June 15, 2026

When Supply Chains Break: The Hidden Fragility Behind Global Fuel Markets

Energy security is rarely front of mind until it becomes a crisis. Most fuel-importing nations operate under the assumption that global refined product markets will self-correct, that tankers will keep moving, and that price fluctuations will remain within manageable bands. That assumption has been severely tested in 2026. South Africa fuel imports from the US following Middle East supply disruptions have emerged as one of the most significant stories in global energy trade, highlighting the dangerous concentration of refined fuel sourcing along a single geographic corridor.

For nations across the Global South, this is not merely a market pricing event. It is a supply chain stress test with real consequences for transport networks, consumer budgets, business operating costs, and macroeconomic stability. South Africa, as the African continent's largest fuel importer, sits at the epicentre of this challenge and has been forced to act with unusual speed to secure alternative supply.

When big ASX news breaks, our subscribers know first

How South Africa Built Its Fuel Supply Chain Around the Gulf

For years, South Africa's refined petroleum import strategy centred on the Gulf Cooperation Council states. The UAE, Saudi Arabia, Oman, and Bahrain collectively formed the backbone of the country's inbound fuel supply, joined by India and Nigeria as secondary contributors. This arrangement made geographic and commercial sense: Gulf refineries operate at world-scale capacity, produce competitively priced products, and historically offered reliable shipping timelines to Southern African ports via established tanker corridors.

The three product categories most critical to South Africa's import strategy are diesel, petrol, and jet fuel. Each plays a distinct economic role:

- Diesel powers the logistics and freight networks that move goods across the country's road-dependent supply chains

- Petrol fuels the private vehicle fleet underpinning daily economic activity

- Jet fuel sustains commercial aviation, a sector deeply integrated with tourism revenue and business connectivity

The Port of Durban has long served as the primary artery for these inbound volumes, handling the bulk of fuel discharged in South Africa before distribution through inland pipeline and road networks. Its infrastructure made it the natural focal point for any supply chain disruption affecting import logistics.

Furthermore, the current crude oil market overview makes clear that the concentration of refined fuel sourcing within a single geographic corridor created an efficiency that, under normal conditions, was commercially rational. Under geopolitical stress, that same concentration became a systemic liability.

The Strait of Hormuz Disruption and Its Global Ripple Effect

The catalyst for the current crisis is the disruption to shipping through the Strait of Hormuz, a narrow waterway connecting the Persian Gulf to the Arabian Sea. The Strait is one of the most consequential maritime chokepoints on earth, and its disruption, linked to the broader conflict involving the United States, Israel, and Iran, effectively severed the supply corridor that South Africa and many other import-dependent economies had relied upon for decades.

The immediate effect on global fuel trade has been multidimensional:

- Tanker operators elevated war risk insurance premiums dramatically, making Gulf-departure voyages significantly more expensive to underwrite

- Many vessel operators chose to reroute away from affected zones entirely, reducing available shipping capacity on key trade lanes

- Global refined product availability tightened as Asian emerging markets and European jet fuel buyers competed for supply from alternative origins

- Freight costs compounded commodity price increases, amplifying the landed cost of every barrel reaching import-dependent nations

Critically, the trade and geopolitics in oil analysis consistently shows that disruptions of this nature are unlikely to be rapidly reversed. Even in scenarios where active hostilities de-escalate, the normalisation of commercial shipping patterns through contested maritime zones can take many months.

Why Diesel Is the Most Acutely Constrained Product

Among the three affected product categories, diesel has emerged as the most supply-constrained in the South African context. This is a function of both demand structure and supply origin concentration. South Africa's freight and logistics sector is almost entirely diesel-dependent, and the agricultural, mining, and construction sectors rely on diesel for machinery operation at scale.

