June 12, 2026

Why Space Technology Demands Have Transformed Critical Minerals Markets

The convergence of technological advancement and geopolitical competition has fundamentally altered how nations approach critical minerals procurement. The new space race for critical metals represents a paradigm shift where aerospace applications command substantial premiums over traditional industrial uses. Modern spacecraft systems represent the pinnacle of materials engineering, requiring specialized compounds that operate reliably across temperature extremes from -150°C to +120°C while withstanding high-energy particle bombardment and vacuum conditions.

The Material Intensity Revolution in Aerospace Engineering

Contemporary space missions demand unprecedented material sophistication that extends far beyond conventional manufacturing requirements. The Orion spacecraft exemplifies this complexity through its integration of aluminum-lithium alloys like 2090-T81 and 2195-T8, which provide 10% density reduction compared to traditional aluminum-copper variants while maintaining superior fracture toughness at cryogenic temperatures. These specifications create procurement challenges that ripple throughout global supply chains.

Titanium Grade 5 (Ti-6Al-4V) remains the aerospace industry standard due to its exceptional strength-to-weight ratio, approximately four times superior to steel, combined with operating temperature capabilities reaching 300°C sustained and 600°C for short-term applications. The material's corrosion resistance in aerospace environments makes it irreplaceable for structural components, yet global processing capacity operates near maximum utilization with lead times extending 18-24 months for space-qualified materials.

Nickel-based superalloys present another critical bottleneck. Components like Inconel 718 and Rene alloys enable rocket engines to function at temperatures between 650-950°C while maintaining structural integrity. These materials form the backbone of propulsion systems from NASA's RS-25 engines to SpaceX's Raptor engine turbopumps, yet their production requires specialized knowledge concentrated in limited geographic regions.

Quantifying the Space Sector's Materials Footprint

Key Performance Requirements for Space-Grade Materials:

- Vacuum Environment Exposure: Materials must maintain structural integrity without atmospheric oxidation protection

- Thermal Cycling Resistance: Components experience extreme temperature variations during mission profiles

- Radiation Hardness: High-energy particle bombardment requires materials with specific nuclear properties

- Defect Tolerance: Space-grade titanium must meet ASTM B265 standards with minimal defect density per production batch

The distinction between space-grade and industrial-grade materials extends beyond performance specifications to encompass entire supply chain methodologies. Achieving aerospace supplier qualification typically requires 3-5 years of testing and certification, creating significant barriers to entry while establishing supply chain stability once qualification is complete.

When big ASX news breaks, our subscribers know first

How Geopolitical Competition Is Reshaping Critical Minerals Supply Chains

Strategic competition has transformed critical minerals from commodity inputs into instruments of national power. The concentration of processing capabilities in single regions creates systemic vulnerabilities that extend far beyond traditional supply and demand dynamics, particularly affecting the new space race for critical metals.

