capacity could theoretically meet domestic needs within a decade, but achieving cost competitiveness with Chinese operations would require sustained policy support and technological advancement, as discussed in critical minerals energy transition strategies.

Scenario 3 – Fragmented Global Rare Earth Markets

The fragmentation scenario anticipates the emergence of regional supply chain blocs with limited cross-bloc trade. This outcome would result from sustained escalation of current tensions combined with similar dynamics in other bilateral relationships, creating a world of parallel supply chains serving different regional markets.

Under this scenario, diplomatic engagement would continue but would focus on managing competition rather than promoting cooperation. Different regions would develop distinct technological standards and supply chain configurations, reducing global efficiency but increasing strategic autonomy for major powers.

This outcome appears least likely in the near term due to the substantial costs involved for all parties. Nevertheless, broader geopolitical developments could make fragmentation seem preferable to continued interdependence despite economic inefficiencies.

What Investment Implications Arise from Shifting Diplomatic Dynamics?

European Rare Earth Processing Opportunities

European rare earth processing presents significant investment opportunities, particularly for companies positioned to benefit from public policy support. The EU's Critical Raw Materials Act creates a framework for substantial public investment in processing capacity, potentially generating attractive returns for private investors willing to accept regulatory and technological risks.

The key challenge involves achieving cost competitiveness with established Chinese operations while meeting European environmental and labour standards. Success requires technological innovation, efficient operations, and sustained policy support through multiple political cycles.

Investment opportunities span the entire processing chain, from ore concentration to finished magnets. Early-stage investments in processing technology and mid-stage investments in manufacturing capacity both offer potential for substantial returns as European demand for non-Chinese sources increases. These developments align with broader trump order on critical minerals initiatives influencing global markets.

Technology Transfer Negotiations and Joint Ventures

Technology transfer negotiations create complex investment dynamics. Chinese companies possess advanced processing technologies that European companies need, while European companies offer market access and technological capabilities in downstream applications.

Joint ventures could provide pathways for technology transfer while maintaining beneficial relationships. However, investors must evaluate the sustainability of such arrangements given broader strategic competition and potential regulatory changes that could limit technology sharing.

The most promising arrangements involve mutual benefit rather than one-way technology transfer. European companies with complementary technologies or market access can negotiate from positions of strength, creating more stable and profitable partnerships.

Risk Assessment for Downstream Manufacturing Sectors

Downstream manufacturers face complex risk assessment challenges. Companies dependent on rare earth materials must evaluate supply security, price volatility, and regulatory compliance across multiple scenarios while maintaining operational efficiency and profitability.

Risk mitigation strategies include supply chain diversification, strategic stockpiling, and investment in alternative technologies. However, these approaches involve significant costs and may not provide complete protection against supply disruptions, making diversification investing strategies essential for portfolio management.

Investors should prioritise companies with strong risk management capabilities and flexible supply chain strategies. Market leaders that can influence supplier selection and maintain multiple sourcing options are likely to outperform companies with rigid supply chain dependencies.

Investment Monitoring Framework:

• Track EU Critical Raw Materials Act funding allocations and implementation timelines

• Monitor Chinese export licence approval rates and processing timelines for European customers

• Assess European magnet manufacturing capacity expansion and technological development

• Evaluate bilateral diplomatic agreements and their commercial implications

How Should Investors Navigate Diplomatic Uncertainty?

Diversification Strategies Beyond Chinese Supply Chains

Effective diversification requires understanding both geographical and technological alternatives to Chinese rare earth processing. Investors should evaluate companies developing processing capabilities in North America, Australia, and other regions with stable regulatory environments and adequate mineral resources.

Technological diversification involves supporting research and development of alternative materials and processing methods. While these approaches may not achieve immediate commercial viability, they offer potential for substantial returns if breakthrough technologies emerge.

Portfolio diversification should balance exposure to current market leaders with investments in potential disruptors. This approach provides protection against supply chain disruptions while maintaining upside potential from technological innovation.

Regulatory Risk Assessment Tools

Regulatory risk assessment requires monitoring multiple policy developments across different jurisdictions. Changes in export controls, environmental regulations, and trade policies can significantly impact rare earth supply chains and investment returns.

