June 15, 2026

The Geology Is Not the Problem: Why South Africa's Mineral Wealth Keeps Leaving as Raw Ore

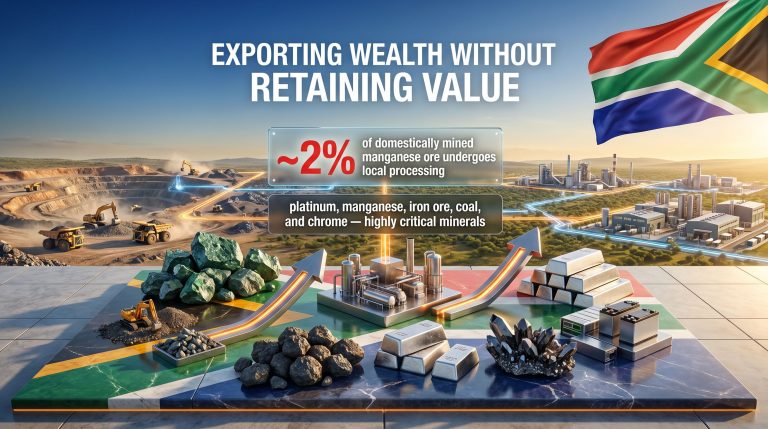

Few economic contradictions are as striking as a nation sitting atop one of the world's most extraordinary mineral endowments while simultaneously watching its industrial base erode. South Africa mineral beneficiation policy has been a central theme of industrial strategy for over a decade, yet the country holds the largest known platinum group metal (PGM) reserves on the planet, contributes a dominant share of global chrome supply, and hosts significant deposits of manganese, vanadium, titanium, and a growing portfolio of energy transition minerals. However, its manufacturing sector has contracted steadily over the past two decades.

In 2025, South Africa formally lost its long-held position as Africa's largest manufacturing economy to Morocco. That milestone, documented institutionally by the African Development Bank in its Africa Industrialisation Index 2025, was not simply a statistical footnote. It was a signal that decades of policy ambition had not translated into structural industrial transformation. Understanding why requires examining the architecture of beneficiation policy — where it has succeeded, where it has stalled, and what would need to change.

When big ASX news breaks, our subscribers know first

What Mineral Beneficiation Actually Means in Policy Terms

The term mineral beneficiation is frequently used but inconsistently understood. In South Africa's policy context, it refers to the deliberate transformation of raw extracted ores into refined, processed, or manufactured products within the country's borders, rather than exporting unprocessed commodities for value addition elsewhere.

The process spans multiple stages of increasing complexity:

- Primary processing: Crushing, concentration, and smelting of raw ore into an intermediate product

- Secondary refining: Chemical separation, purification, and alloy production that upgrades intermediate products into commercially usable materials

- Tertiary manufacturing: Component fabrication and finished goods production, such as battery precursor chemicals, catalytic converters, or specialty alloys

South Africa's foundational 2011 Beneficiation Strategy for the Minerals Industry framed this multi-stage progression as the mechanism for converting geological endowment into a national competitive advantage. The strategy was explicit that value addition should extend as far along the chain as feasible, targeting both employment intensity and export revenue growth. What it did not resolve — and what subsequent policy iterations have continued to struggle with — is how to make domestic processing economically competitive enough to attract and retain investment.

How South Africa's Beneficiation Policy Has Evolved: From 2011 to 2026

A Decade and a Half of Policy Continuity Without Consistent Implementation

The 2011 strategy established the foundational logic: link mineral extraction rights to downstream processing obligations, and coordinate across energy pricing, skills development, infrastructure investment, and trade policy. The framework was conceptually coherent but was applied inconsistently across commodity groups in practice.

The draft Medium Term Development Plan for 2024 to 2029 elevated beneficiation from a sectoral aspiration to an explicit national outcome, mandating that South Africa export processed or semi-processed products wherever feasible rather than raw ores. Despite the stronger language, implementation remained fragmented.

