July 17, 2026

Frontier Basins and the Search for the Next Guyana

Every decade or so, global oil markets witness the emergence of a genuinely transformative frontier province. Guyana in the 2010s rewrote the economics of deepwater exploration. Mozambique briefly promised to do the same for East African gas. Now, in 2026, attention is turning toward a coastline that has barely been touched by modern drilling technology: Somalia's Indian Ocean deepwater, where the prospect of a Somalia offshore oil discovery is generating serious strategic interest.

The timing is not coincidental. With the Strait of Hormuz handling roughly 20% of global seaborne oil trade and geopolitical tensions in the Middle East repeatedly threatening supply continuity, energy importers across Asia are actively seeking crude sources that can bypass the chokepoint entirely. Furthermore, Somalia's geographic position, sitting directly across the Arabian Sea from India's refining complex, makes any potential Somalia offshore oil discovery strategically significant in ways that a comparable find in, say, the South Atlantic simply would not be. The wider geopolitical landscape for energy security is shifting rapidly, making frontier exploration increasingly consequential.

When big ASX news breaks, our subscribers know first

The Curad-1 Well: Technical Scale and What It Represents

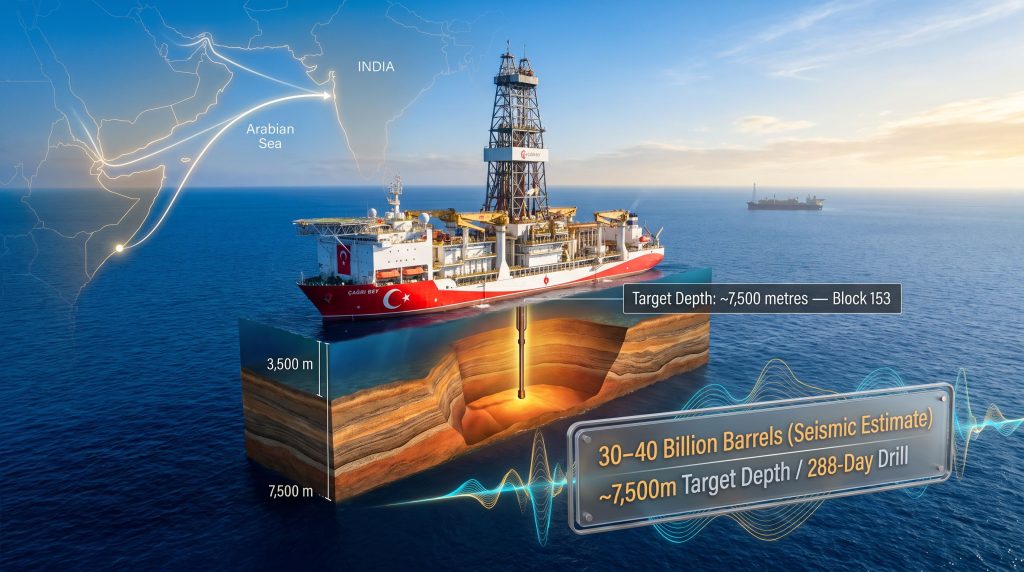

The Curad-1 exploration well is not a routine frontier test. Its specifications place it among the most technically demanding offshore drilling efforts ever undertaken anywhere in the world.

Key Technical Parameters

| Parameter | Detail |

|---|---|

| Location | Approx. 372 km northeast of Mogadishu |

| Water depth | Approx. 3,500 metres |

| Target depth | Approx. 7,500 metres |

| Drilling duration | Up to 288 days |

| Seismic coverage | 4,464 km² of 3D data (Blocks 142, 152, 153) |

| Seismic acquisition period | October 2024 to June 2025 |

| Spud date | April 2026 |

| Operator drillship | Çağrı Bey (TPAO-owned ultra-deepwater vessel) |

The seismic acquisition programme, conducted by TPAO's vessel Oruc Reis, covered three offshore blocks. Early interpretation of Blocks 152 and 153 identified geological structures with characteristics analogous to producing basins in Yemen, Tanzania, and Mozambique. That is an encouraging geological fingerprint, though it is important to note that seismic analogues are indicators of prospectivity, not proof of commercial hydrocarbons.

Critical Context: Only eight wells have ever been drilled in Somalia's offshore waters historically, with just two in the Somali Basin itself. None has resulted in a commercial discovery. The geological dataset underpinning Curad-1 is therefore exceptionally thin by the standards of any mature or even moderately explored basin.