Effective monitoring systems track regulatory developments in real-time and assess their potential commercial impact. This capability allows investors to anticipate market changes and adjust portfolios before regulatory shifts fully materialise.

The most sophisticated approaches involve scenario modelling that estimates probability-weighted outcomes for different regulatory pathways. This analysis helps investors understand downside risks while identifying opportunities created by regulatory changes.

Long-term Supply Security Planning

Long-term planning horizons for rare earth investments extend beyond traditional business cycles. Infrastructure investments in processing facilities require decade-long commitments, while technological development can take even longer to achieve commercial viability.

Successful planning requires balancing current profitability with strategic positioning for different future scenarios. Companies that invest in capabilities needed across multiple scenarios are likely to outperform those that bet on specific outcomes.

Investors should prioritise companies with management teams that understand both technical and geopolitical complexities. The ability to navigate changing diplomatic relationships while maintaining operational excellence separates long-term winners from short-term opportunists.

What Role Does Cultural Diplomacy Play in Resource Negotiations?

Symbolic Meetings vs. Substantive Policy Changes

Cultural diplomacy serves multiple functions in resource negotiations, often providing cover for substantive discussions while creating atmospheres conducive to compromise. However, investors must distinguish between symbolic gestures and concrete policy commitments when evaluating diplomatic developments.

The December 2025 Xi-Macron meeting in Chengdu exemplified this dynamic. While Chinese state media emphasised cultural exchange and civilisational dialogue, the meeting's substance likely involved discussions of trade relationships, technology transfer, and supply chain management that received less public attention.

"The visit highlighted the profound friendship and cooperation between the two civilisations," Chinese state media reported, carefully avoiding mention of rare earth tensions. Symbolic diplomacy can provide early indicators of changing relationships, but investment decisions should focus on policy outcomes rather than ceremonial gestures.

Media Narratives and Their Market Impact

Media coverage of diplomatic meetings can significantly influence market sentiment even when underlying fundamentals remain unchanged. Positive diplomatic imagery often generates optimism about improved trade relationships, while negative coverage can heighten concerns about supply chain disruptions.

Sophisticated investors monitor media narratives while maintaining focus on substantive policy developments. Chinese state media's emphasis on cultural partnership during the Xi-Macron meeting, for example, provided insights into Chinese strategic messaging while revealing topics that were deliberately avoided.

The most valuable analysis involves comparing official statements across different media sources and identifying discrepancies that reveal underlying tensions or disagreements. These gaps often provide more accurate indicators of negotiating dynamics than official diplomatic language.

Reading Between the Lines of Official Statements

Official diplomatic statements require careful interpretation to extract useful investment insights. Standard diplomatic language often obscures substantive disagreements while providing coded messages about negotiating positions and future intentions.

Key analytical techniques include identifying topics that are mentioned versus those that are avoided, comparing emphasis across different statement sections, and tracking changes in language over time. These approaches help investors understand diplomatic dynamics that may not be explicitly stated.

The absence of rare earth or critical mineral discussions in official statements about the Xi-Macron meeting, for example, suggests that these topics remain contentious despite the positive overall tone. This omission provides valuable information about the current state of Sino-French rare earth diplomacy negotiations and likely future developments.

The next major ASX story will hit our subscribers first

Which European Companies Benefit from Supply Chain Restructuring?

Rare Earth Processing Technology Developers

Companies developing advanced rare earth processing technologies stand to benefit significantly from European supply chain restructuring initiatives. These technologies include hydrometallurgical processes, biotechnological approaches, and advanced separation techniques that could reduce processing costs while meeting environmental standards.

Investment opportunities exist across the technology development spectrum, from early-stage research companies to established industrial firms expanding their processing capabilities. The key evaluation criteria include technological differentiation, intellectual property protection, and scalability to commercial production levels.

European companies with existing chemical processing expertise may be particularly well-positioned to adapt their capabilities to rare earth processing. These firms often possess relevant infrastructure, regulatory compliance systems, and technical expertise that can be leveraged for critical mineral applications.

Alternative Magnet Material Innovators

Innovation in alternative magnet materials offers potential for substantial market disruption. Companies developing ferrite-based magnets, electromagnetic alternatives, and novel permanent magnet materials could capture significant market share if their products achieve performance parity with rare-earth-based alternatives.