The 2026 Industrial Development Strategy, published by the Department of Trade, Industry and Competition (dtic) in June 2026, introduced a more direct regulatory mechanism: linking preferential mining permit allocations to binding local processing commitments. This represented a structural escalation in policy posture, moving from incentive-based encouragement toward permit-conditioned obligation.

| Policy Instrument | 2011 Strategy | 2024–2029 MTDP | 2026 Industrial Development Strategy |

|---|---|---|---|

| Beneficiation framing | Competitive advantage | Explicit national outcome | Permit-linked obligation |

| Commodity focus | Broad minerals | Critical minerals emphasis | Chrome + clean-energy minerals |

| Regulatory mechanism | Incentive-based | Policy target | Licensing conditionality |

| Implementation status | Inconsistent | Aspirational | Proposed (not yet legislation) |

| Coordinating agencies | dtic | dtic + DMPR | dtic + DMPR (joint) |

The 2026 Strategy's Core Mechanism and Its Limitations

The dtic's 2026 strategy coordinates implementation with the Department of Mineral and Petroleum Resources (DMPR), signalling an intent to embed processing requirements directly into the licensing architecture. The targeted commodity basket includes chrome, lithium, cobalt, platinum group metals, and rare earth elements — all of which intersect with global clean-energy supply chains.

However, the strategy has not yet defined specific local-processing thresholds, compliance timelines, or enforcement mechanisms for most of the commodities it targets. Chrome remains the most advanced case, with policymakers having already discussed export taxes and export quotas to redirect ore flows toward domestic smelters. For PGMs, lithium, cobalt, and rare earths, the strategy identifies targets without specifying how compliance will be measured or enforced.

Furthermore, the South Africa mining decline in overall output over recent years has amplified the urgency of these policy gaps, adding pressure on policymakers to deliver frameworks that can restore investor confidence.

Critical Policy Gap: Without commodity-specific requirements and measurable compliance frameworks, the 2026 strategy functions as an investment signal rather than a binding industrial mandate. The gap between policy declaration and legislative codification is itself a source of regulatory uncertainty that industry stakeholders identify as a deterrent to long-term capital commitment.

The Minerals That Matter Most: A Critical Mineral Inventory

Platinum Group Metals: South Africa's Defining Geological Advantage

South Africa holds the world's largest known PGM reserves, concentrated primarily in the Bushveld Igneous Complex — a layered intrusion that is geologically unique in its scale and mineralogical richness. The Bushveld hosts the Merensky Reef and the UG2 Chromitite Layer, the latter of which has grown in importance as platinum and palladium prices have fluctuated and rhodium has emerged as a high-value co-product.

What is less commonly appreciated is that PGM ore grades have been declining over time as mines access deeper and lower-grade horizons. This makes the economics of primary PGM mining increasingly sensitive to operating costs, and energy pricing in particular. The shift toward UG2 ore, which carries higher chromite content alongside PGMs, has also created a structurally important byproduct stream that connects the PGM and chrome processing industries.

Chrome: The Most Contested Beneficiation Case

South Africa produces approximately 45% of the world's chrome ore, making it the dominant global supplier. The country also has significant ferrochrome smelting capacity, which converts chrome ore into ferrochrome, the primary input for stainless steel production. However, domestic ferrochrome output has faced sustained pressure as electricity tariff increases have eroded the cost competitiveness of energy-intensive smelting operations.

The Minerals Council South Africa has used the chrome sector as the clearest illustration of a critical structural argument: deindustrialisation in chrome processing is not caused by insufficient ore availability. It is driven by electricity costs that make domestic smelting economically unviable relative to offshore competitors, particularly in China, which has invested heavily in chrome processing infrastructure.

This distinction carries profound implications for policy design. An export quota or export tax on chrome ore would redirect ore flows toward domestic smelters, but if those smelters cannot operate at competitive cost, the intervention generates neither industrial employment nor foreign exchange earnings. It may simply reduce the total volume of productive activity.

The Clean-Energy Mineral Tier: Lithium, Cobalt, and Rare Earths

These commodities are at an earlier stage of both production and beneficiation policy development within South Africa. The surge in critical minerals demand driven by clean energy supply chains has made this tier increasingly strategic. The International Energy Agency projects that demand for lithium could increase by a factor of six or more by 2040 under accelerated energy transition scenarios, with cobalt and rare earth demand rising sharply in parallel.

South Africa's rare earth supply chains remain underdeveloped relative to the country's geological potential. Deposits, including carbonatite-hosted occurrences, warrant further exploration. The country's cobalt resources are largely associated with base metal operations rather than standalone deposits. Lithium occurrences, including hard-rock spodumene and pegmatite-hosted deposits, have attracted increasing exploration interest.