What the Numbers Do and Don't Tell Us

Speculative resource estimates circulating around Somalia's offshore range widely, reflecting the fundamental uncertainty of pre-discovery frontier assessment:

| Estimate | Range | Basis | Status |

|---|---|---|---|

| Seismic-derived basin potential | 30–40 billion barrels | 3D seismic interpretation | Unproven, exploratory |

| Upper-bound geological speculation | Up to 100 billion barrels | Extrapolated geological modelling | Highly speculative |

| Block-level prospect estimate | ~15 billion barrels | Liberty Petroleum block data | Exploratory, unconfirmed |

| Earliest production scenario | 2034–2036 | Development timeline modelling | Conditional on discovery |

Disclaimer: None of the figures above represent proven, probable, or possible reserves under any recognised classification standard. All estimates are pre-discovery, seismic-based assessments subject to substantial revision following drilling results.

Somalia's Fiscal Architecture: Designed to Attract Risk Capital

Understanding why a state-owned company would commit an ultra-deepwater drillship to one of the world's least-explored basins requires understanding the financial terms on offer. Somalia's fiscal framework has been structured to absorb exploration risk on behalf of the operator.

How the Production Sharing Agreement Works

Somalia's 2023 revised Production Sharing Agreement introduced a flat 5% royalty on both oil and gas, replacing an earlier sliding-scale structure. Cost petroleum recovery is capped at 70% for oil and 80% for gas, meaning operators can recover a high proportion of exploration and development expenditure before profit-sharing begins.

The bilateral terms specifically governing Curad-1 go further still. TPAO is permitted to recover up to 90% of production after royalties, with several standard bonus obligations and administrative charges waived entirely. This is not a standard commercial arrangement; it reflects the extraordinary risk premium attached to deepwater frontier drilling in a country that has had no functioning oil sector for over three decades.

Frontier Fiscal Benchmarks Compared

| Country/Basin | Royalty Rate | Cost Recovery Cap | Context |

|---|---|---|---|

| Somalia (2023 PSA) | 5% flat | 70% oil / 80% gas | Pre-discovery frontier |

| TPAO-Somalia bilateral | 5% (waived charges) | Up to 90% post-royalty | Extraordinary frontier risk terms |

| Guyana (original Stabroek) | ~2% | High | Pre-discovery frontier |

| Guyana (post de-risking) | ~10% | Revised | After multiple major finds |

| West Africa deepwater (typical) | 5–8% | Varies | Comparable frontier offshore |

The Guyana comparison is instructive. When ExxonMobil and partners first entered Guyana's Stabroek block, the royalty was approximately 2% and cost recovery terms were highly investor-friendly. As successive major discoveries de-risked the basin, Guyana progressively renegotiated terms, ultimately introducing a 10% royalty for new licences. Somalia's current 5% royalty sits between these two reference points, suggesting the government believes it is offering terms that are competitive but not as distorted as the original Guyana deal.

Strategic Insight: If Curad-1 confirms a large discovery, Somalia will almost certainly face pressure to renegotiate fiscal terms in subsequent licensing rounds, following the same trajectory as Guyana. Early licence holders would retain their original terms, creating a potential windfall for first-mover operators.

TPAO's Strategic Calculus: Why Turkey Is Taking This Risk

Turkey's state oil company TPAO has traditionally operated as a minority participant in established producing projects. Its stakes in Azerbaijan's Shah Deniz gas field and the Azeri-Chirag-Gunashli oil complex are representative of this approach: meaningful exposure to proven assets without the full operational and geological burden of operatorship.

Somalia represents a fundamental departure from that model. TPAO is simultaneously the operator, the seismic data owner, the drillship provider, and a participant in broader Turkish infrastructure and security involvement in Somalia. The only comparable precedent in TPAO's recent history is its Black Sea programme, where the Tuna-1 well led to the Sakarya gas discovery, currently the largest natural gas find in Turkish history.

The motivations behind this strategic pivot are layered:

- Turkey processes a significant volume of Russian, Iraqi, and Kazakh crude grades at its domestic refineries. A Somali crude grade with similar characteristics could provide a non-sanctioned, geographically diversified alternative.

- Equity crude ownership provides supply security advantages that purchase agreements cannot replicate.

- Successful frontier operatorship would substantially enhance TPAO's international standing and technical credibility.

- The bilateral framework embeds Turkish commercial interests in Somalia's emerging energy governance structure, which carries longer-term strategic implications beyond the Curad-1 well itself.

It is worth noting, however, that Somali crude routed to Turkey would still transit Bab el-Mandeb and the Suez Canal, meaning it does not resolve Turkey's own chokepoint exposure in the way it would for Indian buyers.

The Oil vs. Gas Asymmetry: Why Crude Is the Commercial Prize

Curad-1 may encounter both oil and gas accumulations, but the commercial economics strongly favour an oil discovery. This asymmetry is rarely discussed in frontier exploration coverage but is fundamental to assessing development viability.

Why oil works in Somalia's context:

- A large oil discovery can be developed via a Floating Production, Storage and Offloading (FPSO) vessel, enabling direct offshore crude loading without fixed pipeline infrastructure.