The Strategic Concentration Problem

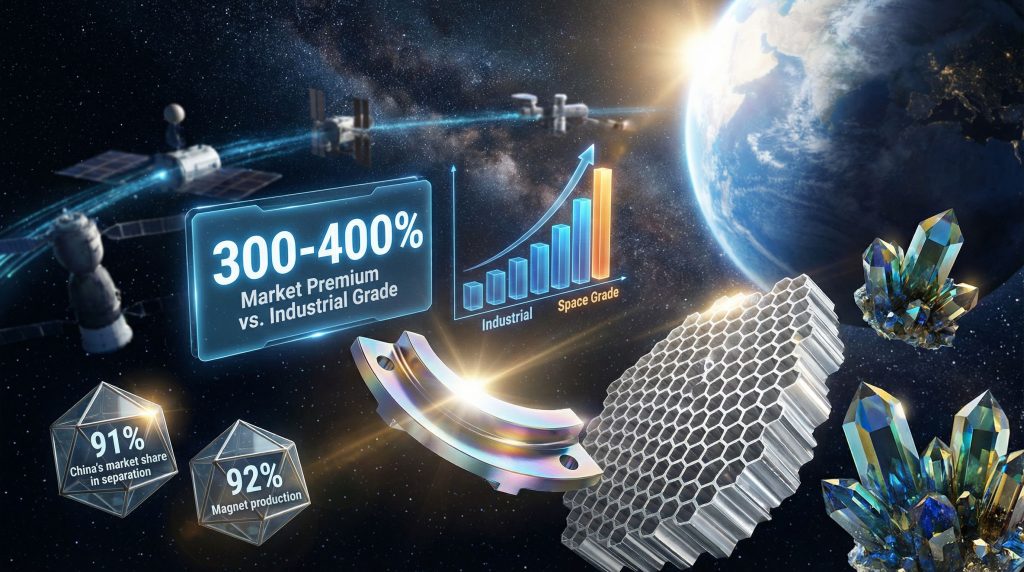

Current supply chain architecture reveals dangerous dependencies across multiple processing stages. According to rare earth reserves analysis, China accounts for approximately 60-70% of global rare earth mining production, but more critically, controls roughly 85-92% of rare earth separation and processing capacity. This dominance extends to permanent magnet production, where China produces 80% of high-performance NdFeB magnets essential for precision guidance systems and advanced propulsion.

Critical Bottlenecks in Rare Earth Supply Chain:

| Processing Stage | Global Capacity Leader | Market Share |

|---|---|---|

| Mining | China | 60-70% |

| Separation | China | 85-92% |

| Magnet Production | China | 80%+ |

| Recycling | Japan/EU | 10-15% |

The separation process itself represents a technological chokepoint. Current commercial separation involves energy-intensive solvent extraction methods requiring specialized expertise developed over decades. Establishing new separation capacity requires minimum 3-5 years for commercial scale operations, with separation efficiency ranging from 85-95% depending on required purity levels.

Export Control Escalation and Market Fragmentation

Recent policy developments demonstrate how rapidly mineral access can become weaponised in geopolitical competition. Export controls targeting gallium, germanium, and certain rare earth elements directly impact space-grade component manufacturing. These restrictions force aerospace manufacturers to develop alternative supply routes whilst maintaining stringent quality requirements.

The dual-use nature of critical minerals amplifies these vulnerabilities. Materials essential for spacecraft propulsion systems, such as tantalum capacitors and cobalt superalloys, serve identical functions in defence applications. This convergence means supply disruptions impact both civilian space exploration and national security infrastructure simultaneously.

Geographic risk extends beyond China's market position to encompass processing knowledge concentration. Separation technology represents proprietary intellectual property with limited alternative processing routes available globally. This knowledge concentration creates barriers competitors cannot easily overcome through capital investment alone.

What Government Stockpiling Initiatives Reveal About Future Demand

Strategic stockpiling programmes across major economies signal a fundamental shift in how governments view critical minerals. These materials are increasingly treated as essential national infrastructure, comparable to strategic petroleum reserves in terms of economic security importance.

Strategic Reserve Building Across Major Economies

Government stockpiling initiatives demonstrate that critical minerals are now viewed as essential national infrastructure. The Australia strategic reserve represents one of several international efforts to secure material access for strategic applications.

The United States National Defense Stockpile maintains strategic reserves of titanium sponge, cobalt, and chromium, with approximately $500 million in cobalt acquisitions announced between 2022-2024. European Union initiatives under the Critical Raw Materials Act allocate €1.2 billion for strategic autonomy in cobalt, lithium, nickel, and rare earths through 2030. Japan's strategic resource stockpiling through JOGMEC represents an estimated ¥500 billion investment in rare earth, lithium, and cobalt reserves.

These investments reflect recognition that material access determines technological capabilities across defence, aerospace, and emerging technology sectors. The convergence of demand signals from space exploration, electric vehicle production, renewable energy infrastructure, and defence modernisation creates competition for identical materials across multiple strategic industries.

The Defence-Space Materials Nexus

Pentagon supply chain reviews explicitly identify titanium, cobalt, antimony, tantalum, and scandium as dual-use materials where aerospace and defence applications converge on identical specifications. This overlap means supply disruptions affect both civilian space missions and military readiness simultaneously, amplifying the strategic importance of secure supply chains.

