May 13, 2026

When Energy Chokepoints Redraw the Map of Global Commodity Trade

Every few years, a single geographic bottleneck reminds energy markets just how fragile the architecture of global supply truly is. The Persian Gulf's maritime corridor has played this role repeatedly across modern history, but the scale and complexity of the current standoff centred on the Strait of Hormuz is generating market responses that differ meaningfully from prior episodes. This time, the reverberations are reaching far beyond oil markets, cascading through liquefied natural gas pricing, bulk shipping rates, and ultimately into the global thermal coal trade in ways that are reshaping export opportunities for producers operating thousands of kilometres from the conflict zone.

For South Africa, Africa's largest coal producer, the confluence of Strait of Hormuz tensions and South Africa coal exports has created a demand environment that analysts would not ordinarily associate with the shoulder season between northern hemisphere winter heating and summer cooling. Understanding why this moment is different, and why geography and logistics will ultimately determine how much of this opportunity South Africa can actually capture, requires working through the mechanics of energy substitution, freight market dynamics, and the stubborn realities of rail infrastructure.

When big ASX news breaks, our subscribers know first

The Mechanics of Energy Substitution: Why Gas Disruption Becomes Coal Demand

The Strait of Hormuz is the world's single most critical maritime energy passage, responsible for approximately 20% of global oil shipments and a substantial share of liquefied natural gas flows from Gulf producers. When this corridor is disrupted, the consequences do not stop at petroleum. Gas-fired power generators across Asia and Europe that rely on LNG sourced from Gulf producers face immediate procurement pressure, triggering a search for alternative fuel inputs. The LNG supply outlook for 2025 and beyond had already signalled tightening conditions, making this disruption particularly consequential.

The substitution arithmetic is striking. Navios Partners CEO Angeliki Frangou conveyed to the Financial Times that the energy replacement ratio sits at roughly two tonnes of coal for every tonne of gas displaced. This is not simply a volume calculation. It reflects the lower energy density of coal relative to gas, meaning that utilities switching from gas to coal must secure and transport significantly larger physical quantities of fuel to maintain equivalent generation output. The practical consequence is that even a partial interruption to Hormuz gas flows generates a disproportionate demand signal in global coal markets.

The substitution ratio matters because it acts as a demand multiplier. A moderate gas supply disruption translates into an outsized coal procurement surge, amplifying price signals and absorbing available shipping capacity far faster than a simple tonne-for-tonne replacement would suggest.

The current confrontation involving US naval operations, Iranian maritime responses, and multi-party military deployments has generated a fragile and volatile shipping environment. The introduction of advanced submarine technology modelled on North Korean designs adds a layer of unpredictability that distinguishes this episode from historical Hormuz flashpoints, where diplomatic de-escalation timelines were more legible to markets. Energy buyers are responding with procurement urgency rather than patience, pulling coal volumes forward in ways that are distorting typical seasonal patterns.

Safe-haven demand has simultaneously driven spot gold to $4,723.40 per ounce, while US gasoline prices have surged by more than $1.50 per gallon, with forecasts projecting prices beyond $5.00 per gallon by mid-2026 if the strait remains effectively closed. The previous US gasoline price peak of $5.02 per gallon was recorded in 2022. These simultaneous signals across energy, metals, and refined products markets confirm that this is not a localised disruption but a systemic shock being priced across multiple asset classes.

Coal Demand in 2026: Breaking the Seasonal Calendar

April and May typically represent the quietest stretch of the annual coal trade calendar. Northern hemisphere heating demand recedes, industrial activity follows moderate seasonal patterns, and utilities draw down stockpiles accumulated during winter procurement cycles. This year, the pattern has broken decisively.

Global coal imports for May 2026 are tracking toward their third-highest monthly total on record, according to the Financial Times citing pricing intelligence firm Argus. This is a statistically significant anomaly that reflects the convergence of several forces simultaneously overriding seasonal norms.

Across Asia, governments have moved rapidly to restore coal generation capacity that had been either restricted or placed in operational reserve:

- South Korea lifted seasonal caps on coal-fired power generation in March 2026, reversing a policy that had been used to manage air quality during lower-demand periods.

- Thailand reactivated dormant coal plant capacity that had been held in reserve, signalling that energy security concerns were outweighing decarbonisation commitments in the near term.

- Vietnam and Japan both increased coal-fired generation output, adding to procurement volumes flowing through international shipping lanes.

