July 8, 2026

The Hidden Fault Line Running Through the Global Energy Transition

Every industrial revolution carries within it a material contradiction. The transition away from fossil fuels is no exception. At the centre of the clean energy buildout sits a metal whose production is anything but clean, and whose supply is anything but secure. Aluminium, the structural backbone of solar photovoltaic infrastructure, has quietly become one of the most strategically consequential commodities of the 2020s. Understanding solar subsidies and aluminium supply chains requires looking not at the metal itself, but at the policy architecture that governs the industry consuming it at scale.

Solar subsidies and aluminium supply chains are no longer parallel conversations. In 2026, they are a single, interlocked system, and disruption in one is immediately felt in the other.

When big ASX news breaks, our subscribers know first

Why Aluminium Is the Unsung Backbone of Solar PV

The visible face of solar energy is silicon, but the structural reality is aluminium. Frames, racking systems, mounting hardware, and inverter housings all depend on the metal in quantities that most energy transition analysts consistently underestimate.

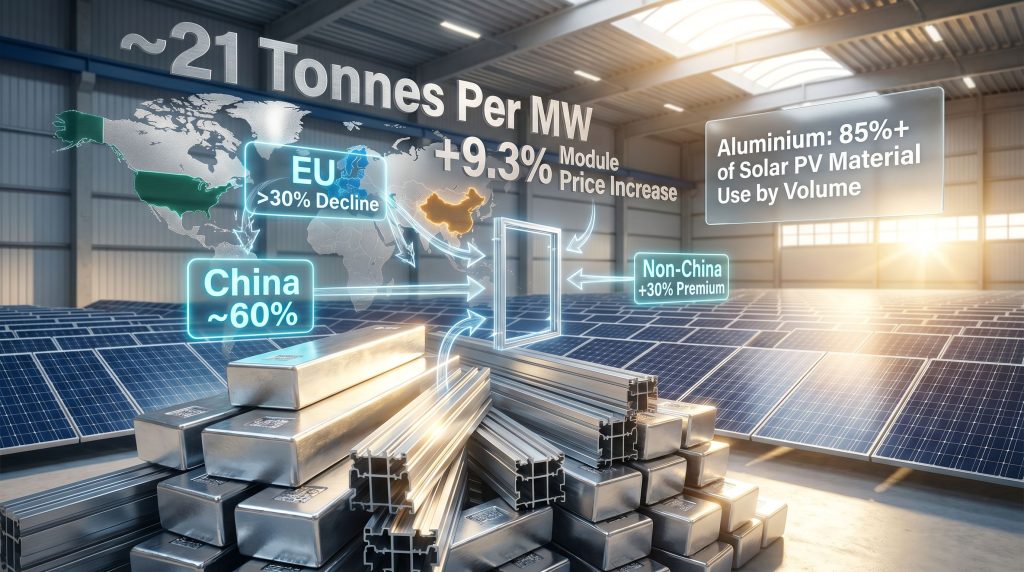

Each megawatt of installed solar PV capacity requires approximately 21 tonnes of aluminium. Scaled to the installation targets now embedded in national and regional energy strategies, that figure becomes staggering. Aluminium accounts for over 85% of total material volume across the dominant solar PV technologies, making it the single largest material input by mass in the global solar build.

This creates what analysts have termed the congealed electricity paradox: a metal that demands extraordinary quantities of electrical energy to produce from raw ore is now the foundational material of the infrastructure designed to generate clean electricity. The irony is structural, not incidental, and it has direct implications for how solar subsidies interact with aluminium markets.

Demand Projections That Redefine the Supply Equation

The scale of aluminium demand implied by global solar targets is rarely presented with the clarity it deserves. Consider the following projections:

| Scenario | Projected Aluminium Demand Increase | Timeframe |

|---|---|---|

| IRENA Remap Pathway | +160 million tonnes | To 2050 |

| EU Solar Strategy (320 GW) | +4 to 10 million tonnes | By 2025 |

| EU Solar Strategy (600 GW) | Compounding uplift | By 2030 |

| IEA 2°C Scenario (PV alone) | 840 MtCO₂e embedded | Long-term |

Solar PV accounts for approximately 87% of incremental aluminium demand growth within the renewables sector. This figure reframes aluminium from a commodity input into a strategic transition material, one whose pricing, availability, and carbon intensity will shape the viability of the energy transition itself. Furthermore, the global bauxite supply feeding into primary aluminium production adds another layer of geopolitical complexity to this equation.