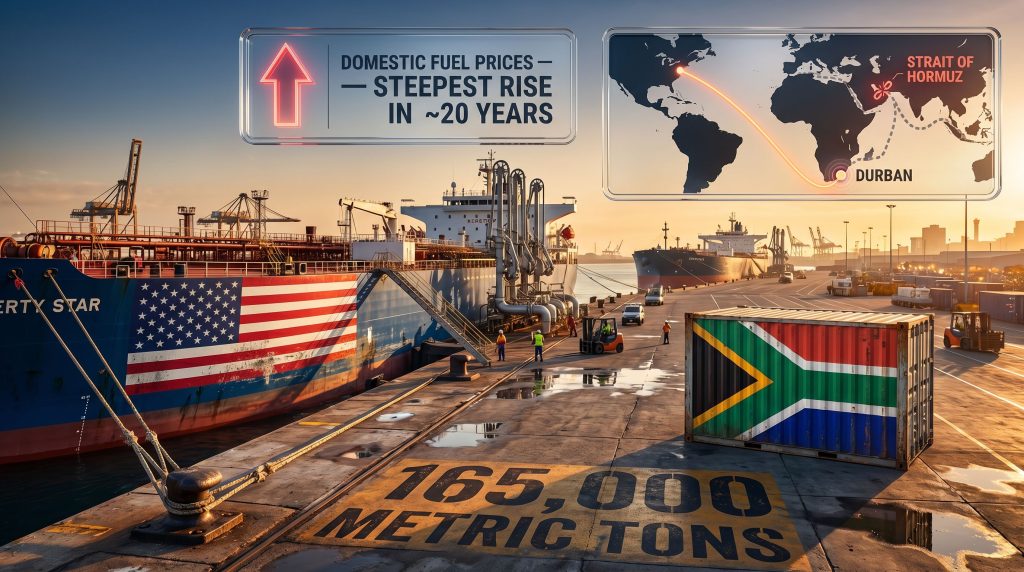

The April 2026 domestic price adjustment cycle reflected this pressure acutely, with diesel price movements contributing meaningfully to what analysts described as one of South Africa's steepest fuel cost increases in approximately two decades.

South Africa Fuel Imports from the US: Quantifying the Pivot

The response from South Africa's fuels procurement sector has been both pragmatic and swift. Shipping data cited by Bloomberg confirmed that at least four tankers carrying a combined cargo of approximately 165,000 metric tons of refined fuel products originating from the United States offloaded at the Port of Durban during April 2026. This volume represents a clear and statistically significant departure from earlier 2026 sourcing patterns, where US-origin fuel played a negligible role in the supply mix.

| Metric | Detail |

|---|---|

| US fuel delivered to Durban (April 2026) | ~165,000 metric tons |

| Tankers involved | At least 4 |

| Primary receiving port | Port of Durban |

| Products affected | Diesel, petrol, jet fuel |

| Traditional Gulf suppliers displaced | UAE, Saudi Arabia, Oman, Bahrain |

| Domestic price impact | Among steepest increases in ~20 years |

Avhapfani Tshifularo, chief executive of the Fuels Industry Association of South Africa, confirmed that the US had been formally identified by the industry as a viable alternative sourcing origin and that a measurable increase in fuel shipments from American refineries had occurred. He further noted that while global fuel availability had not entirely collapsed, the cost of accessing that fuel had risen substantially due to elevated freight rates and longer voyage distances.

South Africa's Mineral Resources and Energy Minister Gwede Mantashe characterised the situation as representing the most serious threat to the country's fuel security in recent memory, noting that active engagement was underway to formalise additional alternative supply relationships beyond the US.

Why American Refineries Are Positioned to Fill the Gap

The United States operates one of the world's largest and most sophisticated refining systems, concentrated along the Gulf Coast in states including Texas and Louisiana. American refineries are configured to produce large volumes of diesel, gasoline, and jet fuel to internationally compatible specifications, and the country has progressively expanded its refined product export infrastructure over the past decade.

Several factors make the US a credible alternative supplier for South Africa in the current environment:

- Export capacity: US Gulf Coast export terminals can load Suezmax and Aframax-class tankers capable of carrying volumes compatible with Durban's receiving infrastructure

- Product availability: American refineries are not capacity-constrained in the way that some Middle Eastern facilities facing operational disruption are

- Trade economics: Despite the longer voyage distance, the combination of competitive refinery gate pricing and available cargo slots makes US-origin fuel commercially viable

- Supply reliability: US-origin cargoes are not exposed to the maritime insurance and routing disruptions affecting Hormuz-adjacent departure points

The voyage from US Gulf Coast terminals to Durban is considerably longer than the Gulf-to-Durban route, adding to freight costs. However, when those costs are compared against the inflated insurance premiums, routing detours, and supply uncertainty attached to Gulf departures, American fuel has emerged as competitively positioned on a total landed cost basis.