- Comparable ultra-deepwater FPSO developments in Angola and Brazil have demonstrated breakeven prices of approximately $40–$45 per barrel, but only where recoverable resources exceed 300 million barrels and reservoir complexity is manageable.

- India's proximity provides an immediate large-volume off-take market with minimal transit risk.

Why gas faces a structurally harder path:

- Somalia has no domestic gas consumption base capable of anchoring a development.

- There is no offshore pipeline network connecting Somalia to regional gas markets.

- Commercialisation would require Floating LNG technology and a substantially larger reserve base than oil development demands.

- Regional LNG market implications are already shaped by established East African producers, creating competitive barriers for a new entrant grade.

The practical implication is that even a moderate oil discovery could be commercially viable under the current fiscal terms, while a gas-weighted result would likely require a far larger accumulation before development pencils out.

Somalia's Contested Licensing History: Legal Complexity Beneath the Seabed

The geological prospectivity of Somalia's offshore acreage has been understood in broad terms since the 1950s. By the late 1980s, major international operators including Conoco, Chevron, Eni, Shell, and ExxonMobil had collectively secured concessions covering close to half of Somalia's landmass and offshore territory.

When Somalia's state collapsed in 1991, operators did not formally relinquish their acreage. Instead, most declared force majeure, a legal mechanism that suspends contractual obligations under extraordinary circumstances without terminating the underlying agreement. This left legacy rights legally dormant but not extinguished, creating a complex inheritance problem for Somalia's eventual re-emergence as an exploration jurisdiction.

Shell and ExxonMobil subsequently reached a roadmap agreement with the reconstituted federal government addressing their historical offshore interests. Newer licences were awarded to companies including Coastline Exploration. Simultaneously, the semi-autonomous administrations of Puntland and Somaliland began granting their own licences to operators including Genel Energy — awards that the federal government in Mogadishu formally rejected as unauthorised.

Legal Risk Callout: Somalia's offshore licensing map contains overlapping federal awards, legacy force majeure concessions, and competing regional permits. Any development financing from international institutions will require full jurisdictional clarity before commitments can be made. This legal complexity represents a risk layer that sits entirely outside the geological uncertainty of Curad-1.

The next major ASX story will hit our subscribers first

Somalia vs. Uganda: Two Competing East African Oil Development Models

A Somalia offshore oil discovery at meaningful scale would place the country in direct structural competition with Uganda's Lake Albert project for Asian export market share. The two developments represent contrasting approaches to East African crude monetisation.

| Factor | Somalia Offshore | Uganda Lake Albert |

|---|---|---|

| Development stage (2026) | Exploration drilling underway | FID reached; EACOP under construction |

| Peak production target | 200,000–300,000 b/d (if discovered) | ~230,000 b/d |

| Export infrastructure | FPSO (offshore loading) | 1,443 km heated East African Crude Oil Pipeline to Tanga |

| Breakeven complexity | Ultra-deepwater FPSO capex | Landlocked logistics; pipeline operating costs |

| Timeline to first oil | Potentially 2034–2036 | Mid-to-late 2020s (pipeline dependent) |

| Primary export market | India and Asia (Arabian Sea) | Asia via Indian Ocean ports |

| Geopolitical complexity | Federal-regional jurisdiction disputes | Multi-country pipeline diplomacy |

The comparison highlights a non-obvious insight: Uganda's pipeline model, despite avoiding deepwater drilling costs, carries extraordinary operational complexity. The East African Crude Oil Pipeline must maintain crude at elevated temperatures throughout its entire length due to the high wax content of Ugandan oil. This heating requirement creates ongoing operating costs that have no equivalent in an FPSO-based offshore development. Consequently, Somalia's approach, if a discovery materialises, would be logistically simpler at the export stage despite higher upstream capital requirements.

The India Demand Anchor: Geography as Strategic Advantage

No discussion of a potential Somalia offshore oil discovery is complete without examining the demand side of the equation. India is not merely the nearest large refining market; it is structurally the most motivated buyer of a new non-Hormuz crude stream.

Several factors converge to make India the natural primary off-take market for any Somali production:

- Geographic proximity: The Arabian Sea crossing from Somalia's offshore blocks to India's west coast refining complex is among the shortest conceivable supply chains for a frontier deepwater basin.

- Supply concentration risk: India currently sources approximately 60% of its crude imports from Russia, a concentration that policymakers have identified as a strategic vulnerability given ongoing sanctions risk.

- Refinery flexibility: Indian refineries process a broad range of crude grades, reducing the technical barriers to absorbing a new Somali grade.

- Hormuz exposure: India urging shipowners to avoid deploying nationals on Hormuz voyages reflects a genuine policy concern about chokepoint dependency. Somali crude requires no Hormuz transit for Indian-bound shipments.