The most promising opportunities involve incremental improvements to existing technologies rather than revolutionary breakthroughs. Companies that can achieve modest performance gains while significantly reducing rare earth content may find substantial market demand from manufacturers seeking supply chain security.

Investment evaluation should focus on technical feasibility, commercial viability, and patent protection. Companies with strong research partnerships and adequate funding for extended development cycles are most likely to achieve commercial success in this challenging but potentially rewarding sector.

Strategic Stockpiling and Trading Operations

Strategic stockpiling operations offer opportunities for companies that can effectively manage commodity price volatility while providing supply chain security for industrial customers. These operations require sophisticated understanding of market dynamics, storage costs, and regulatory requirements.

Trading operations can capture value from price differences across time periods, geographical regions, and product specifications. Success requires detailed market knowledge, strong customer relationships, and adequate capital for inventory management during volatile market conditions.

The most successful strategic stockpiling operations combine financial trading expertise with technical understanding of material specifications and quality requirements. This combination allows them to serve industrial customers while managing financial risks associated with commodity price movements.

How Do Geopolitical Tensions Affect Pricing Mechanisms?

Premium Pricing for Non-Chinese Sources

Non-Chinese rare earth sources command premium pricing due to supply chain diversification demands and perceived reliability advantages. These premiums reflect both immediate supply constraints and long-term strategic value for customers seeking to reduce dependence on Chinese suppliers.

Premium levels vary significantly across different materials and applications. High-performance permanent magnet applications typically justify higher premiums than bulk commodity applications, reflecting the strategic importance and technical requirements of different end uses.

Pricing dynamics also reflect quality considerations and supply reliability factors beyond pure geopolitical concerns. Customers often prefer suppliers with consistent quality standards, reliable delivery performance, and transparent business practices even when premium pricing is required.

Long-term Contract Structures and Risk Mitigation

Long-term contracts have become increasingly important for managing supply chain risks in volatile geopolitical environments. These contracts typically include price stability mechanisms, force majeure provisions, and supply guarantee clauses that protect both suppliers and customers.

Contract structures often incorporate indexing mechanisms that adjust prices based on market conditions while providing baseline price stability. These arrangements help suppliers manage input cost volatility while giving customers predictable pricing for planning purposes.

Risk mitigation provisions may include alternative sourcing arrangements, strategic stockpiling requirements, and technology sharing agreements. The most sophisticated contracts create mutual dependencies that incentivise both parties to maintain beneficial relationships even during broader geopolitical tensions.

Spot Market Volatility During Diplomatic Crises

Spot market pricing exhibits significant volatility during periods of heightened diplomatic tension. Market participants often react to political developments with buying or selling decisions that may not reflect underlying supply and demand fundamentals.

Volatility patterns typically follow predictable cycles: initial price spikes during crisis escalation, followed by consolidation as market participants assess actual supply impact, and eventual stabilisation once diplomatic resolution or alternative sourcing arrangements are established.

Sophisticated market participants can potentially profit from these volatility cycles by maintaining adequate liquidity to capitalise on price dislocations while avoiding panic buying or selling during peak uncertainty periods. Success requires disciplined risk management and deep understanding of both market fundamentals and geopolitical dynamics.

What Are the Long-term Consequences for Global Trade Architecture?

Bilateral vs. Multilateral Approach to Critical Minerals

The choice between bilateral and multilateral approaches to critical mineral governance will significantly influence future trade architecture. Bilateral agreements offer flexibility and speed but may create inconsistent standards and preferential arrangements that undermine global efficiency.

According to the European Council on Foreign Relations, "Europe cannot afford to blink on China's rare earth blackmail, as the continent's green transition depends critically on securing alternative supply chains."

Multilateral frameworks could provide more stable and predictable governance structures but require consensus among participants with different strategic interests and competitive positions. The challenge involves balancing national security concerns with economic efficiency and global stability.

Current trends suggest a hybrid approach where bilateral agreements operate within broader multilateral frameworks. This structure allows for customised arrangements while maintaining general principles of fair trade and transparent governance.