Is This a Temporary Adjustment or a Lasting Realignment?

The more consequential question is not whether South Africa can source fuel from the United States in a crisis. It demonstrably can. The more strategically significant question is whether this pivot will prove durable once the immediate geopolitical trigger fades. Indeed, the trade war impact on oil markets demonstrates that supply chain disruptions frequently outlast the events that caused them.

Energy trade history offers a clear pattern on this point. Supply chain disruptions that force the establishment of new commercial relationships, logistics corridors, and contractual arrangements tend to exhibit significant persistence. Once traders, refiners, and procurement teams have invested in establishing alternative supply chains, the commercial inertia favouring continuation is substantial.

When emergency supply pivots prove operationally successful, they frequently become permanent features of procurement strategy rather than temporary workarounds. The COVID-era supply chain rewiring across multiple industries demonstrated precisely this dynamic.

Several scenarios govern the medium-term trajectory of South Africa's fuel import mix:

- Partial Gulf route normalisation: Shipping resumes through the Strait of Hormuz but at reduced volumes and elevated cost, creating a two-track import market where both Gulf and US suppliers compete for South African business simultaneously

- Full route restoration: Gulf-to-Durban tanker movements return to pre-disruption levels, but US supply relationships are maintained as a diversification hedge

- Prolonged disruption: Geopolitical conditions prevent meaningful Gulf route normalisation for 12 months or more, entrenching US and other alternative suppliers as primary sources

Africa's Broader Fuel Vulnerability

South Africa's position as Africa's largest fuel importer makes its experience a leading indicator for continental trends rather than an isolated national event. Multiple African economies are simultaneously experiencing elevated import costs, supply uncertainty, and pump price inflation driven by the same underlying global forces. In addition, the resource and energy export challenges facing other commodity-dependent nations illustrate how broadly these disruptions are reverberating globally.

The continent faces a structural challenge that predates the current crisis: a significant refinery capacity deficit relative to total fuel demand. Several African refineries have closed or reduced throughput in recent years due to ageing infrastructure, maintenance backlogs, and insufficient investment in downstream upgrades.

The Dangote Refinery Question

Nigeria's Dangote Refinery, one of the largest greenfield refinery projects ever completed globally, has attracted considerable attention as a potential buffer against this continental vulnerability. With nameplate capacity of 650,000 barrels per day, the facility has been progressively ramping up output and is theoretically capable of supplying refined products to neighbouring economies at scale.

However, industry observers have consistently tempered expectations about the refinery's capacity to offset the broader structural import dependence across Africa. Several constraining realities apply:

- Ramp-up timelines for large-scale refineries are typically measured in years, not months, before nameplate capacity is reliably achieved

- Product quality specifications, distribution logistics, and pricing competitiveness all determine whether regional buyers will source from Dangote versus international alternatives

- Multiple economies facing simultaneous supply constraints cannot all be served adequately from a single regional facility

- Nigeria's own domestic fuel demand remains substantial, competing with export ambitions for available refinery output

The next major ASX story will hit our subscribers first

Real-World Cost Pressures: What the Disruption Means for Consumers and Businesses

Supply chain disruptions of this nature do not remain abstract market dynamics for long. Their effects translate into concrete cost pressures felt by consumers and businesses across the economy. The geopolitical tensions reshaping trade have accelerated these pressures considerably across import-dependent nations.

How Cost Pressures Are Flowing Through the Economy

The mechanics of cost transmission in South Africa's fuel market are relatively direct:

- Higher landed fuel costs are reflected in regulated pump price adjustments

- Transport operators absorb higher fuel expenses, compressing margins or raising freight tariffs

- Elevated freight costs increase the delivered price of goods across consumer categories

- Broader consumer price inflation accelerates, potentially influencing Reserve Bank monetary policy decisions

The rand's weakness against the US dollar has compounded this pressure. Because refined petroleum products are priced and traded in US dollars globally, a weaker rand amplifies the domestic cost impact of every dollar-denominated price increase.

