June 5, 2026

Why the South32 Hermosa project update matters in a tougher mining cycle

Large underground mine builds rarely move in a straight line. Costs can rise before value becomes visible, schedules can stretch even as asset quality improves, and reserve growth can change a project far more than a single headline figure suggests.

That is the right lens for reading the latest South32 Hermosa project update. This was not simply a bigger resource story. It was an operational reset that made the Taylor development look larger, longer-lived, and potentially more productive, while also making the capital burden and execution task more obvious.

For investors, industry watchers, and mining professionals, the key question is not whether the update was good or bad in isolation. It is whether the added mine life, throughput flexibility, and district-scale optionality are enough to justify the higher spend and later ramp-up timetable.

The central trade-off is clear: Hermosa now appears more substantial as an asset, but also more demanding as a build.

What does the latest South32 Hermosa project update actually change?

The short answer

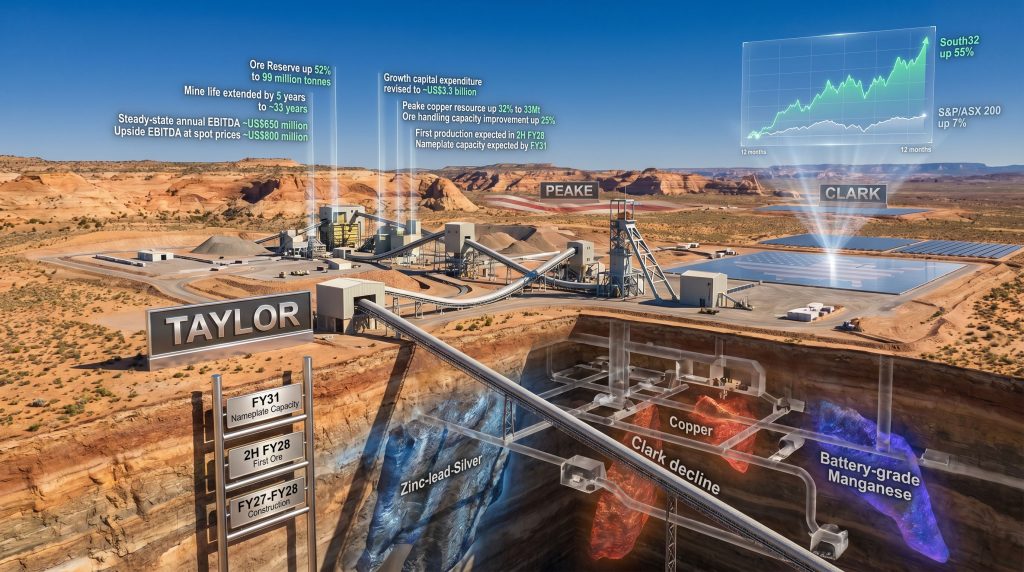

The latest update lifted the Taylor Ore Reserve by 52% to 99 million tonnes, extended initial operating life by 5 years to about 33 years, raised growth capital to around US$3.3 billion, and pushed first production to 2H FY28, with nameplate capacity targeted by FY31.

Why this is more than a reserve headline

A reserve increase matters because reserves are not the same as broad mineral inventory. In mining, a resource describes mineralisation with varying confidence levels, while an ore reserve is the economically mineable portion supported by tighter drilling, engineering work, and mine planning.

That distinction matters for valuation. A larger reserve can improve several things. For instance, it can strengthen production visibility, development confidence, and infrastructure use over a longer period. In addition, investors often assign greater weight to reserve-backed plans than early-stage resource estimates.

For readers wanting more context on how engineering studies support mine planning, a definitive feasibility study is often the bridge between concept and executable development.

The update therefore changed Hermosa’s expected operating envelope, not just its headline scale.

Before-and-after snapshot

| Metric | Previous view | Updated view | Why it matters |

|---|---|---|---|

| Taylor Ore Reserve | Lower base | 99Mt | Bigger mineable inventory |

| Reserve change | Baseline | +52% | Strong reserve conversion outcome |

| Operating life | About 28 years | About 33 years | Longer infrastructure payback window |

| Growth capex | Lower prior estimate | ~US$3.3bn | Higher upfront funding need |

| First production | Earlier expectation | 2H FY28 | Later initial cash generation |

| Nameplate capacity | Earlier than current plan | FY31 | Longer ramp-up period |

| Ore handling capacity | Baseline | +25% | Potentially smoother operating throughput |

| Steady-state EBITDA | Baseline | ~US$650m | Strong operating earnings potential |

| EBITDA at spot prices | N/A | ~US$800m | Commodity upside, but cyclical |

How Hermosa is structured as a multi-deposit platform

One reason the update drew attention is that Hermosa is not just one orebody. It is better understood as a district with multiple development pathways. South32’s own Hermosa project overview also reflects that broader platform logic.