From Expansion to Discipline: The Subsidy Inflection of 2025 to 2026

For nearly two decades, solar subsidies operated as blunt instruments of scale. Between 2005 and 2024, support mechanisms globally averaged approximately 3.2% of firm revenues, functioning as broad capacity accelerants rather than precision tools. The result was a manufacturing ecosystem defined by volume over margin, and a supply chain that prioritised speed over resilience.

That era has structurally ended.

Three distinct regulatory environments are now operating simultaneously, each pulling solar and aluminium markets in different directions:

- China's subsidy withdrawal, forcing consolidation after decades of state-supported overcapacity

- The EU's conditional incentive model, tying support to supply chain provenance and carbon thresholds

- The US domestic-first framework, using tax credits to rebuild manufacturing capacity within its own borders

The interaction between these three policy regimes is generating price signals, supply pressures, and strategic realignments that are reshaping how aluminium moves through global solar supply chains. In addition, US aluminium tariffs introduced in this period have further complicated procurement strategies for solar manufacturers operating outside American borders.

China's VAT Reversal and Its Industrial Consequences

China's position in solar manufacturing is without parallel. The country built approximately 900 gigawatts of module manufacturing capacity, a volume sufficient to satisfy projected global demand through 2032. This buildout was underwritten by decades of subsidised energy inputs, state-directed financing, and VAT export rebates that made Chinese modules structurally cheaper than anything produced elsewhere.

In April 2026, that calculation changed materially. The elimination of VAT export rebates on solar products represents the most significant policy break in the sector in over two decades. The trajectory of that rebate tells the story clearly:

- Historical VAT rebate level: 13%

- Interim level (2024): 9%

- Post-April 2026: 0%

The market response was immediate and measurable. Module prices rose 9.3%, with TOPCon module pricing moving from approximately USD 0.086 per watt in January 2026 toward a projected USD 0.098 per watt by year-end.

The aluminium dimension of this shift is frequently overlooked. Aluminium frames account for approximately 14% of total module manufacturing costs. When VAT buffers are removed, this cost exposure becomes fully unhedged against global metal price volatility. A subsidy withdrawal in Beijing thus creates a direct transmission mechanism into aluminium procurement costs for solar manufacturers worldwide.

The removal of VAT export rebates does not merely affect module pricing. It functionally eliminates the cost cushion that previously absorbed aluminium price volatility at the manufacturing stage, transferring that risk downstream to installers, developers, and ultimately energy consumers.

How China's Dominance Creates Systemic Supply Chain Risk

The concentration of solar manufacturing capacity in a single country is not a new observation, but the depth of that concentration across the full value chain is less widely appreciated. Consider the following breakdown:

| Supply Chain Stage | China's Market Share |

|---|---|

| Primary aluminium production | ~60% globally |

| Polysilicon manufacturing | >80% |

| Solar wafer production | >90% |

| Module assembly | >80% |

| Aluminium frame fabrication | Dominant position |

This degree of vertical integration means that a single policy decision in Beijing can simultaneously affect module costs, aluminium frame pricing, and global installation economics. The April 2026 VAT removal is precisely this kind of decision: a policy signal that reverberates across every stage of the solar supply chain, including the metals markets that feed into it.

The 30% Cost Premium of Supply Chain Diversification

Non-China solar PV supply chains carry an estimated cost premium of approximately 30% under current conditions without compensating subsidies or protective tariffs. This premium is not purely a manufacturing cost differential. It reflects the accumulated advantage of subsidised energy inputs to Chinese aluminium smelters, state-directed capital allocation, and decades of learning curve compression driven by volume.

Aluminium production globally generates approximately 1.1 billion tonnes of CO₂ annually. Chinese smelters, predominantly coal-powered, represent a disproportionate share of that total. This creates a secondary problem: the 30% cost premium of diversification is partially a carbon accounting gap. Western producers operating on cleaner energy grids carry higher input costs but lower lifecycle emissions, a distinction that current market pricing does not fully reward. For instance, renewable-powered aluminium initiatives in Australia illustrate how energy transition investment can begin to close this gap.

Strategic Scenarios for Aluminium Supply Chains Through 2030

Three distinct pathways are available to the global solar manufacturing ecosystem, each carrying different implications for solar subsidies and aluminium supply chains.

