July 16, 2026

The Unconventional Lithium Frontier: Why Formation Water Is Attracting Serious Attention

The global race to secure lithium supply has quietly moved beyond the salt flats of South America and the hard-rock mines of Western Australia. A less visible but increasingly consequential frontier is emerging beneath the world's oil and gas fields, where billions of cubic metres of mineralised formation water are pumped to the surface every year as an operational byproduct. For decades, this produced water was managed as a waste liability. Today, Sinopec lithium extraction from oilfield-produced water is being reappraised as a latent resource, and the implications for battery supply chains are only beginning to come into focus.

Understanding why this shift is happening requires a clear-eyed look at both the chemistry of produced water and the structural pressures reshaping how critical minerals are sourced globally.

When big ASX news breaks, our subscribers know first

What Is Oilfield-Produced Water and What Makes It Interesting?

Produced water, also known as formation water, is the saline fluid trapped within subsurface reservoir rock that travels to the surface alongside oil and gas during hydrocarbon extraction. Its chemical composition is far from uniform. Salinity, mineralisation, temperature, and the presence of specific ions vary significantly depending on the depth of the geological formation, regional mineralogy, and how mature the reservoir is.

In lithium-bearing geological belts, produced water can carry commercially relevant concentrations of dissolved lithium. Some formations globally, including the Smackover limestone in the southern United States, have recorded concentrations exceeding 500 mg/L of lithium. The general industry threshold for economically viable extraction is considered to be around 100 mg/L, though this benchmark is technology-dependent and continues to shift as processing methods improve.

The table below contextualises how oilfield-produced water compares with conventional lithium sources:

| Lithium Source | Typical Concentration | Key Advantage | Key Challenge |

|---|---|---|---|

| Hard-rock spodumene | N/A (solid ore) | High-grade, established processing | High capital cost, energy-intensive |

| Salar brine | 200–1,500 mg/L | Large scale, low extraction cost | Long evaporation timelines, high water usage |

| Geothermal brine | 100–400 mg/L | Co-production opportunity | Geographic constraints |

| Oilfield produced water | Typically below 100 mg/L (variable) | Existing infrastructure, widespread distribution | Low concentration, complex competing ion chemistry |

The strategic appeal of produced water is not anchored in concentration. It lies in infrastructure leverage. Oil and gas operators are already handling, treating, and disposing of enormous volumes of this fluid. Furthermore, layering lithium recovery onto existing operational workflows means the marginal capital required to add value is far lower than building a greenfield lithium project from scratch. For a deeper understanding of how lithium brine extraction compares across different source types, the contrast with oilfield-produced water becomes particularly instructive.

