June 15, 2026

The Resource Curse in Reverse: Why Processing Power Defines the Next Industrial Era

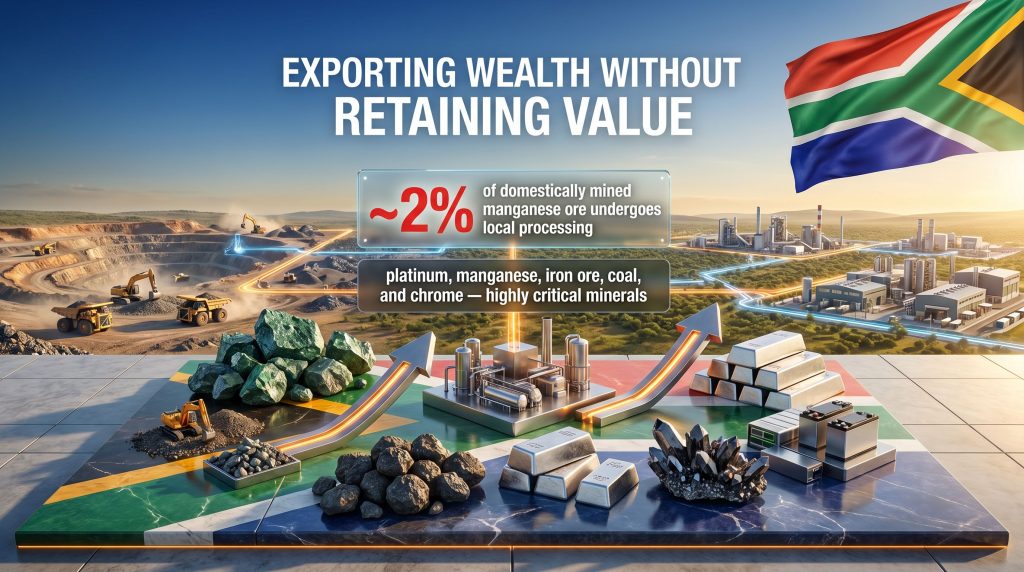

For most of modern economic history, the countries that controlled raw material extraction held significant leverage over global supply chains. That assumption has been quietly dismantled over the past two decades. The real power in commodity markets has shifted downstream, toward nations that can transform ore into components, components into products, and products into export revenue that multiplies through an entire domestic economy. Countries that remain stuck at the extraction end increasingly find themselves trapped in a cycle of volume dependency, price volatility, and limited employment generation. South Africa mineral beneficiation policy is confronting this reality with unusual urgency in 2026.

When big ASX news breaks, our subscribers know first

South Africa's Industrial Decline: A Structural Problem, Not a Cyclical One

The African Development Bank's Africa Industrialisation Index 2025 formally documented what industry analysts had long observed: South Africa's industrial competitiveness has been in sustained retreat. The landmark consequence became official in 2025, when Morocco displaced South Africa as Africa's largest manufacturing economy. This was not a close contest decided by a single year's data. It reflected a prolonged erosion of South Africa's manufacturing base, with the mining sector continuing to dominate export earnings while downstream processing capacity stagnated.

Manufacturing's share of South Africa's GDP has contracted meaningfully over the past two decades. The mining sector, by contrast, has maintained its role as the primary engine of export revenue, but almost entirely through the export of raw and semi-processed materials. The consequence is what economists describe as a price-taker position: South Africa sells commodities at market prices set by global demand and processing capacity located elsewhere, rather than capturing the margin that comes from adding value before export.

The gap between what South Africa extracts and what it processes is starkest in manganese. The country is one of the world's leading manganese producers, yet an estimated only approximately 2% of domestically mined manganese ore undergoes local processing. That single statistic encapsulates the structural inefficiency at the heart of the beneficiation debate.

Defining Beneficiation: More Than a Policy Buzzword

The term beneficiation carries specific technical meaning in the South African mining policy context. At its most basic, it refers to physical upgrading processes such as crushing, sorting, and concentration that improve ore quality before sale. More ambitiously, it encompasses smelting, refining, and the production of intermediate chemical or metallurgical products. At its most advanced, it extends into component manufacturing and finished goods production.

The economic significance of each step increases substantially as you move along this spectrum. A nation that exports manganese ore earns a fraction of what it would earn exporting electrolytic manganese metal — which itself commands a fraction of the value embedded in manganese-based battery cathode materials. Furthermore, strategic manganese processing at scale requires significant upfront infrastructure commitment, a challenge South Africa is only beginning to address.

