May 11, 2026

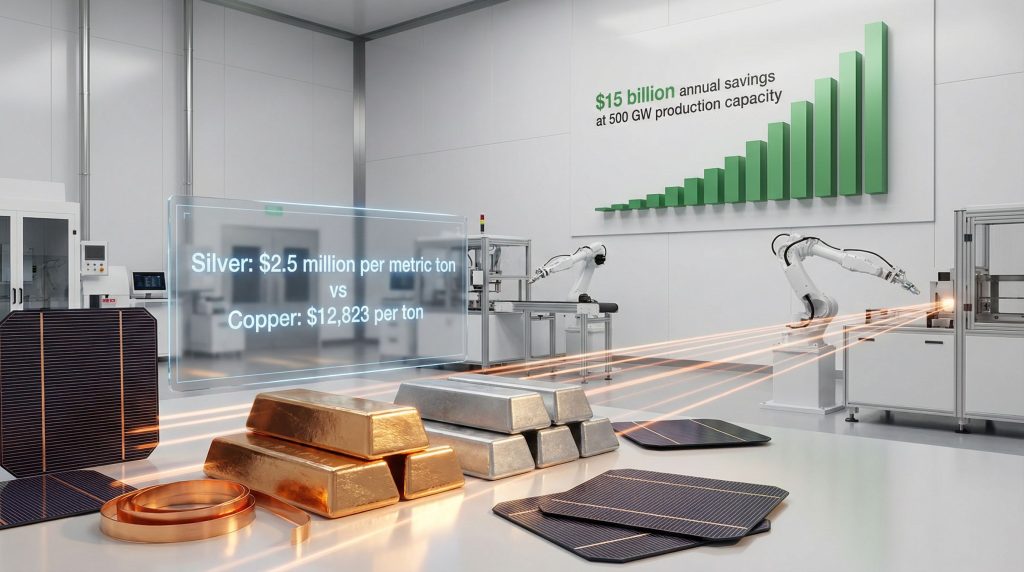

The solar manufacturing sector confronts an unprecedented metallization cost surge that fundamentally challenges production economics. Silver paste, valued at $2.5 million per metric ton, now trades at approximately 200 times the price of copper alternatives, which cost roughly $12,823 per ton. This dramatic price differential represents more than a simple commodity arbitrage opportunity—it signals a structural shift in manufacturing input economics that demands immediate technological responses. Furthermore, the shift to copper in solar industry has emerged as the most viable solution to address these mounting pressures.

Economic Pressures Driving the Shift to Copper in Solar Industry

Silver Price Volatility Creates Manufacturing Cost Crisis

Industry cost analysis reveals that silver paste comprises 30% of total solar cell manufacturing expenses, creating direct exposure to precious metal price volatility. Manufacturing facilities report 7-15% increases in solar panel costs over 12 months, primarily attributed to silver price escalation. The photovoltaic sector's consumption of 196 million troy ounces annually—representing 17% of global silver demand—creates significant market pressure that compounds with jewelry, electronics, and investment demand.

The cost impact becomes starkly evident in per-module economics: silver paste costs per 450-watt module increased from $5.22 to $17.65 over approximately 12 months, representing a 238% cost escalation. This dramatic increase directly translates to project economics, where utility-scale installations face margin compression that threatens grid parity achievements in emerging markets.

Moreover, the silver market squeeze has intensified these challenges, creating ripple effects throughout the entire photovoltaic supply chain. Additionally, silver supply deficits continue to worsen, further exacerbating the economic pressures facing manufacturers worldwide.

Supply Chain Vulnerabilities in Precious Metal Dependence

Geographic concentration risks compound the economic pressures facing solar manufacturers. Silver mining operations concentrate in specific producing regions, creating supply disruption vulnerabilities that extend beyond normal commodity price cycles. The 147% silver price rally in 2025, culminating in an all-time high of $121.64 per ounce before stabilizing at $77 per ounce, demonstrates the volatility manufacturers must navigate.

Production overcapacity, particularly concentrated in Chinese manufacturing facilities, amplifies silver cost pressure by reducing manufacturers' ability to pass commodity price increases to downstream customers. This creates a margin compression scenario where facilities face simultaneous pressure from overcapacity pricing competition and input cost inflation, accelerating the urgency for alternative metallization technologies.