Taylor as the base-case development engine

Taylor is the first planned production centre and remains the anchor asset. It is a zinc-lead-silver deposit, and management has framed it as a long-life, comparatively low-cost operation once fully established.

Polymetallic deposits can be attractive because they spread revenue across more than one metal stream. However, they also add processing and marketing complexity.

Peake as the copper growth option

The Peake copper resource estimate increased 32% to 33Mt, adding another layer to the broader district story. That matters because copper exposure can extend the usefulness of regional infrastructure beyond Taylor’s initial mine plan.

If Peake is progressively integrated into long-range planning, Hermosa starts to look less like a single-mine build and more like a staged mining district with shared infrastructure logic.

Clark as the manganese leg

Clark is the battery-grade manganese component. South32 has said the Clark deposit has received US government support, and federal permitting across Hermosa components is progressing. Recent reporting on federal permitting advances suggests the project is moving closer to key approvals.

It is also important not to overstate policy relevance. Hermosa may align with broader critical minerals demand trends in the United States, but policy alignment is not the same as project-specific operational support across the entire development.

What drove the bigger reserve and longer mine life?

Infill drilling in plain English

South32 attributed the Taylor reserve growth to infill drilling. In simple terms, infill drilling means placing drill holes closer together inside a known deposit to reduce uncertainty around thickness, continuity, and grade distribution.

That process can move tonnes from a less certain category into a reserve-supported mine schedule. Furthermore, it can improve the credibility of engineering and cost assumptions.

A helpful way to think about it is this:

- Exploration drilling finds the system.

- Resource drilling defines its size and geometry.

- Infill drilling improves confidence enough for mine design and reserve conversion.

This is why reserve growth is often more meaningful than a broad exploration headline. For anyone assessing how geologists turn assay tables into mine plans, understanding drill results is essential.

Why 52% reserve growth matters operationally

A 52% reserve increase can influence a project in several ways:

- support longer production scheduling

- justify larger or more durable infrastructure investment

- improve fixed-cost absorption across a longer life

- create optionality in underground sequencing

- increase the chance that early capital can be amortised over more saleable tonnes

Open for growth does not mean guaranteed growth

Taylor is still described as open for further growth. That is a positive geological signal, but it should be read carefully. Open means there is room for additional drilling success, not certainty that future drilling will become reserve-grade or economically recoverable material.

Reserve growth is most valuable when it boosts geological confidence, recoverable tonnes, and mine-planning clarity rather than simply expanding the exploration footprint.

Why capex increased to about US$3.3 billion

Higher capital spending was one of the most important parts of the latest South32 Hermosa project update. South32 said the increase reflected scope changes, inflation, and contractor challenges.

The three main drivers

| Driver | What it means in practice | Why it matters |

|---|---|---|

| Scope changes | More developed engineering definition or altered build requirements | Can improve long-term asset quality but lifts upfront cost |

| Inflation | Higher costs for labour, steel, equipment, energy, and construction inputs | Reduces project returns if not offset elsewhere |

| Contractor constraints | Limited specialist availability and productivity pressure | Can hit both budget and schedule |

When higher capex is a red flag and when it is not

Higher capex is a warning sign if the project becomes less economic without a corresponding rise in asset quality or earnings capacity. But capex growth can be more acceptable if it accompanies:

- materially larger reserves

- longer mine life

- improved throughput design

- stronger operating margins at steady state

That appears to be the debate around Hermosa. The project has become more expensive, but it has also become larger and longer-lived. In addition, long-life projects often hinge on economic thresholds such as cut-off grade, which can materially shape reserve estimates and cash flow profiles.

How the project economics look after the FY26 update

South32 outlined steady-state annual EBITDA of around US$650 million, with potential for about US$800 million at spot prices.

What steady-state EBITDA actually means

Steady-state EBITDA is an operating earnings measure once a mine is running at intended levels. It is useful, but it is not the same as distributable cash or free cash flow.

It does not fully tell readers:

- how much debt may be needed

- sustaining capital requirements over time

- tax impacts

- working capital swings

- closure liabilities

- ramp-up shortfalls during early production years

Why long-life, low-cost language matters

Management has described Taylor as long-life and low-cost. In mining analysis, that combination matters because large upfront capital can be more digestible when spread across decades of production and healthier operating margins.