For all three commodity groups, approximately 10% of iron and platinum ores are currently beneficiated locally — a figure that has remained broadly stable despite successive policy commitments to improve it. The gap between stated policy ambition and measured processing intensity is one of the most important metrics for evaluating the effectiveness of South Africa mineral beneficiation policy.

What the Mining Industry Is Actually Arguing

The Minerals Council's Structural Objection

The Minerals Council South Africa, whose member companies collectively account for approximately 90% of the total annual value of South Africa's mining production, published a formal response to the 2026 strategy on June 9, 2026. The council's position is nuanced and worth understanding precisely, because it is frequently mischaracterised as opposition to industrialisation itself.

The council's argument is structural rather than ideological. Mining project developers evaluate permit conditions as part of their long-term capital allocation models. Adding mandatory downstream processing commitments to a mining permit increases the capital requirement, operational complexity, and risk profile of any given project in ways that are fundamentally different from the mining operation itself.

Mzila Mthenjane, Chief Executive Officer of the Minerals Council, articulated the organisation's position by stating that mining and mineral processing represent structurally distinct economic activities within the broader minerals value chain, and that processing obligations should not be embedded within mining permits. Instead, the council argued that dedicated policy instruments specifically calibrated for the manufacturing and processing sectors are needed to incentivise and attract the investment required to drive industrialisation forward.

The Investment Risk Calculus for Junior and Mid-Tier Miners

For junior and mid-tier operators, the implications of permit-linked processing obligations are particularly acute. These companies typically rely on project finance structures that are sensitive to permitting conditions and bankability assessments. A processing obligation attached to a mining permit changes the risk profile of the entire project in ways that can render it unbankable under conventional financing frameworks.

The council's preferred alternative involves a package of dedicated industrial incentives directed specifically at the processing sector. In addition, special economic zones have been identified as a potential vehicle for delivering many of these incentives in a geographically targeted manner:

- Preferential electricity tariffs for energy-intensive industrial processors

- Development finance instruments designed for the capital structures of processing projects

- Infrastructure co-investment to reduce logistics and energy access constraints

- Long-term skills pipeline investment in metallurgical and chemical engineering disciplines

- Stable, legislated policy frameworks that give investors certainty over multi-decade time horizons

Industry Perspective: The council's argument implies that the most effective beneficiation policy is one that makes South Africa the most attractive location for processing investment globally, rather than one that coerces mining operators into processing commitments they are structurally ill-equipped to fulfil.

How South Africa Compares to Other African Beneficiation Models

| Country | Target Commodity | Beneficiation Mechanism | Implementation Stage |

|---|---|---|---|

| Zimbabwe | Lithium | Export ban on raw spodumene ore | Active (enforced from 2023) |

| Democratic Republic of Congo | Cobalt | Domestic refining promotion + export levies | Partial implementation |

| Guinea | Bauxite | Domestic alumina refinery requirements | Early stage |

| South Africa | Chrome, PGMs, lithium, REEs | Permit-linked processing commitments | Proposed (2026 strategy) |

| Namibia | Uranium, lithium | Local value addition targets | Policy development phase |

Zimbabwe's approach deserves particular analytical attention. By implementing an outright ban on unprocessed lithium ore exports from 2023, Zimbabwe adopted the most prescriptive regulatory posture on the continent and attracted significant Chinese investment in domestic processing facilities. The outcome illustrates that export prohibition can accelerate processing investment when the resource is sufficiently attractive and when downstream market access is secured.

However, Zimbabwe's model also illustrates the risks. The ban created immediate disruption to existing export revenue streams and produced a processing industry that is heavily concentrated among a small number of well-capitalised investors — primarily Chinese state-connected entities — rather than a diversified domestic industrial base.

The DRC's cobalt beneficiation experience offers a cautionary counterpoint. Infrastructure deficits and unreliable energy access have constrained the effectiveness of export levies and refining promotion policies, mirroring precisely the structural challenges that South Africa's Minerals Council identifies as preconditions that must be resolved before processing mandates can deliver intended outcomes.