The combined effect was visible in shipping data. According to the Baltic and International Maritime Council (BIMCO), coal shipments to Japan, South Korea, and the European Union rose 27% year-on-year in April 2026. This is a freight market signal of genuine demand rather than speculative inventory building, particularly given the simultaneous surge in bulk carrier rates.

Supply Compression: The Indonesia and China Variables

Demand acceleration alone does not fully explain the tightness developing in global thermal coal markets. Supply-side disruptions are compounding the pressure from the buyer side, with coal supply challenges emerging from multiple directions simultaneously.

Indonesia, the world's largest coal exporter, introduced export restrictions in April 2026, reducing the volume of Indonesian coal available to international buyers. The mechanism mirrors restrictions that Indonesia has deployed previously, typically involving domestic market obligation requirements that divert coal to state-controlled utilities before export licences are granted. The timing is particularly consequential given that Indonesian coal was already facing a sharp freight cost disadvantage.

| Exporter | Freight Rate Change vs. February 2026 | Key Factor |

|---|---|---|

| Indonesia | Up 60-75% | Export restrictions plus distance premium |

| Australia | Up 40-50% | Strong demand but high origin freight cost |

| South Africa | Relatively improving | Competing origin costs rising faster |

| Russia | Sanctioned in key markets | Geopolitical exclusion from Western buyers |

| Colombia | Reduced availability to select markets | Diplomatic constraints |

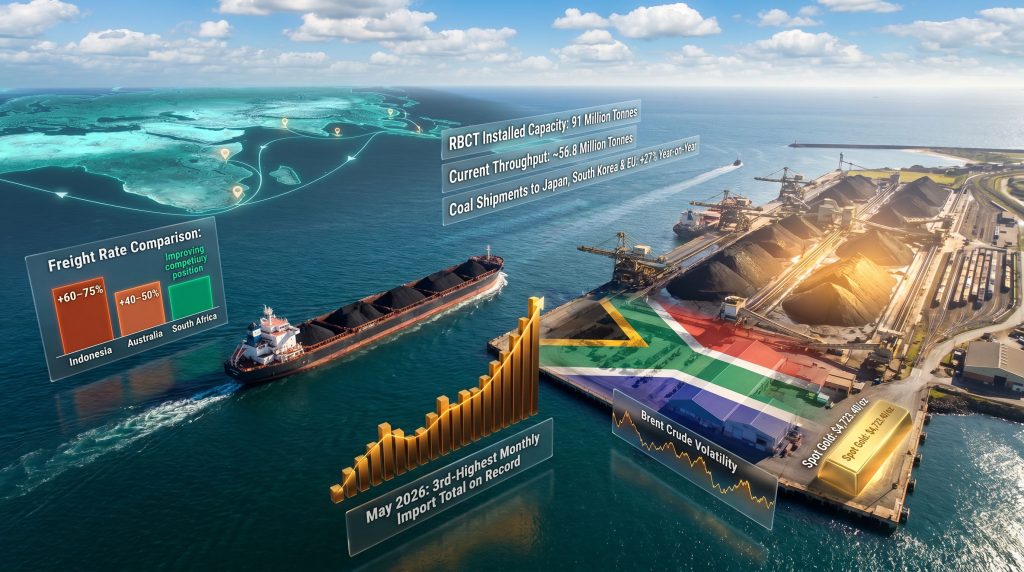

Medium-sized bulk carrier freight rates overall are running approximately 50% above February 2026 levels, a freight market condition that reflects genuine physical demand rather than paper positioning. When shipping costs rise this sharply, the origin of coal becomes a meaningful competitive variable. Producers whose delivered cost to key markets rises less than their competitors gain relative market share even without changing their own pricing.

China's role in the tightening adds another layer. Gulf-linked petrochemical shortages have accelerated a domestic shift toward coal-to-chemicals production, a segment of Chinese heavy industry that converts coal into petroleum-derived chemical feedstocks. This increases Chinese domestic coal consumption, reduces the volume of coal available for potential re-export or competitive pressure on international markets, and adds incremental demand to an already constrained global supply picture.