Strategic material sourcing becomes critical as the shift to copper in solar industry gains momentum. Unlike silver's concentrated mining geography, copper production benefits from broader geographic distribution and established supply chains serving multiple industrial sectors, potentially providing greater price stability and supply security. In contrast, copper price trends have shown relatively more stable patterns compared to precious metals volatility.

When big ASX news breaks, our subscribers know first

Copper Metallization Performance and Technical Implementation

Electrical Conductivity and Contact Resistance Analysis

The fundamental challenge in implementing copper metallization lies in balancing material properties with manufacturing economics. Silver exhibits superior electrical conductivity at 63 × 10⁶ S/m compared to copper's 59.6 × 10⁶ S/m, creating initial performance concerns that required extensive materials science research to address.

Breakthrough research demonstrates that copper metallization achieves 99% of silver cell performance, indicating that the 6% conductivity disadvantage does not translate proportionally to efficiency losses. This achievement required sophisticated engineering solutions addressing contact resistance, current collection geometry, and interface optimization between copper contacts and silicon substrates.

The performance achievement results from understanding that cell-level efficiency depends on multiple factors beyond bulk material conductivity:

- Contact geometry optimization to compensate for conductivity differences

- Interface engineering to minimise contact resistance at the metal-semiconductor junction

- Current collection pathway design to reduce resistive losses through improved finger patterns

- Thermal management during manufacturing to prevent copper diffusion into silicon

Manufacturing Process Adaptations and Equipment Modifications

Successful copper metallization implementation requires comprehensive manufacturing process adaptations that extend beyond simple material substitution. Screen-printing technology, the industry standard for contact application, demands significant modifications to accommodate copper paste's different rheological properties.

Paste formulation adjustments address fundamental differences in copper's behaviour during printing and sintering processes:

- Viscosity modifications to ensure consistent printing resolution across substrate variations

- Particle size optimisation to achieve proper contact formation without compromising adhesion

- Organic vehicle chemistry reformulation to prevent copper oxidation during storage and application

- Sintering atmosphere control requiring nitrogen or reducing environments rather than air sintering

Quality control protocol evolution becomes essential to address copper's unique characteristics:

- Oxidation prevention testing during manufacturing and storage phases

- Adhesion strength quantification under thermal cycling conditions

- Contact resistance measurement across humidity and temperature ranges

- Long-term stability validation through accelerated ageing protocols

The shift to copper in solar industry requires diffusion barrier solutions to prevent copper migration into silicon substrates under high-temperature processing. These barriers, potentially involving titanium or molybdenum layers, add manufacturing complexity while maintaining the overall cost advantage over silver systems.

Financial Impact Assessment of Copper Adoption

Global Manufacturing Cost Reduction Projections

The economic implications of copper metallization adoption extend across multiple production scales, creating compound savings effects throughout the solar value chain. Comprehensive cost analysis reveals dramatic savings potential across different manufacturing scenarios:

| Production Scale | Silver Costs (Annual) | Copper Alternative Costs | Potential Savings |

|---|---|---|---|

| 500 GW Global Production | $18.2 billion | $3.2 billion | $15 billion |

| Per MW Installation | $36,400 | $6,400 | $30,000 |

| 450W Module Unit | $17.65 | $3.10 | $14.55 |

These projections assume copper paste costs approximately 17.5% of silver paste expenses, based on current commodity price differentials and manufacturing process adaptations. The $15 billion annual global savings potential at 500 GW production capacity represents approximately 15% of total manufacturing costs across the industry, creating substantial competitive advantages for early adopters.

Per-module savings of $14.55 translate directly to project economics, potentially reducing utility-scale installation costs by $30,000 per MW while maintaining equivalent electrical performance. This cost reduction accelerates grid parity achievement in emerging markets and enhances returns for utility-scale developers.

Return on Investment Analysis for Technology Transition

Manufacturing facility conversion to copper metallization requires careful analysis of capital expenditure requirements versus operational savings. Equipment retooling costs include:

- Screen-printing equipment modifications for copper paste compatibility

- Sintering furnace atmosphere control systems to prevent copper oxidation

- Quality control equipment upgrades for copper-specific testing protocols

- Staff training and process development for new metallization technologies

Break-even analysis suggests that facilities processing 100 MW annually can recover conversion investments within 18-24 months based on current silver-copper price differentials. Higher-volume facilities benefit from accelerated payback periods, while smaller operations may require longer amortisation schedules.