South Africa's beneficiation framework is explicitly designed to capture more of that value ladder domestically. However, the challenge is that each step up the value chain also requires meaningfully higher capital investment, deeper technical expertise, and more reliable and affordable energy input. This is where policy aspiration routinely collides with industrial reality.

The 2026 Industrial Development Strategy: What Is Actually Being Proposed

South Africa's Department of Trade, Industry and Competition published its 2026 Industrial Development Strategy in June 2026. The document identifies deindustrialisation as a central national challenge and elevates mineral processing as a primary mechanism for reversing it. The most significant and contested element is its proposal to link preferential mining permit allocations to binding local-processing commitments for designated critical minerals.

This mechanism represents a material shift in the policy toolkit. Previous approaches relied predominantly on incentives: tax concessions, mining beneficiation zones benefits, and industrial support programmes administered through the Department of Trade, Industry and Competition in coordination with the Department of Mineral and Petroleum Resources. The new proposal, however, introduces regulatory conditionality, making preferential access to mining rights contingent on demonstrated commitment to domestic value addition.

The existing legislative architecture provides the foundations for this approach:

| Policy Instrument | Administering Body | Primary Function |

|---|---|---|

| Minerals and Petroleum Resources Development Act | Dept. of Mineral and Petroleum Resources | Foundational mining rights and beneficiation obligations |

| Mining Charter | Dept. of Mineral and Petroleum Resources | Transformation and local content requirements |

| Industrial Policy Action Plan | Dept. of Trade, Industry and Competition | Sector-specific industrial support |

| Special Economic Zones | Dept. of Trade, Industry and Competition | Location-based processing investment incentives |

| Critical Minerals and Metals Strategy (2025) | dtic and DMPR | Strategic prioritisation of high-demand minerals |

As of June 2026, the strategy remains a policy proposal rather than enacted legislation. Critical specifics — particularly the precise local-processing thresholds to be required for individual commodities — have not yet been gazetted. Chrome is the most advanced case, with export taxes and export quota mechanisms already under active policy discussion, though these too have not been formalised.

The Critical Minerals Targeted and Why They Matter

South Africa's 2025 Critical Minerals and Metals Strategy establishes a tiered prioritisation framework classifying platinum, manganese, iron ore, coal, and chrome as highly critical. The 2026 strategy extends this framework to encompass a broader basket relevant to clean-energy technology supply chains. In the context of surging critical minerals demand globally, South Africa's geological endowment positions it as a strategically significant supplier — provided it can translate extraction into processing.

- Platinum Group Metals (PGMs): South Africa holds the world's largest known PGM reserves. Significant downstream processing already occurs domestically, but further value addition into hydrogen economy applications and advanced catalyst manufacturing remains underdeveloped.

- Chrome: South Africa is a dominant global chromite producer. The sector is the most advanced in terms of specific policy discussion, but processing capacity is constrained by the energy cost environment rather than ore availability.

- Manganese: The value-addition gap is most extreme here. With approximately 2% of mined ore processed locally, the upside potential from beneficiation is correspondingly enormous.

- Lithium and Cobalt: Both are targeted primarily for their centrality to battery manufacturing supply chains as electric vehicle penetration accelerates globally.

- Rare Earth Elements: An emerging priority given the extreme geographic concentration of global REE processing capacity in China, which creates supply chain vulnerability for Western manufacturers.

The draft Mineral Resources Development Bill, released for public consultation in 2025, provides the legislative vehicle for embedding these strategic priorities into the regulatory framework in a binding way.

The Investment Deterrence Question: Industry's Core Objection

The Minerals Council South Africa, whose member companies collectively account for approximately 90% of the total annual value of South Africa's mining production, published a formal position note on June 9, 2026 raising substantive concerns about the proposed permit conditionality approach.

The Minerals Council's chief executive, Mzila Mthenjane, articulated the industry's core position: that mining and mineral processing are structurally distinct economic activities with different capital requirements, risk profiles, and operational economics. The council's argument is that attaching processing obligations to mining permits conflates two separate industries and misallocates regulatory burden in a way that could deter investment in extraction without actually generating the processing capacity the policy intends to create.

The industry's concern is not philosophical opposition to beneficiation. Rather, it is that regulatory mandates imposed into an environment of structural cost disadvantage will produce compliance costs and investment deterrence, not industrial outcomes.