Scenario 1: Accelerated Western Onshoring

The US Inflation Reduction Act's Section 45X tax credits create direct incentives for domestic solar and aluminium-linked manufacturing. The numbers in the pipeline are substantial:

- New US polysilicon capacity: projected 9 GW by 2035

- US module manufacturing pipeline: approximately 19 GW currently under construction

- Critical gap: Even under optimistic projections, US facilities may satisfy only 19 to 61% of domestic polysilicon requirements by 2035

The aluminium dimension of this onshoring scenario is equally constrained. Domestic smelter viability requires access to competitively priced, carbon-free electricity, a condition met in very few US markets. The onshoring narrative is compelling strategically but faces significant infrastructure and energy cost barriers that tax credits alone cannot resolve.

Scenario 2: Managed Plurilateral Diversification

India's Production Linked Incentive scheme mirrors the IRA's intent but targets different segments of the value chain. Southeast Asian manufacturing hubs absorbing displaced Chinese capacity face their own aluminium sourcing constraints. A plurilateral model distributes concentration risk but does not eliminate the 30% cost premium without coordinated energy policy across multiple jurisdictions. This scenario reduces single-country dependency without achieving cost parity.

Scenario 3: Geopolitical Shock Absorption

Middle East trade route disruptions in 2025 and 2026 introduced freight and logistics volatility into aluminium delivery timelines. Geopolitical stress-testing has revealed that just-in-time aluminium supply models for solar manufacturers carry unpriced tail risk. Scenario modelling suggests that a 15 to 20% supply disruption in primary aluminium flows could delay solar installation targets by 12 to 18 months in affected regions.

The critical variable across all three scenarios is not module pricing. It is the carbon intensity and cost structure of aluminium production. Nations that can offer low-carbon, competitively priced aluminium will hold decisive strategic leverage in the solar supply chain of the 2030s.

The EU's Conditional Incentive Architecture and Its Aluminium Paradox

European solar targets require an additional 4 to 10 million tonnes of aluminium to achieve the 320 GW deployment goal by 2025, with further compounding demand implied by the 600 GW target for 2030. Yet European primary aluminium capacity has declined by more than 30% over two decades, with a further 50% curtailment recorded since 2021 due to elevated energy costs.

This structural deficit creates a fundamental tension. The EU's conditional incentive model ties support to supply chain provenance and carbon intensity thresholds, yet the continent lacks the domestic aluminium production base to satisfy those provenance requirements at scale. Import reliance from China simultaneously contradicts the EU's Green Deal objectives and exposes the solar buildout to the same geopolitical concentration risks that energy dependence on Russian gas previously created.

The EU's policy response attempts to resolve this contradiction through conditional subsidies, but the energy cost problem driving smelter curtailments cannot be solved by incentive design alone. It requires a structural solution to industrial electricity pricing that remains politically and technically unresolved.

The next major ASX story will hit our subscribers first

Where Climate Policy and Aluminium Policy Collide

The Embedded Carbon Problem

Solar PV expansion under the IEA's 2°C scenario could embed up to 840 MtCO₂e in aluminium-related manufacturing alone. This creates a direct challenge to the lifecycle carbon credentials of solar energy: the metal enabling decarbonisation carries a significant carbon liability in its own production when sourced from coal-powered smelters.

Recycled aluminium offers the most structurally sound response to this challenge. Secondary production of aluminium requires approximately 95% less energy than primary smelting from bauxite. At scale, a shift toward recycled aluminium in solar frame manufacturing would simultaneously reduce the carbon intensity of solar PV production and reduce exposure to the geopolitical concentration risks associated with primary aluminium supply chains. The Clean Energy Council has similarly identified clean energy integration as foundational to a sustainable aluminium manufacturing future in Australia.

