July 8, 2026

The Copper Corridor Taking Shape in Oman's North Batinah Governorate

Across the global mining landscape, a quiet but meaningful reorientation is underway. International exploration capital, long concentrated in Latin America, sub-Saharan Africa, and Central Asia, is increasingly turning toward the Middle East — a region with deep geological heritage, improving investment frameworks, and strategic proximity to the world's largest copper-consuming economies. Understanding the mineral exploration importance of this shift is essential for investors tracking frontier opportunities.

The Solidcore Oman copper-gold project, formally centred on the Khabiyat deposit in North Al Batinah Governorate, crystallises this trend with unusual precision. It brings together a Kazakhstan-headquartered precious metals producer making its first move outside its home market and a state-backed Omani concession holder that has spent years systematically de-risking a geologically compelling licence area. Understanding what this joint venture actually represents, structurally and strategically, requires looking well beyond the headline agreement.

When big ASX news breaks, our subscribers know first

Why Oman's Copper Heritage Matters More Than Most Investors Realise

A Geological Province With Ancient Roots

Oman's relationship with copper extraction predates most of the world's major modern mining jurisdictions by millennia. Archaeological evidence points to active smelting operations in the Al Hajar Mountains stretching back more than four thousand years, with Omani copper traded across the ancient Gulf under the name of the land of Magan. This is not merely historical colour — it speaks directly to the geological richness of an ophiolite sequence that geologists regard as one of the world's most significant and best-exposed ancient oceanic crustal sections.

Ophiolites form when oceanic crust is thrust onto continental margins during tectonic collisions. Oman's Semail Ophiolite, which stretches across much of the northern mountain range, represents a near-complete cross-section of ancient oceanic lithosphere. Critically for exploration targeting, this environment is precisely the setting in which Volcanogenic Massive Sulphide, or VMS, mineralisation forms. Hydrothermal fluids venting through seafloor fractures deposit concentrated sulphide minerals containing copper, gold, zinc, and silver in discrete, often high-grade lenses.

VMS Deposits: What Makes Them Attractive and Technically Demanding

The VMS deposit characteristics found in Oman's ophiolite belt make it a globally recognised prospective address for exactly the style of mineralisation identified at Khabiyat. VMS deposits occupy a distinctive position in the copper exploration universe. Unlike large porphyry copper systems, which are typically lower grade but vast in scale, VMS deposits tend to be smaller, higher grade, and geometrically complex. The tradeoffs are significant:

- VMS ore bodies can carry copper grades materially above the global average, often exceeding 2% copper with meaningful gold and silver credits

- Their lenticular geometry means resource continuity is not guaranteed along strike or at depth without intensive drilling

- The multi-metal nature of VMS deposits creates valuation complexity, requiring copper-equivalent calculations to aggregate economic value across different payable metals

- Processing VMS ore typically requires flotation circuits capable of producing separate copper and zinc concentrates, adding capital intensity but also product flexibility

For investors evaluating the Solidcore Oman copper-gold project, these geological characteristics are foundational. The presence of VMS-style mineralisation in Oman's ophiolite setting does not guarantee a commercially viable deposit, but it does establish a scientifically credible exploration thesis backed by one of the most thoroughly studied geological sequences on earth.