South Africa's Coal Export Architecture: Scale, Concentration, and Constraint

South Africa occupies a structurally important position in global seaborne coal trade, holding approximately 4.5% of global market share and ranking among the world's top five seaborne coal exporters. Coal is not merely an export commodity for the South African economy. It is the fuel source powering roughly 80% of domestic electricity generation through Eskom's fleet of coal-fired power stations, creating a dual function that complicates any simple narrative about redirecting volumes toward export markets during demand spikes.

Approximately one-third of total South African coal production flows to export markets, with annualised volumes estimated at around 72 million tonnes in 2025. The Richards Bay Coal Terminal serves as the dominant export gateway, handling close to 94% of all outbound coal shipments and ranking as one of the largest coal export terminals anywhere in the world.

The geographic concentration of South African coal exports is striking:

| Destination | Share of Exports | Key Buyers |

|---|---|---|

| Asia | ~80% | India (~46%), South Korea, Pakistan, Vietnam |

| Europe | ~10% | Multiple EU member states |

| Africa | ~10% | Regional buyers |

India's position as the dominant buyer, absorbing approximately 46% of total export volumes, reflects both the proximity advantage of Indian Ocean routing from Richards Bay and India's structural dependence on thermal coal for base-load power generation. India's import volume from South Africa reached 21.3 million tonnes in the first nine months of 2024, representing an 8.1% year-on-year increase, demonstrating that demand growth from this anchor buyer was already underway before the current Hormuz disruption intensified procurement urgency further.

European demand presents a more volatile picture. Following sanctions on Russian coal after 2022, European buyers pivoted sharply toward South African supply, with volumes rising 655% to 17.6 million tonnes in 2023. That surge proved temporary. By the first nine months of 2024, EU import volumes had contracted 64% to 1.9 million tonnes, reflecting both European efforts to diversify away from coal dependency and the partial restoration of alternative supply channels. The pattern illustrates a critical dynamic: geopolitical demand windows can open very quickly and close equally fast.

The Historical Export Trajectory

| Period | Export Volume | Defining Trend |

|---|---|---|

| 2023 | ~60.8 million tonnes | EU emergency surge; India purchases 27.6M tonnes |

| January to September 2024 | 43.9 million tonnes (-2.5% year-on-year) | EU volumes collapsed; India growth continued |

| 2025 (annualised) | ~72 million tonnes | RBCT throughput at ~56.8M tpa; export value ~ZAR 99 billion |

The Infrastructure Ceiling: Why RBCT's Nameplate Capacity Is Not the Real Limit

Richards Bay Coal Terminal was engineered to handle 91 million tonnes per annum, one of the largest design capacities of any coal export facility globally. The gap between this installed capacity and actual 2025 throughput of approximately 56.8 million tonnes represents more than a technical underperformance statistic. It is the quantified cost of the Transnet Freight Rail bottleneck that has persistently constrained South Africa's coal export ambitions. Furthermore, these resource export challenges are not unique to South Africa, though the specific rail constraints make the local situation particularly acute.

South Africa's primary coal export terminal is operating at roughly 62% of its nameplate capacity. The gap between actual throughput and theoretical maximum represents tens of millions of tonnes of export opportunity left unrealised annually, not because of terminal limitations, but because insufficient coal is arriving by rail.

The logistics failure is multi-dimensional. Infrastructure theft and vandalism along the rail corridor connecting inland collieries to the coast have been persistent problems, with copper cable theft and equipment sabotage regularly disrupting service. Ageing rolling stock and deferred maintenance programmes have compounded operational inefficiencies. While Transnet has reported incremental improvements in rail performance, the pace of recovery has consistently lagged the scale of the demand opportunity.

The revenue arithmetic of closing even part of this gap is significant. At a benchmark thermal coal price of approximately $90 per tonne (compared to $122 per tonne in 2023), each additional 10 million tonnes of export volume generates approximately $900 million in incremental export earnings. The full theoretical gap of 34 million tonnes between current throughput and nameplate capacity represents approximately $3 billion in additional annual export revenue at current prices, a figure that provides context for the urgency with which logistics reform discussions should be approached.

What Realistic Capacity Improvement Would Look Like

Rather than targeting the theoretical maximum immediately, a phased improvement framework might consider three sequential stages:

- Security intervention: Deploying enhanced protection along rail corridors to reduce theft and vandalism disruption, which could recover several million tonnes of throughput relatively quickly without capital-intensive infrastructure investment.

- Rolling stock rehabilitation: Accelerating the maintenance cycle for existing locomotives and wagons to reduce unplanned downtime and improve schedule reliability on the coal line.