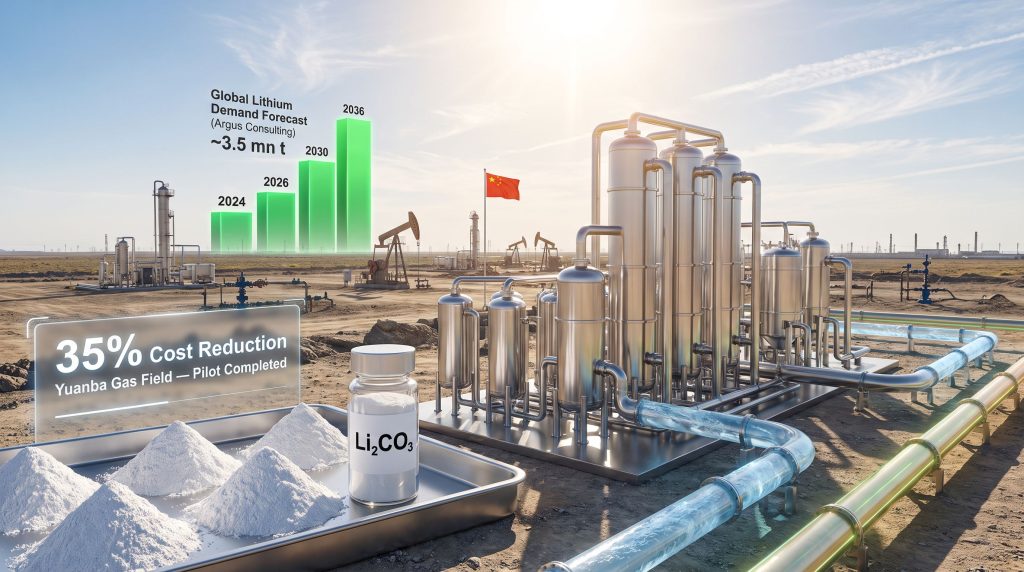

Sinopec's Pilot at Yuanba: How the Technology Actually Works

Sinopec completed a pilot demonstration of its proprietary extraction methodology at the Yuanba gas field in southwestern China, operated by its regional oil and gas subsidiary. The technology was independently developed by Sinopec's engineering and construction arm, described as a rapid adsorption and desorption process. Critically, the pilot executed the complete production chain: from raw produced water intake through to extraction, precipitation, and drying, culminating in the output of industrial-grade lithium carbonate, the standard commercial form used as feedstock in battery manufacturing.

The step-by-step process works as follows:

-

Pre-treatment – Removal of suspended solids, organic compounds, and competing ions such as calcium and magnesium that interfere with selective lithium capture.

-

Adsorption – Lithium-selective adsorbent materials, typically manganese oxide or titanium-based compounds, preferentially bind lithium ions from the high-salinity brine.

-

Desorption (Elution) – A mild acid wash or water flush strips the captured lithium from the adsorbent, producing a concentrated lithium-rich eluate.

-

Concentration and Purification – Membrane filtration or controlled evaporation increases lithium concentration to levels suitable for downstream processing.

-

Precipitation – Introduction of sodium carbonate or CO₂ triggers lithium carbonate precipitation from solution.

-

Drying and Finishing – The precipitate is dried and refined to meet industrial-grade specifications, typically exceeding 99% Li₂CO₃ purity.

Sinopec reported that its process can reduce production costs by more than 35% relative to conventional lithium extraction methods while also shortening the overall processing chain. Specific lithium recovery rate percentages were not disclosed at the pilot stage. This approach shares conceptual similarities with direct lithium extraction technologies being developed elsewhere, particularly in their use of selective adsorbent materials to isolate lithium from complex brines.

*Analytical note: A claimed 35%+ cost reduction requires careful contextualisation. Conventional salar brine production in the Atacama region operates at some of the world's lowest costs, estimated at approximately $3,000 to $5,000 per tonne of lithium carbonate equivalent (LCE). Hard-rock spodumene processing typically sits in the $8,000 to $12,000/t LCE range. If Sinopec's cost comparison is benchmarked against hard-rock methods, a 35% reduction would still position produced water lithium at a meaningful premium relative to best-in-class Atacama brine production. The commercial case likely rests on co-production economics rather than standalone competitiveness with low-cost brine supply.*

Comparing Lithium Extraction Methodologies

| Method | Selectivity | Scalability | Cost Efficiency | Maturity Level |

|---|---|---|---|---|

| Adsorption (Sinopec approach) | High | High | Moderate to High | Emerging commercial |

| Solvent or ion exchange | Moderate | Moderate | Moderate | Pilot to commercial |

| Membrane separation | Moderate | Moderate | Moderate | Pilot |

| Electrochemical extraction | High | Low to Moderate | High (theoretical) | Early-stage R&D |

| Evaporation (traditional brine) | Low | Very High | Low to Moderate | Mature commercial |

It is worth noting that multiple Chinese research institutions have independently mapped recommended processing architectures for oilfield lithium that closely mirror Sinopec's approach, generally proposing combined pretreatment, enrichment concentration using adsorption or membrane separation, and a final precipitation step. According to research published in peer-reviewed literature, this alignment between academic roadmaps and Sinopec's proprietary method suggests the company is operating at the leading edge of a broader national research programme rather than in isolation.

Why China Is Pursuing Every Domestic Lithium Vector Available

China's structural exposure in the lithium supply chain is acute. Despite being the world's single largest consumer of lithium, the country holds only approximately 7% of global lithium resources and depends on imports for roughly 70% of its supply, according to industry data cited by Sinopec. This dependency creates a compounding strategic vulnerability as domestic EV adoption accelerates. Consequently, understanding the pressures shaping the global lithium market helps contextualise why China is so aggressively pursuing every available domestic supply vector.