The chrome sector provides the most instructive illustration of this dynamic. South Africa's chromite ore endowment is world-class, and processing infrastructure exists. The constraint on domestic ferrochrome and chromium chemical production is not ore supply — it is the cost of electricity. South Africa's electricity cost trajectory, shaped by Eskom's structural challenges and successive tariff increases, has progressively undermined the economics of operating and expanding processing facilities.

Imposing local-processing requirements without resolving the underlying energy cost disadvantage would consequently make South African processing operations economically uncompetitive relative to equivalents in jurisdictions with lower industrial electricity costs, such as parts of Asia and the Middle East.

The next major ASX story will hit our subscribers first

Africa's Beneficiation Landscape: A Continental Comparison

South Africa is not operating in a vacuum. Several African nations have moved from policy aspiration to active implementation in mineral beneficiation, providing both precedent and cautionary lessons. Furthermore, the broader global shift toward energy transition minerals processing means South Africa faces growing competition for the capital needed to build out these capabilities.

| Country | Target Commodity | Mechanism Used | Current Status |

|---|---|---|---|

| Zimbabwe | Lithium | Domestic processing mandates, raw spodumene export restrictions | Active enforcement from 2023 |

| DRC | Cobalt and Copper | Export levy frameworks, local value-addition promotion | Partial implementation |

| Guinea | Bauxite | Domestic refining requirements in mining agreements | Ongoing negotiation |

| South Africa | PGMs, Chrome, Manganese, Lithium | Permit conditionality proposal, export taxes under discussion | Policy proposal stage (2026) |

Zimbabwe's lithium processing mandate offers the most directly comparable precedent. Implemented from 2023, it restricts the export of raw spodumene concentrate and requires domestic processing before export. The approach has been partially effective at attracting processing investment but was implemented in a context of lower existing industrial infrastructure, meaning the counterfactual cost of deterring extraction investment was lower than it would be in South Africa's more mature mining economy.

The DRC's experience with cobalt value addition highlights a recurring challenge across African beneficiation programmes: infrastructure deficits and constrained access to long-term capital undermine even well-designed regulatory frameworks. South Africa shares modified versions of both challenges.

The Policy Design Challenge: Getting the Architecture Right

The fundamental tension in South Africa mineral beneficiation policy design lies between two approaches that are not mutually exclusive but are frequently treated as competing:

- Incentive-led beneficiation: Subsidised industrial energy tariffs, tax concessions for processing facilities, SEZ benefits, and concessional development finance attract investment without creating compliance obligations. The limitation is that incentives alone have not produced structural transformation across multiple previous policy cycles.

- Mandate-led beneficiation: Export taxes, export quotas, and permit conditionality create compliance pressure and potentially generate processing investment through regulatory necessity. The risk is investment deterrence, legal challenge, and processing without competitiveness if underlying structural costs are not addressed.

The 2026 strategy leans toward mandate-led intervention but without yet specifying the thresholds or timelines that would allow investors to assess compliance obligations. This ambiguity is itself an investment deterrent. A credible beneficiation policy framework, in addition, requires simultaneous progress across five dimensions:

- Regulatory clarity: Commodity-specific processing thresholds with transparent timelines and compliance pathways published in advance.

- Energy cost competitiveness: Dedicated industrial energy pricing mechanisms or on-site generation rights for qualifying processing facilities.

- Infrastructure co-investment: State or development finance institution support for logistics, water, and utility infrastructure serving processing zones.

- Financing instruments: Blended finance structures through institutions such as the Industrial Development Corporation to de-risk capital-intensive early-stage processing investment.

- Trade strategy alignment: Negotiated market access for processed South African mineral exports within major procurement frameworks in Europe, the United States, and Asia. A coherent metals supply chain strategy at this level is increasingly expected by international buyers.