The Khabiyat Earn-In: Anatomy of a Risk-Adjusted Entry

How Staged Investment Mechanics Protect Both Parties

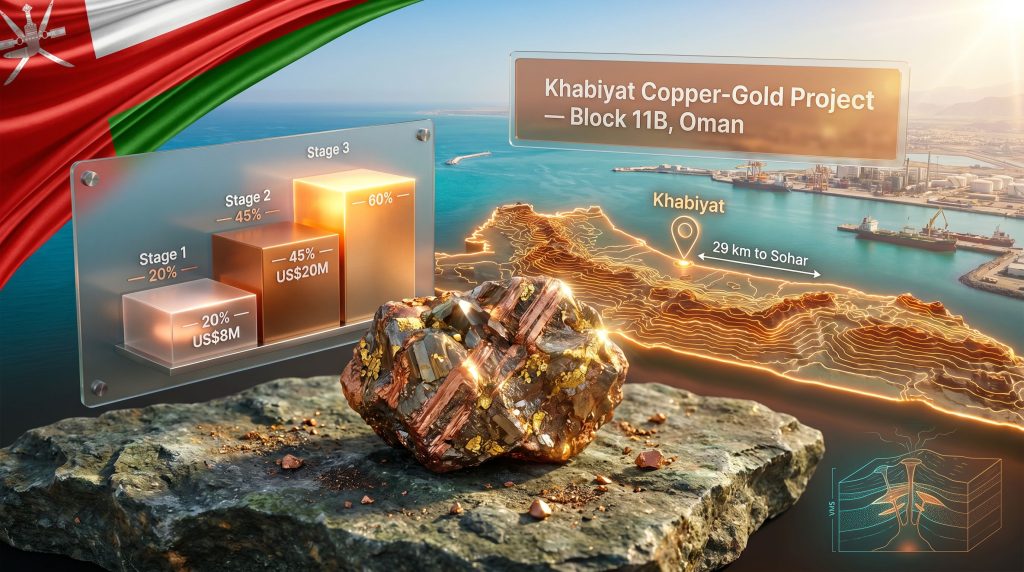

The agreement between Solidcore Resources and Minerals Development Oman is structured as a three-stage earn-in, a mechanism that functions very differently from a conventional acquisition. Rather than purchasing an equity interest outright, the incoming partner funds exploration and development activities to earn progressively larger ownership stakes tied to technical milestones. This model has become increasingly common in jurisdictions where state-owned entities hold mineral concessions, because it aligns incentives without requiring the sovereign party to relinquish control prematurely.

Earn-in structures are fundamentally about distributing geological risk over time. The incoming partner validates assumptions at each stage before committing the next tranche of capital, while the concession holder retains majority control until exploration materially de-risks the asset.

The Khabiyat earn-in breaks down across three clearly defined thresholds:

| Stage | Equity Earned | Exploration Investment | Cash to MDO | Primary Deliverable |

|---|---|---|---|---|

| Stage 1 | 20% | US$8 million | US$0.5M upfront + US$1.5M on completion | Exploration programme over up to two years |

| Stage 2 | Additional 25% (total 45%) | US$20 million | US$1.5M on proceeding | Additional drilling plus JORC Mineral Resource Estimate |

| Stage 3 | Additional 15% (total 60%) | CuEq resource-linked pricing | To be confirmed | Transition to project development |

An important and often overlooked detail within earn-in agreements of this type is that the cash payments flowing to MDO — totalling US$3.5 million across Stages 1 and 2 — are typically non-refundable regardless of exploration outcomes. This provides MDO with tangible financial compensation for its years of pre-investment exploration work, while Solidcore retains the option, not the obligation, to advance to each subsequent stage.

The JORC Resource Estimate as the Critical Value Inflection Point

The requirement to deliver a JORC-compliant Mineral Resource Estimate at Stage 2 deserves particular attention. The JORC Code, administered by the Joint Ore Reserves Committee and widely adopted across Australia, Asia, and the Middle East, establishes the internationally accepted methodology for classifying and publicly reporting mineral resources. Furthermore, classification progresses through three confidence levels:

- Inferred Resources — sufficient geological evidence to assume continuity, but limited data density

- Indicated Resources — enough data to apply assumptions about grade and tonnage with reasonable confidence

- Measured Resources — the highest confidence category, supported by closely spaced sampling and detailed geological modelling

For project financing purposes, lending institutions and project financiers typically require a material proportion of resources to sit within the Indicated or Measured categories before committing debt capital. Achieving a robust JORC estimate at Khabiyat would therefore not merely satisfy a contractual condition; it would fundamentally transform the project's bankability. Robust mining feasibility studies would then open the door to third-party financing structures that could fund the transition toward development.

MDO's Pre-Partnership Exploration Work: A Frequently Underappreciated Asset

One element of the Khabiyat story that tends to receive insufficient analytical attention is the scope of work MDO conducted before Solidcore arrived at the table. The exploration programme executed across the 84.5 square kilometre Block 11B licence area encompassed drilling campaigns, geological and geochemical studies, aerial and ground-based geophysical surveys, and satellite imagery interpretation. This multi-technique approach is sophisticated by any standard.

The practical significance of this pre-work is substantial. In jurisdictions where exploration data is scarce, incoming partners frequently spend the early stages of an earn-in simply understanding the regional geology. At Khabiyat, however, Solidcore enters with an existing dataset that narrows the aperture of geological uncertainty and allows exploration capital to be deployed more efficiently toward target drill testing rather than basic reconnaissance.

This positions the Khabiyat project as a genuinely de-risked entry point relative to typical greenfield exploration ventures, where the first stage of any earn-in is essentially speculation backed only by regional geological inference.

Solidcore's Strategic Logic: Why Oman and Why Now

Geographic Diversification as Balance Sheet Strategy

Solidcore Resources is primarily known as a Kazakhstan-focused gold producer. The company's publicly articulated 2024–2030 strategic framework targets a doubling of gold-equivalent output, with ambitions toward the one million ounce per annum threshold that separates mid-tier producers from genuine senior mining company status. Achieving that growth organically within Kazakhstan alone would require either significant new discoveries or the commissioning of large capital-intensive projects.