The next major ASX story will hit our subscribers first

The Electricity Problem: South Africa's Non-Negotiable Constraint

No analysis of South Africa mineral beneficiation policy is complete without a rigorous examination of the electricity cost problem. Eskom's financial restructuring over the past decade, combined with the costs of transitioning ageing coal-fired generation infrastructure and managing an increasingly constrained grid, has produced electricity tariff increases that have been devastating for energy-intensive industrial users.

Ferrochrome smelting is among the most electricity-intensive industrial processes in existence, consuming approximately 3,200 to 4,000 kilowatt-hours per tonne of ferrochrome produced. At the tariff levels South African smelters currently face, the electricity cost component of ferrochrome production is structurally uncompetitive relative to Chinese producers operating with different energy pricing arrangements.

The same logic applies, with varying degrees of intensity, to PGM refining, lithium hydroxide production, cobalt sulphate processing, and rare earth separation — all of which are energy-intensive at different stages of their processing chains.

Additional Structural Barriers

Beyond electricity, South Africa's beneficiation policy faces a set of compounding structural constraints:

- Skills and technical capacity: Advanced mineral processing requires specialised metallurgical, hydrometallurgical, and chemical engineering expertise that takes years to develop through education and training pipelines

- Infrastructure gaps: Reliable logistics networks, water access, and industrial infrastructure are not uniformly available across South Africa's mining regions

- Financing constraints: Processing projects carry risk profiles that differ fundamentally from mining operations, and development finance institutions have not consistently provided capital structures suited to bridging this gap

- Policy consistency: Investors require regulatory certainty over multi-decade time horizons, and South Africa's history of policy revision and implementation delays has eroded confidence in industrial policy commitments

- Regulatory ambiguity: The absence of commodity-specific thresholds and compliance timelines for most targeted minerals creates the very uncertainty that deters the investment the strategy is designed to attract

Can Permit-Linked Obligations Actually Drive Industrialisation?

What the Evidence from Other Jurisdictions Suggests

Cross-country analysis of resource processing policies reveals a consistent pattern. Processing obligations attached to extraction rights tend to accelerate industrialisation when they are accompanied by competitive operating conditions, dedicated infrastructure, accessible development finance, and stable long-term policy frameworks. Where these enabling conditions are absent, mandatory processing requirements suppress investment in extraction without generating commensurate growth in processing.

Indonesia's nickel model, implemented progressively from 2014 and extended to cover all nickel ore in 2020, is frequently cited as a successful example of permit-linked beneficiation in a developing economy context. Indonesia attracted large-scale Chinese investment in domestic nickel processing and stainless steel manufacturing. However, Indonesia also benefited from significantly lower electricity costs, access to large-scale hydropower in Sulawesi, proximity to major Asian demand centres, and a different labour cost structure.

The transferability of Indonesia's model to South Africa's context is therefore limited. The enabling conditions that made Indonesia's nickel processing mandate viable are not currently present in South Africa's industrial landscape at the same level of competitiveness.

A Policy Design Framework

| Policy Lever | Type | Potential Impact | Key Risk |

|---|---|---|---|

| Permit-linked processing commitments | Obligation | Direct compliance pressure | Investment deterrence without competitive conditions |

| Preferential electricity tariffs for processors | Incentive | Reduces primary operating cost barrier | Fiscal cost and cross-subsidy complexity |

| Export taxes on unprocessed ores | Disincentive | Redirects ore to domestic processors | Revenue reduction, potential trade friction |

| Development finance for processing plants | Incentive | Lowers capital access barrier | Deployment efficiency and selection risk |

| Skills and training investment | Enabler | Builds long-term processing capacity | Long lead times relative to policy urgency |

| Infrastructure co-investment | Enabler | Reduces logistics and energy constraints | Capital-intensive, long execution timelines |

The most durable beneficiation outcomes globally have combined regulatory signals with active industrial support. Neither processing mandates alone nor incentive packages alone have consistently delivered sustained value-chain development. South Africa's 2026 strategy is currently weighted heavily toward the obligation end of this spectrum without yet specifying the enabling conditions that would make compliance economically rational for investors. For a deeper examination of how mineral processing can reshape economies, the structural prerequisites become even more apparent.

Frequently Asked Questions: South Africa Mineral Beneficiation Policy

What is South Africa's mineral beneficiation policy?