- Capacity expansion investment: Longer-term investment in rail infrastructure upgrades and new rolling stock procurement to sustainably lift throughput toward RBCT's 91-million-tonne ceiling.

Even lifting throughput to 80% of design capacity, approximately 73 million tonnes, would represent an additional 16 million tonnes of annual export potential from current levels. At $90 per tonne, that incremental volume translates to roughly $1.4 billion in additional export earnings, a compelling economic case for prioritising logistics investment.

The Competitive Window: Why South Africa's Relative Position Is Improving

The freight rate movements reshaping global coal trade are not uniform across origins. Because Indonesian and Australian shipping costs to Asian markets have risen 60-75% and 40-50% respectively above February 2026 baseline levels, South Africa's delivered cost position relative to these key competitors has improved even without any change in South African mine-gate pricing. This is the freight rate arbitrage dynamic that makes the current environment particularly significant for South African coal producers and directly relevant to the broader commodity price impact on mining company performance.

South Africa's track record in filling supply gaps created by geopolitical disruption provides additional context. By late 2025, South Africa had become the leading supplier of thermal coal to Israel after Colombia halted its shipments, demonstrating that South African mining companies are operationally willing and capable of redirecting volumes toward markets experiencing sudden supply voids. This precedent is analytically relevant: the Hormuz disruption creates a structurally similar dynamic at a far larger scale, with Asian utilities urgently seeking to diversify away from gas-dependent generation.

Competitive Positioning Across Origin Countries

| Exporter | 2026 Competitive Positioning | Primary Constraint |

|---|---|---|

| Indonesia | Freight costs up 60-75%; export restrictions active | Policy-driven supply reduction |

| Australia | Freight costs up 40-50%; competitive but expensive | Distance premium to Asian buyers |

| Russia | Excluded from key Western markets | Geopolitical sanctions |

| Colombia | Reduced availability to certain markets | Diplomatic considerations |

| South Africa | Improving freight competitiveness; supply gap opportunity | Transnet rail bottleneck |

The next major ASX story will hit our subscribers first

The Broader African Commodity Positioning Dynamic

The Hormuz crisis does not exist in isolation from broader patterns in how Middle Eastern energy disruptions redirect global commodity procurement. Africa's oil producers, including Angola, Nigeria, and Algeria, have historically benefited from Gulf supply shocks as buyers seek alternative crude sources. Saudi Aramco has reportedly warned of potential losses of 100 million barrels weekly if the Strait remains closed, a figure that illustrates the scale of supply risk now being priced into global energy markets. The resulting supply chain disruption is reverberating across industries far removed from the Gulf itself.

For South Africa specifically, the dual role of coal creates a tension that policymakers must navigate carefully. Redirecting export volumes during a demand spike generates valuable foreign exchange earnings and strengthens the current account, but it does so against the backdrop of ongoing domestic energy supply challenges. Eskom's dependence on coal for approximately 80% of generation capacity means that aggressive export maximisation during a global demand window carries domestic energy security implications that cannot be dismissed.

The medium-term trajectory of global coal demand adds further complexity. Despite the near-term demand surge driven by Strait of Hormuz tensions and South Africa coal exports reaching a pivotal inflection point, the structural direction of travel in global energy systems remains toward reduced coal consumption as renewable capacity continues to scale across Asia and Europe. South Africa's coal export infrastructure investment decisions made during the current demand window will ultimately determine whether the country can capture export premiums before addressable market size contracts meaningfully.

However, the urgency is real: demand windows created by geopolitical disruption can close as rapidly as they open, as the 2023 European coal surge and its subsequent collapse clearly demonstrated. Consequently, South Africa faces a narrow but meaningful window in which the combination of Strait of Hormuz tensions and South Africa coal exports aligns favourably with global procurement dynamics, provided the infrastructure constraints can be at least partially addressed in time to capture the opportunity.

Disclaimer: This article contains forward-looking statements, projections, and scenario analyses relating to energy markets, freight rates, and commodity demand. These reflect conditions and forecasts as reported at the time of publication and are subject to rapid change. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research before making any investment decisions.

Want To Stay Ahead of the Next Major Commodity Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex geological and commodity data into actionable investment insights — explore historic examples of exceptional discovery returns that demonstrate why timing matters, and begin your 14-day free trial today to position yourself ahead of the broader market.