The competitive advantage duration depends on industry adoption rates. Early movers benefit from cost advantages until widespread implementation equalises manufacturing expenses. Technology licensing arrangements may provide revenue streams for research organisations and early developers.

Industry Leaders Driving the Copper Transition

Manufacturing Giant Implementation Strategies

Major solar manufacturers demonstrate varying approaches to metallization technology transition, reflecting different risk tolerance levels and market positioning strategies. LONGi Green Energy, China's leading solar panel manufacturer, announced copper-based metallization advances with mass production planned between April and June 2026, representing one of the most aggressive implementation timelines among industry leaders.

The implementation strategy involves hybrid silver-copper paste intermediate solutions that provide graduated transition pathways rather than abrupt technology replacement. This approach offers several strategic advantages:

- Reduced silver content while maintaining performance during technology validation

- Supply chain integration testing without complete process overhaul

- Workforce skill development in copper metallization gradually

- Customer confidence building through proven intermediate performance

Pure copper metallization development programmes represent the ultimate technology target, with research focusing on complete silver elimination while maintaining equivalent cell efficiency. Leading manufacturers invest heavily in proprietary formulations and process technologies to secure competitive advantages.

Regional Manufacturing Hub Adaptations

Chinese manufacturing facilities, representing the majority of global solar production capacity, face unique advantages and challenges in copper transition implementation. Existing overcapacity pressures create urgency for cost reduction technologies, while established supply chains provide copper sourcing advantages.

European manufacturing initiatives focus on technology differentiation and premium positioning, potentially targeting specialised applications where performance optimisation justifies higher costs during transition periods. European facilities benefit from established relationships with chemical suppliers and research institutions.

North American manufacturing expansion incorporates copper metallization as a foundational technology rather than retrofit application, potentially providing cost structure advantages over established facilities requiring conversion investments.

The shift to copper in solar industry creates opportunities for emerging market manufacturers to enter global supply chains with cost-optimised production capabilities, potentially redistributing market share away from traditional manufacturing centres.

Technical Challenges and Solutions in Copper Implementation

Materials Science and Engineering Obstacles

Copper's chemical properties create unique technical challenges that require sophisticated materials science solutions. Copper oxidation prevention represents the primary manufacturing concern, as oxidised copper contacts exhibit significantly higher resistance and reduced adhesion to silicon substrates.

Atmospheric control during processing becomes critical, requiring nitrogen or hydrogen-containing environments during sintering operations. This contrasts with silver paste processing, which tolerates air sintering, adding complexity and operational costs that partially offset raw material savings.

Diffusion barrier implementation prevents copper migration into silicon crystal structures under high-temperature processing. Common barrier materials include:

- Titanium thin films providing excellent diffusion resistance with minimal electrical impact

- Molybdenum layers offering superior thermal stability during processing

- Nickel barriers providing cost-effective solutions with moderate performance

- Multi-layer systems combining materials for optimised performance and cost

Adhesion strength optimisation requires surface preparation modifications and possible silicon substrate treatments to ensure long-term mechanical stability. Thermal expansion coefficient differences between copper and silicon demand careful contact design to prevent mechanical failure during temperature cycling.

Quality Assurance and Long-Term Performance Validation

Copper-based solar cell reliability testing protocols require extensive validation to establish equivalency with decades of silver system field performance data. Accelerated ageing testing must demonstrate copper contact stability under:

- Thermal cycling between -40°C and +85°C for 200+ cycles

- Humidity exposure at 85% relative humidity and 85°C for 1000+ hours

- UV radiation exposure simulating 20+ years of field conditions

- Mechanical stress testing validating contact integrity under wind loading

Field performance monitoring of early copper-based installations provides critical validation data, though long-term performance requires years of data collection. Initial deployments focus on controlled environments with extensive monitoring equipment to identify potential degradation mechanisms.

International certification requirements for copper metallization systems include IEC 61215 and IEC 61730 compliance, necessitating extensive testing and documentation for global market acceptance. Certification costs and timelines may influence adoption rates among smaller manufacturers.

Economic Impact on Global Solar Market Dynamics

Wholesale Pricing Evolution and Cost Cascades

The shift to copper in solar industry creates downstream cost reduction cascades that extend through entire value chains. Wholesale solar panel price reductions of 10-15% become achievable with copper implementation, directly impacting utility-scale project economics and residential installation affordability.