WTO Challenges to Export Restriction Policies

Export restriction policies face potential challenges under World Trade Organization rules, particularly provisions regarding quantitative restrictions and discriminatory treatment. However, national security exceptions may provide justification for certain restrictions, creating complex legal and political dynamics.

WTO dispute resolution mechanisms operate slowly compared to the pace of geopolitical developments, potentially making legal challenges less relevant than diplomatic and economic responses. The effectiveness of WTO enforcement also depends on political willingness to comply with dispute panel decisions.

Future WTO governance may need to incorporate clearer guidelines for critical mineral trade that balance security concerns with free trade principles. This evolution could establish precedents for managing strategic competition through international legal frameworks rather than purely bilateral negotiations.

Regional Bloc Formation in Resource Trading

Regional bloc formation appears increasingly likely as nations seek to secure critical mineral access through preferential trading arrangements. These blocs could provide enhanced security and economic efficiency within member countries while potentially creating barriers for non-members.

The most viable blocs combine resource-rich regions with major consuming markets, creating mutual dependencies that strengthen negotiating positions relative to external competitors. Geographic proximity and existing political relationships often facilitate bloc formation and operational effectiveness.

According to Politico Europe, "The EU faces no quick release from China's rare earth chokehold, despite increasing investment in alternative supply chains and processing capabilities." Regional blocs may compete with each other while maintaining limited cooperation on global challenges requiring broader coordination.

Frequently Asked Questions About Sino-French Rare Earth Relations

Will diplomatic engagement reduce supply chain risks?

Diplomatic engagement can moderate supply chain risks by improving communication and reducing the likelihood of sudden disruptions, but it cannot eliminate fundamental structural dependencies. The effectiveness of diplomatic risk reduction depends on broader geopolitical stability and the willingness of all parties to prioritise economic relationships over strategic competition.

Recent diplomatic meetings like the Xi-Macron summit demonstrate both the potential and limitations of diplomatic approaches. While such meetings can establish frameworks for managing tensions, they do not address the underlying asymmetries that create vulnerability in the first place.

Long-term risk reduction requires structural changes in supply chain configuration rather than relying solely on diplomatic solutions. Diplomacy can facilitate these changes and manage transitions, but cannot substitute for fundamental diversification and capacity building efforts.

How quickly can Europe develop independent processing capacity?

European independent processing capacity development faces significant technical, financial, and regulatory challenges that limit the speed of implementation. Realistic timelines for meaningful capacity development extend over multiple years, with full independence requiring sustained investment over a decade or more.

The most optimistic scenarios assume aggressive public policy support, successful technology transfer or development, and sustained private investment despite competitive pressures from established suppliers. Even under favourable conditions, achieving cost competitiveness with existing operations requires substantial scale and operational efficiency.

Incremental progress is more likely than rapid transformation. European processing capacity will probably increase gradually while maintaining some level of import dependence for economic efficiency. The goal involves reducing strategic vulnerability rather than achieving complete self-sufficiency.

What triggers China's export control decisions?

China's export control decisions reflect multiple considerations including domestic supply requirements, strategic relationship management, and responses to perceived hostile policies from importing countries. Understanding these triggers requires monitoring both Chinese domestic developments and international political dynamics.

Economic factors include domestic demand growth, environmental compliance costs, and global price considerations. Strategic factors involve technology transfer concerns, military applications of exported materials, and broader geopolitical competition with importing countries.

Policy decisions often combine immediate tactical considerations with long-term strategic positioning. Recent emphasis on domestic consumption and high-value-added processing suggests that export controls increasingly serve industrial policy objectives beyond traditional trade management goals.

This analysis is based on publicly available information and industry insights. Investment decisions should consider multiple factors beyond geopolitical dynamics, including company fundamentals, market conditions, and individual risk tolerance. Geopolitical developments remain inherently unpredictable, and their commercial impacts may differ from current expectations.

Looking for Investment Opportunities in Critical Minerals?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market whilst geopolitical tensions reshape global supply chains. Explore Discovery Alert's dedicated discoveries page to understand why major mineral discoveries can lead to substantial returns, then begin your 30-day free trial today to position yourself strategically during this period of unprecedented supply chain transformation.