Aviation Sector Under Acute Pressure

Commercial aviation has experienced some of the sharpest cost impacts from the jet fuel supply tightening. Airline operating costs have risen dramatically in the current environment, with some carriers reporting fuel cost increases of up to 70% in affected periods. Jet fuel is typically the largest single cost item for commercial airlines, meaning that movements of this magnitude compress profitability significantly and risk feeding through to higher airfares.

Localised fuel availability disruptions have also been reported at service stations outside major urban centres, where delivery frequency is lower and buffer inventory thinner. Over 140 stations reportedly faced supply challenges during earlier phases of the disruption, illustrating that the impact is not uniform across the geography.

How Businesses Are Adapting

Faced with elevated and volatile fuel costs, South African businesses are exploring several adaptive strategies:

- Fuel hedging instruments are attracting renewed attention among large commercial consumers seeking price certainty over forward periods

- Route and fleet optimisation is being pursued by logistics operators to reduce fuel consumption per delivery kilometre

- Inventory management adjustments are being made to reduce the frequency of delivery runs while maintaining service levels

- Energy efficiency investments, including vehicle fleet upgrades and load optimisation technologies, are being evaluated with shortened payback period assumptions

Frequently Asked Questions: South Africa Fuel Imports from the US

Why is South Africa importing fuel from the United States?

Disruptions to Middle East maritime supply routes, particularly those linked to the Strait of Hormuz and the broader regional conflict involving the US, Israel, and Iran, have forced South African fuel importers to identify alternative sourcing origins. South Africa fuel imports from the US following Middle East supply disruptions represent a direct response to the inaccessibility of previously relied-upon Gulf supply corridors.

How much fuel has South Africa imported from the US in 2026?

Shipping data indicates that approximately 165,000 metric tons of refined fuel products were delivered to Durban by at least four US-origin tankers during April 2026 alone.

Will South Africa's fuel supply remain stable?

Import schedules for May and June 2026 have been confirmed, and no widespread supply disruptions are anticipated in the near term. However, diesel remains supply-constrained, and landed costs are elevated due to longer voyage distances and freight premiums embedded in non-Gulf supply chains.

What products are most affected?

Diesel has been identified as the most acutely constrained product category, followed by petrol and jet fuel. All three were previously sourced heavily from Gulf states including the UAE, Saudi Arabia, and Oman.

Could South Africa return to Gulf suppliers once the conflict eases?

Industry participants have indicated that even if geopolitical conditions improve, trade flows may not quickly revert to previous patterns. Once alternative supply relationships are established, commercial inertia tends to sustain them. A two-track import market where both Gulf and US suppliers compete for South African volumes is a credible medium-term outcome.

What is the impact on South African fuel prices?

South Africa recorded one of its steepest domestic fuel price increases in approximately two decades during early 2026, driven by a combination of global supply tightening, elevated freight costs, rand weakness, and the transition to longer-haul supply chains.

Key Takeaways at a Glance

- 165,000 metric tons of US-origin refined fuel were delivered to Durban in April 2026, marking a clear departure from Gulf-centric sourcing

- The Strait of Hormuz disruption has fractured South Africa's traditional supply chain in ways that may prove structurally persistent rather than cyclical

- Diesel remains the most supply-constrained and economically sensitive product category, with price pressures flowing directly into transport and logistics costs

- Africa's refinery infrastructure deficit leaves the continent broadly unable to self-insulate from global supply shocks in the near or medium term

- The US sourcing pivot carries durable commercial logic beyond the immediate crisis, as supply chain diversification reduces concentration risk

- Consumer and business cost pressures are compounding, with fuel inflation intersecting with rand weakness, freight cost escalation, and broader inflationary momentum

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or energy policy advice. Forward-looking statements, scenario projections, and market assessments reflect publicly available information and analytical interpretation as of the date of publication. Readers should conduct independent research before making any decisions based on the information contained herein. Market conditions, geopolitical developments, and supply chain dynamics are subject to rapid change.

Want to Stay Ahead of the Resource and Commodity Shifts Reshaping Global Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity and resource data into clear, actionable investment insights — ideal for investors navigating volatile supply chain and energy market conditions. Explore why major mineral discoveries have historically generated substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.