Policy Levers for Low-Carbon Aluminium Integration

Aligning solar subsidies and aluminium supply chains with decarbonisation goals requires policy interventions across multiple dimensions. Consequently, both government and industry must act in concert to address the following priorities:

- Prioritise recycled aluminium in solar frame specifications through green public procurement standards and tendering requirements

- Extend tax credit horizons to a minimum of 10 years, the threshold identified by industry consensus as necessary for new smelter investment decisions

- Mandate clean power inputs for aluminium smelters supplying solar manufacturers that receive public incentives

- Coordinate internationally on carbon border adjustment mechanisms to prevent carbon leakage through low-cost, high-carbon aluminium imports

- Develop aluminium-specific supply chain provenance standards embedded within solar incentive frameworks, rather than treating aluminium as a commodity afterthought

However, the success of these levers depends significantly on the participation of top aluminium producers who must align their own investment strategies with the decarbonisation requirements now embedded in solar procurement frameworks. Furthermore, emerging corporate initiatives such as the low-carbon aluminium venture between major industry players signal that commercial momentum is beginning to align with policy intent.

Frequently Asked Questions: Solar Subsidies and Aluminium Supply Chains

How do solar subsidies directly affect aluminium demand?

Subsidies accelerate solar installation targets, which proportionally increase demand for aluminium used in frames, mounting systems, and racking. Each gigawatt of solar capacity requires approximately 21,000 tonnes of aluminium, meaning subsidy-driven installation surges translate directly into aluminium procurement pressure across the full supply chain.

Why did China remove its VAT rebates on solar exports in 2026?

China's removal of VAT export rebates reflects a strategic shift from volume-led export growth toward margin discipline and domestic market consolidation. With 900 GW of manufacturing capacity already constructed, the priority has moved from global market capture to sustainable profitability and supply chain quality control.

What is the cost impact of diversifying away from Chinese aluminium and solar supply chains?

Independent supply chains outside China carry an estimated 30% cost premium under current market conditions. This premium narrows as Western subsidies scale but does not disappear without structural improvements in energy cost competitiveness for non-Chinese smelters.

How does aluminium's carbon footprint affect solar energy's environmental credentials?

Aluminium production accounts for approximately 1.1 billion tonnes of CO₂ annually. If solar expansion relies on coal-powered primary aluminium, the lifecycle carbon benefit of solar installations is materially reduced. Transitioning to recycled or renewably-powered primary aluminium is essential for solar to deliver its full decarbonisation potential. The Australian Government's green aluminium support programme reflects the growing policy recognition of this imperative.

Which policy mechanisms most effectively align solar subsidies with low-carbon aluminium supply?

Long-duration tax credits of 10 years or more, carbon border adjustments, green procurement mandates specifying recycled aluminium content, and coordinated international financing frameworks are considered the most effective tools for aligning solar subsidy design with low-carbon aluminium supply chain development.

Key Takeaways: The Strategic Realignment Underway in 2026

The data points defining this inflection moment are worth consolidating in a single view:

| Metric | Value |

|---|---|

| Aluminium per MW of solar capacity | ~21 tonnes |

| Solar PV share of renewables aluminium demand | ~87% |

| China's share of primary aluminium production | ~60% |

| EU aluminium capacity decline (20 years) | >30% |

| EU aluminium curtailment since 2021 | ~50% |

| Module price increase post-VAT removal | +9.3% |

| TOPCon module price (January 2026) | USD 0.086/W |

| TOPCon module price (projected year-end 2026) | USD 0.098/W |

| Non-China supply chain cost premium | ~30% |

| Global aluminium CO₂ emissions annually | ~1.1 billion tonnes |

For industry participants navigating this environment, four strategic imperatives emerge:

- Reframe aluminium as a transition-critical material, not a commodity input, in both procurement strategy and policy advocacy

- Stress-test supply chain concentration risk against scenarios involving Chinese export policy shifts, VAT changes, and geopolitical disruptions

- Prioritise recycled aluminium integration as both a cost management and carbon liability mitigation strategy

- Engage actively with subsidy policy design to ensure that solar incentive frameworks include supply chain provenance requirements and carbon intensity standards

The intersection of solar subsidies and aluminium supply chains is no longer a niche concern for materials specialists. It is a central strategic variable for every organisation operating in or investing in the global energy transition. The policy decisions being made in 2026 will define the cost structure, carbon integrity, and geopolitical resilience of solar energy for the decade ahead.

For ongoing coverage of aluminium's role in the global energy transition and solar PV supply chain dynamics, AL Circle publishes regular analysis across the aluminium value chain at alcircle.com.

Want to Track the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data across 30+ commodities to surface actionable opportunities the moment they're announced. Start your 14-day free trial at Discovery Alert today, or explore how historic discoveries have generated extraordinary returns for investors who positioned early.