Scandium applications exemplify this convergence. Aluminium-scandium alloys provide weight reduction and strength enhancement for both military aircraft and spacecraft structures. With global scandium production limited to approximately 15-20 tonnes annually, mostly from processing byproducts, supply security becomes critical for maintaining aerospace capabilities.

Which Materials Face the Most Severe Supply-Demand Imbalances

Material-specific bottlenecks reveal where the new space race for critical metals creates the most acute pressure points in global supply chains.

Titanium Processing Bottlenecks

Despite abundant titanium ore reserves globally, aerospace-grade processing capacity represents the primary constraint. Current facilities operate near maximum capacity, creating 18-24 month lead times for space-qualified materials. The titanium sponge production process requires specialised vacuum arc remelting (VAR) capabilities concentrated in limited geographic regions.

Processing yield issues compound these constraints. Converting titanium ore to aerospace-grade material involves multiple energy-intensive steps with yields typically ranging from 85-95% depending on final specifications. The specialised knowledge required for achieving space-grade quality creates additional barriers to capacity expansion.

Rare Earth Processing Dependencies

Rare earth element supply chains face multiple simultaneous constraints across processing stages. Whilst global reserves exceed 120 million metric tonnes, processing capacity remains concentrated. China's integrated approach from mining through magnet production creates economies of scale competitors struggle to match.

Current Global Rare Earth Processing Capacity:

- Annual Global Production: Approximately 300,000 metric tonnes of rare earth oxides

- Processing Concentration: 90%+ of separation capacity in single region

- Lead Time for New Capacity: 5-7 years minimum for commercial scale

- Recycling Rates: Currently 1-5% globally, with Japan and EU achieving 10-15%

The technical complexity of rare earth separation creates additional vulnerabilities. Each element requires specific extraction parameters, and achieving space-grade purity levels often necessitates multiple processing cycles.

How Private Sector Investment Is Responding to Supply Chain Risks

Corporate strategies increasingly prioritise supply security over cost optimisation as material access concerns intensify across the aerospace sector. This shift reflects broader trends in the mining industry evolution towards strategic materials.

Accelerated Development Programmes

Private sector responses demonstrate urgent timeline compression across critical mineral projects. Development programmes previously scheduled for 2030+ completion are receiving acceleration funding targeting 2028-2029 production timelines. This acceleration reflects industry recognition that supply security imperatives override traditional project economics.

SpaceX's decision to use stainless steel 304L for Starship represents one alternative material strategy, deliberately choosing abundant materials over traditional aluminium-lithium approaches. However, this substitution approach has limitations for applications requiring maximum performance optimisation.

Vertical Integration Strategies

Aerospace manufacturers increasingly pursue backward integration into materials processing rather than relying on merchant market availability. Boeing and Lockheed Martin have announced strategic partnerships targeting titanium and aluminium processing capabilities, seeking greater control over supply chain reliability.

This vertical integration extends beyond procurement to encompass recycling operations. Aerospace component recycling achieves over 95% efficiency for titanium applications, potentially supplying 15-20% of industry demand by 2030 if scaled appropriately.

What Alternative Sourcing Strategies Are Emerging

Resource security concerns drive innovation across multiple alternative sourcing approaches as traditional supply chains prove inadequate for strategic requirements. Furthermore, emerging technologies like asteroid mining advances offer potential long-term solutions.

Recycling and Urban Mining Potential

Electronic Waste Recovery Opportunities:

- Electronic waste contains 40-50 times higher rare earth concentrations than primary ores

- Current global recycling rates remain below 5% for most rare earth elements

- Technical challenges include separation complexity and collection infrastructure

- Japan leads recycling technology development with 15% current recovery rates

Urban mining represents substantial untapped potential, particularly for rare earth elements concentrated in electronic devices. However, scaling recycling operations requires overcoming technical challenges in separation and collection infrastructure development.

Titanium recycling demonstrates successful implementation potential. Current aerospace recycling achieves 95%+ efficiency, with recycled titanium meeting identical specifications to primary material. Expanding this model across other critical materials could significantly reduce primary material dependencies.

