July 10, 2026

Africa's Critical Mineral Map Is Being Redrawn From the Inside Out

For most of the past two decades, global capital chasing African mining exposure defaulted to a familiar playbook: gold in West Africa, copper in the Democratic Republic of Congo, and platinum group metals anchored to South Africa's Bushveld Complex. What that framework consistently underweighted was the Northern Cape, a vast and geologically ancient province that once produced copper in commercially significant volumes and then, largely, went quiet.

That silence is ending. The simultaneous revival of two historically producing copper districts in the Northern Cape, combined with accelerating innovation within South Africa's platinum group metals sector, is reshaping how analysts and investors think about the country's critical mineral identity. Northern Cape copper and South African PGMs are not unified stories, however. They are two distinct commodity narratives, separated by geology, geography, and investment thesis, both gaining momentum at the same time.

Understanding the difference between them, and the structural conditions enabling each, matters considerably for anyone building a view on South Africa's mining sector in 2026.

The Northern Cape Copper Revival: Geology, History, and a 40-Year Production Gap

Why Previously Producing Districts Carry a Different Risk Profile

There is a principle in mining economics that is frequently overlooked in favour of exploration headlines: a historically producing district is categorically different from a greenfield discovery. When a mine has previously operated at commercial scale, the resource geometry is understood, metallurgical behaviour has been tested, infrastructure corridors often still exist, and the permitting environment carries institutional memory.

Both of the Northern Cape's major copper revival projects benefit from exactly this dynamic.

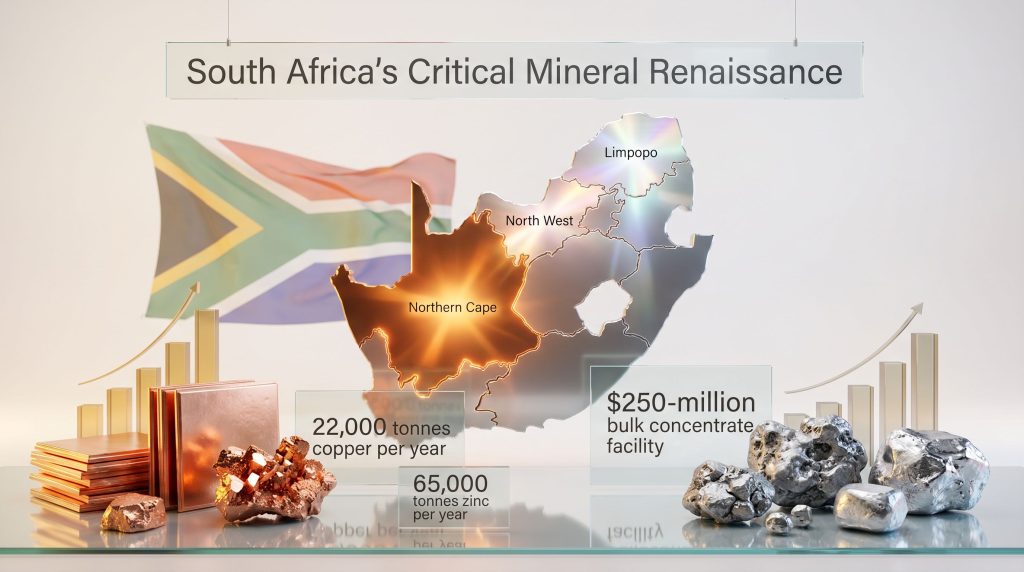

The Okiep Copper District, located in Namaqualand in the Northern Cape's northwestern corner, was one of South Africa's most significant copper producers for over a century before operations wound down. Primary copper production has now resumed at the district for the first time in more than four decades, a milestone that marks a genuine structural shift rather than an incremental exploration update. The Okiep Copper Project represents one of the most compelling copper revival stories on the African continent.

Current processing throughput at the Rietberg plant stands at 12,000 tonnes per month, with a second plant commissioning expected to lift that figure to 45,000 tonnes per month once fully operational. Plant recovery rates are running at 75 to 85%, a range consistent with the district's sulphide-dominant ore character. New drilling at the Flat Mine East target has confirmed high-grade intercepts at depth, with the mineralisation system remaining open below current resource limits, suggesting meaningful upside beyond what is already defined.