Historical Performance: Why Previous Policy Cycles Fell Short

Understanding why the 2026 proposals represent a break from past approaches requires examining why earlier commitments did not deliver structural transformation. According to South Africa's beneficiation strategy documentation, the foundational policy intent has existed for well over a decade — yet execution gaps have consistently undermined outcomes.

| Policy Era | Primary Instrument | Outcome |

|---|---|---|

| Post-2002 (MPRDA era) | Beneficiation obligations in mining rights | Limited compliance; inconsistent enforcement |

| 2010-2018 (IPAP cycles) | Sector-specific industrial support programmes | Modest progress in selected sectors; no systemic shift |

| 2019-2024 | SEZ expansion and investment promotion | Incremental processing investment; structural gap persists |

| 2025-2026 | Critical Minerals Strategy and permit conditionality proposal | Implementation pending; outcomes uncertain |

The pattern across these cycles is consistent: policy instruments were deployed without sufficient enabling conditions. Beneficiation obligations existed in mining rights frameworks but enforcement was inconsistent. Industrial support programmes provided assistance but did not address the systemic cost competitiveness barriers that made processing economically unattractive relative to simple export.

Three Scenarios for South Africa's Beneficiation Trajectory

The outcome of the current policy moment is genuinely uncertain. Three plausible scenarios frame the range of possibilities:

Scenario 1: Coordinated Reform. Permit conditionality is implemented alongside credible energy cost relief for processing facilities, infrastructure co-investment in key processing corridors, and blended finance instruments through the IDC. Processing investment accelerates in chrome, manganese, and PGM downstream applications. South Africa begins recovering manufacturing share.

Scenario 2: Regulatory Stalemate. Conditionality is enacted without adequate enabling conditions. Mining investment slows in affected sectors. Processing facilities are not built at scale. The policy is partially reversed under industry pressure, perpetuating the structural gap.

Scenario 3: Incentive-Only Pivot. Industry pushback causes the government to abandon permit conditionality in favour of purely voluntary incentive mechanisms. Incremental processing investment occurs in SEZs, but the structural beneficiation gap narrows only marginally over the medium term.

The window matters. Global demand for critical minerals is widely projected to grow substantially through the 2030s, driven by electric vehicle adoption, grid-scale energy storage, and hydrogen economy development. Indonesia in nickel, Chile in lithium, and the DRC in cobalt are all simultaneously pursuing domestic processing agendas. South Africa's geological endowment is exceptional, however geological endowment alone does not determine who captures processing investment in a competitive global environment. As noted by the Minerals Council South Africa, coordinated policy design — not mandate alone — will ultimately determine success.

Disclaimer: Scenario projections and demand forecasts referenced in this article represent analytical frameworks and consensus estimates from cited sources. They do not constitute financial advice or guaranteed outcomes. Investors and policymakers should conduct independent due diligence before making decisions based on forward-looking mineral demand projections.

Frequently Asked Questions: South Africa Mineral Beneficiation Policy

What does South Africa's 2026 Industrial Development Strategy actually propose?

The strategy proposes linking preferential mining permit allocations to binding commitments on local processing of designated critical minerals. It also identifies deindustrialisation as a primary structural challenge and proposes coordination between the Department of Trade, Industry and Competition and the Department of Mineral and Petroleum Resources to accelerate domestic processing investment.

Why did South Africa lose its position as Africa's largest manufacturer?

The African Development Bank's Africa Industrialisation Index 2025 documented a steady decline in South Africa's industrial competitiveness, linking it to shrinking manufacturing output relative to GDP and continued dependence on raw-commodity exports. Morocco's displacement of South Africa in 2025 reflected this prolonged structural deterioration rather than a sudden reversal.

What is the Minerals Council's position on mandatory beneficiation?

The Minerals Council South Africa, representing members accounting for approximately 90% of annual mining production value, argues that mining and mineral processing are structurally distinct industries. Its position, stated in a June 9, 2026 note, is that policymakers should introduce measures that actively incentivise processing investment rather than attaching processing obligations directly to mining permits.

What is the status of beneficiation legislation in South Africa?

As of June 2026, the 2026 Industrial Development Strategy is a policy proposal and not enacted legislation. The draft Mineral Resources Development Bill, released for consultation in 2025, provides a potential legislative vehicle for formalising requirements, but specific processing thresholds for critical mineral projects have not been gazetted.

Why is electricity cost a barrier to South African mineral processing?

Energy-intensive smelting and refining operations require large volumes of reliably priced electricity. South Africa's industrial electricity costs have risen substantially due to Eskom's structural challenges and successive tariff adjustments, consequently making domestic processing less competitive relative to equivalent operations in lower-cost energy jurisdictions.

Want To Know Which ASX Mineral Discoveries Could Benefit From The Global Critical Minerals Processing Race?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into clear, actionable investment insights across more than 30 commodities. Explore why historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.