The numbers driving demand urgency are striking:

-

China's NEV fleet reached 48.97 million units at the end of June 2026, representing 13.2% of the total national vehicle fleet, according to data from China's Ministry of Public Security.

-

Battery electric vehicles (BEVs) accounted for 68.8% of all NEVs, at 33.68 million units.

-

During the first half of 2026, China registered 5.2 million new NEVs, comprising 49.4% of all newly registered vehicles, a 4.5 percentage point increase year on year. Effectively, nearly one in every two newly registered vehicles in China was electric.

-

China has set a national target of 30% NEV fleet penetration by 2030 under a carbon emissions reduction plan released by the State Council.

Against this demand trajectory, global lithium supply requirements look increasingly demanding:

| Year | Projected Global Lithium Demand (LCE) | Primary Driver |

|---|---|---|

| 2024 | ~1.0 million tonnes | EV battery manufacturing |

| 2026 | ~1.4 million tonnes (estimated) | EV + energy storage systems |

| 2030 | ~2.0 to 2.5 million tonnes (estimated) | EV scale-up, grid storage |

| 2036 | ~3.5 million tonnes | Full EV transition + ESS buildout (Argus Consulting forecast) |

Within this context, the motivation for a state-owned enterprise like Sinopec to convert an operational waste stream into a domestically sourced battery material becomes straightforward. China's oil and gas sector generates billions of cubic metres of produced water annually, most of it currently treated and injected back underground or discharged. Converting even a fraction of this volume into a recoverable lithium stream represents a meaningful, if incremental, contribution to domestic supply security.

Structural insight often overlooked: Produced water treatment is already a mandatory regulatory obligation for oil and gas operators in China. This means the cost base for handling the water exists regardless of whether lithium is recovered. In economic terms, the true marginal cost of lithium extraction from produced water must be assessed against what the operator was already spending on produced water management, not against the full cost of a standalone lithium project. This reframing substantially improves the apparent economics for integrated operators.

Sinopec's Wider Energy Transition Repositioning

The Yuanba pilot should not be read in isolation. It forms one component of a broader strategic transformation that Sinopec is executing as it repositions from a hydrocarbon-dominant company toward an integrated energy and materials group.

In June 2026, Sinopec signed a joint development agreement with BYD, China's leading NEV manufacturer, to co-develop fast-charging infrastructure, directly tying Sinopec's extensive fuel retail network into the EV adoption ecosystem. Separately, Sinopec has made an investment in CATL, China's largest battery cell producer, with a stated objective of contributing to a network of 10,000 EV battery exchange stations.

| Initiative | Partner or Asset | Strategic Objective |

|---|---|---|

| Lithium from produced water | Yuanba gas field (internal) | Domestic lithium supply security |

| Fast-charging infrastructure | BYD (joint development) | Capture EV transition revenue streams |

| Battery exchange stations | CATL (investment) | Integrate into EV charging ecosystem |

This triangulated positioning reflects a recognition that the energy transition creates structural risks for traditional hydrocarbon business models, but also substantial opportunities for companies with the infrastructure footprint and capital resources to pivot. Sinopec's lithium extraction pilot is arguably the most technically novel element of this strategy, converting a liability stream into a strategic commodity.

How Sinopec Compares to Global Peers

Sinopec is not alone in pursuing produced water as a lithium source, but it is among the most advanced operationally.

ExxonMobil represents the most mature Western equivalent, targeting the Smackover Formation in Arkansas, where produced water lithium concentrations can exceed 500 mg/L, placing it firmly above the typical economic threshold. ExxonMobil's Smackover project is targeting commercial production and has attracted significant attention as a potential domestic US lithium supply source. Industry analysts have noted that oilfield produced water could represent produced profits for operators willing to invest in the appropriate recovery infrastructure.

MGX Minerals in Canada has demonstrated lithium recovery from oilfield produced water using proprietary membrane filtration technology, though the project remains at pilot scale.

| Company | Country | Technology | Stage | Reported Li Concentration |

|---|---|---|---|---|

| Sinopec | China | Rapid adsorption and desorption | Pilot completed | Not publicly disclosed |

| ExxonMobil | USA | Adsorption-based | Development | ~500 mg/L (Smackover) |

| MGX Minerals | Canada | Membrane filtration | Pilot | Variable |

| Chinese research institutions | China | Multiple approaches | Laboratory to pilot | Variable |

One distinction worth highlighting is that the Smackover Formation in Arkansas benefits from unusually high lithium concentrations relative to most global produced water sources. The formation was deposited under ancient evaporitic conditions that concentrated lithium and bromine over geological time. Most produced water encountered globally does not approach these concentrations, which is why the Smackover has attracted disproportionate attention in the US lithium from brines conversation.