The Prieska Copper-Zinc Project: Scale, History, and a Glencore Anchor

The Prieska Copper-Zinc Project represents the other pillar of the Northern Cape's copper renaissance. The deposit's historical production record is substantial:

| Metric | Historical Output (1971 to 1991) | Projected Steady-State Output |

|---|---|---|

| Copper | 430,000 tonnes total | 22,000 tonnes per year |

| Zinc | 1,000,000 tonnes total | 65,000 tonnes per year |

What makes the Prieska project particularly significant from a capital markets perspective is the financial architecture underpinning its development. A binding prepayment agreement with Glencore supports a $250-million bulk concentrate facility, providing the kind of offtake-linked capital certainty that is increasingly rare in junior mining finance. Furthermore, capital raising is actively underway to advance the project toward construction and commissioning.

The involvement of a major global commodity trader in the financing structure of a junior copper project fundamentally changes the risk calculus for co-investors. Offtake-linked prepayment removes the price discovery uncertainty that typically burdens early-stage project finance.

How the Northern Cape's Established Producers Provide Comparative Context

The Northern Cape is not exclusively a story of revival projects. Vedanta's Black Mountain Mine, which operates the Gamsberg zinc operation alongside base metal extraction, produced approximately 2,720 tonnes of copper in 2023. For context, Palabora Mining Company in Limpopo produced approximately 15,420 tonnes in the same period, illustrating the scale differential that the revival projects are ultimately working toward closing. The largest copper mines globally provide a useful benchmark when assessing how these revival projects might ultimately position themselves.

The Northern Cape's Broader Mineral Identity

Copper is the most discussed commodity in the Northern Cape right now, but it sits within a much broader mineral endowment that investors should understand before forming a provincial-level view:

| Commodity | Key Operations | Status |

|---|---|---|

| Iron Ore | Sishen, Kolomela | Active, large-scale |

| Manganese | Hotazel, Black Rock | Active, globally significant |

| Zinc | Gamsberg, Aggeneys | Active |

| Copper | Okiep (Rietberg), Prieska | Revival underway |

| PGMs | None | Not geologically present |

That final row carries critical weight for investors. The Northern Cape does not host platinum group metal deposits. Any conflation of the province's copper revival with South Africa's PGM narrative reflects a fundamental geographic and geological misunderstanding. In addition, understanding the broader South Africa mining decline provides essential context for why these revival projects are attracting such significant attention now.

South Africa's PGM Sector: A Bushveld Story That Has Nothing to Do With the Northern Cape

The Geological Boundary That Defines the PGM World

Platinum group metals in South Africa are the product of one geological formation: the Bushveld Igneous Complex, the world's largest known layered igneous intrusion, spanning Limpopo and North West provinces. Its lateral extent, covering an area exceeding 65,000 square kilometres, and its remarkably consistent reef horizons, most notably the Merensky Reef and the UG2 Reef, are what enable the long-life, large-scale mining operations that define the global PGM industry.

South Africa holds an estimated 70% of global platinum reserves and is the world's leading producer of both platinum and rhodium. The three dominant producers operating across the Bushveld are Sibanye-Stillwater, Impala Platinum, and Anglo American Platinum, each running multi-reef, multi-shaft operations that have no geological equivalent anywhere else on earth. However, the global PGM market challenges facing these producers are driving meaningful investment in processing innovation.

What Mintek Is Doing to Extract More Value Per Tonne

Mintek, South Africa's state-owned mineral technology research organisation, is advancing a processing methodology that targets a challenge at the core of PGM economics: how to improve the value extracted from each tonne of ore before it enters the energy-intensive smelting circuit.

The approach centres on PGM preconcentration, a technique that upgrades the head grade of material destined for smelting, effectively concentrating the valuable metals before the high-cost processing steps begin. The economic logic is straightforward but the operational execution is technically demanding:

- Lower-grade material is separated early in the processing chain, reducing the total volume requiring smelting.

- Energy consumption per unit of recovered PGM decreases as a result of processing a higher-grade feed.

- Chrome recovery becomes a viable parallel revenue stream, since UG2 Reef ore, which is high in chromite, can yield saleable chrome concentrate as a co-product when the preconcentration circuit is designed appropriately.

- Overall recovery economics improve, with less metal value lost in the tailings stream.

The dual benefit of improved PGM recovery and chrome co-product capture positions preconcentration not merely as a cost-reduction strategy but as a genuine margin-expansion tool. This is particularly relevant in a PGM price environment where producers are under sustained pressure to reduce costs per platinum ounce equivalent.