Still, investors should be cautious. Commodity projects are cyclical, and valuation outcomes can change materially if zinc, lead, silver, or future copper prices weaken for extended periods.

Forecast economics are scenario-based, not guarantees. All project-level EBITDA assumptions depend on commodity prices, recoveries, ramp-up success, and actual capital discipline.

What the revised timeline means for execution risk

The timeline now points to key infrastructure completion between FY27 and FY28, first production in 2H FY28, and nameplate capacity by FY31.

Why first ore before shaft commissioning matters

South32 said first ore is expected via the Clark decline before shaft commissioning, alongside a 25% increase in ore handling capacity. Operationally, that can matter because alternative early access may reduce bottlenecks in underground development if executed properly.

In underground mines, shafts are critical but complex. Delays in sinking, equipping, ventilation integration, or materials handling can have cascading effects. A decline-based path to early ore can create useful flexibility, although it does not eliminate commissioning risk.

A practical milestone ladder looks like this:

- Complete major infrastructure across FY27 to FY28.

- Deliver first ore through the decline system.

- Commission shafts and associated systems.

- Ramp processing and underground mining rates.

- Reach nameplate capacity in FY31.

The biggest technical and execution risks at Hermosa

Even after the encouraging reserve update, major risks remain.

Core execution risks to watch

- Underground development complexity including shaft delivery, ventilation planning, geotechnical control, and access sequencing

- Contractor availability because specialist underground teams are hard to secure

- Input-cost inflation across steel, power, heavy equipment, and construction services

- Commissioning risk because reserve quality does not guarantee clean plant ramp-up

- Commodity-price sensitivity since project returns can shift with zinc, lead, silver, and copper prices

A wider industry backdrop also matters. Across the sector, mining consolidation and portfolio reshaping are increasingly influenced by capital intensity and execution risk.

How Hermosa fits into the US critical minerals supply chain

Hermosa has broader relevance because it combines exposure to zinc, lead, silver, copper, and manganese in a US jurisdiction. That makes it noteworthy within conversations about domestic and allied-source critical minerals supply.

Still, nuance matters. Project relevance to supply-chain resilience does not mean guaranteed economics, and permitting progress is best read as a step toward timeline visibility rather than proof that every development hurdle has been removed.

For Clark specifically, the disclosed US government support is relevant to the manganese component and may influence stakeholder confidence. It should not be generalised into blanket support across all Hermosa streams unless directly stated in company disclosures.

How to weigh the positives and negatives in the update

The bullish case

- Taylor Ore Reserve up 52% to 99Mt

- Initial operating life extended to about 33 years

- Steady-state EBITDA of about US$650m

- Potential EBITDA of about US$800m at spot prices

- Ore handling capacity improved by 25%

- Multi-deposit optionality across Taylor, Peake, and Clark

The cautious case

- Growth capex lifted to about US$3.3bn

- First production pushed to 2H FY28

- Nameplate capacity not expected until FY31

- Contractor constraints remain a live issue

- Inflation and procurement pressures can still evolve

- Commodity prices remain outside management control

What to watch in the next update

The next phase of the South32 Hermosa project update story will likely be less about headline reserve growth and more about delivery evidence.

Key checkpoints include:

- further drilling outcomes at Taylor and whether they improve mine-plan flexibility

- progress on shafts, underground access, and processing plant construction

- contractor performance and procurement discipline

- how Peake copper is integrated into longer-term district development plans

- any new milestones for Clark manganese and federal permitting progress

Over the last 12 months, South32 shares rose 55%, compared with a 7% gain in the S&P/ASX 200 over the same period, according to the cited market summary. Consequently, strong prior performance can raise expectations for flawless execution.

Final assessment: scale improved, but execution now matters more

The latest South32 Hermosa project update looks best understood as a trade-off rather than a one-directional win. The project now appears bigger, longer-lived, and more strategically interesting, particularly because Taylor, Peake, and Clark together create district-scale optionality.

At the same time, the update also made the cost and execution burden harder to ignore. A US$3.3 billion capital bill, a later path to full output, and explicit references to contractor challenges mean the investment case now depends increasingly on construction quality and ramp-up discipline.

Hermosa appears stronger in geological and district-development terms after the FY26 update, but the next stage of value creation will depend far more on delivery than on resource headlines.

Ready to Spot The Next Major Discovery?

Investors following large-scale project updates can stay ahead of the market with real-time ASX mineral discovery alerts powered by Discovery Alert’s proprietary Discovery IQ model. See how major discoveries have delivered exceptional returns by exploring Discovery Alert’s discoveries page and start a 14-day free trial today.