China's Yuanba gas field, by contrast, operates in a sedimentary basin context with different geochemical conditions. The fact that Sinopec has not publicly disclosed the lithium concentrations in its Yuanba produced water is noteworthy. In the absence of this data, the scale-up pathway and commercial economics cannot be independently assessed.

The next major ASX story will hit our subscribers first

The Real Barriers: What Needs to Be Solved Before Scale-Up

Completing a successful pilot is a proof of chemistry. It is not a proof of commercial viability at scale. Several material challenges remain before Sinopec lithium extraction from oilfield-produced water can be considered a meaningful supply contributor:

-

Concentration challenge: Most produced water globally carries lithium well below the 100 mg/L viability threshold, requiring energy-intensive pre-concentration that adds cost complexity.

-

Competing ion interference: High concentrations of sodium, calcium, magnesium, and potassium reduce adsorbent material selectivity and drive up reagent consumption.

-

Organic fouling: Residual hydrocarbons and chemical additives from oilfield operations degrade adsorbent materials and membrane systems over repeated use cycles, compressing operational lifetimes.

-

Volume management: Generating commercially meaningful lithium output requires processing enormous volumes of produced water. The infrastructure required to move, treat, and process these volumes at scale is non-trivial.

-

Adsorbent material degradation: Repeated adsorption and desorption cycles cause physical and chemical deterioration of the adsorbent over time, creating an ongoing consumable cost that affects long-run economics.

The scaling question that matters most: A pilot proves the chemistry functions. The harder interrogation is whether the unit economics hold across a full commercial operation when lithium carbonate prices are cyclically volatile. At depressed spot prices below $10,000/t LCE, which markets have experienced in recent cycles, marginal-cost unconventional lithium projects face severe profitability pressure regardless of technological novelty. The lithium market downturn experienced in recent years illustrates precisely how exposed higher-cost producers can become during periods of oversupply. Long-term supply contract structures, rather than spot exposure, may therefore be essential to underwrite investment at scale.

Where Produced Water Lithium Sits in the Global Supply Stack

Produced water lithium is not going to displace established brine or spodumene lithium extraction in any near-term timeframe. However, as a supply diversification vector, it occupies a structurally compelling position, particularly for operators where produced water management is an existing cost obligation.

| Supply Category | Cost Position | Scale Potential | Timeline to Materiality |

|---|---|---|---|

| South American salar brine | Lowest | Very large | Already material |

| Australian hard-rock spodumene | Moderate | Large | Already material |

| Chinese domestic salt lake brine | Moderate | Moderate | Growing |

| Geothermal lithium | Moderate to High | Moderate | 5 to 10 years |

| Oilfield produced water | Variable, co-production dependent | Moderate (long-term) | 5 to 15 years |

| Deep-sea nodules | High | Very large | 10 to 20+ years |

If Sinopec successfully scales its technology across multiple oilfield assets, and if other Chinese state-owned energy companies follow a similar path, the cumulative contribution could reduce China's import dependency at the margin over a decade-long horizon. The technology's success could also catalyse similar programmes at PetroChina and CNOOC, both of which operate substantial produced water volumes across domestic fields.

The broader pattern here mirrors what traditional hydrocarbon majors globally are navigating: how to extract value from existing assets and operational capabilities while positioning for a structural shift in energy markets. For Sinopec, the Yuanba pilot represents the most technologically original expression of that challenge so far, and a compelling indicator of where unconventional lithium supply may be heading in the years ahead.

This article contains forward-looking projections and demand forecasts sourced from Argus Consulting and industry data. These represent estimates based on prevailing conditions and are subject to material change. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence before making investment decisions related to lithium, battery materials, or energy sector equities.

Want To Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential opportunities across lithium and more than 30 other commodities — turning complex mineral data into clear, actionable insights. Explore historic discoveries and their remarkable returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.