Installation cost improvements multiply copper's direct manufacturing savings through reduced balance-of-system expenses. Lower module costs justify premium mounting systems and inverter technologies, potentially improving overall system performance while maintaining target price points.

Grid parity acceleration in emerging markets becomes achievable through copper cost reductions, expanding global solar deployment opportunities. Markets previously dependent on subsidies or favourable financing may achieve economic competitiveness with conventional generation sources.

Utility-scale project returns improve through reduced capital expenditure requirements, enhancing project finance availability and reducing power purchase agreement pricing. Developer margins expand, potentially accelerating deployment timelines and market growth.

Supply Chain Restructuring and Strategic Material Management

Copper demand increases from solar industry adoption must be assessed against existing industrial consumption patterns. Mining capacity requirements for supporting terawatt-scale solar manufacturing may strain existing copper production, potentially creating new commodity price pressures. This connection highlights how the critical minerals transition affects broader industrial sectors.

Silver market demand reduction could stabilise precious metal pricing, benefiting remaining silver-dependent applications while reducing investment speculation. The 17% demand reduction from photovoltaic applications may significantly impact silver trading dynamics.

Strategic material stockpiling becomes important for manufacturers securing copper supply during transition periods. Long-term procurement agreements and vertical integration strategies may provide cost stability and supply security advantages.

Recycling infrastructure development for copper-based panels requires long-term planning, as recycling becomes economically viable with higher copper content compared to silver systems. End-of-life value recovery may partially offset initial manufacturing costs.

The next major ASX story will hit our subscribers first

Future Outlook and Industry Transformation Implications

Production Capacity Expansion and Technology Scaling

Terawatt-scale manufacturing feasibility improves dramatically with copper metallization economics, enabling aggressive capacity expansion plans that were previously constrained by silver supply limitations and cost structures. Manufacturing facilities can target higher production volumes without proportional increases in working capital requirements for precious metal inventory.

Geographic manufacturing distribution may shift toward regions with favourable copper supply chain access and lower energy costs for modified processing requirements. Countries with established copper mining and refining industries gain competitive advantages in solar manufacturing.

Technology transfer acceleration to developing economies becomes economically viable with copper systems, as lower material costs reduce barriers to manufacturing facility investment. This democratisation of solar manufacturing technology could reshape global production patterns. Consequently, energy transition innovation becomes more accessible to emerging markets.

Innovation pipeline development focuses on next-generation metallization solutions, including aluminium alternatives and advanced contact geometries that further optimise performance and cost structures beyond current copper implementations.

Competitive Landscape and Market Share Evolution

First-mover advantages in copper metallization create temporary competitive benefits lasting 18-36 months until industry-wide adoption equalises cost structures. Early adopters gain market share through pricing flexibility and margin advantages during transition periods.

Vertical integration strategies become attractive as manufacturers seek copper supply chain control and processing optimisation. Companies with metallurgical expertise or mining relationships may pursue upstream integration opportunities.

Investment capital allocation redirects toward copper-optimised manufacturing facilities rather than silver-dependent systems, potentially stranding assets in facilities unable to adapt quickly to metallization transitions.

The shift to copper in solar industry represents more than incremental cost optimisation—it enables fundamental restructuring of manufacturing economics that supports global renewable energy expansion at unprecedented scales. Success requires coordinated technical innovation, supply chain adaptation, and strategic capital allocation across the entire photovoltaic value chain.

As the solar industry accelerates its shift away from silver-based systems, manufacturers worldwide are positioning themselves for this transformational change. However, implementation success will depend on careful attention to technical challenges, quality assurance protocols, and strategic supply chain management. The industry stands at a critical juncture where early adopters may gain significant competitive advantages, whilst delayed implementation could result in substantial cost disadvantages in an increasingly price-sensitive market.

Disclaimer: Cost projections and performance estimates are based on current technological developments and commodity pricing. Actual results may vary due to technical implementation challenges, supply chain dynamics, and market conditions. Investment decisions should consider comprehensive risk assessments and professional consultation.

Ready to Discover the Next Copper Mining Breakthrough?

As the solar industry's shift to copper creates unprecedented demand for this critical metal, Discovery Alert's proprietary Discovery IQ model identifies significant copper discoveries on the ASX the moment they're announced, providing immediate market advantages for both short-term traders and long-term investors. Explore historic examples of transformative copper discoveries and begin your 14-day free trial today to position yourself ahead of this massive industrial transformation.