Substitution Technology Development

Research into alternative materials focuses on reducing dependency on the most constrained elements whilst maintaining performance specifications. Advanced ceramics development targets replacement of traditional metal alloys in specific applications, though performance trade-offs remain significant.

Emerging Substitution Technologies:

- Advanced ceramic composites for high-temperature applications

- Additive manufacturing enabling optimised material usage

- Nanotechnology approaches reducing required material volumes

- Synthetic alternatives to specific rare earth functions

Additive manufacturing presents particular promise for aerospace applications, enabling complex geometries that reduce material waste whilst maintaining structural performance. Current adoption rates suggest 20-30% material savings achievable through optimised design approaches.

The next major ASX story will hit our subscribers first

Where New Production Capacity Is Being Developed

Geographic diversification efforts target reducing concentration risks whilst building processing capabilities in strategically favourable regions. The critical minerals strategy involves establishing alternative production centres globally.

Geographic Diversification Efforts

Emerging Production Regions and Timelines:

| Region | Primary Materials | Timeline to Production | Current Status |

|---|---|---|---|

| Greenland | Heavy Rare Earths | 2028-2029 | Permitting ongoing |

| Australia | Lithium, Titanium | 2026-2027 | Multiple projects advancing |

| North America | Processing Capacity | 2027-2028 | Investment committed |

| Europe | Recycling Infrastructure | 2025-2026 | Construction phase |

Australia's position in lithium production through projects like Pilgangoora and Greenbushes provides alternative sourcing for space applications requiring lithium-ion battery systems. Mount Weld operations through Lynas Rare Earths represent one of the few non-Chinese rare earth production sources, though processing still requires geographic diversification.

Greenland's potential heavy rare earth production could address specific supply constraints for high-performance applications. However, permitting timelines remain uncertain, with production unlikely before 2028 given current regulatory processes.

Processing Capability Expansion

New facility development prioritises achieving space-grade specifications rather than maximising volume production. This approach reflects the premium nature of aerospace applications where quality requirements exceed volume considerations.

Processing technology transfer represents a critical component of capacity expansion efforts. Establishing new separation capabilities requires not just capital investment but access to proprietary processing knowledge currently concentrated in limited regions.

How Market Dynamics Differ for Space-Grade vs. Industrial Materials

Aerospace applications create distinct market segments with fundamentally different pricing, supply, and demand characteristics compared to traditional industrial uses. This differentiation drives much of the new space race for critical metals.

Pricing Premium Analysis

Space applications command substantial premiums reflecting stringent quality requirements and limited supplier qualification pools. These premiums create market dynamics independent of broader commodity cycles, where aerospace demand often remains stable despite industrial market volatility.

Quality certification requirements explain much of the pricing differential. Space-grade materials must meet specifications including vacuum compatibility, radiation resistance, and thermal cycling performance that exceed industrial applications. Testing and certification processes add substantial costs whilst limiting supplier participation.

Supply Chain Qualification Barriers

Achieving aerospace supplier qualification typically requires 3-5 years of testing and certification, creating significant barriers to entry whilst establishing supply chain stability once qualification is complete.

The qualification process creates market stability by limiting supplier changes, but also creates vulnerabilities when qualified suppliers face capacity constraints or geopolitical access restrictions. Aerospace manufacturers often maintain relationships with multiple qualified suppliers to mitigate these risks, though qualification costs limit the practical number of alternative sources.

Lead time dynamics differ significantly between aerospace and industrial applications. Industrial users often accept longer lead times in exchange for lower prices, whilst aerospace applications require schedule certainty that commands premium pricing.

What Long-Term Scenarios Could Reshape This Competition

Technological developments and geopolitical shifts could fundamentally alter the competitive landscape for critical minerals in space applications.

Space Mining Technology Development

The race to mine the moon could transform terrestrial supply dynamics by accessing material concentrations far exceeding Earth-based deposits. Near-Earth asteroids contain platinum group metals and rare earth elements at concentrations 10-100 times higher than terrestrial ores.

However, commercial viability remains 10-15 years away for most scenarios. Current technology demonstrations focus on resource identification and extraction methodology rather than full-scale commercial operations. Initial applications will likely target highest-value materials where transportation costs can be justified.