In a commodity sector where price is largely beyond a producer's control, the competitive advantage increasingly lies in the processing chain. Preconcentration technology represents one of the more underappreciated levers available to South African PGM producers.

Sibanye-Stillwater's Domestic PGM Reinvestment: What Secondary Mining Signals

Sibanye-Stillwater has received internal validation for the first phase of its secondary mining programme within its South African PGM operations. Secondary mining refers to the systematic extraction of reef material that was left behind or deemed uneconomic during a primary mining phase.

This material accumulates in a few distinct forms:

- Pillars left to support underground workings during primary extraction phases

- Low-grade zones bypassed when metal prices or cost structures made them unviable

- Residual reef adjacent to mined-out panels that was inaccessible using the equipment configurations of an earlier era

By returning to this material with updated cost structures, modern extraction equipment, and refined processing approaches, Sibanye-Stillwater is effectively extending the economic life of underground infrastructure that is already fully depreciated. Consequently, secondary mining operations can generate positive margins at metal price points that would be insufficient to justify primary development.

The validation of the first phase is significant not just operationally but as a signal of the company's medium-term commitment to its South African PGM asset base, particularly given the operational challenges the group has faced at its international operations in recent years.

Two Narratives, One Jurisdiction: What South Africa's Critical Mineral Moment Actually Means

The Structural Case for South Africa as a Multi-Commodity Destination

What is genuinely notable about South Africa's current mining moment is not any single project or discovery but the simultaneous forward movement across two entirely separate critical mineral corridors. Northern Cape copper and South African PGMs are each advancing on the back of distinct geological endowments, different investor bases, and separate processing and infrastructure requirements.

The convergence of activity across both corridors in the same period reflects several underlying forces:

- Global copper demand driven by electrification infrastructure, electric vehicle manufacturing, and renewable energy deployment is providing a structural demand floor that makes marginal copper projects viable

- PGM processing innovation is allowing existing Bushveld producers to extract more value from orebodies that have been mined for decades, extending asset life without requiring new discoveries

- Institutional capital from entities like Mintek on the processing side, and major offtake partners like Glencore on the project finance side, is reducing the binary risk that typically deters investment in revival and innovation projects alike

Furthermore, robust copper market trends in 2025 and 2026 are reinforcing the investment case for revival projects that might otherwise have struggled to attract capital in a more subdued commodity environment. For project developers, however, the rigour of a mining project feasibility study remains the critical gateway through which institutional capital ultimately flows.

A Note on Investor Discipline

This article contains forward-looking projections, including production targets and financial structures, that are subject to operational, regulatory, and commodity price risks. Readers should treat all forward-looking statements as indicative rather than guaranteed, and seek independent financial advice before making investment decisions based on information contained herein.

Frequently Asked Questions: Northern Cape Copper and South African PGMs

Is copper currently being mined in the Northern Cape?

Yes. The Northern Cape hosts two active copper revival projects. The Okiep Copper District has resumed primary copper production after more than four decades of inactivity, currently processing at 12,000 tonnes per month with expansion planned to 45,000 tonnes per month. The Prieska Copper-Zinc Project is advancing toward construction, targeting 22,000 tonnes of copper and 65,000 tonnes of zinc per year at steady state.

Does the Northern Cape produce platinum group metals?

No. PGMs are geologically confined to the Bushveld Igneous Complex in Limpopo and North West provinces. The Northern Cape has no commercially viable PGM deposits.

What is PGM preconcentration and why does it matter?

Preconcentration is a processing step that upgrades the grade of ore before it enters the smelter. For PGM producers, it reduces the volume of material requiring energy-intensive smelting, lowers cost per ounce of recovered metal, and in UG2 Reef operations, enables the simultaneous recovery of saleable chrome concentrate as a co-product.

What is secondary mining in the context of Sibanye-Stillwater?

Secondary mining involves the extraction of reef material bypassed or left in place during primary mining phases. Because the underlying infrastructure is already in place and depreciated, secondary mining can be economically viable at lower metal price thresholds than primary development, making it a margin-efficient way to extend asset life.

What is the significance of the Glencore prepayment agreement at Prieska?

The agreement provides $250-million in capital linked to a bulk concentrate offtake arrangement. For a project at the development stage, this structure removes a significant portion of the financing risk by tying capital provision to future production rather than relying entirely on equity markets or traditional project debt.

Ready to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — from copper revivals to critical mineral opportunities — instantly translating complex data into actionable insights for investors at every level. Explore historic discoveries and the exceptional returns they've generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.