South Africa mineral beneficiation policy is a framework designed to encourage the processing, refining, and manufacturing of minerals within the country rather than exporting raw ores. The policy aims to generate greater economic value, employment, and export revenue from South Africa's mineral endowment by developing downstream industrial capacity.

What minerals does the 2026 beneficiation strategy target?

The 2026 Industrial Development Strategy identifies chrome, lithium, cobalt, platinum group metals, and rare earth elements as priority commodities for domestic value addition, given their strategic importance to global clean-energy supply chains.

Why has beneficiation been so difficult to implement in South Africa?

Implementation has been constrained primarily by electricity costs that make domestic processing uncompetitive, compounded by inconsistent application of policy tools, infrastructure gaps, financing constraints, and the absence of commodity-specific compliance frameworks for most targeted minerals.

How does South Africa's approach compare to Zimbabwe's lithium policy?

Zimbabwe implemented an outright ban on unprocessed lithium ore exports — a more prescriptive mechanism that attracted significant processing investment, primarily from Chinese-linked entities. South Africa's 2026 strategy proposes permit-linked processing commitments, a directive but less absolute mechanism that has not yet been legislated.

Is the 2026 Industrial Development Strategy binding law?

No. As of June 2026, the strategy remains a policy proposal published by the dtic. Specific processing requirements, compliance timelines, and enforcement mechanisms have not yet been codified into legislation.

What Needs to Change for South Africa's Beneficiation Policy to Succeed

A conditions-based assessment of the policy's prospects points to several non-negotiable prerequisites:

- Regulatory specificity: Policymakers must define commodity-by-commodity processing thresholds, measurable compliance targets, and clear timelines. Without this, the strategy cannot function as an effective investment signal.

- Energy cost resolution: Competitive electricity tariffs for industrial processors are a structural prerequisite, not an optional complement, to any processing mandate.

- Coordinated incentive architecture: Export taxes, development finance, infrastructure investment, and skills programmes must be deployed as a coordinated and mutually reinforcing package.

- Industry co-design: The mining industry's concerns about permit-linked obligations are structurally legitimate. A consultative process that co-designs implementation mechanics with industry is more likely to generate durable investment outcomes than top-down regulatory imposition.

- Legislative codification: Converting the 2026 strategy from a policy document into enforceable legislation with clear accountability mechanisms is essential for enabling the long-term investment planning that processing projects require.

South Africa's beneficiation ambitions are unfolding within a continental and global shift toward resource nationalism and supply chain localisation. The EU Critical Raw Materials Act, US Inflation Reduction Act supply chain provisions, and an expanding web of bilateral mineral partnership agreements are reshaping how processing location decisions are made globally. South Africa's capacity to attract processing investment will depend not only on its domestic policy design but on how effectively it positions itself within these emerging international supply chain architectures.

Key Takeaways: South Africa's Mineral Beneficiation Policy at a Glance

| Dimension | Current Status |

|---|---|

| Policy framework | 2026 Industrial Development Strategy (proposal stage) |

| Primary regulatory mechanism | Permit-linked processing commitments |

| Target commodities | Chrome, lithium, cobalt, PGMs, rare earths |

| Manufacturing economy ranking | Lost No.1 position in Africa to Morocco (2025) |

| Local beneficiation rate (iron and platinum) | Approximately 10% of ore processed domestically |

| Industry body position | Minerals Council supports dedicated incentives over permit-linked obligations |

| Key structural barrier | Electricity cost competitiveness |

| Legislative status | Not yet binding law |

| Continental comparators | Zimbabwe (export ban), DRC (export levies), Guinea (refinery requirements) |

South Africa's mineral beneficiation policy sits at a genuinely critical inflection point. The geological endowment is not in question. The policy intent is clearly articulated. What remains unresolved is whether the government will build the enabling conditions that make domestic processing economically rational, or whether permit-linked obligations will arrive ahead of the infrastructure, energy pricing, and financing frameworks that would make compliance commercially viable. The answer to that question will determine whether the 2026 strategy marks the beginning of South Africa's industrial renaissance or becomes another chapter in a long history of well-intentioned policy falling short of transformative impact.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across critical commodities — including the platinum group metals, chrome, and lithium at the centre of global supply chain strategies — and converting complex data into clear, actionable investment insights. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to secure a market-leading edge.