Geographic diversification addresses several constraints simultaneously:

- It reduces single-jurisdiction political and regulatory concentration risk

- It provides access to copper, a metal with a structurally different demand profile from gold that hedges the portfolio against precious metals price cycles

- It establishes a presence in a region where mining investment competition from established Western majors remains relatively limited

- It signals to institutional capital markets that Solidcore is pursuing a growth trajectory beyond Central Asia

Solidcore's first international venture has been characterised by the company's leadership as consistent with a strategy of disciplined growth and geographic diversification, with the project described as potentially evolving into a significant mining and processing hub for the Oman region. This framing suggests the company views Khabiyat not merely as a single asset but as a platform from which broader regional activity could be developed over time.

Why the Sohar Proximity Matters Commercially

The Khabiyat licence area sits approximately 29 kilometres from Sohar, home to one of Oman's principal industrial and port complexes. For a copper concentrate project — which is the likely initial product form for any VMS deposit brought into production — proximity to export infrastructure is not a secondary consideration. It is frequently among the top three variables determining project economics.

Copper concentrate typically carries freight costs that are sensitive to haul distance. Moving concentrate by road to a deepwater port capable of loading bulk carrier vessels materially affects the net revenue per tonne of metal produced. The Sohar location, combined with Oman's planned minerals seaport development for which a tender has already been launched, suggests that the infrastructure environment surrounding the Solidcore Oman copper-gold project could improve substantially over the exploration and development timeline.

Scenario Modelling: Three Plausible Outcomes for the Khabiyat Project

Responsible analysis of any early-stage exploration project requires acknowledging the full range of possible outcomes rather than anchoring to optimistic projections. The following scenarios reflect the genuinely contingent nature of the project at this stage.

Scenario 1: Full Validation and Development Progression

Drilling confirms high-grade VMS mineralisation at depth and along strike within the Block 11B licence. Solidcore completes all three earn-in stages, acquires 60% ownership, and the joint venture advances toward a pre-feasibility study. Proximity to Sohar supports development of an integrated processing facility. Indicative timeline to a production decision sits in the six to ten year range from Stage 1 commencement, reflecting the typical cadence of VMS project development in comparable jurisdictions.

Scenario 2: Partial Validation and Joint Venture Restructuring

Stage 1 and Stage 2 drilling yields positive but sub-threshold results. Solidcore retains a 45% interest following Stage 2 completion, and the joint venture pursues a scaled development concept or invites a third-party technical partner to participate. MDO retains majority control and manages any subsequent partnership restructuring.

Scenario 3: Stage 1 Exit

Exploration data from Stage 1 does not justify the US$20 million Stage 2 commitment. Solidcore holds a 20% interest and elects not to proceed. MDO retains the Block 11B concession with a materially improved geological dataset and a strengthened basis for marketing the project to alternative international partners. The US$2 million in cash payments received from Solidcore remains with MDO regardless of outcome.

Disclaimer: These scenarios are illustrative projections based on structural analysis of the earn-in agreement and general mining industry precedent. They do not constitute investment advice. Exploration outcomes are inherently uncertain and actual results may differ materially from any projection.

The next major ASX story will hit our subscribers first

What This Deal Signals for GCC Mining Investment

The Solidcore-MDO partnership is not occurring in isolation. It reflects a broader and accelerating trend of non-Western mining capital entering Gulf Cooperation Council mineral concessions, a shift driven by improving regulatory transparency, state entity professionalism, and the strategic appeal of the region's geological endowment. In addition, the growing critical minerals demand from electric vehicles, grid infrastructure, and renewable energy systems is sharpening global interest in early-stage copper exploration across politically stable Middle Eastern jurisdictions.

Saudi Arabia's mining sector push under Vision 2030, with its rapidly expanding Saudi mining licences programme, the UAE's emerging critical minerals agenda, and Oman's own Vision 2040 diversification framework are collectively reshaping regional perceptions of the GCC as a mining investment destination. Oman's ophiolite copper belt, its existing export infrastructure at Sohar, and MDO's increasingly sophisticated approach to international partnership structures position the country as a credible participant in that global competition for copper development capital.

The Khabiyat joint venture, whatever its ultimate geological outcome, represents a meaningful data point in that larger story. For investors and industry observers tracking the evolution of GCC mining, Zawya's dedicated mining projects coverage provides ongoing reporting on concession activity, infrastructure tenders, and international partnership announcements across the region.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across copper, gold, and more than 30 other commodities — turning complex geological data into clear, actionable investment insights. Explore how historic discoveries have generated substantial market returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.