The proposed 700,000 barrels per day refinery at Lamu in Kenya adds a further regional dimension. Neither this facility nor a developed Somali offshore field is likely to be operational before the mid-2030s, creating a potential timeline alignment. A scenario in which Somali crude partially supplies regional East African refining rather than flowing entirely to Asia would materially alter the trade economics.

Risk Matrix: What Could Go Wrong

Frontier exploration carries layered risks that operate independently of each other. A realistic assessment of Curad-1's potential outcomes requires understanding all of them simultaneously.

Geological Risk

The Somali Basin's geological dataset is among the thinnest of any active frontier exploration programme globally. Seismic analogues to Yemen, Tanzania, and Mozambique are suggestive but not deterministic. Ultra-deepwater reservoirs can harbour structural complexity that only drilling reveals. The presence of hydrocarbons does not guarantee commercial concentrations.

Political and Revenue Risk

Large parts of Somalia remain outside effective federal government control. Revenue-sharing arrangements between Mogadishu and regional administrations in Puntland and Somaliland are structurally unresolved. The historical precedent from resource-rich conflict-affected states is mixed: oil revenue has sometimes consolidated state authority and sometimes intensified competition for territorial control. Furthermore, broader oil market impacts from geopolitical disruption could affect the commercial viability of any discovery at the time of development.

Commercial Threshold Risk

Ultra-deepwater development economics demand scale. A discovery of fewer than 300 million recoverable barrels at manageable reservoir complexity may not achieve commercial viability even under Somalia's generous fiscal terms. Sub-commercial discoveries are a routine outcome in frontier exploration and do not necessarily indicate geological failure across the broader basin.

Regulatory and Financing Risk

International financing institutions applying environmental, social, and governance standards will require full jurisdictional clarity on licensing, community consultation frameworks, and revenue management governance before committing to project finance. Somalia's institutional capacity to meet these requirements is still developing. In addition, an oil price shock during the development phase could fundamentally alter project economics for any discovery made today.

Frequently Asked Questions: Somalia Offshore Oil Discovery

Has Somalia confirmed an offshore oil discovery?

No commercial discovery has been confirmed as of mid-2026. The Curad-1 well began drilling in April 2026 and represents Somalia's first serious modern deepwater exploration campaign. All reserve estimates remain speculative, derived from seismic interpretation rather than drilling results.

Who is drilling for oil in Somalia?

Turkey's state-owned energy company TPAO is operating the Curad-1 well under a bilateral agreement with Somalia's federal government, using its own ultra-deepwater drillship Çağrı Bey.

When could Somalia realistically begin oil production?

If Curad-1 confirms a commercially viable find, appraisal drilling, development engineering, FPSO procurement, and regulatory processes would push first production to approximately 2034–2036 at the earliest. Peak production of 200,000–300,000 barrels per day represents a plausible scenario for a large discovery.

Why does Somalia's offshore matter for India specifically?

Somalia sits directly across the Arabian Sea from India's west coast refineries, making it one of the closest potential new crude sources for India. It also offers a supply route that completely bypasses the Strait of Hormuz, a chokepoint that India's policymakers have increasingly flagged as a strategic vulnerability given the country's significant dependence on Middle Eastern crude flows. Somalia hopes for results from the Türkiye-led offshore drilling programme by year-end, which could substantially clarify the country's upstream potential.

The Bigger Picture: Frontier Exploration in a Geopolitically Fragmented World

What Somalia's current exploration moment reveals most clearly is a structural shift in who takes frontier risk and why. The international oil majors that dominated frontier exploration through the 1980s have largely withdrawn from the highest-risk, pre-discovery end of the exploration spectrum, preferring to acquire de-risked acreage or concentrate capital in established producing provinces.

The vacuum has been filled by state-owned companies from emerging energy powers — Turkey, China, and India among them — for whom resource security and geopolitical positioning carry value that does not appear in a conventional net present value calculation. TPAO's willingness to deploy its own drillship, its own seismic vessel, and its own capital into Somalia's frontier reflects this logic precisely.

The outcome of Curad-1 will test whether this model can deliver what conventional IOC-led frontier exploration has repeatedly failed to achieve in Somalia. If it succeeds, it will not only establish a new oil province but also validate a state-to-state exploration model that other resource-rich frontier nations will be watching closely.

Final Note: This article contains forward-looking analysis, scenario modelling, and speculative geological assessments. Nothing in this article constitutes investment advice or a recommendation to buy or sell any security. All resource estimates for Somalia's offshore are pre-discovery and unproven. Readers should conduct independent due diligence before making any investment decisions related to companies or projects discussed herein.

Want to Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, turning complex data into actionable insights for investors at every level — explore historic discoveries and their extraordinary returns to understand the potential at stake, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.