Space-based manufacturing presents an alternative approach, using materials extracted in space for space-based construction projects. This scenario could reduce Earth-to-orbit transportation requirements whilst creating new demand patterns for space-accessible materials.

Technology Substitution Pathways

Potential Technology Substitutions:

- Advanced ceramics replacing traditional metal alloys in high-temperature applications

- Additive manufacturing reducing material waste through optimised design

- Nanotechnology enabling enhanced performance with reduced material volumes

- Synthetic alternatives replacing specific rare earth element functions through engineered solutions

Ceramic matrix composites show promise for replacing metal alloys in specific high-temperature applications, though thermal shock resistance remains challenging. Silicon carbide and ultra-high temperature ceramics could substitute for some superalloy applications whilst reducing reliance on critical metals.

Why This Competition Extends Beyond Traditional Mining

The new space race for critical metals encompasses technological capabilities, processing expertise, and intellectual property beyond simple material extraction.

The Processing and Refinement Advantage

Control over processing capabilities often determines market access more than raw material ownership. China's dominance in rare earth markets stems from processing capacity rather than exclusive ore access, demonstrating how downstream capabilities create strategic advantages.

Processing technology represents decades of accumulated expertise that cannot easily be replicated through capital investment alone. Establishing new separation facilities requires not only equipment but operational knowledge developed through years of experience optimising yields and quality.

Technology Transfer and Intellectual Property

Competition encompasses technical knowledge required for achieving space-grade specifications across multiple processing stages. This knowledge concentration creates additional strategic vulnerabilities beyond simple supply access.

Patent landscapes around critical mineral processing create additional barriers to establishing alternative supply sources. Key separation technologies remain protected by intellectual property frameworks that limit technology transfer options.

How Investment Strategies Are Adapting to Material Security Concerns

Investment approaches increasingly incorporate supply chain security considerations alongside traditional financial metrics as material access becomes a strategic priority.

Risk Assessment Evolution

Investment evaluation now includes geopolitical supply risk assessments that examine not just resource availability but processing capacity concentration and export control vulnerabilities. These assessments recognise that material access determines project viability regardless of underlying resource quality.

Key Investment Considerations:

- Geographic diversification of supply sources across multiple jurisdictions

- Processing capability development rather than simple resource extraction

- Technology qualification timelines and certification requirements

- Strategic partnership opportunities with aerospace end-users

Portfolio strategies increasingly favour projects offering supply chain diversification benefits over pure resource quality metrics. This shift reflects recognition that reliable access often outweighs cost optimisation in strategic applications.

Market Psychology Shifts

Investor sentiment has shifted toward viewing critical mineral projects as strategic infrastructure rather than traditional commodity investments. This perspective creates different valuation methodologies that incorporate security premiums alongside conventional resource assessments.

Long-term contracts with aerospace manufacturers provide investment security that traditional commodity sales cannot match. These partnerships offer stable revenue streams that justify higher development costs associated with achieving space-grade specifications.

The convergence of space exploration ambitions with material security concerns creates investment opportunities that extend far beyond traditional mining sector boundaries. As the new space race for critical metals intensifies, success will depend on securing reliable access to specialised materials rather than simply identifying resource deposits. This reality transforms critical minerals from commodity inputs into strategic assets that determine technological capabilities across multiple industries essential to national competitiveness.

Understanding these dynamics provides insight into how geopolitical competition, technological advancement, and resource security intersect to reshape global supply chains. The aerospace sector's material requirements illustrate broader trends affecting electric vehicle production, renewable energy infrastructure, and defence modernisation, where identical materials compete across strategic applications.

This analysis is based on publicly available information and industry reports. Investment decisions should consider multiple factors including market volatility, regulatory changes, and technological developments. Material supply chain dynamics can change rapidly due to geopolitical developments or technological breakthroughs.

Ready to capitalise on critical minerals opportunities in the space sector?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why major mineral discoveries can lead to substantial returns by exploring historic examples of exceptional outcomes, then begin your 14-day free trial today to position yourself ahead of the market.